The past five years for Nexa Resources (NYSE:NEXA) investors has not been profitable

For many, the main point of investing is to generate higher returns than the overall market. But in any portfolio, there will be mixed results between individual stocks. So we wouldn't blame long term Nexa Resources S.A. (NYSE:NEXA) shareholders for doubting their decision to hold, with the stock down 50% over a half decade.

It's worthwhile assessing if the company's economics have been moving in lockstep with these underwhelming shareholder returns, or if there is some disparity between the two. So let's do just that.

See our latest analysis for Nexa Resources

Nexa Resources wasn't profitable in the last twelve months, it is unlikely we'll see a strong correlation between its share price and its earnings per share (EPS). Arguably revenue is our next best option. Shareholders of unprofitable companies usually expect strong revenue growth. As you can imagine, fast revenue growth, when maintained, often leads to fast profit growth.

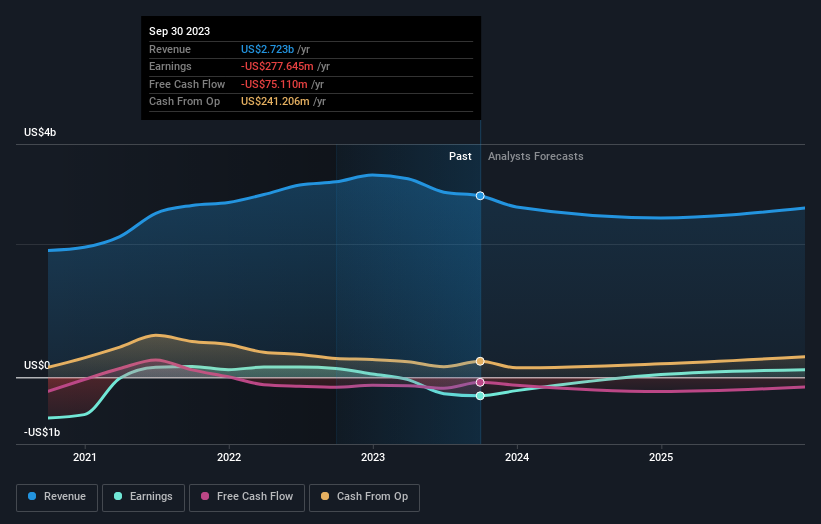

Over five years, Nexa Resources grew its revenue at 5.3% per year. That's not a very high growth rate considering it doesn't make profits. This lacklustre growth has no doubt fueled the loss of 8% per year, in that time. We'd want to see proof that future revenue growth is likely to be significantly stronger before getting too interested in Nexa Resources. When a stock falls hard like this, some investors like to add the company to a watchlist (in case the business recovers, longer term).

The company's revenue and earnings (over time) are depicted in the image below (click to see the exact numbers).

It's probably worth noting that the CEO is paid less than the median at similar sized companies. It's always worth keeping an eye on CEO pay, but a more important question is whether the company will grow earnings throughout the years. So we recommend checking out this free report showing consensus forecasts

What About Dividends?

When looking at investment returns, it is important to consider the difference between total shareholder return (TSR) and share price return. The TSR incorporates the value of any spin-offs or discounted capital raisings, along with any dividends, based on the assumption that the dividends are reinvested. It's fair to say that the TSR gives a more complete picture for stocks that pay a dividend. We note that for Nexa Resources the TSR over the last 5 years was -39%, which is better than the share price return mentioned above. And there's no prize for guessing that the dividend payments largely explain the divergence!