shulz

shulz

Looking for high yield exposure to infrastructure and utilities in 2024?

With interest rates expected to decline in the latter part of this year, those sectors could become more profitable, due to lower interest expenses.

The Cohen & Steers Infrastructure Fund (NYSE:UTF) is a closed-end fund, a CEF, which invests in infrastructure assets.

The Fund's objective is to achieve total return, with an emphasis on income. Under normal market conditions, the Fund will invest at least 80% of its managed assets in securities issued by infrastructure companies, which consist of utilities, pipelines, toll roads, airports, railroads, ports, telecommunications companies and other infrastructure companies. The fund benchmarks the performance of its portfolio against a composite index of 80% FTSE Global Core Infrastructure 50/50 Net Tax Index (FTSE 50/50) and 20% BofA Merrill Lynch Fixed-Rate Preferred Securities Index.

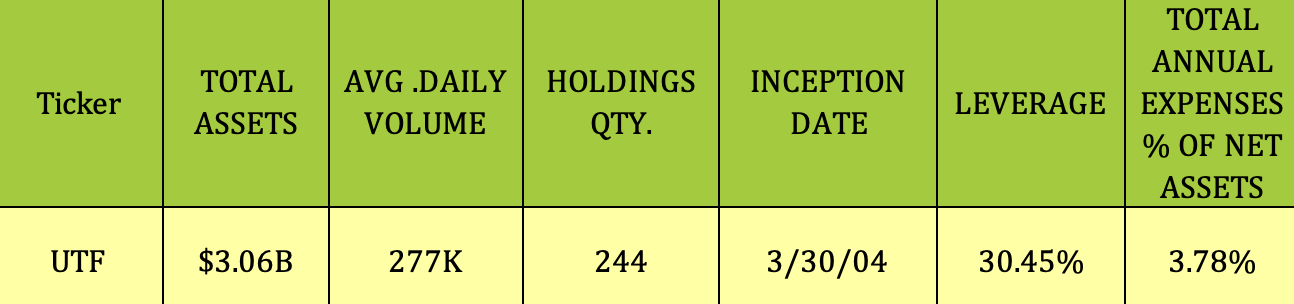

UTF is one of the largest Infrastructure CEF's, with a $2.14B market cap, and over $3B in assets, as of 12/31/23. It has 244 holdings, and daily average volume of 277K. Management uses leverage, which was at 30.45% as of 12/31/23. Annual expenses were 3.78% in 2023, including 2.58% in interest expense.

Hidden Dividend Stocks Plus

Holdings:

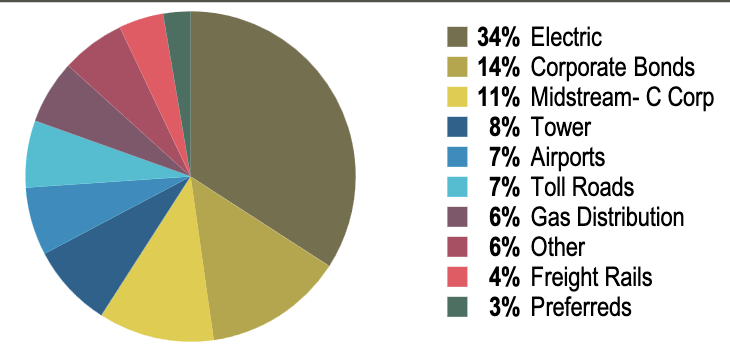

As of 12/31/23, Electric Utilities were UTF's biggest exposure, at 34%, followed 14% in Corporate Bonds, and 11% in Midstream Energy holdings. Its other sector holdings run from 4% in Freight Rails to 8% in Cell Towers, plus 3% in Preferreds.

UTF site

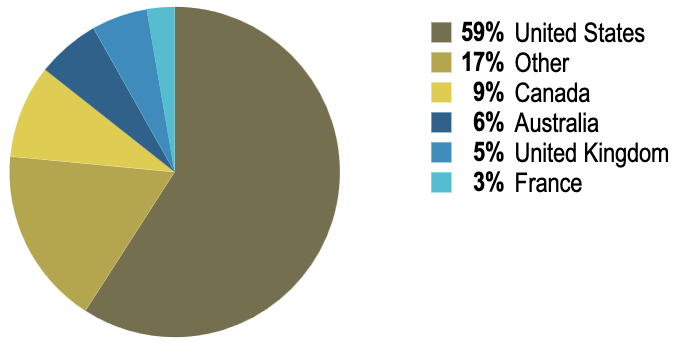

US holdings form 59% of its holdings, distantly followed by Canada, at 9%, Australia, at 6%, the UK, at 5%, and France, at 3%, with 17% in other countries:

UTF site

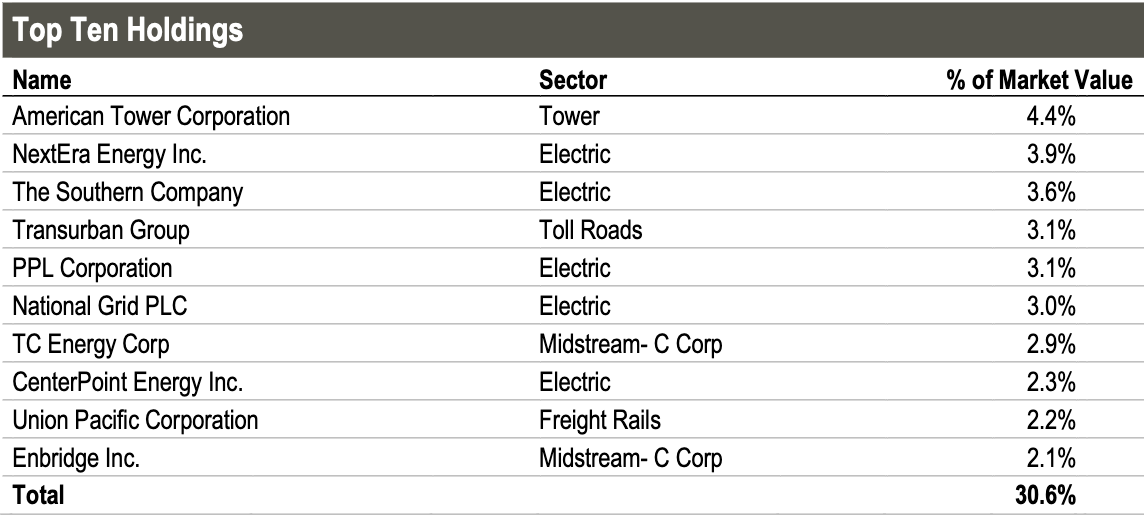

UTF's 3 biggest positions are American Tower (AMT), at 4.4%, NextEra Energy Partners (NEP), at 3.9%, and the Southern Company (SO), at 3.6%. The remainder of its top 10 holdings run from 2.1% in Enbridge to 3.1% in in Transurban Group. UTF's top 10 holdings formed 30.6% of its portfolio, as of 12/31/23.

UTF site

Dividends:

Management has maintained monthly $.155 distributions since Q1 2018.

At its 3/15/24 intraday price of $22.29, UTF's dividend yield was 8.43%. It pays monthly, and should go ex-dividend next on ~4/11/24, with a ~4/29/24 pay date.

Hidden Dividend Stocks Plus

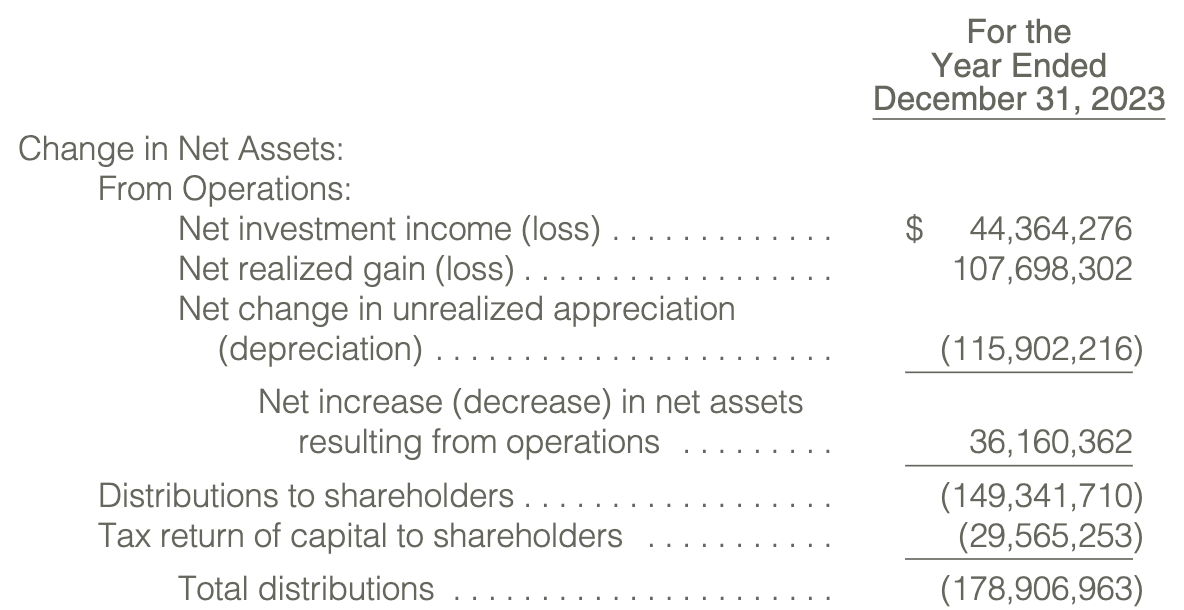

Taxes:

For the year ended 12/31/23, ~16.5% of UTF's distributions came from Return of Capital, ROC, which offers unit holders a tax deferral benefit. However, ROC lowers your tax basis, which will affect your taxable profit when and if you sell your UTF holdings.

UTF site

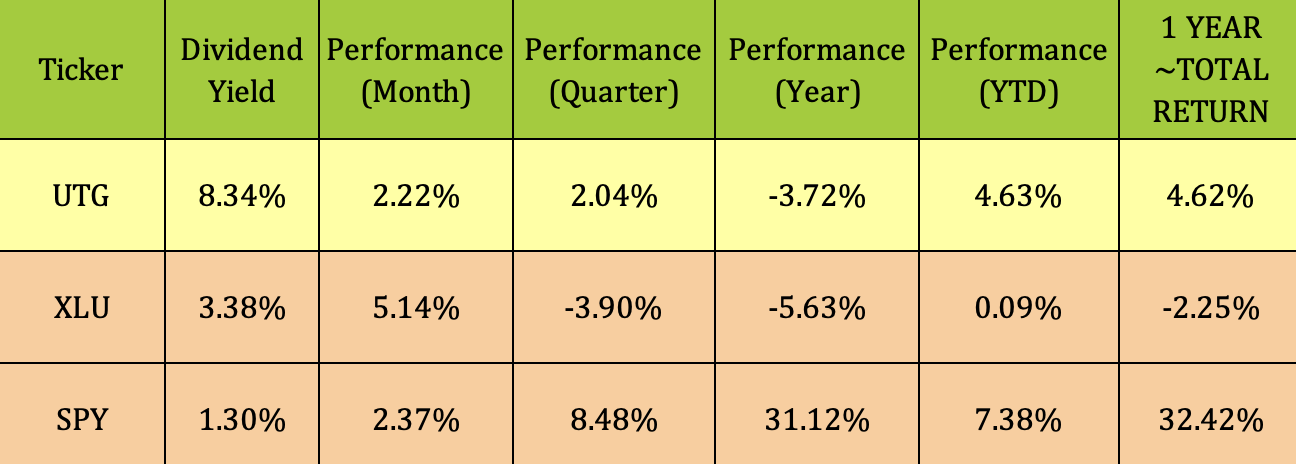

Performance:

While UTF has outperformed the broad Utilities sector over the past year and so far in 2024, it has trailed the S&P 500.

Hidden Dividend Stocks Plus

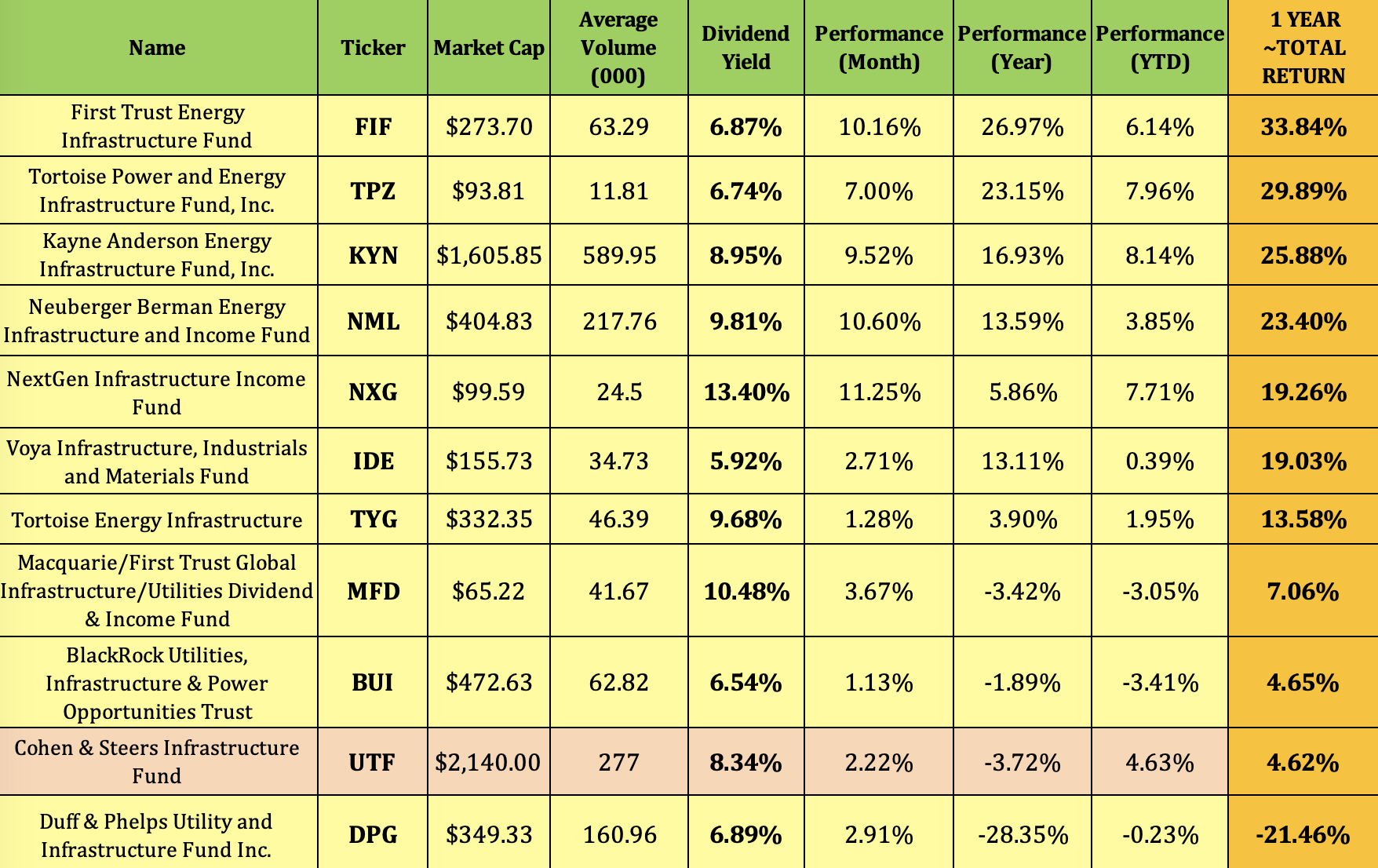

UTF's Infrastructure CEF peers include these funds:

First Trust Energy (FIF), Tortoise Power & Energy (TPZ), Kayne Anderson Energy Infrastructure Fund (KYN), Neuberger Berman Energy Infrastructure and Income Fund (NML), NextGen Infrastructure Income Fund (NXG), Voya Infrastructure, Industrials and Materials Fund (IDE), Tortoise Energy Infrastructure Fund (TYG), Macquarie/First Trust Global Infrastructure/Utilities Dividend & Income Fund (MFD), BlackRock Utilities, Infrastructure & Power Opportunities Trust (BUI), and Duff & Phelps Utility and Infrastructure Fund (DPG).

FIF has had the best total return over the past year, gaining ~27% in price, with a ~34% total return, followed by TPZ, at ~30%, KYN, at ~26%, and NML, at 23.4%.

The next tier, NXG, IDE, and TYG have returned 19.3%, 19%, and 13.6%, respectively.

UTF is in the 3rd tier down, with a 4.62% total return behind MFD, at 7%, and BUI, at 4.65%, leaving DPG in last place by a wide margin, at -21.46%:

Hidden Dividend Stocks Plus

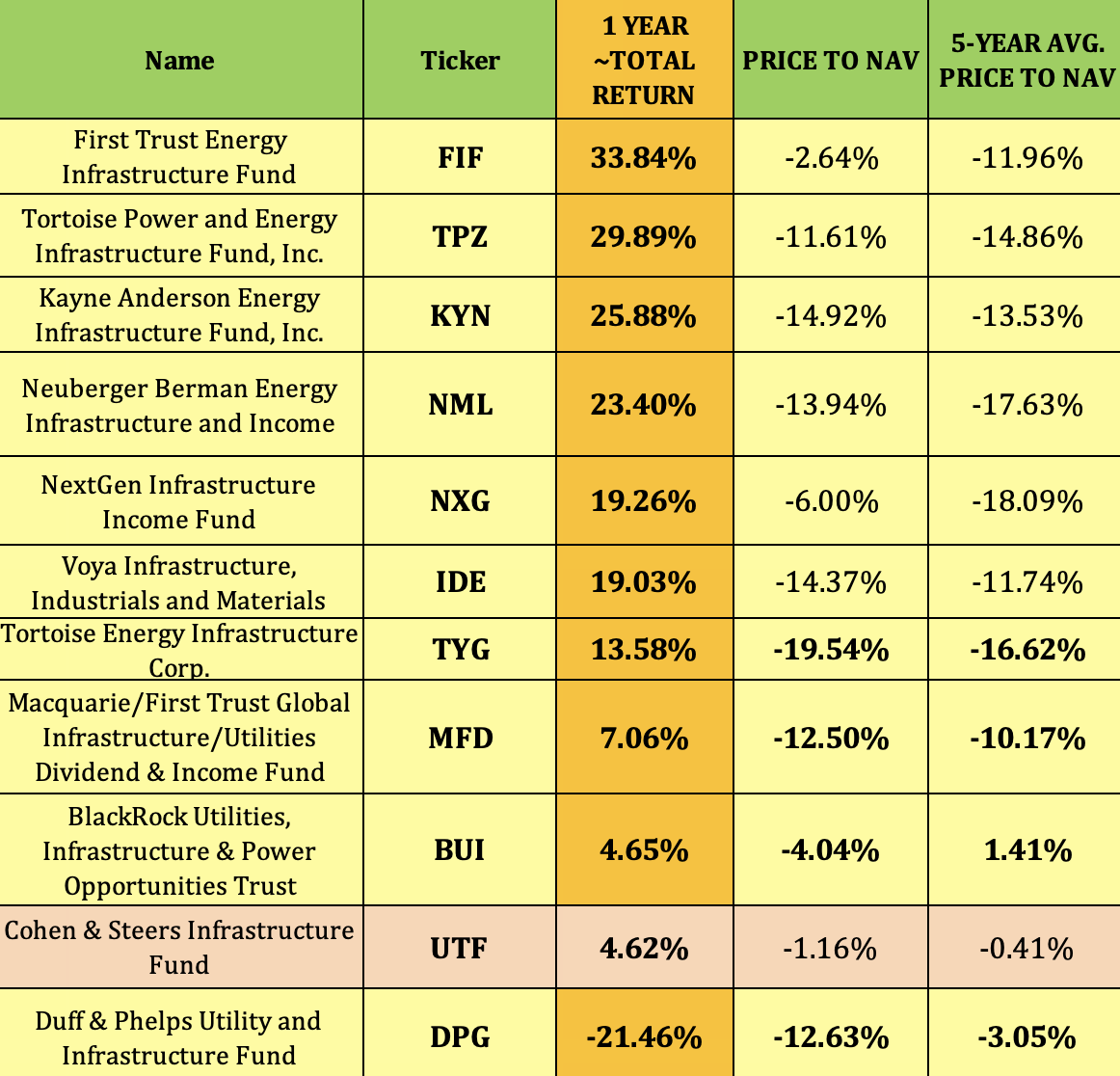

Valuations:

Since NAV/Share is calculated at the end of each trading day, you have to look at the most recent closing values to determine the current NAV discount or premium. Buying CEF's at a deeper discount than their historical average discounts/premiums can be a useful strategy, due to mean reversion.

As of the 3/13/24 close, UTF was selling at a 1.16% discount, not as deep as its 1-year 2.59% discount, but deeper than its 3-year 0.50% average premium, and its 5-year 0.41% discount.

Hidden Dividend Stocks Plus

Not surprisingly, the top performers in this group are mostly selling at shallower NAV discounts to their 5-year averages, with the exception of IDE, and KYN, which we covered in more depth in a recent article.

DPG, the worst 1-year performer, has the biggest spread, at 958 basis points, between its current discount, at 12.6%, vs. its 5-year average of 3%.

BUI has a ~545 basis point spread, while TYG has a 292 point spread. IDE, which returned 19% in the past year, has a 263 point spread, and MFD has a 233 point spread:

Hidden Dividend Stocks Plus

We rate UTF a hold - we'll wait for a bigger discount before buying new shares. UTF's biggest discount was 7.3% below NAV over the past year.

All tables furnished by Hidden Dividend Stocks Plus, unless otherwise noted.

Editor's Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.