da-kuk

da-kuk

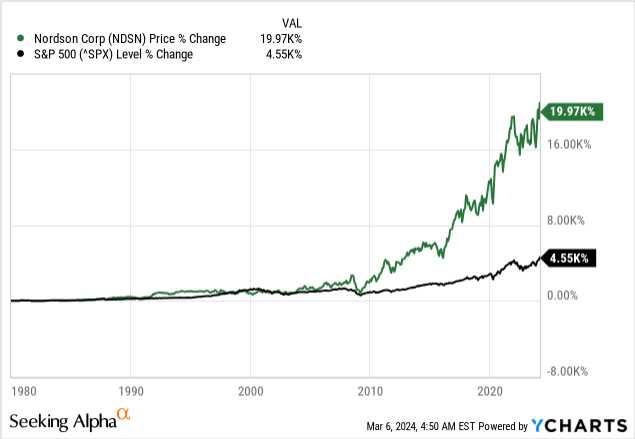

Over the last few years, Nordson Corporation (NASDAQ:NDSN) performed more or less in line with the S&P 500. Since my last article published in September 2023, the index as well as the stock returned about 13% and in the last five years, Nordson Corporation increased 91% while the S&P 500 increased 82%.

But over the long run, Nordson Corporation clearly outperformed the S&P 500 underlining that Nordson Corporation is a great business. About two weeks ago, Nordson Corporation reported first quarter results, and we take a closer look at the business in the following article.

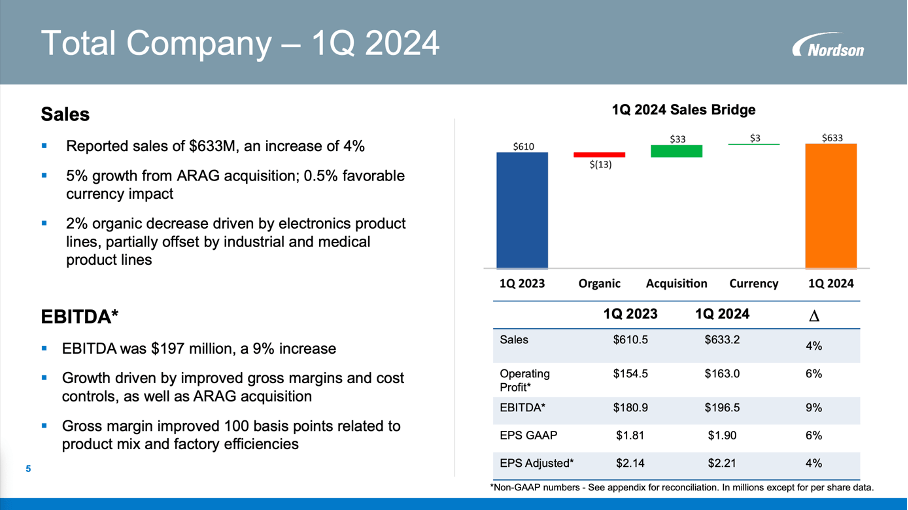

On February 21, 2024, Nordson Corporation reported first quarter results and the company could beat analysts’ expectations for earnings per share as well as revenue (although the revenue beat was only slightly). But not only were results better than estimated by Wall Street, Nordson also performed well compared to the same quarter last year.

Sales increased from $610.5 million in Q1/23 to $633.2 million in Q1/24 – resulting in 3.7% year-over-year growth. However, we must point out that growth was driven by a favorable 5% benefit from the ARAG acquisition and partially offset by an organic decline of 2%. And while the top line increased only in the low single digits, operating profit increased from $144.2 million in the same quarter last year to $159.4 million in Q1/24 – resulting in 10.5% year-over-year growth. And finally, diluted earnings per share increased 5.0% YoY from $1.81 in the same quarter last year to $1.90 this quarter.

Nordson Corporation Q1/24 Presentation

When can also look at adjusted earnings per share, which increased 3.3% YoY to $2.21. And finally, free cash flow was $165 million, which was a 150% cash conversion rate – the highest in a first quarter in the company’s history.

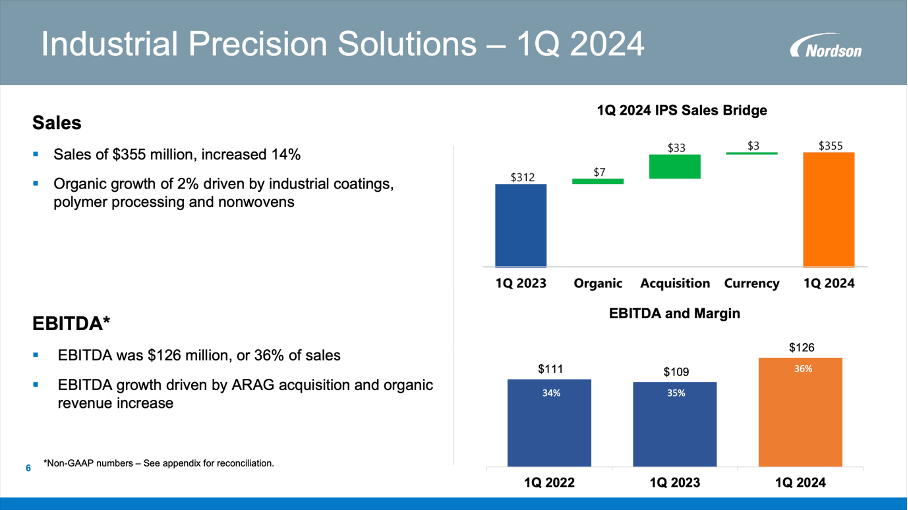

When looking at the three different segments, growth was driven by Industrial Precision Solutions. Revenue for the segment increased from $311.6 million in the same quarter last year to $354.5 million in Q1/24. And while organic growth for the segment was 2.3%, the biggest part stemmed from acquisitions (which contributed 10.6% growth). Operating profit for the segment also increased 6.0% YoY from $102.3 million to $108.4 million. Especially the ARAG integration, which is processing well, is contributing to sales and EBITDA growth.

Nordson Corporation Q1/24 Presentation

And while the Industrial Precision Solutions was performing well, the Medical and Fluid Solutions segment rather stagnated. Revenue could increase slightly from $154.3 million in the same quarter last year to $159.5 million this quarter. And while reported growth was 3.4%, organic growth was 3.1% YoY. At least, operating income for the segment increased 17.0% YoY to $46.1 million.

Nordson Corporation Q1/24 Presentation

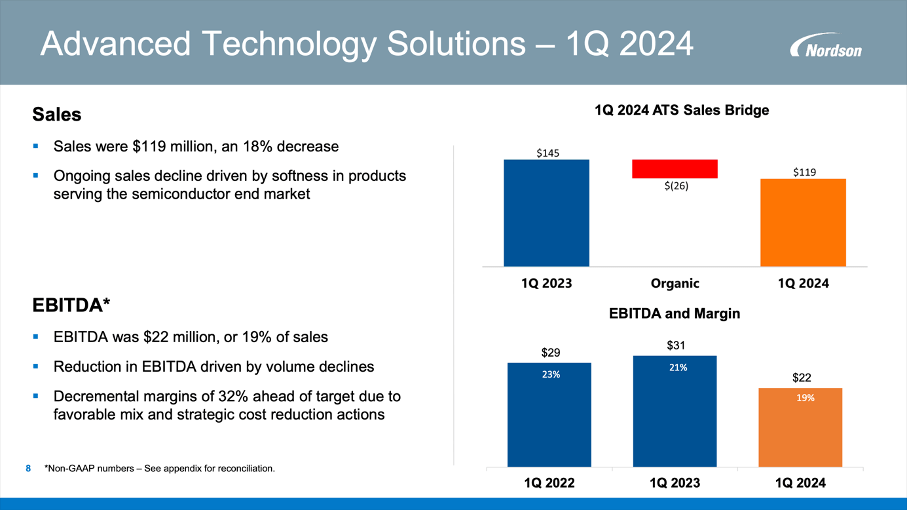

The worst performing segment was Advanced Technology Solution, which had to report a declining revenue. Compared to $144.6 million in the same quarter last year, revenue in Q1/24 was only $119.1 million – resulting in 17.6% YoY decline. But despite a declining top line, operating income increased from $17.0 million to $19.0 million – resulting in 11.8% YoY growth. The reason for the declining sales was the ongoing sales decline driven by softness in products serving the semiconductor end market. However, management pointed out one glimmer of hope during the earnings call:

And then the third thing I would note for you is that we are beginning to see in a very small way in some niche businesses where we supply UV lamps to some front end semiconductor manufacturing customers. Order entry is very nicely up when compared to last year. It is a small part of the business, but it's a good early indicator.

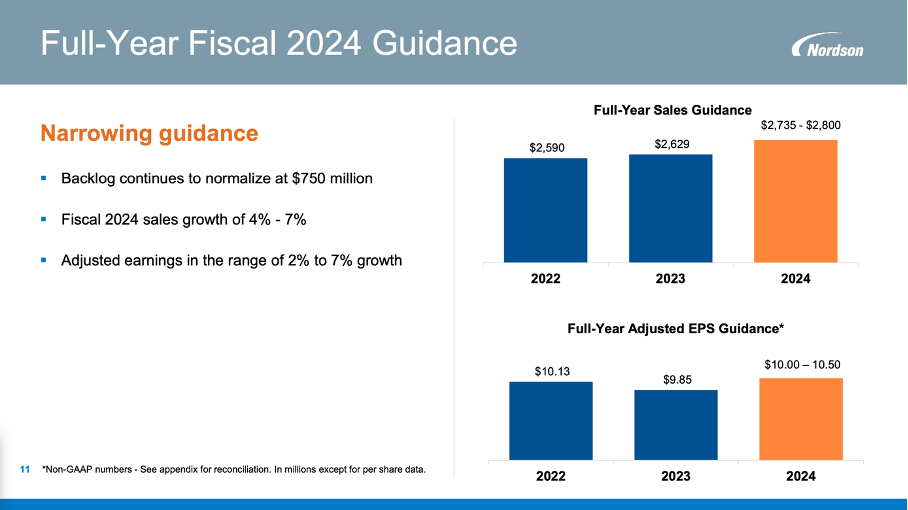

Nordson Corporation also narrowed the guidance for fiscal 2024 and is now expecting the top line to grow between 4% and 7% resulting in $2,735 million to $2,800 million in sales and adjusted earnings per share are now expected to be in a range of $10.00 to $10.50 per share. And compared to adjusted earnings per share of $9.03 for fiscal 2023 this would result in 11% to 16% growth year-over-year.

Nordson Corporation Q1/24 Presentation

And management as well as analysts are not only optimistic for fiscal 2024 but also for the years to come. When looking at analysts’ estimates for the years between fiscal 2023 and fiscal 2028, we see rather optimistic growth assumptions. Earnings per share is expected to grow with a CAGR of 10.30% in the next five years.

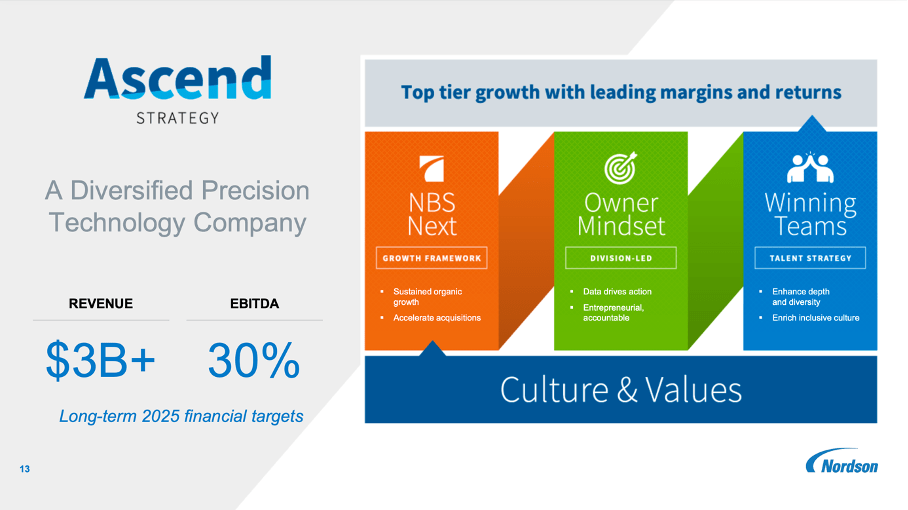

Management also has its goal to reach $3,000 million in revenue in 2025. This is part of the company’s Ascend Strategy and management set a long-term growth target of at least 7% growth for the top line and 10% growth for EBITDA (we can assume that these growth targets will be updated in 2025).

And although I have written three articles about Nordson Corporation in the past, I did not talk about the Ascend Strategy in any of the three articles. Nordson Corporation has always been growing with a healthy pace in the past decades, but in 2021 the company launched its Ascend strategy to deliver market leading growth. This strategy was structured around three pillars built around Nordson’s culture and values.

Nordson Corporation Q1/24 Presentation

The Ascend Strategy is including the talent strategy – including to enhance depth and diversity – and an owner mindset, which is focusing on data-driven action and an entrepreneurial and accountable approach of the business. Nordson is also focusing on making decisions close to the customer and every strategy decision should be focused on deploying NBS Next. But the heart of the Ascend strategy is the growth framework NBS Next. It is the company’s strategy to sustained organic growth in the years to come, which is also including to accelerate acquisitions.

Nordson Corporation Q1/24 Presentation

The company is writing on its homepage:

At the heart of Nordson’s Ascend Strategy is NBS Next, Nordson’s data-driven growth framework. It is rooted in the belief that a small group of customers and products contribute to a significant portion of our revenues and profits. More importantly, investing disproportionately in these customers and products will deliver top-tier profitable growth. Put simply, it is about making choices, focusing on those choices, and simplifying the rest.

And during the last earnings call, management explained once again that Nordson is focusing on top products driving a favorable product mix as well as focusing on improved factory efficiencies. During the last earnings call, CEO Sundaram Nagarajan commented:

Nordson is sustaining market leading positions in diversified end markets through our close to the customer business model and differentiated precision technology. Now, NBS Next has become a new core strength and is manifested in how we operate our businesses.

Using data, our teams have a crystal clear view of the profitable growth opportunities in each division. Coupled with an entrepreneurial owner mindset, they are making choices on where they should prioritize growth, as well as where they must simplify.

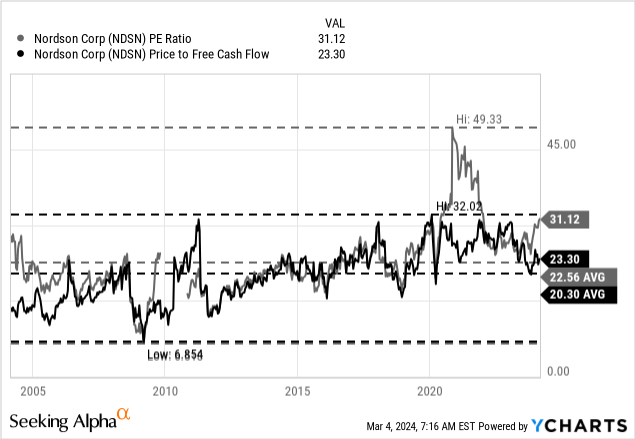

And when being more or less optimistic about Nordson and the potential to grow in the years to come, it also seems like the stock is fairly valued or even undervalued at this point. However, when looking at the price-earnings ratio, it seems rather difficult to call the stock cheap as it is trading for 31 times earnings, which is not only above the long-term average of 22.56 but one of the higher valuation multiples Nordson has been trading for in the past two decades.

When looking at the price-free-cash-flow ratio, the picture is looking a bit brighter as Nordson is trading “only” for 23 times free cash flow. This is still above the long-term average of 20.30 but is a valuation multiple that can be justified for a great business growing with a stable pace.

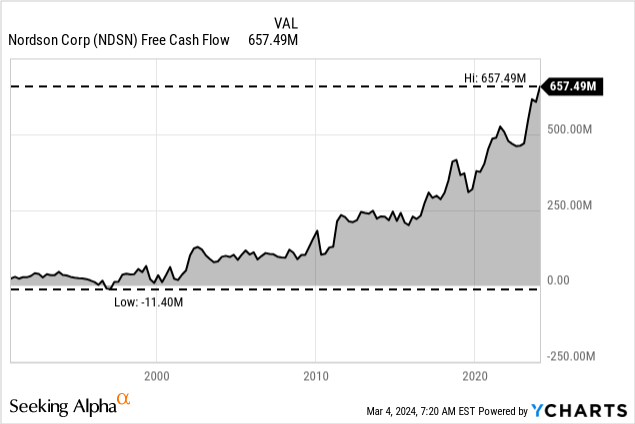

But as always, P/E ratio and P/FCF are only a first hint if a stock is undervalued or not. When using a discount cash flow calculation, we can come to the conclusion that Nordson is trading below its intrinsic value. We are calculating with 57.56 million outstanding shares and a 10% discount rate and as basis for such a calculation we can use the free cash flow of the last four quarters, which was $657 million.

Of course, this is the highest free cash flow Nordson every reported, but the business is constantly growing and the amount does not seem unreasonable. In my last article I calculated with 6% growth from now till perpetuity for Nordson Corporation and when using this growth rate once again we get an intrinsic value of $285.35. At the time of writing, Nordson Corporation is trading for $265 and is therefore slightly undervalued.

Here we can make the argument that Nordson Corporation can also grow with a higher pace than 6% in the years to come. Not only are analysts expecting Nordson Corporation to grow with a CAGR of 10%, but the company also grew with a CAGR of 9.48% in the last ten years. And in the last 30 years, Nordson Corporation grew with a CAGR of 9.67%. When being a little more optimistic and assume a growth rate of 8% in the next 10 years, we get an intrinsic value of $328.79 for Nordson Corporation (when calculating with 9% growth, we even get an intrinsic value of $352.90).

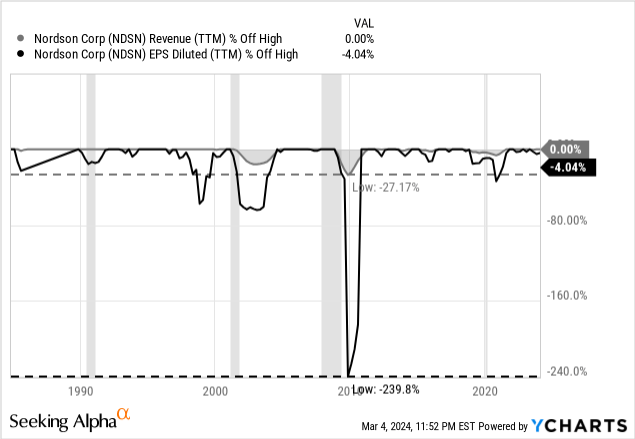

Although Nordson Corporation might be slightly undervalued, I would still be rather cautious. Especially when looking at the performance during last recessions, we see revenue as well as earnings per share decline (during the Great Financial Crisis it was an extremely steep decline). And with a high risk of the U.S. economy heading for turbulent times, we should be more cautious at this point.

But as we are dealing with a high-quality business, I would argue to “Hold” the stock at this point – at least if you are a long-term investor with a time horizon of at least 5 to 10 years.