pixelfit

pixelfit

December 21st ended up being a pretty good day for shareholders of nCino (NASDAQ:NCNO). Shares of the company closed up about 3.4% after news broke that the business has revised and extended its partnership with Salesforce (CRM). While the specifics are currently unknown, this should bode well for the company of what management stated in the press release is true. On top of this, it's also true that the company has been doing quite well from a revenue growth perspective, and it has been doing a fine job in pushing in the direction of profitability. Those who are bullish about the business will, without any doubt, see recent developments as even more reasons why to pick up shares of the company. But I'm not so sure.

You see, back in September of 2022, I wrote an article that took a rather bearish stance on the company. I found myself impressed by how rapid revenue was growing, and my overall feeling was that the long-term outlook for the company was probably going to be fine. Having said that, the continued cash outflows for the business were discouraging, as was the fact that it would need to generate significant amounts of cash flow in order to be even fairly valued. This led me to rate the business a ‘sell’. Since then, that call has proven to be a good one. While the S&P 500 is up 15.7%, shares of nCino have experienced downside of 9.6%. And that's even after this tick higher on December 21st. I really like that management is making good progress in areas that count. But with how pricey the stock remains, I unfortunately have to keep it rated a ‘sell’ at this time. But if management can get to the point of achieving consistently positive cash flows, it might not be too long before I upgrade the company to a ‘hold’.

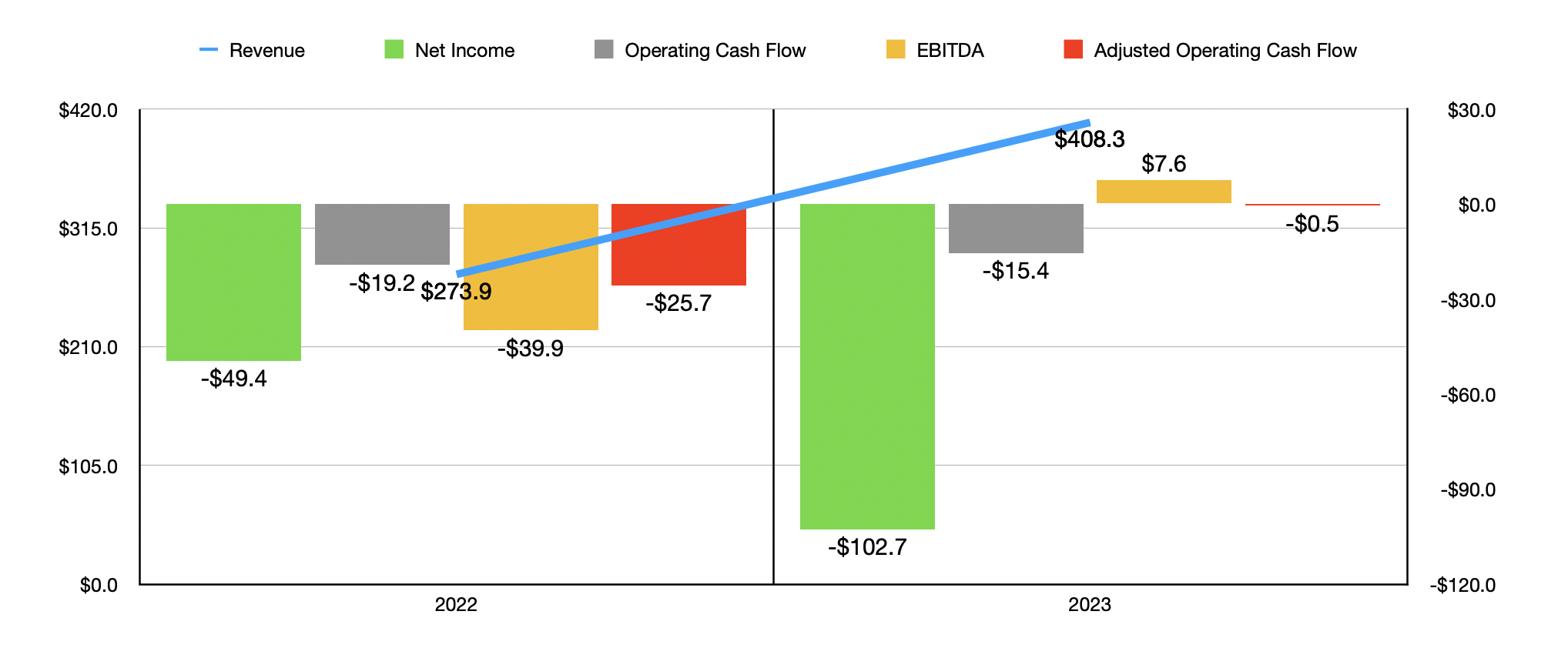

Since I last wrote about nCino over a year ago, a lot has happened for the cloud banking enterprise. As an example, we need only look at recent financial data. For the 2023 fiscal year, revenue for the company came in strong at $408.3 million. That's 49.1% above the $273.9 million generated one year earlier. Even though the firm saw continued revenue growth associated with its professional services and other revenues category, the vast majority of the increase came from subscription sales. These jumped from $224.9 million to $344.8 million. 44.5% of the revenue increase came from existing customers that added additional seats to their services and from customers and expanded their adoption of the solutions the business provides. An even larger 46.8% of the increase was attributable to the company’s acquisition of SimpleNexus.

Author - SEC EDGAR Data

With the rise in revenue came a worsening of the company's bottom line. The firm's net loss widened from $49.4 million to $102.7 million. But other than that, all of its profitability metrics actually got better. Operating cash flow went from negative $19.2 million to negative $15.4 million. If we adjust for changes in working capital, it improved from negative $25.7 million to negative $0.5 million. And lastly, EBITDA for the company went from negative $39.9 million to positive $7.6 million.

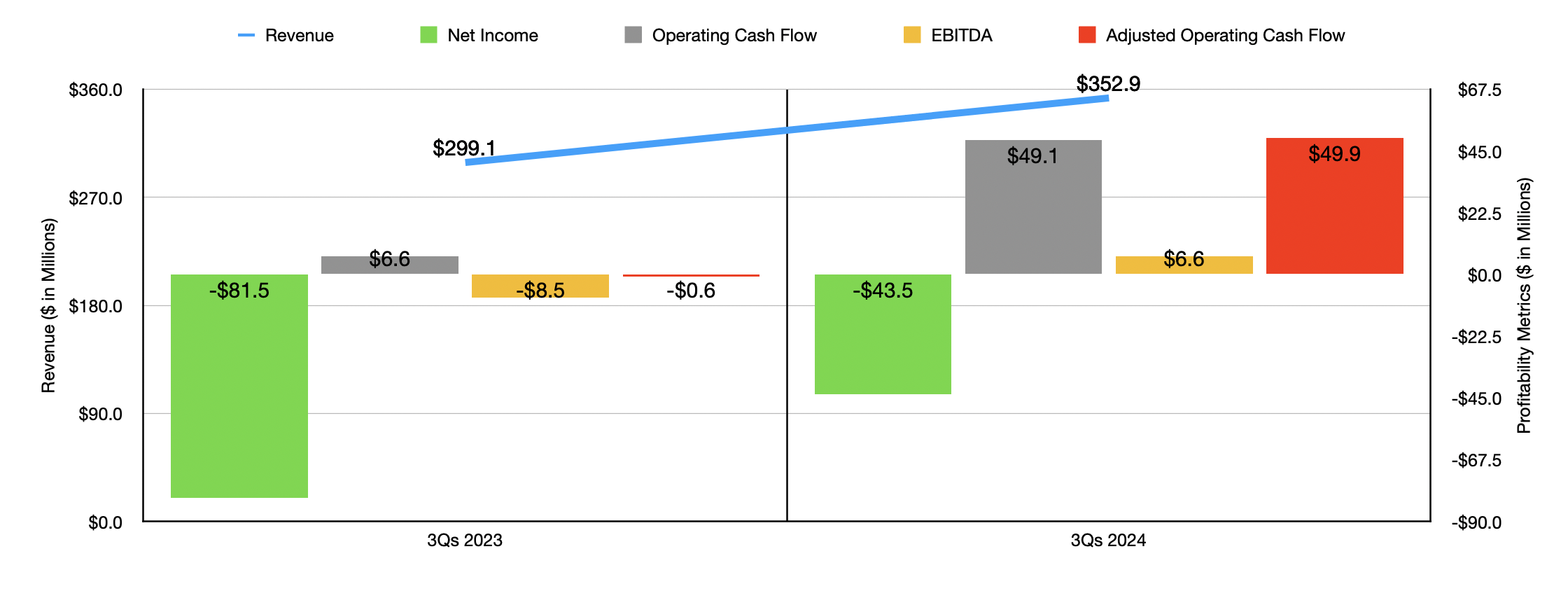

Since the 2023 fiscal year came to an end, the company has had three additional quarters worth of data covering the 2024 fiscal year. We have seen continued growth on that front, with some meaningful improvements from a cash flow perspective. For starters, revenue in the first nine months of the 2024 fiscal year came in at $352.9 million. That's an increase of 18% over the $299.1 million generated the same time last year. What's really exciting is that, while 19.3% of the sales increase was attributable to revenues coming in from customers who are new to the platform, 80.7% of the increase came from existing customers filling additional seats and expanding their adoption of the company's solutions. Although it's great to see new customers and that should be the long-term goal, such rapid expansion in sales from existing customers shows that the firm has a sticky business model they should help to lock in customers for the long haul.

Author - SEC EDGAR Data

With this rise in revenue came improvements on the company's bottom line. Its net loss went from $81.5 million in the first nine months of 2023 to $43.5 million the same time this year. Even better, operating cash flow went from only $6.6 million to $49.1 million. If we adjust for changes in working capital, we get an even better picture, with the metric climbing from negative $0.6 million to positive $49.9 million. And lastly, EBITDA for the company went from negative $8.5 million to positive $6.6 million.

Even though management has been doing a fine job improving the company's bottom line, there is still plenty of room for improvement. And that's where the December 21st announcement came into play. In its press release, the company said that it was expanding its partnership with Salesforce by utilizing more of its platform tools, including its CRM, powered by AI and automation, and its Financial Services Cloud. These will help nCino’s customers when it comes to experiences like onboarding, loan origination, the opening of deposit accounts, and even portfolio management. The extension of the agreement is to 2031, so both companies are looking at this from a long-term perspective.

Author - SEC EDGAR Data

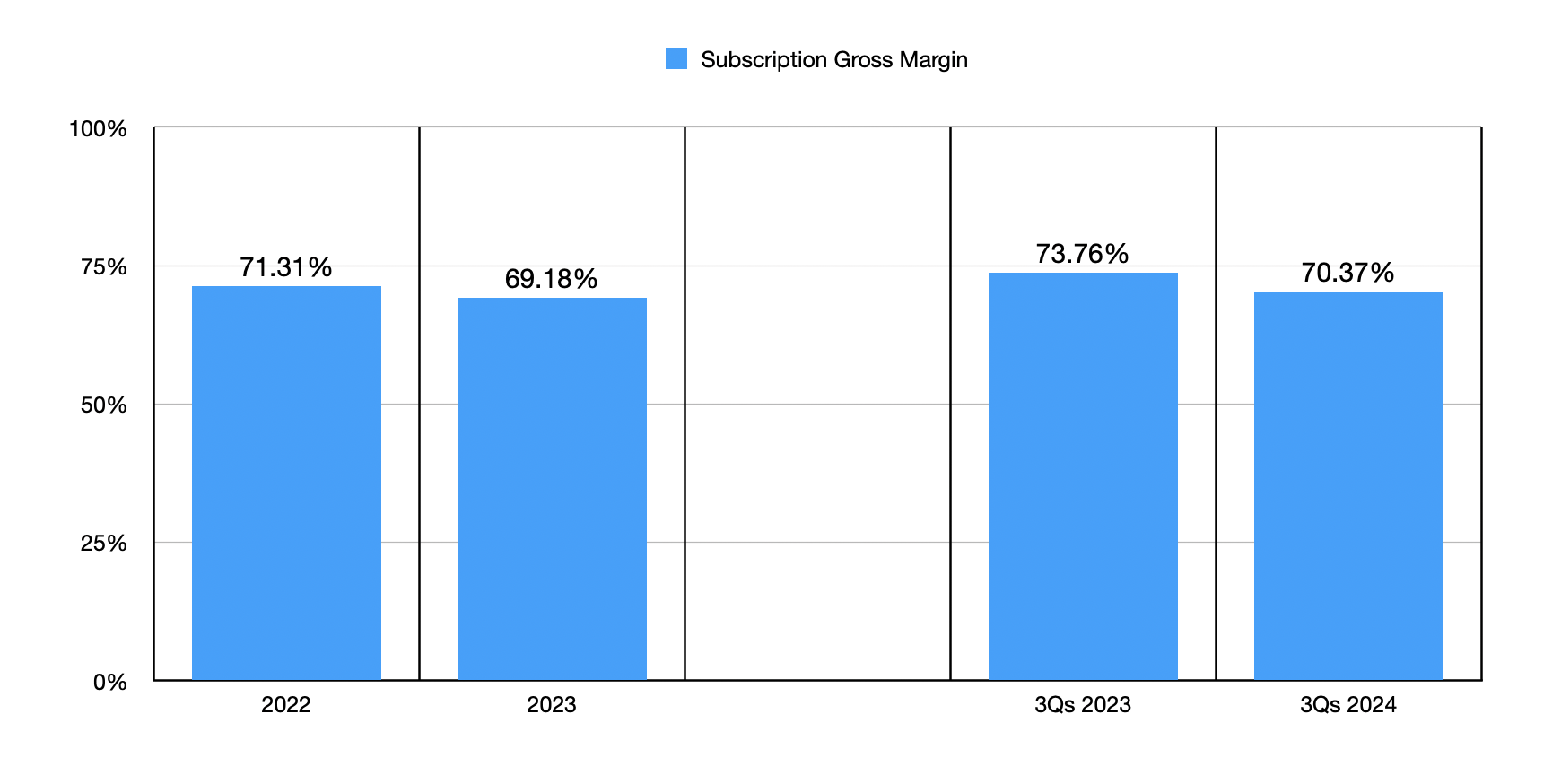

Unfortunately, we don't know what kind of financial impact this will have on the company. But we do know that, with minimum payment commitments expected from nCino during the first four fiscal years of the term of the extension, management is expecting subscription gross margins to improve by an unspecified sum. This is actually really great, because, in recent years, subscription margins have actually contracted. In the chart above, you can see how they contracted from 2022 to 2023 and how they have contracted so far for 2024 relative to 2023.

Meaningful margin improvement and meaningful revenue growth is likely what will be required for the company to become an appealing opportunity. The good news is that we at least have some idea what revenue should look like for the 2024 fiscal year. Management is expecting sales of between $476.5 million and $478.5 million. At the midpoint, that should represent a 16.9% increase over what the company generated in 2023. But even with this growth, shares look very pricey.

Author - SEC EDGAR Data

*$ in Millions

To see what I mean, I would like you to look at the table above. In it, you can see how much operating cash flow the company would need to generate in any given year to be fairly valued at a price to operating cash flow multiple of 10, a multiple of 15, and a multiple of 20. And then did the same thing with EBITDA for the EV to EBITDA multiple. Even if you assume that the company should trade a very lofty multiples, it would need to generate cash flow that is very close to half of the revenue generated in all of the 2023 fiscal year just to be fairly valued. Someday, management probably will take the company to that point. But the wasted opportunity cost waiting for that time to occur just does not make sense to me.

Seeking Alpha

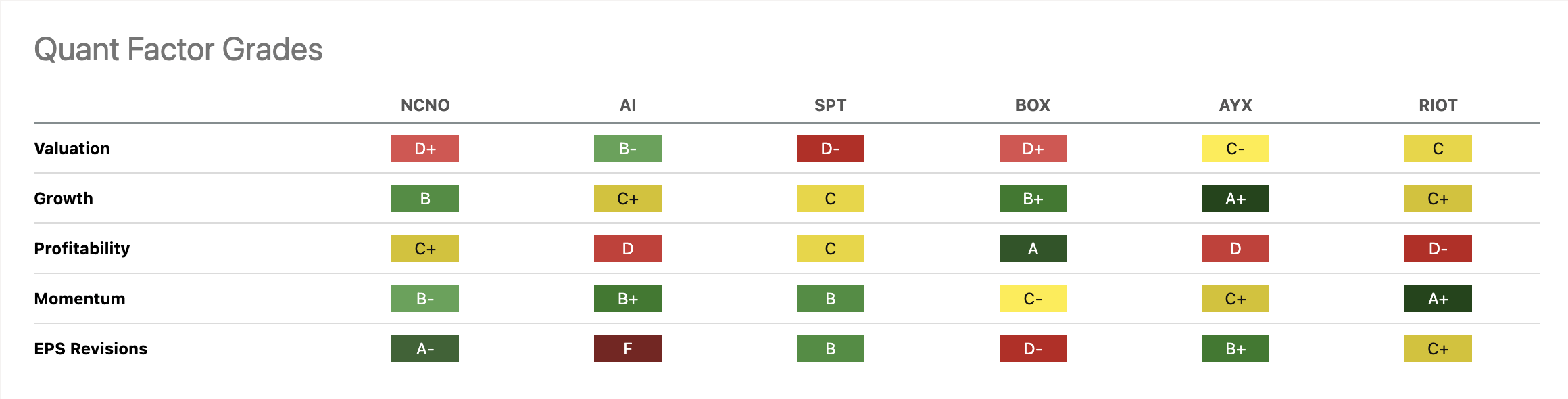

I don't expect everyone or everything to agree with me when it comes to this. And it's entirely possible that this time I could be wrong. Let's take, for instance, the Quant Rating system on Seeking Alpha and compare the company to some similar firms according to that system. As you can see in the image above, while Seeking Alpha analysts rate nCino a ‘hold’, Wall Street analysts and the Quant Rating system both rate the company a ‘buy’. When you dig deeper, such as with the information below, you can see what goes into the ratings for these firms. I actually agree with a lot of the various components. For instance, I commented favorably on the growth that nCino is experiencing. If anything, the B rating provided by Seeking Alpha looks a bit conservative to me. On the profitability side of things, the system very well could be assigning more weight to the most recent financial results, which is definitely understandable. And on the momentum side of things, the B- is probably justifiable, since shares are up 10.3% in the last month alone.

Seeking Alpha

As a value investor, I place a tremendous amount of weight on the valuation of the companies that I analyze. Sometimes, this even results in missed opportunities, companies that are growing rapidly but are so pricey that I end up passing on them. Those firms sometimes continue to achieve such rapid growth that shares appreciate anyways. I would say that the D+ assigned by the system is appropriate. It's just that I have a different weighting for that than Seeking Alpha’s Quant Rating system does.

Conceptually, I really like what nCino does, and I would love nothing more than to be bullish about it. This is especially after seeing such rapid growth on the top line over the past year or so. But at the end of the day, investing is not about buying what you want. It's about buying what you believe will make you wealthier. And from the numbers I see here, there just is not anything substantive for shareholders at this time. Maybe as we see this suppose that margin improvement and as sales grow further, my mindset might change. But for now, I fully anticipate that shares will continue to underperform the broader market for the foreseeable future.