courtneyk/iStock via Getty Images

courtneyk/iStock via Getty Images

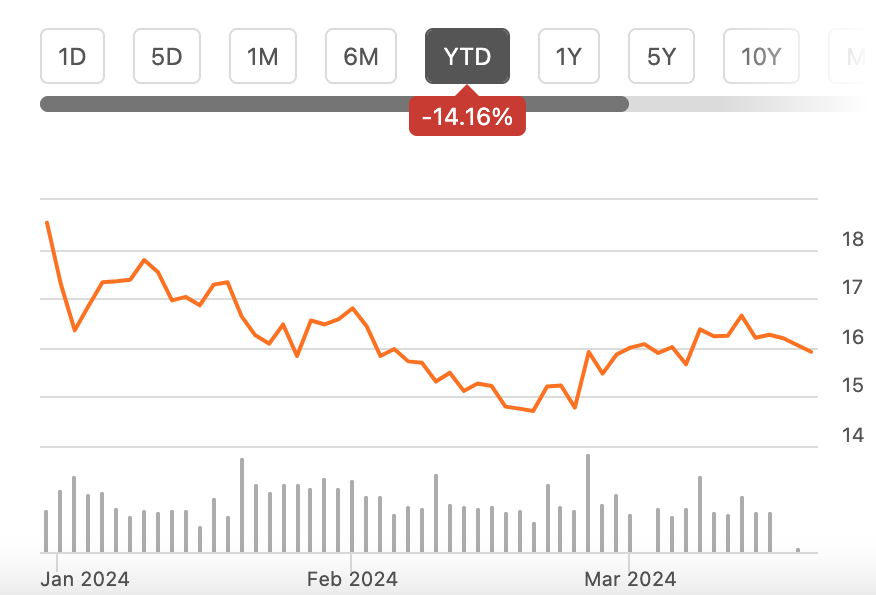

Since I last wrote about the cruise operator Carnival Corporation (NYSE:CCL, NYSE:CUK) in December last year, the exceptional price rise in 2023 has petered out. On the contrary, it has actually seen a small 3.6% decline since. The stock's year-to-date [YTD] fall at the time of writing is even sharper at over 14% (see chart below).

Price Chart (Source: Seeking Alpha)

This is in contrast to the upside still indicated by both its financial performance and its market multiples in December. This was even though the company had marginally revised down the upper end of its adjusted EBITDA range for its full-year 2023 (financial year ending November 30, 2023).

However, Carnival has released its final quarter (Q4 2023, year ending November 30, 2023) and full financial year 2023 results since. The results release also carried its outlook for 2024. With Carnival’s Q1 2024 results due later this month, here I look at (i) whether and how the last results and projections impacted the stock and (ii) what the upcoming quarterly figures can mean for it.

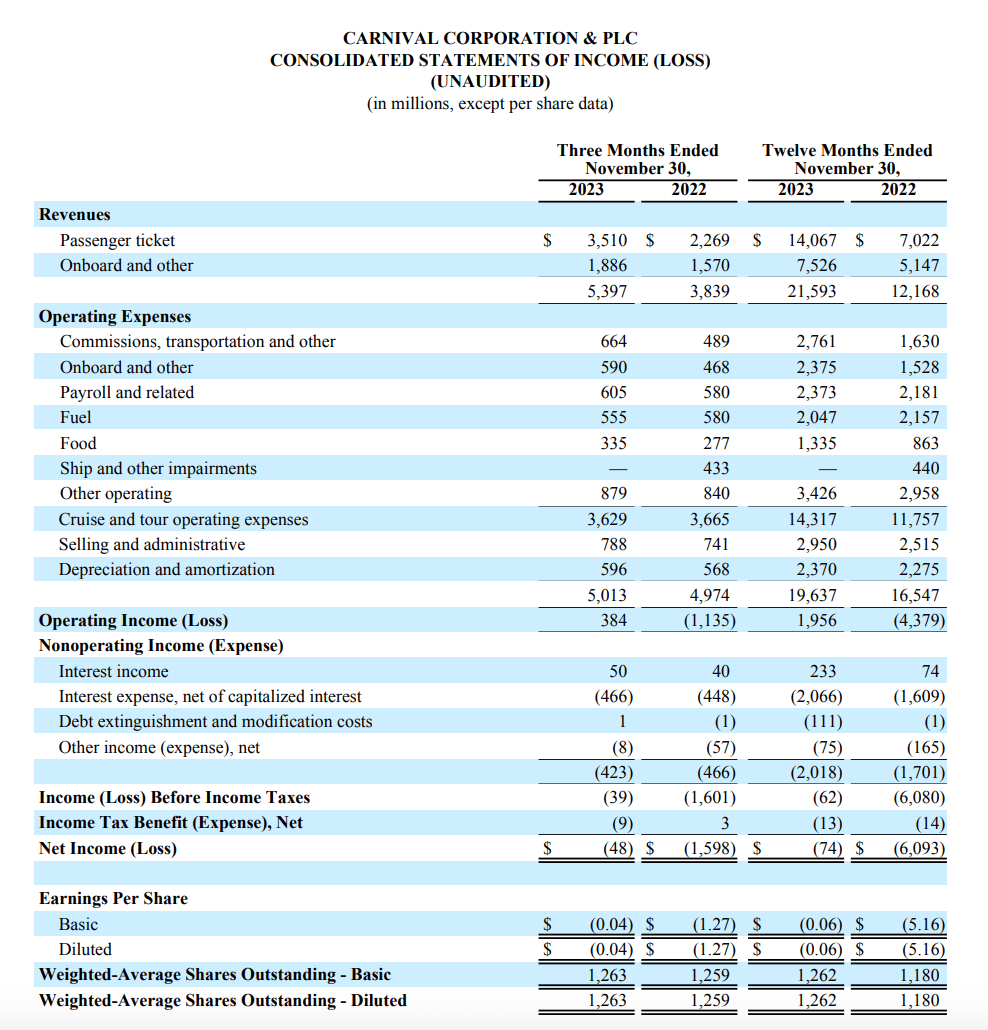

There’s really little to complain about as far as the latest earnings report goes. Net revenues grew by a very healthy 77.5% in 2023, which was higher than my estimate of 68% growth. Even growth in Q4 2023 came in at a very healthy 40.6% year-on-year (YoY), even on a high base as revenues grew by almost 3x YoY in Q4 2022.

Further, Carnival’s adjusted EBITDA also slightly exceeded the company’s projections. For the full year, it came in slightly higher at USD 4,231 million than the downwardly revised guidance range of USD 4,100-4,200 million. In Q4 2023, the number came in at USD 946 million, which was also higher than its projection of USD 800-900 million.

Source: Carnival Corporation

Carnival even reported an adjusted net income of USD 1 million in 2023, after having clocked losses since the pandemic. It did, as expected, however, show a reported loss in both Q4 2023 and for the full year 2023.

Finally, its debt has also started receding. The company saw a big 2.5x jump in debt in 2020 due to the pandemic and increases in debt in the following two years. However, it finally reversed the trend in 2023, with an 11% reduction. The net debt-to-assets ratio also improved marginally to 60% from 61.6% in 2022. While its net interest expenses are just about covered by the operating income now, even this is an improvement considering that 2023 is the first year of its reporting operating income since 2019.

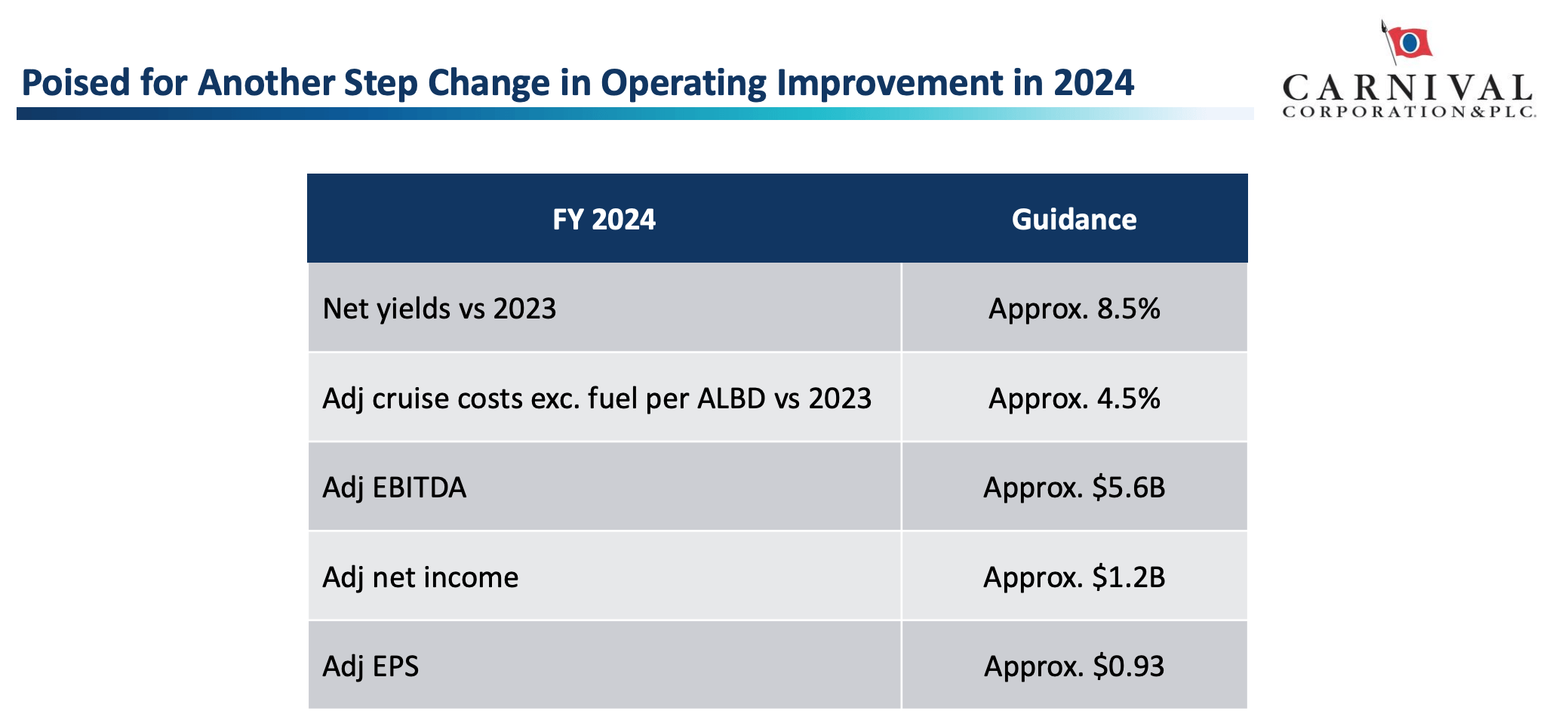

The numbers are expected to improve even further this year. And the signs are already here. The company’s CEO, Josh Weinstein noted in the last results release “We entered the year with the best booked position we have ever seen, and now have nearly two-thirds of our occupancy already on the books for 2024..” This is particularly encouraging at a time when macroeconomic projections indicate weakness in its biggest markets, particularly the US.

Carnival also expects a 30% increase in adjusted EBITDA to USD 5.6 billion. It also expects a significant jump in adjusted net earnings of USD 1.2 billion.

Forecast, 2024 (Source: Carnival Corporation)

However, despite the strong performance in the past year as well as the positive outlook for the current financial year, there are two reasons why the price can continue to correct now.

Even as Carnival expects the adjusted EBITDA to double from Q1 2023 to USD 800 million in Q1 2024, on the whole, the results could be a downer for two reasons.

First, after a massive 2.7 increase in net revenues in Q1 2023, it’s unlikely that it can match the same rise in the upcoming results. Analysts’ estimates on Seeking Alpha put the growth at a still strong but comparatively softer 22%. Second, Carnival expects an adjusted net loss during the quarter as well, indicating that it will become profitable only later in the year.

Even with the huge improvement expected in full-year 2024 adjusted net income, the stock’s forward non-GAAP price-to-earnings (P/E) ratio of 16.9x is comparatively somewhat elevated. First, consider the comparison to the consumer discretionary sector, whose corresponding P/E is at 15.6x. Carnival isn't terribly higher than this level, but at the very least, it shows little upside to the stock.

Second, the trend is further cemented when the company’s closest peers, Norwegian Cruise Line Holdings (NCLH) and Royal Caribbean Cruises (RCL) are considered. They are trading at corresponding P/Es of 15.2x and 12.8x, respectively.

In the past, I’ve compared the price-to-sales (P/S) for cruise operators to determine where Carnival stands. And in terms of the TTM P/S, at 0.95x, it's still better placed compared with both RCL at 2.36x and also NCLH at 0.98x. However, this multiple was relevant when cruise companies weren’t income generating. Since they are expected to become profitable this year forward, I’d deemphasise the P/S. And the P/E indicates overvaluation for Carnival.

Based on the forward non-GAAP P/E for Carnival’s peers, there's a possibility of another 15-20% price correction from the current levels. However, this decline will be justified only if the company’s net income projection is on point. Going by last year’s adjusted EBITDA figures, it may well exceed projections this year too. This is especially so considering the strong booking numbers for 2024 so far. Further, reduced debt and interest expenses can also give income a fillip.

It’s not as if there aren’t risks. Cruises are a discretionary spend and the weak economic outlook for 2024, particularly in its big US market, is a risk. Whether it plays out, though, remains to be seen.

For now, I’m downgrading the rating to Hold anyway until the upcoming results are released. If it shows outperformance in either revenue growth compared with analysts' estimates or manages to clock an unexpected net profit in Q1 2024, the outlook on the stock can change.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.