Peter Jordan/Popperfoto/Popperfoto via Getty Images

Peter Jordan/Popperfoto/Popperfoto via Getty Images

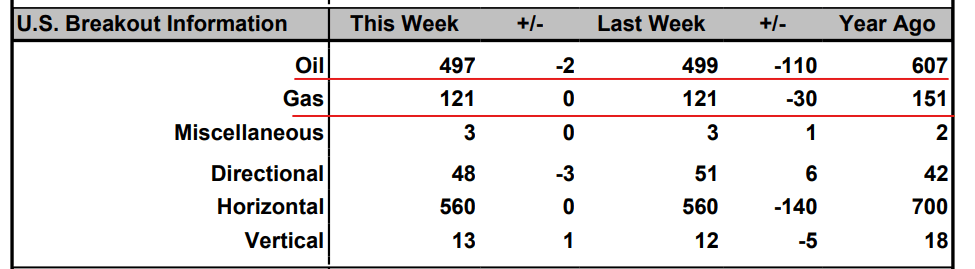

Nabors Industries (NYSE:NBR) didn't have a good 2023, similar to other onshore oilfield services (or OFS) providers (OIH) with exposure to the U.S. oil and gas basins. Lower prices led to rig count reductions, and U.S. rigs are now down year-on-year by approximately 20% on both the oil and gas side:

Baker Hughes Rig Count

Nabors, however, is as much an international company as it is a U.S. one. For a couple of quarters now, the "big fish" in the OFS space, Schlumberger (SLB), Halliburton (HAL) and Baker Hughes (BKR), have been highlighting the ongoing bifurcation in energy services markets. Namely, U.S. activity has been flat to modestly declining while international growth remains steady.

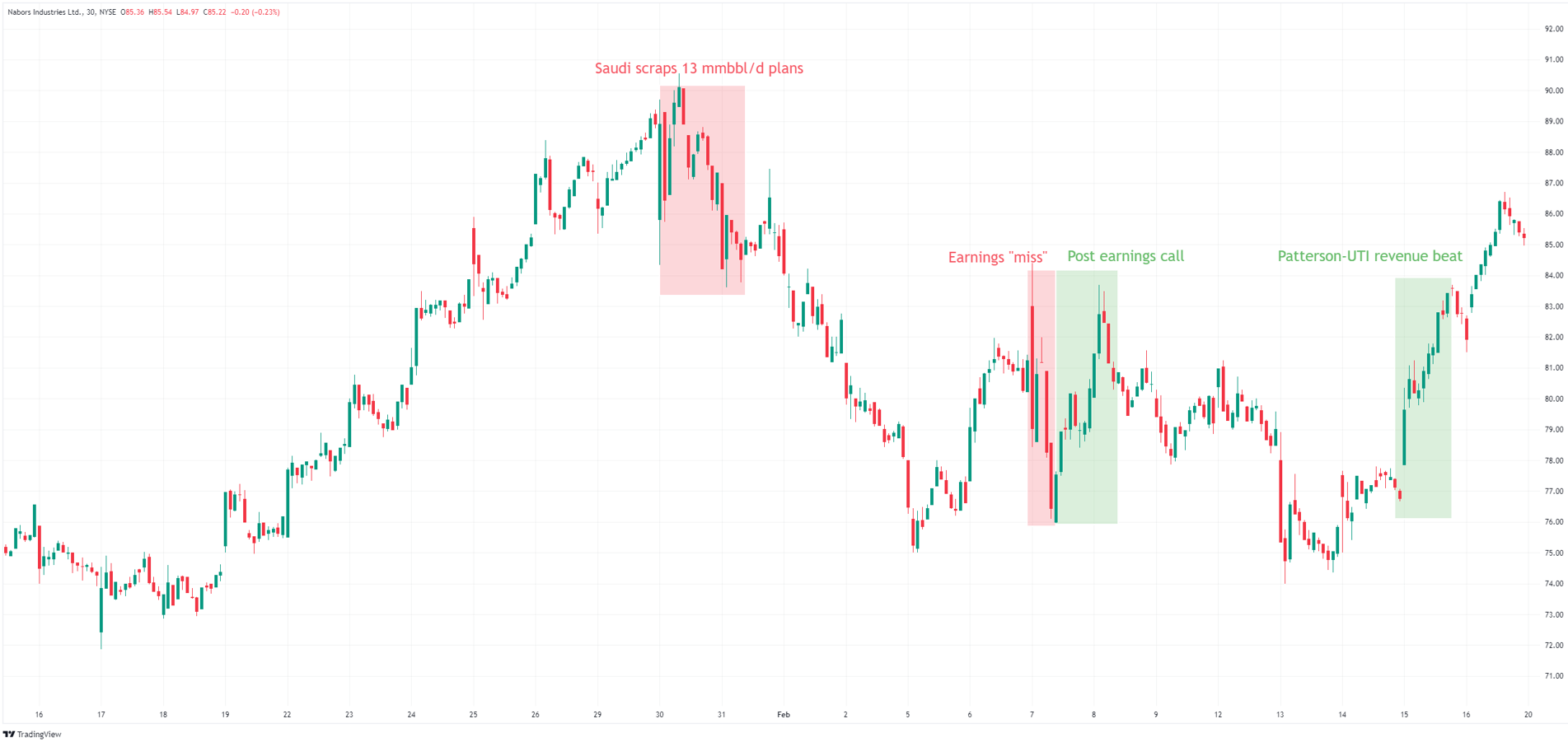

Nabors' international exposure while being valued like a domestic player had turned it into a reasonable investment idea by Q4 '23. Going into 2024, NBR sold off a bit more, but probably bottomed around mid-January:

TradingView

For the latter half of the month, things were going quite well until January 30, when Saudi Aramco (ARMCO) "shocked the world" - or at least shocked the few investors still interested in the oilfield services space. As reported by Seeking Alpha:

The country's Ministry of Energy ordered the world's largest oil producer to maintain its Maximum Sustainable Capacity at 12M bbl/day. "The company will update its capital spending guidance when its 2023 results are announced in March," Aramco said in a statement.

Aramco had been aiming to expand its maximum capacity to 13M bbl/day by 2027, as it expected energy demand to increase over the mid- to long-term.

The market interpreted this as an end to the Middle East capex bonanza that was benefitting the likes of SLB, HAL or BKR, and several OFS stocks levered to Saudi Arabia, including Nabors, got mauled pretty badly.

Nabors gave up most of its January gains and saw a couple of volatile sessions around its earnings "miss" (the earnings were good actually despite the headline EPS number). Last week, Nabors resumed its upward movement after its U.S. competitor Patterson-UTI (PTEN) reported a beat.

In the few weeks since the Saudi announcement, the dust has cleared a bit, and we have now heard from Nabors' management, as well as from other OFS players and energy research firms, about what the Saudi announcement could mean in practice.

SLB was probably the first one to issue a press release that clarified Aramco may potentially cancel two offshore projects. Nabors itself isn't involved in either of them.

The second nuance that is perhaps eluding some market participants is that land rigs in Saudi Arabia drill not just for oil, but also for unconventional gas. Only a minority of Nabors' Saudi rigs work on oil, and those contracts were just extended for 4 years.

As for the gas rigs, it's unlikely that Saudi will curtail this activity. One reason Saudi is exploring gas is to displace the oil used in power generation and free up additional oil for exports. The gas-for-oil substitution is basically an alternative strategy to get to the same exporting capacity as raising the production capacity to 13 million. This appears to make Nabors' gas rigs in the Kingdom pretty safe.

So to recap - the market penalized Nabors for the perceived risk on its Saudi revenue stream, but by all evidence, there won't be much if any impact. As this gets clear over time, I expect Nabors to recover from the January 30 news. Perhaps Aramco's capex plan to be revealed at the end of March could be the catalyst.

Note: I have previously written about Nabors on Seeking Alpha, so this article should be seen as a continuation of my prior coverage.

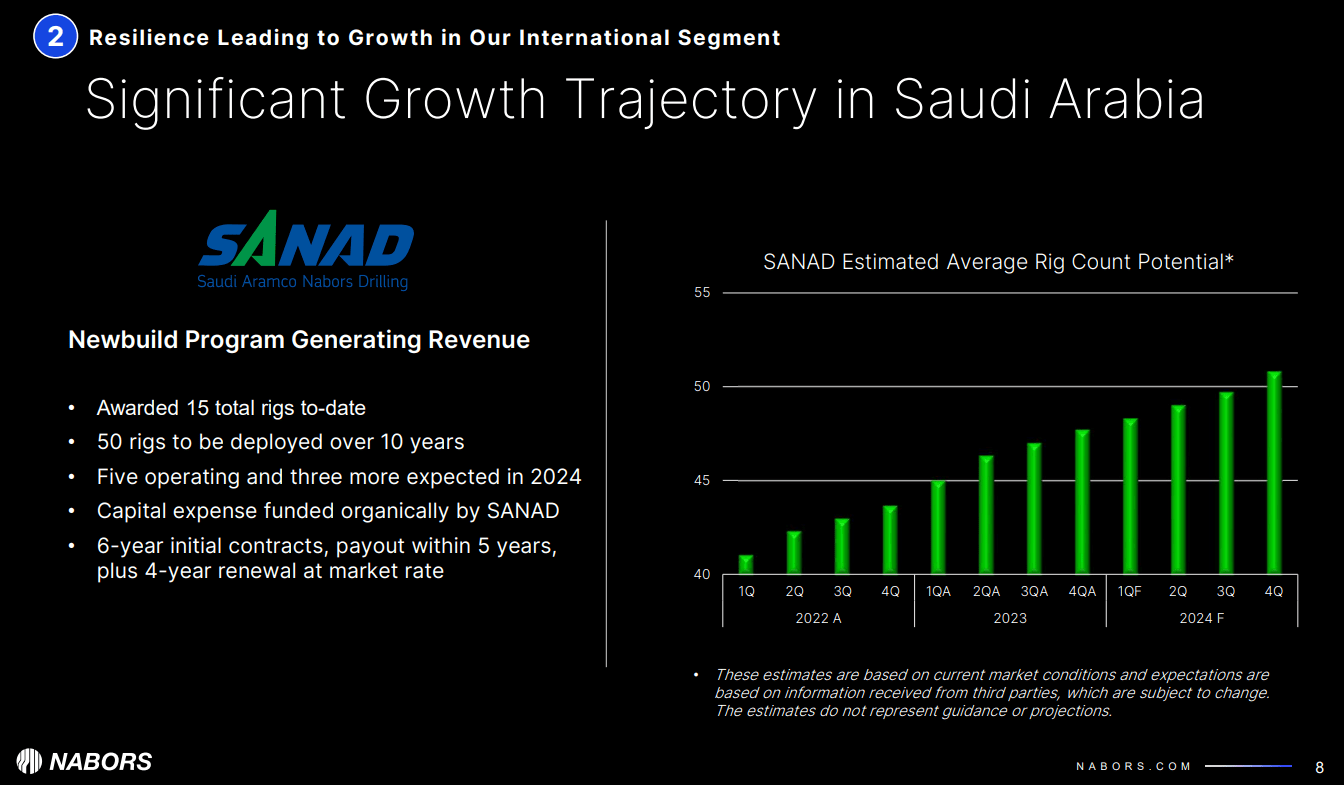

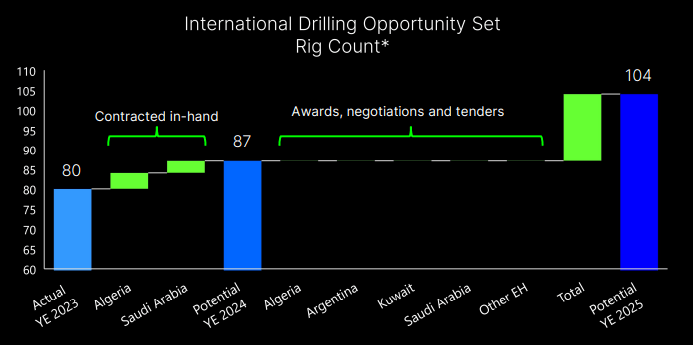

Nabors' SANAD joint venture in Saudi Arabia operates 48 rigs, and there could be a lot more coming:

Nabors Presentation

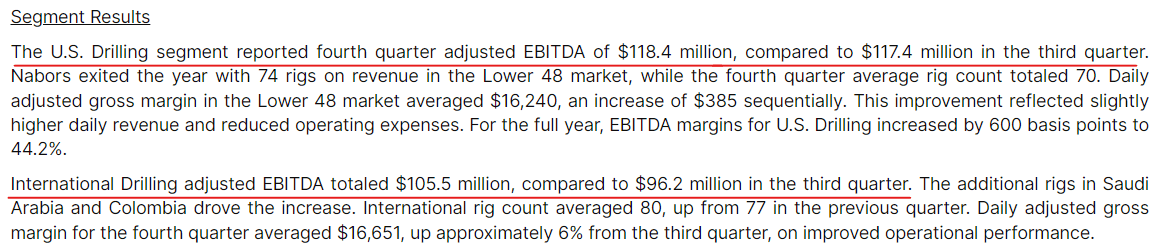

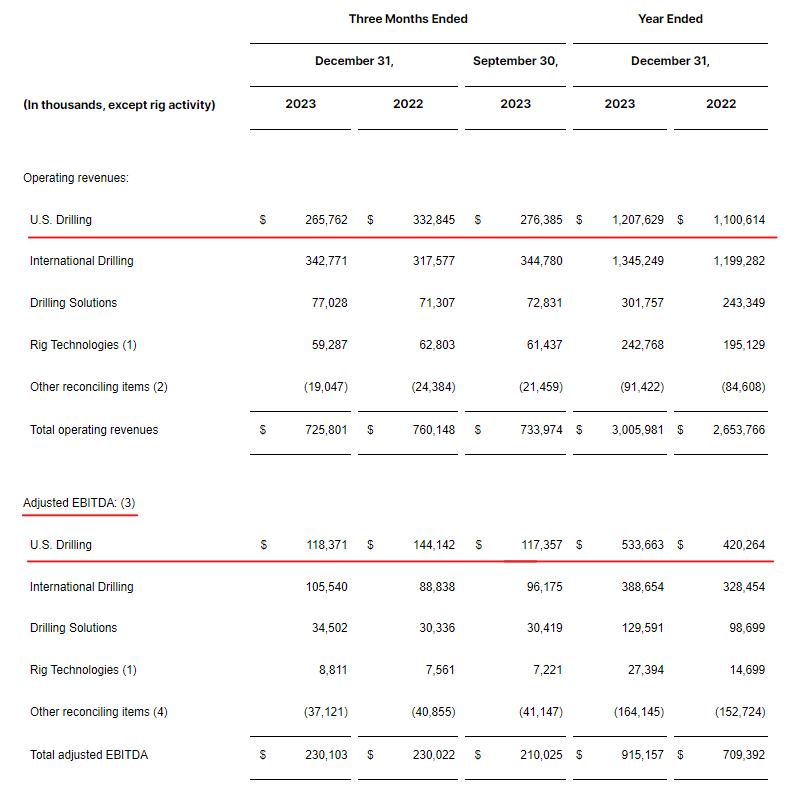

In Q4, the international segment contributed almost as much EBITDA as the U.S. and Saudi Arabia was a big contributor:

Nabors Press Release

To be fair, the Saudi joint venture also consumes a lot of capex, and the uncertainty over how many additional rigs will be awarded apparently also makes management reluctant to guide on free cash flow (the rigs are constructed in Saudi Arabia):

For the first quarter of 2024, we expect capital expenditures of approximately $170 million to $180 million, including $50 million for SANAD newbuild. This should be the high water quarterly mark for the year. We will refrain on providing annual free cash flow and CapEx guidance at this point.

However, with U.S. activity challenged, I think the Saudi expansion makes a lot of sense and will pay back. Algeria and Kuwait are also countries where Nabors is looking to add rigs:

Nabors Presentation

To be clear, none of this means that Nabors is giving up on the U.S. I have argued in my prior articles that the pressure on U.S. producers to remain profitable as their acreage deteriorates is driving a preference for more advanced rigs that can deliver efficiencies. For Nabors and a few others, this means that their rig counts may grow even if the overall U.S. pie shrinks.

At the earnings call, management again highlighted how Nabors is well-positioned to accommodate operators' growing preference for longer lateral wells:

And also the longer laterals that -- you have one super major really buying into that others haven't yet got there in large part because they don't have that to do it. But Nabors is unique in terms of our capacity to do that. I think today, I want to say that is not true, but I think we do have the longest lateral out there. I think it was something like 32,900 feet for Exxon. It was -- with the total measured depth, I think the lateral was like more than 22,000 feet. And so our top drive and the rest of our equipment is really poised to handle that racking capacity and other things.

The speculation is that the recent consolidation events, e.g., Exxon (XOM) buying Pioneer (PXD) and a couple of big private producers getting acquired, may accelerate these trends and improve Nabors' market position. Last year, NBR grew its exposure to public operators from 61% to 72%.

There has been much discussion about why the Saudis scrapped their expansion plans. Bearish takes suggest they see falling oil demand, but I have also heard bullish arguments that Aramco realized it would be more difficult to get up to 13 million than what they thought. Perhaps what makes most sense is the more pragmatic explanation that there is no need in the near term for another 1 million, given Aramco already produces below capacity due to the OPEC cuts.

In either case, the more important point is that the 13 million figure was an aspirational goal and not necessarily sanctioned capex. So while the optics are bad, nothing really is getting canceled except perhaps a couple of offshore projects (namely, Safaniya and Manifa).

According to well-known energy research firm Rystad:

The anticipation is that drilling in legacy onshore and offshore fields will persist over the next few years, maintaining Saudi Arabia's current production levels of 12 million bpd. Approximately 11,000 new wells are expected to be drilled from 2023 to 2030, primarily driven by infill operations, accounting for over two-thirds of new wells, with onshore drilling declining slightly from 2027 to 2030. As the decade progresses, gas drilling is predicted to increase in the country, reflecting rising production from Saudi Arabia's unconventional assets, such as Jafurah. This expansion is evident in the growing demand for rigs dedicated to shale gas operations.

Rystad's point on the link between land rigs and the unconventional gas projects was also brought by Nabors' management:

Let me finish this discussion on the international business with a few comments on the recent news on Saudi Arabia. SANAD currently operates 48 rigs there. Of these, 40 working gas and the balance in oil. Contracts for the oil directed rigs have really been extended for a four year period. With the Kingdom's focus on developing the natural gas resource, we are very comfortable with our position there. As to the newbuild program, this was contemplated well before capacity expansion plans in Saudi Arabia. The newbuild program is also a key element in the Kingdom's Vision 2030 plan. As such, we are confident in the program's future.

In other words, the demand for the gas rigs is robust and the company's rigs drilling for oil just got extended.

The international growth is expected to continue while the U.S. should be similar to 2023. According to NBR's CFO:

And finally, I can say that the future bodes well with double-digit international revenue growth expected in 2024 and a base being built for further Lower 48 recovery...

... Although at this point, we will not provide annual guidance, we expect Lower 48 rig count to recover throughout the year from the 2023 quarterly average. Our full year 2024 average should end up somewhere close to our average for the full year 2023. International average rig count should increase by somewhere between seven and 10 rigs, depending on timing of deployments.

"Similar to 2023" as it comes to the U.S. is not bad at all:

Nabors Press Release

Both U.S. drilling revenue and EBITDA in 2023 were a considerable increase over 2022, even though the latter had much higher oil and gas prices.

Nabors earned $915 million in EBITDA last year. Sell-side analysts expect on average $918 million in 2024 and about $1 billion in 2025. Either way, you look at it, that is slightly less than 4x enterprise value to EBITDA, which is way below the company's historical multiple.

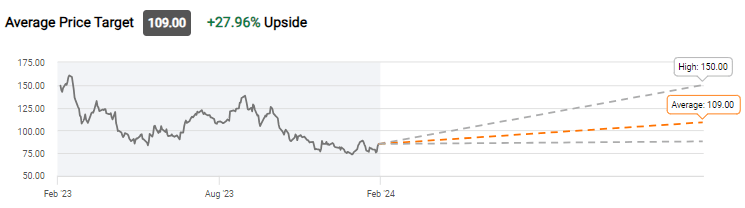

Given the high financial leverage, a modest multiple expansion to 5x already implies about 90% equity upside. The average sell-side targets are more modest, though:

Seeking Alpha

Even so, there is some disagreement with Morgan Stanley up at $150. I think 30% upside is a reasonable short-term target, but there is a lot more asymmetry to the upside. Nabors was close to $200 only a year ago.

So what are the risks? In theory, the high leverage. But I see that the 2030 notes, which are the furthest out maturity, are trading at a premium to par, at about 400 bps option-adjusted spread. It doesn't seem to signal imminent danger.

Management's reluctance to guide on 2024 free cash flow may also be a risk for how the actuals will be perceived when they come out. The average sell-side estimate for 2024 is $128 million, which will help a modest reduction in debt. But ATB Capital is at $66 million while Benchmark is at $193 million! The absence of management guidance is throwing the analysts all over the place, and this may backfire.

For 2025, the average FCF estimate is $227 million, with the highest one being $300 million. That should already start making more meaningful dents in the debt load.

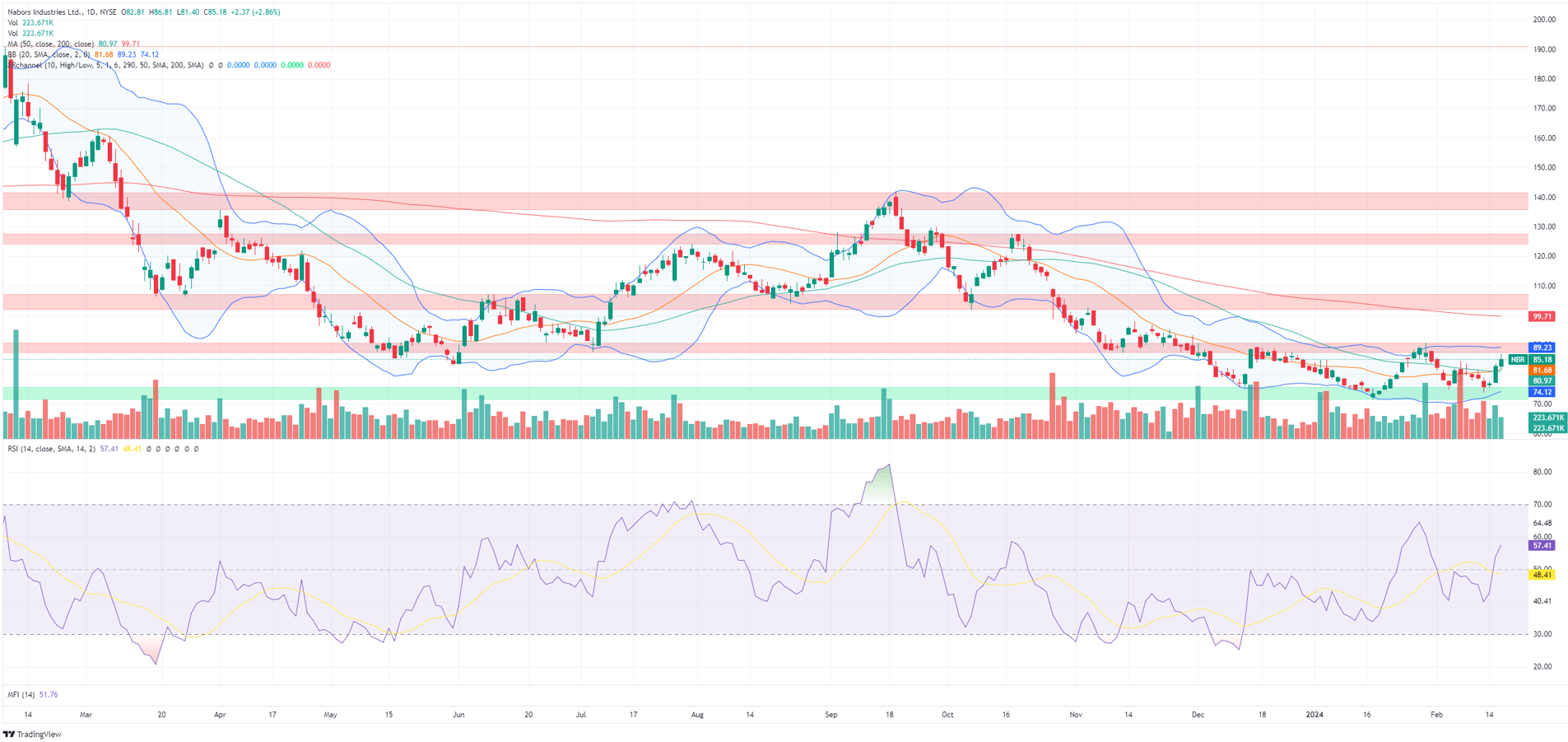

Michael Burry is said to have recommended buying stocks at 10-15% off their 52-week lows, as that presumably indicates some support has already been found.

Nabors seems to be in this exact target zone right now:

TradingView

Nabors bounced three times off the apparent support zone around $75 and is close again to resistance around $90. If we get past that, I wouldn't be surprised to see a move up to $100. Beyond that, $130 may be possible.

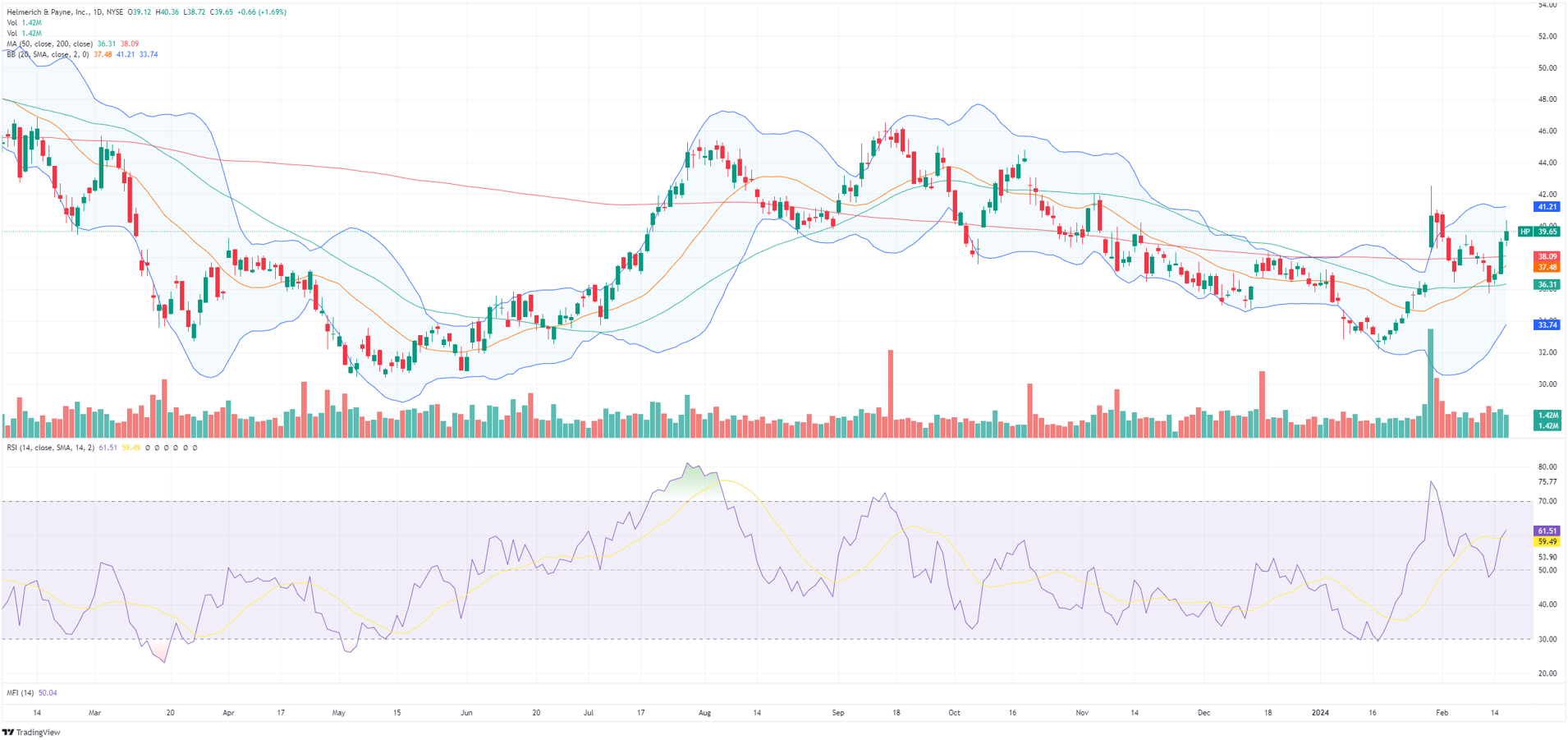

What gives me additional comfort is that Nabors' peers also seem to breaking out. Helmerich & Payne (HP) is above its 200-day moving average now:

TradingView

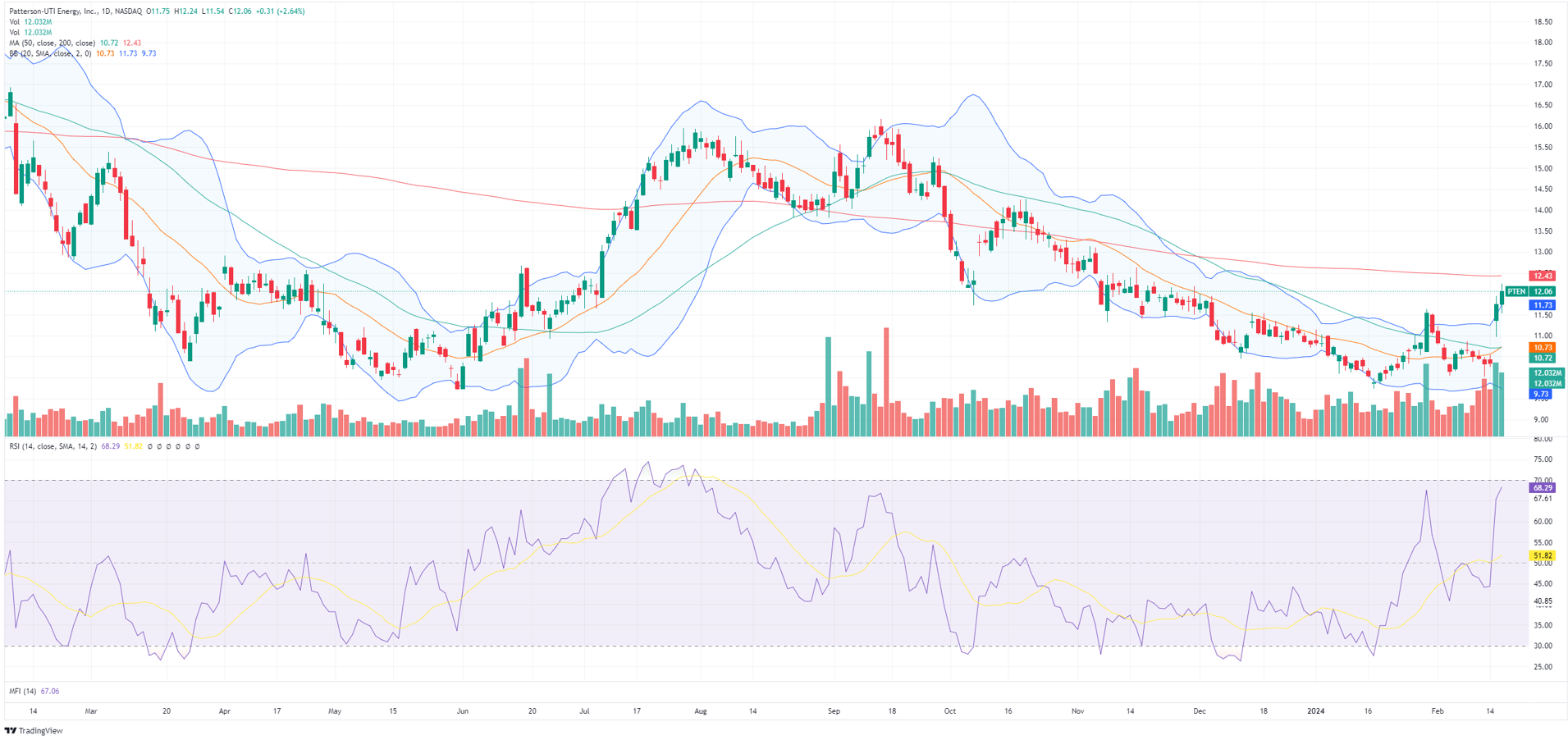

Patterson-UTI also appears to breaking out:

TradingView

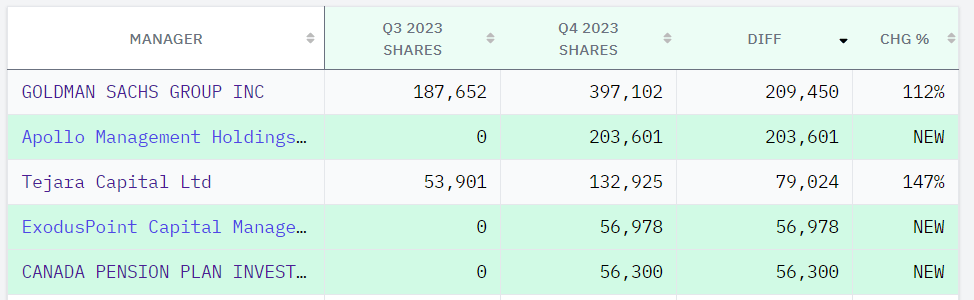

The institutional flows reported in the latest 13-Fs also look promising. These are the 5 largest reported position increases as absolute share count:

13F.info

For reasons unbeknownst to me, Goldman Sachs seems to have doubled its position in Q4. The Canadian Pension Plan, a savvy institutional investor, has apparently initiated a new position.

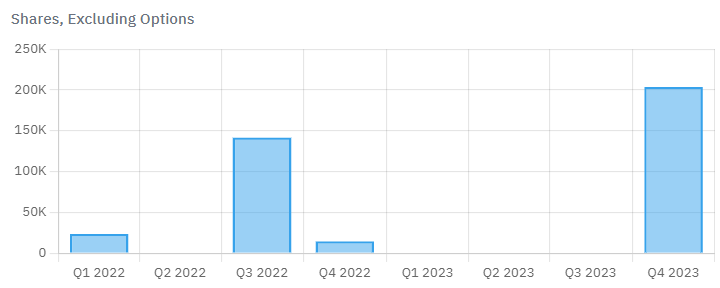

Apollo is another renowned investor who added Nabors. Interestingly, they appear to have sold in Q4 '22 when Nabors was trading at $170-$180:

13F.info

They probably thought it made sense to add again at $80 or so in Q4 '23.

Apollo's 200,000 shares are a bit more than 2% of the outstanding shares, so these numbers aren't such a small deal.

Nabors has been undervalued for the majority of the past year, except perhaps last September, when it traded at $140 or so. The stock had already started ascending when the Saudi news prompted a fresh sell-off. As Nabors' position in the Kingdom remains unaffected, this sell-off should be corrected soon. Technically, the stock has also likely bottomed and large institutional investors appear to show some interest in it too.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.