e-crow

e-crow

Do you hold any royalty trusts in your portfolio?

These entities are mainly within the Exploration & Production, E&P, Energy industry - their income is derived from arrangements with E&P companies that handle the operations on the Trust's property and pay the Trust a percentage of the income. MV Oil Trust (NYSE:MVO) is virtually a pure play on crude oil, with ~99% of its income coming from crude. The revenues from oil production are typically received by MV Partners one month after production.

Company Profile:

MVO's earnings come from a profits interest of 80% of the net proceeds attributable to the sale of production from the underlying properties during the term of the Trust. These net profits interest will terminate on the later to occur of (1) June 30, 2026 or (2) the time when 14.4 million barrels of oil equivalent ("MMBoe") have been produced from the underlying properties and sold (which amount is the equivalent of 11.5 MMBoe with respect to the Trust's net profits interest), and the Trust will soon thereafter wind up its affairs and terminate.

"As of September 30, 2023, cumulatively, since inception, the Trust has received payment for 80% of the net proceeds attributable to MV Partners' interest from the sale of 13.9 MMBoe of production from the underlying properties (which amount is the equivalent of 11.2 MMBoe with respect to the Trust's net profits interest)." (MVO Q3 '23 10Q)

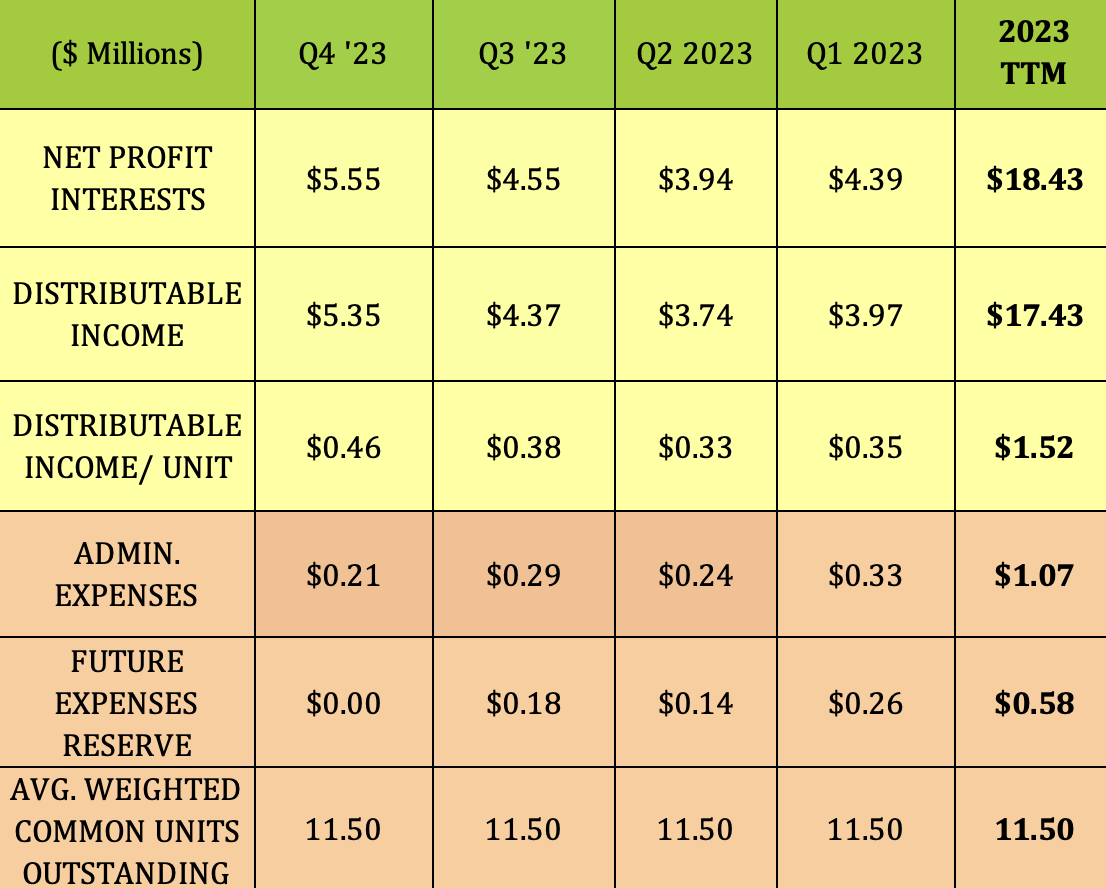

Earnings:

Q4 '23: While Net Profit Interests, NPI, have been much lower in 2023 than in 2022, they have been on the rise in the past two quarters, jumping from $3.9M in Q2, to $4.55M in Q3, and then to $5.55 in Q4 '23.

Q4 '23 was the highest NPI since Q4 '22.

With the unit count fixed, and expenses and reserves minimal, MVO's distributable income/unit rose from $.38 to $.46 in Q4 '23:

Hidden Dividend Stocks Plus

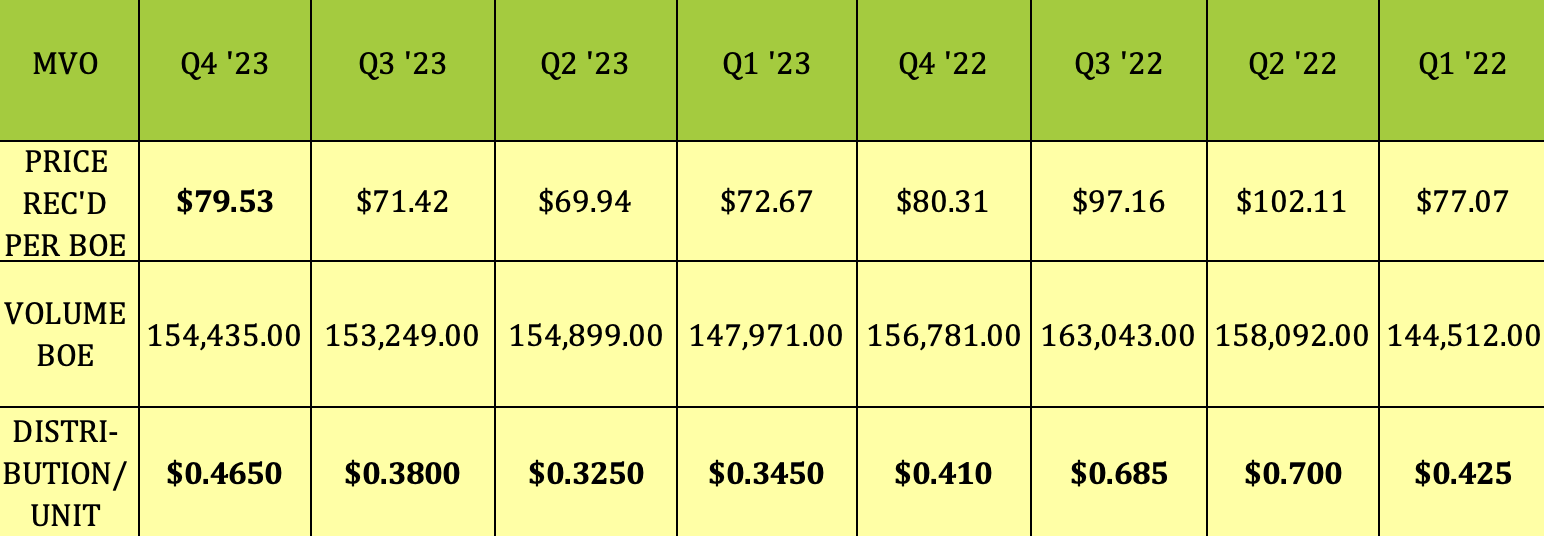

Both volume and price per barrel improved in Q4 '23, with price/barrel hitting $79.53, resulting in a higher distribution/unit of $.465.

Hidden Dividend Stocks Plus

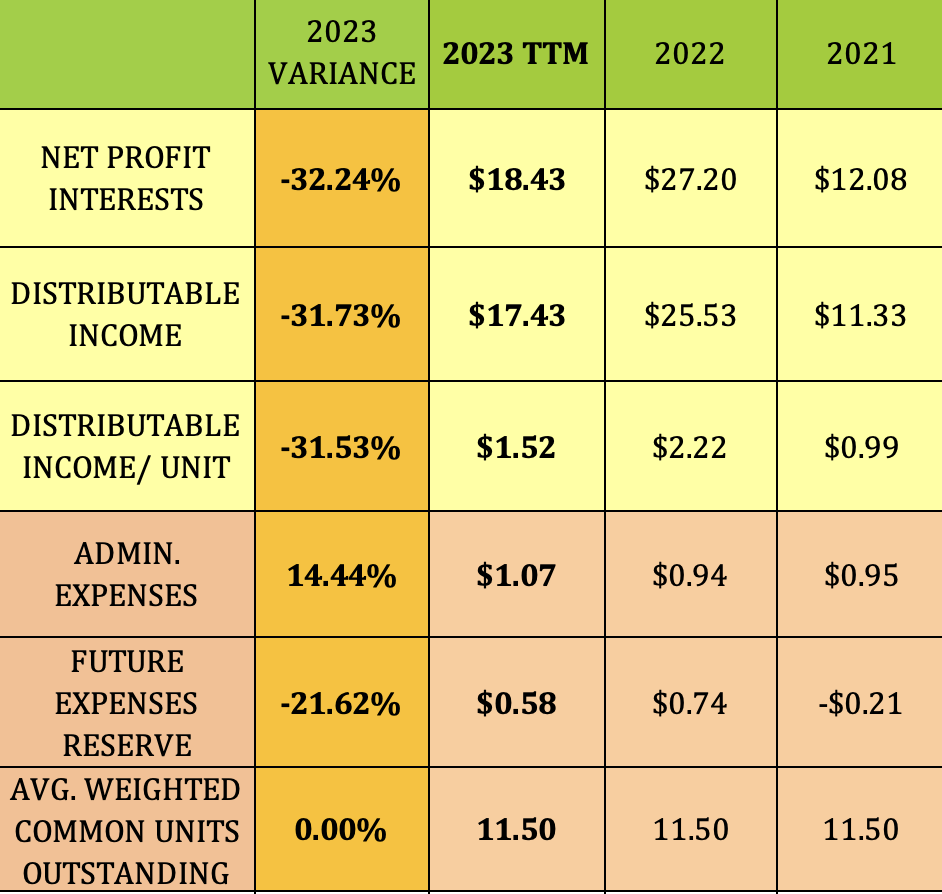

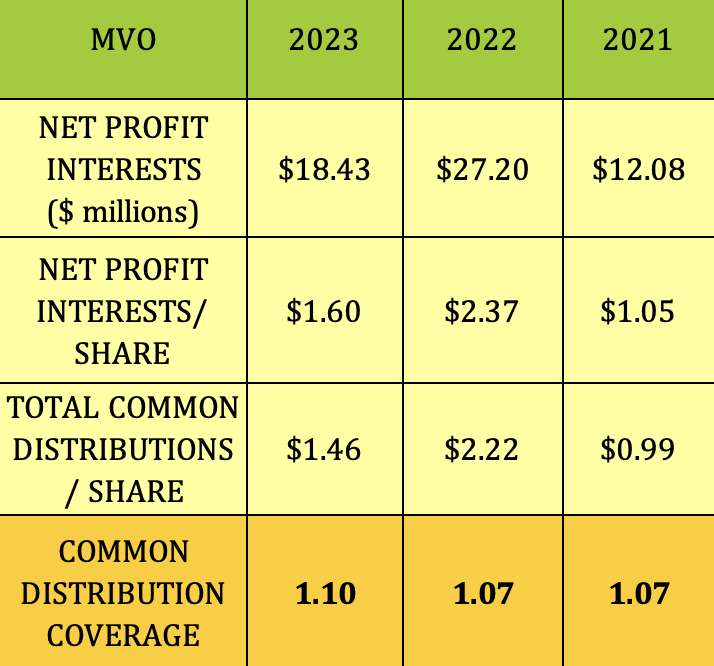

Full Year 2023:

Coming out of COVID-impaired 2021, 2022 was a huge year for MVO, with NPI and distributable income more than doubling. While 2023 was down ~32% for those metrics, it was still up by ~50% vs. 2021:

Hidden Dividend Stocks Plus

Dividends:

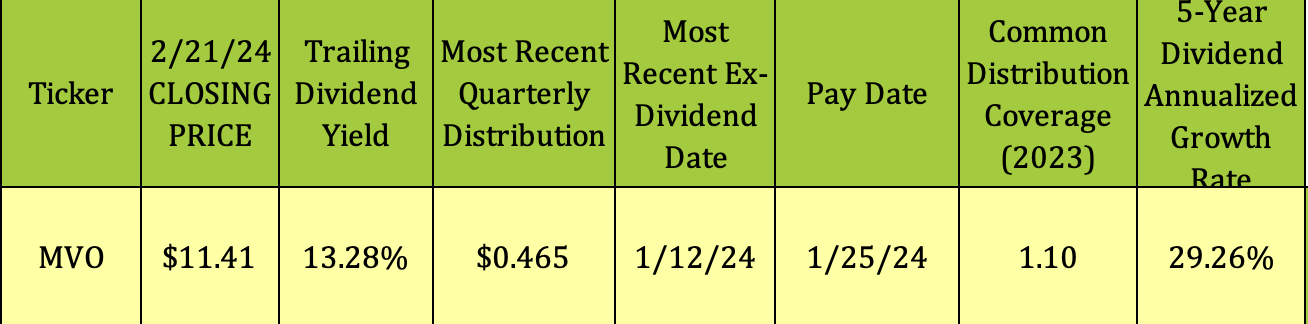

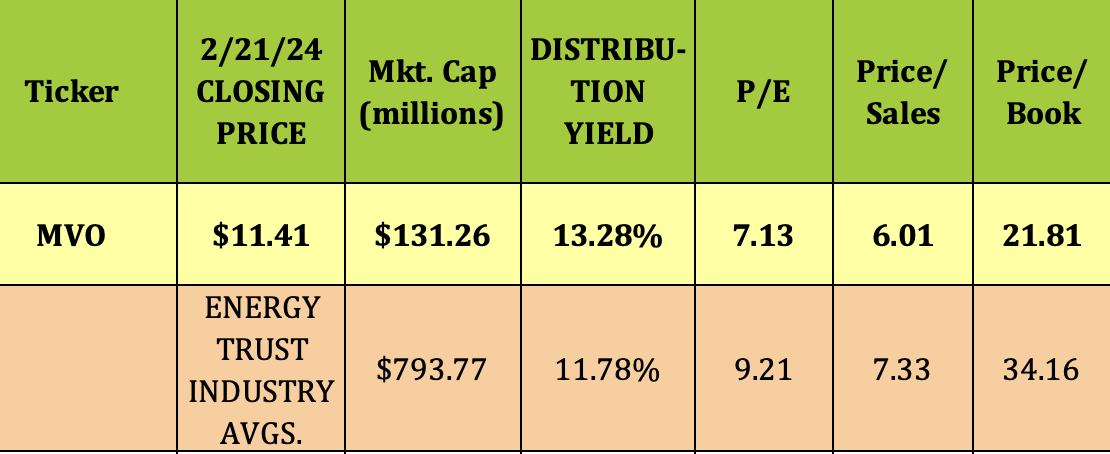

At its 2/21/24 closing price of $11.41, MVO had a very attractive trailing dividend yield of 13.28%. Its most recent distribution was $.465, which was paid on 1/25/24. MVO goes ex-dividend and pays in a Jan./April/July/Oct. schedule.

Hidden Dividend Stocks Plus

NPI/distribution coverage ran at 1.07X in 2021 and 2022, and has increased to 1.10X in 2023:

Hidden Dividend Stocks Plus

Debt and Liquidity:

MVO has no debt. However, "The Trustee may cause the Trust to borrow funds required to pay expenses if the Trustee determines that the cash on hand and the cash to be received are insufficient to cover the Trust's expenses. If the Trust borrows funds, the Trust unitholders will not receive distributions until the borrowed funds are repaid. During the three and nine months ended September 30, 2023 and 2022, there were no such borrowings. MV Partners has provided a letter of credit in the amount of $1.8 million to the Trustee to protect the Trust against the risk that it does not have sufficient cash to pay future expenses." (MVO Q3 '23 10Q)

Performance:

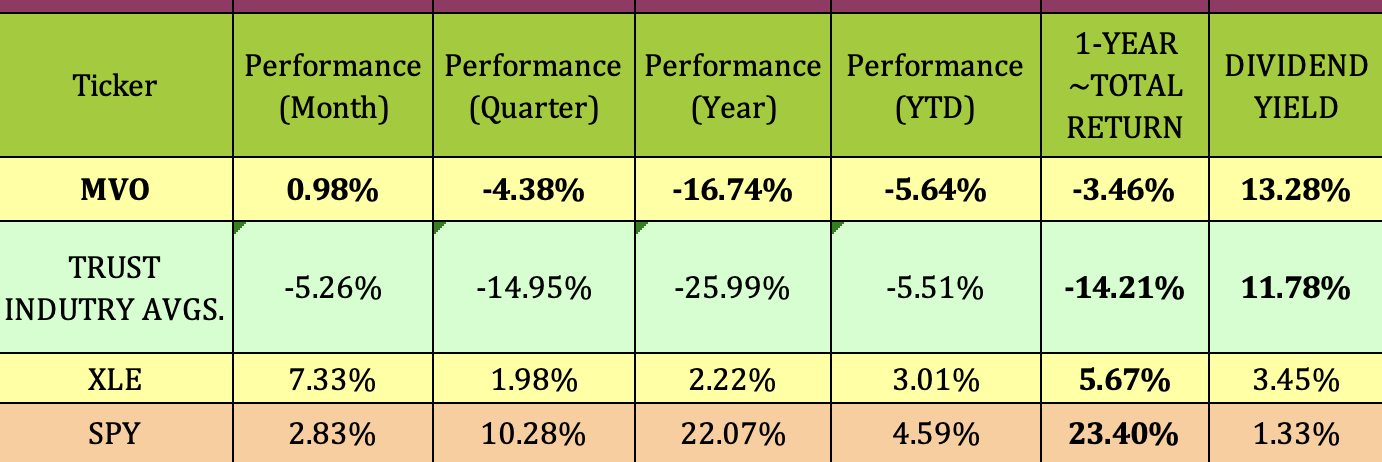

Unlike 2022, when it surged 84%, the past year hasn't been so hot for price performance for MVO and other trusts, which fell 16.7% and 26% respectively. MVO's one-year total return of -3.46% outperformed the trust industry, but seriously lagged the S&P and the broad energy sector. That lag has continued so far in 2024, with MVO down 5.6% and the Trust industry down 5.5%.

Hidden Dividend Stocks Plus

Valuations:

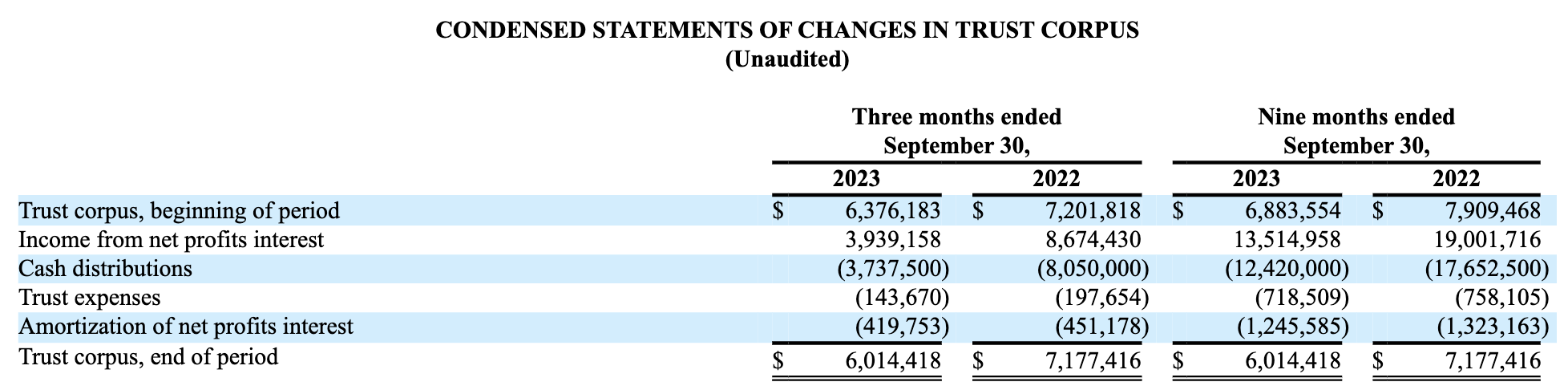

MVO's corpus, i.e. capital or principal amount, declined from $7.18M to $6.01M in the nine months ending 9/30/24.

Hidden Dividend Stocks Plus

At its 2/21/24 closing price of $11.41, MVO's trailing P/E of 7.13X is much cheaper than the trust industry's 9.21X mark. Its Price/Book and P/Sales are also lower than average.

Hidden Dividend Stocks Plus

Parting Thoughts:

As of 9/30/23, MVO had received the equivalent of 11.2 MMBoe with respect to the trust's net profits interest, up .2 MMBoe vs. 6/30/23. That's not that far from the 11.5 MMBoe stated as a trigger for termination in its SEC filings.

For that reason, we rate MVO a Hold. There's no Q4 10K filed yet, which would update the total MMBoe for NPI received as of 12/31/23.

All tables furnished by Hidden Dividend Stocks Plus, unless otherwise noted.