SimonSkafar

SimonSkafar

Almost a year ago, in late March of 2023, I ended up revisiting a company called Murphy USA Inc. (NYSE:MUSA). Through the properties that the company owns, it sells motor fuel products and convenience merchandise to customers that need it. This is not exactly an exciting industry. Furthermore, it's not a space that is likely to see a lot of growth. However, at that time, the firm had been doing really well from a revenue, profit, and cash flow perspective. Even though the 2023 fiscal year was slating up to be rather disappointing, I felt as though the stock was cheap enough to warrant significant optimism.

This led me to keep the firm rated a "buy" to reflect my view that the stock would likely outperform the broader market for the foreseeable future. So far, that call has proven to be quite successful. While the S&P 500 (SP500) has shot up 24.5% since the time that article was written, shares of Murphy USA have seen upside of 60.9%. Fast forward to today, with data covering the final quarter of the 2023 fiscal year having recently been reported, and it is clear that my stance on how the year would play out was right. Even with that, however, the stock does not look unreasonably priced at this point in time. I would argue that some additional upside likely exists. However, it is also clear to me that the easy money has been made.

For those not terribly familiar with Murphy USA, the company owns and operates a chain of retail stores that specialize in the sale of gasoline and various types of merchandise. The locations that it operates, totaling 1,733 in all and spread across 27 different states, fall under three different brand names. The first two of these are Murphy USA and Murphy Express. According to management, 1,577 of the firm's locations fall under this category. The other 156 are under the QuickChek brand name. In addition to selling its products through these locations, the firm also markets petroleum products to unbranded wholesale customers using both its own terminals and the terminals of third parties.

Author - SEC EDGAR Data

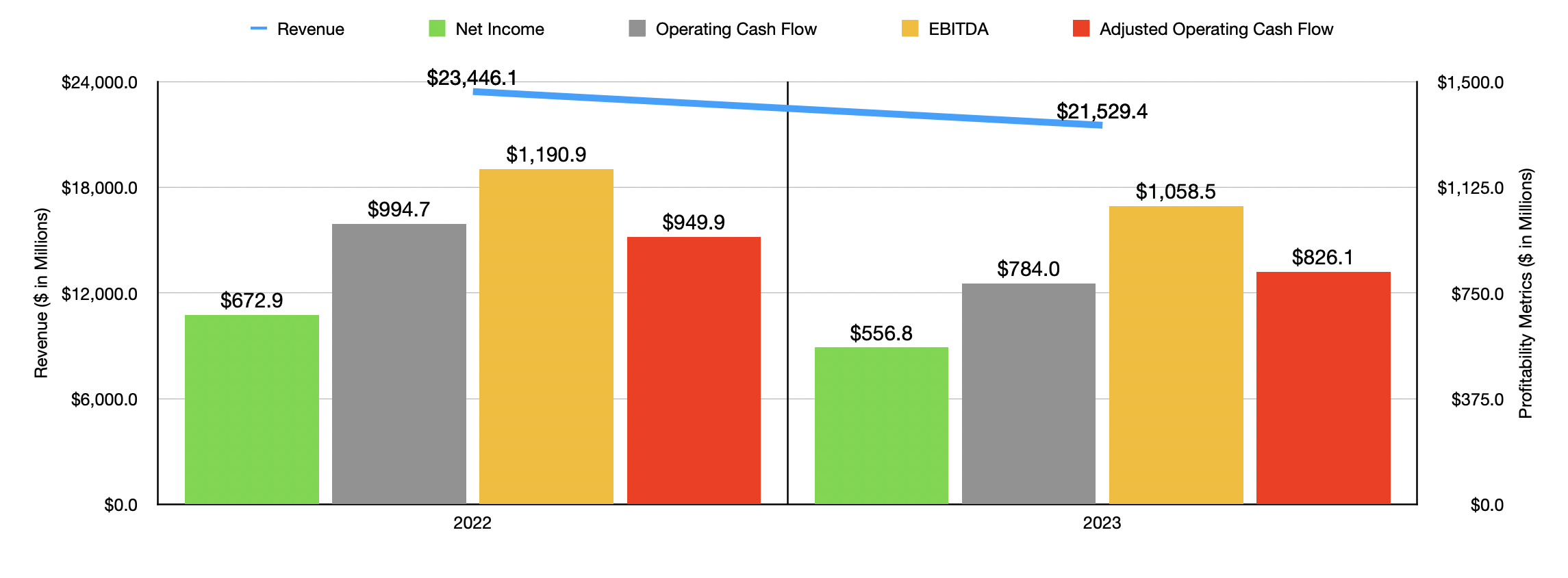

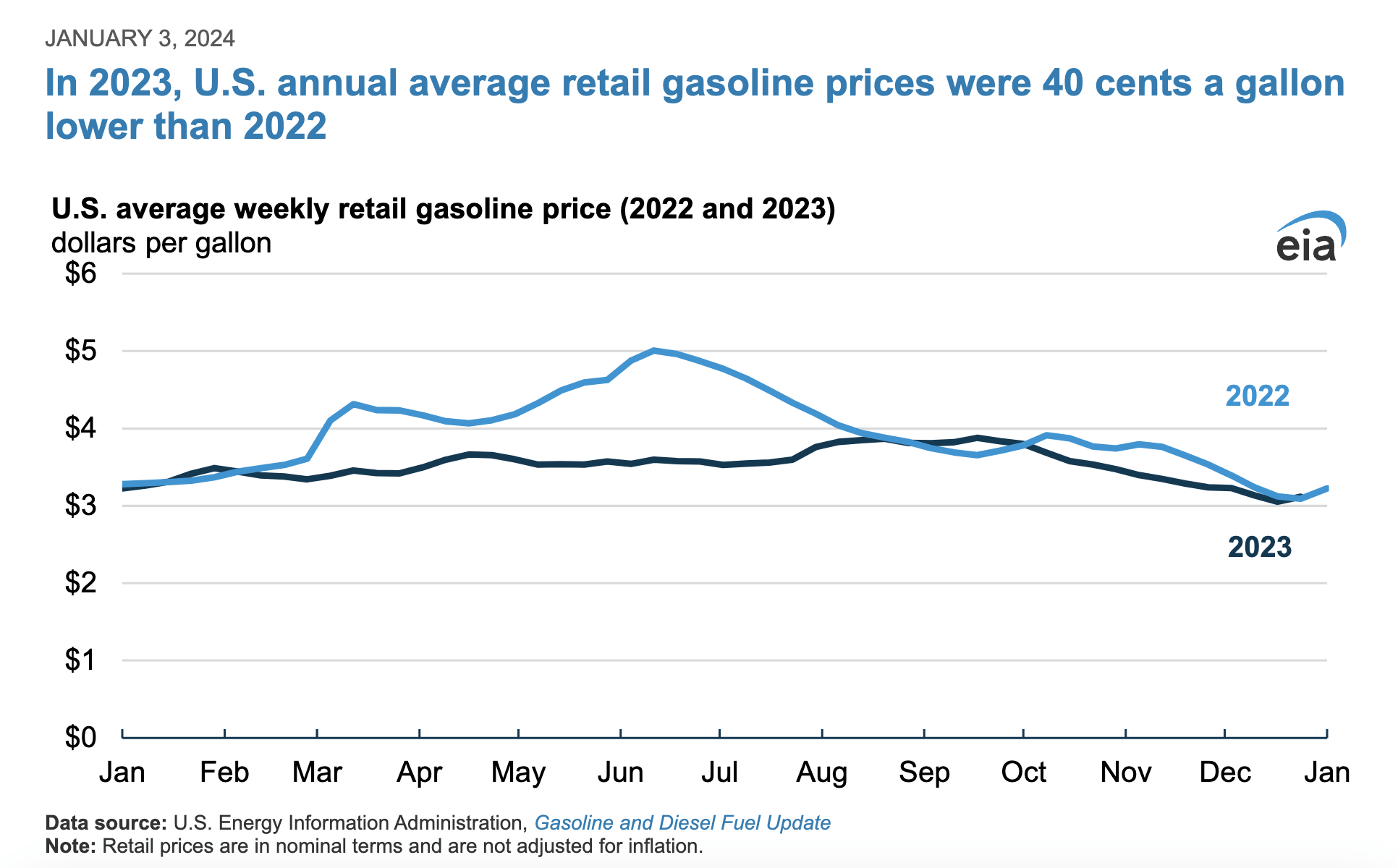

Even though the economy remained strong during the 2023 calendar year, financial results for the 2023 fiscal year for Murphy USA were not exactly great. Revenue during the year came in at $21.53 billion. That represents a decline of 8.2% compared to the $23.45 billion generated one year earlier. Even though the company enjoyed a 1.1% increase in retail fuel volumes sold and a 4.8% rise in merchandise sales revenue, it was hit by a 12.3% drop in average retail fuel prices. This drop amounted to roughly $0.45 per gallon. To be clear, there can be some rather significant differences in pricing when it comes to fuel costs in the US. But this decline largely conforms with the $0.43 per gallon drop in retail gasoline prices that the EIA calculated for 2023 relative to 2022.

EIA

This drop in revenue brought with it, unfortunately, a decline in profits. Net income dropped from $672.9 million down to $556.8 million. Other profitability metrics followed a very similar trajectory. Operating cash flow, for instance, managed to drop from $994.7 million to $784 million. If we adjust for changes in working capital, then the drop was from $949.9 million to $826.1 million. And lastly, EBITDA for the enterprise went from $1.19 billion to just under $1.06 billion.

Author - SEC EDGAR Data

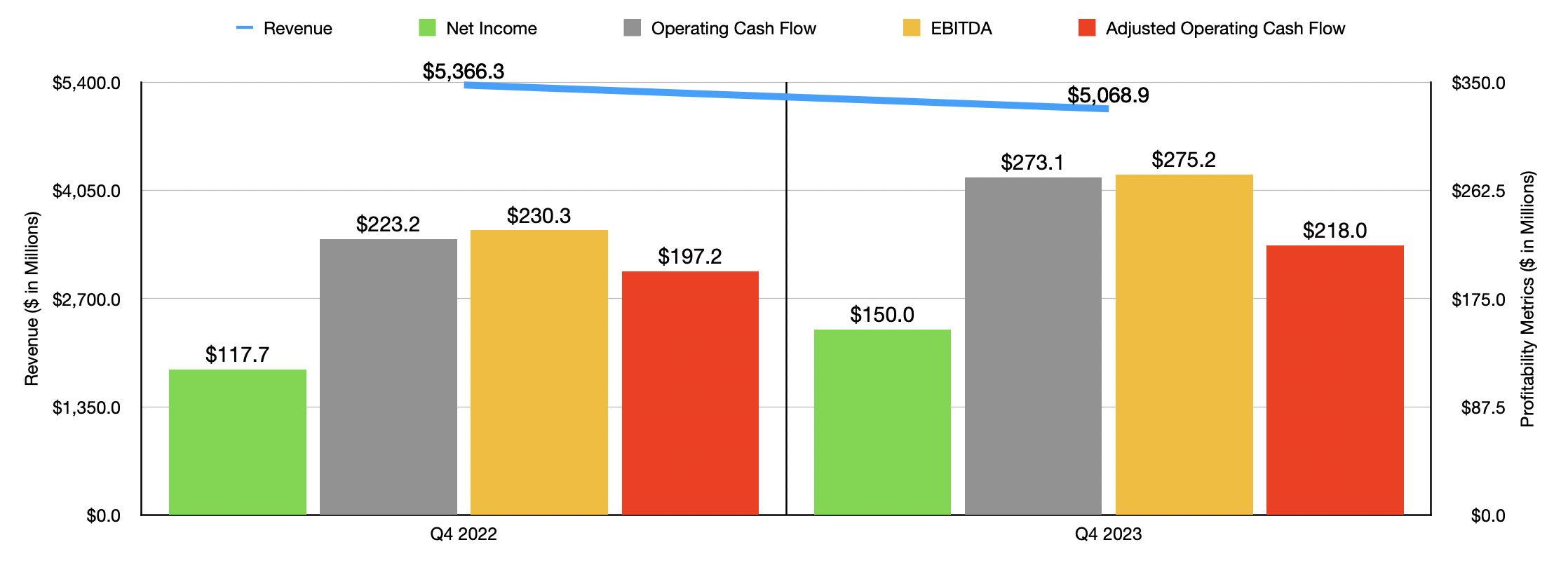

Despite the issues that the company experienced during 2023, there were some signs of improvement, at least on the bottom line, in the final quarter of the year. Even though revenue dropped from $5.37 billion to $5.07 billion, net profits jumped from $117.7 million to $150 million. There were a couple of different contributors to this bottom line improvement. For instance, selling, general, and administrative costs went from $81.7 million down to only $62.1 million. In addition to this, merchandise costs relative to the revenue they brought in fell from 80.9% of sales to 80.6%. Even larger than this was a reduction in the cost of petroleum products from 92.9% of the revenue they brought in to 91.4%. As the chart above illustrates, the company's net income was not the only profitability metric to experience an improvement. Operating cash flow, adjusted operating cash flow, and EBITDA also improved year over year.

Even though Murphy USA experienced pain for the year as a whole, management continues to allocate capital in a way that I would consider to be positive. During the year, management allocated $336.2 million toward buying back stock. But I doubt that management is done in that regard. At present, the firm has another $1.4 billion in capacity under its share buyback program. For a business with a market capitalization of $8.37 billion as of this writing, that represents a rather significant number of the shares currently outstanding.

Murphy USA

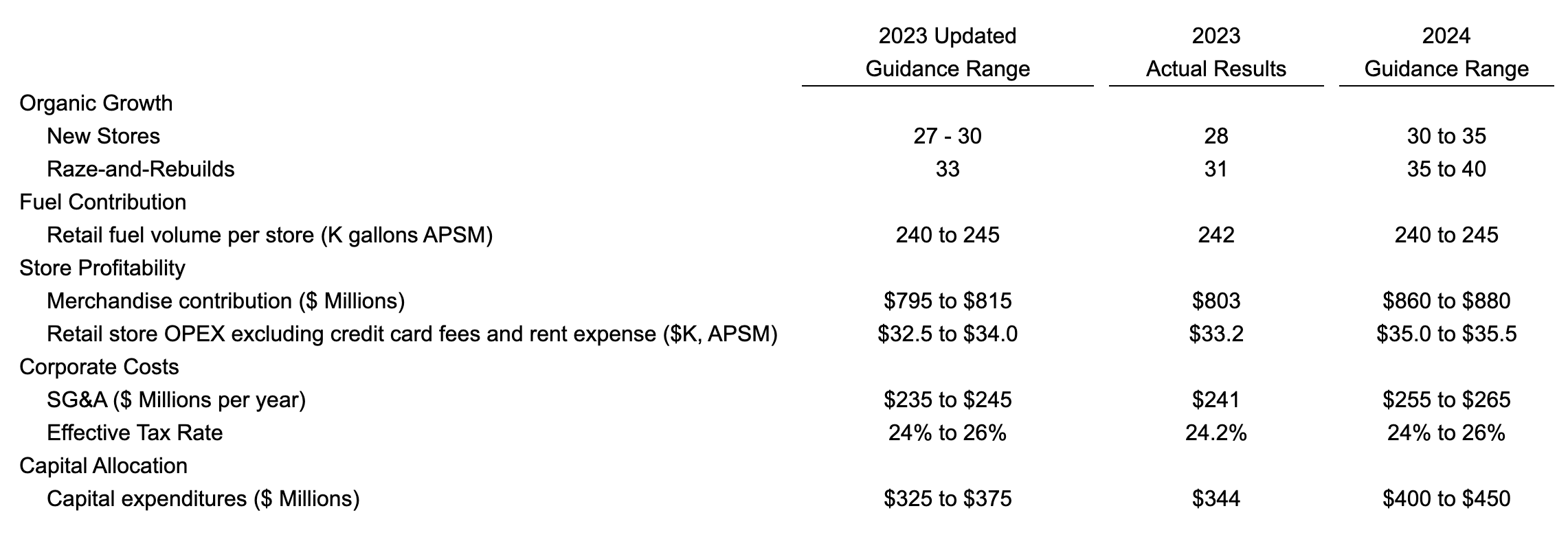

Generally speaking, I prefer that companies allocate capital toward growth as opposed to buying back stock. But when shares are attractively priced, buying back stock makes sense. None of this means, however, that Murphy USA is no longer focused on growth. During the 2023 fiscal year, the company added 28 new stores to its network. This was in addition to 31 stores that they tore down and rebuilt. In total, these developments, combined with any other capital requirements, cost shareholders $344 million. For 2024, the company intends to up the game. The expectation is to spend between $400 million and $450 million. That should allow for the opening of 30 to 35 additional locations. On top of this, the company will tear down and rebuild another 35 to 40 locations if all goes according to plan.

Author - SEC EDGAR Data

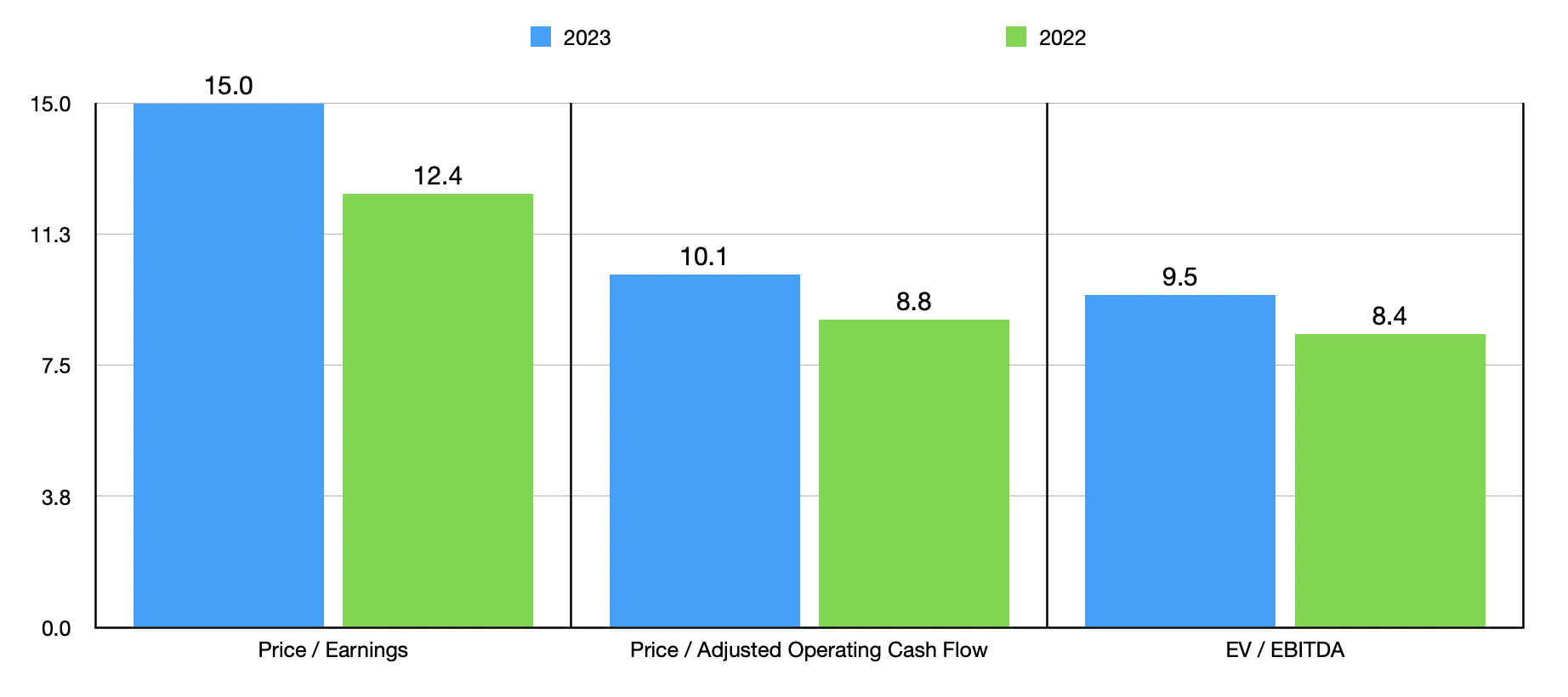

Even without growth, I would argue that shares likely have some additional upside to them. In the chart above, you can see how the stock is priced using data from both 2022 and 2023. Even with the more depressed 2023 figures, shares look to be perhaps undervalued or, at worst, around fair value. Unfortunately, comparing the company to similar firms really is a challenge given the nature of the business. Many of the other operators are subsidiaries that are privately held that are owned by large publicly traded energy companies. And not long ago, TravelCenters of America, which was probably the best publicly traded comparable, was taken private. But as a general rule of thumb, price to operating cash flow and EV to EBITDA multiples of around 10 or lower are typically appealing.

Recently, the fundamental picture for Murphy USA has not been perfect. The company has been faced with top line and bottom line weakness. However, data from the final quarter of the 2023 fiscal year does seem to suggest that the bottom line issues are easing. Management continues to grow the business while using significant amounts of cash to buy back stock at levels that are fundamentally attractive.

All combined, this paints a picture of Murphy USA Inc. that, in my mind, is rather positive. It is true that the easy money has been made by this point. However, I wouldn't be surprised to see a bit of additional upside. For investors who don't mind hanging on for a bit longer, I think that a soft "buy" rating is logical.