Jeremy Poland

Jeremy Poland

Murphy Oil (NYSE:MUR) recently announced a roughly 10% dividend increase. This is the second year in a row that the dividend has increased at that pace. Murphy Oil now has a portfolio of projects that enables them to take chances finding an elephant while repaying debt and increasing the dividend. The strategy here is different from the usual return of capital to shareholders in that the search for elephants cost money. But this very profitable company also has that "homerun" chance that many higher yield upstream competitors do not have.

For a number of years, I covered Murphy Oil in the process of shuffling the portfolio. Not only did this make for a very complicated analysis, but it also was hard to tell if the company was growing. Whenever a company does a major disposal, comparisons are hard because the disposed operations are immediately discontinued. Meanwhile, any acquisitions that replace those discontinued operations only count in results from the present forward. This whole process for a company like Murphy (which bought and sold several divisions) made analysis next to impossible.

Underpinning all of the strategies is a very profitable (generous cash flow) operation.

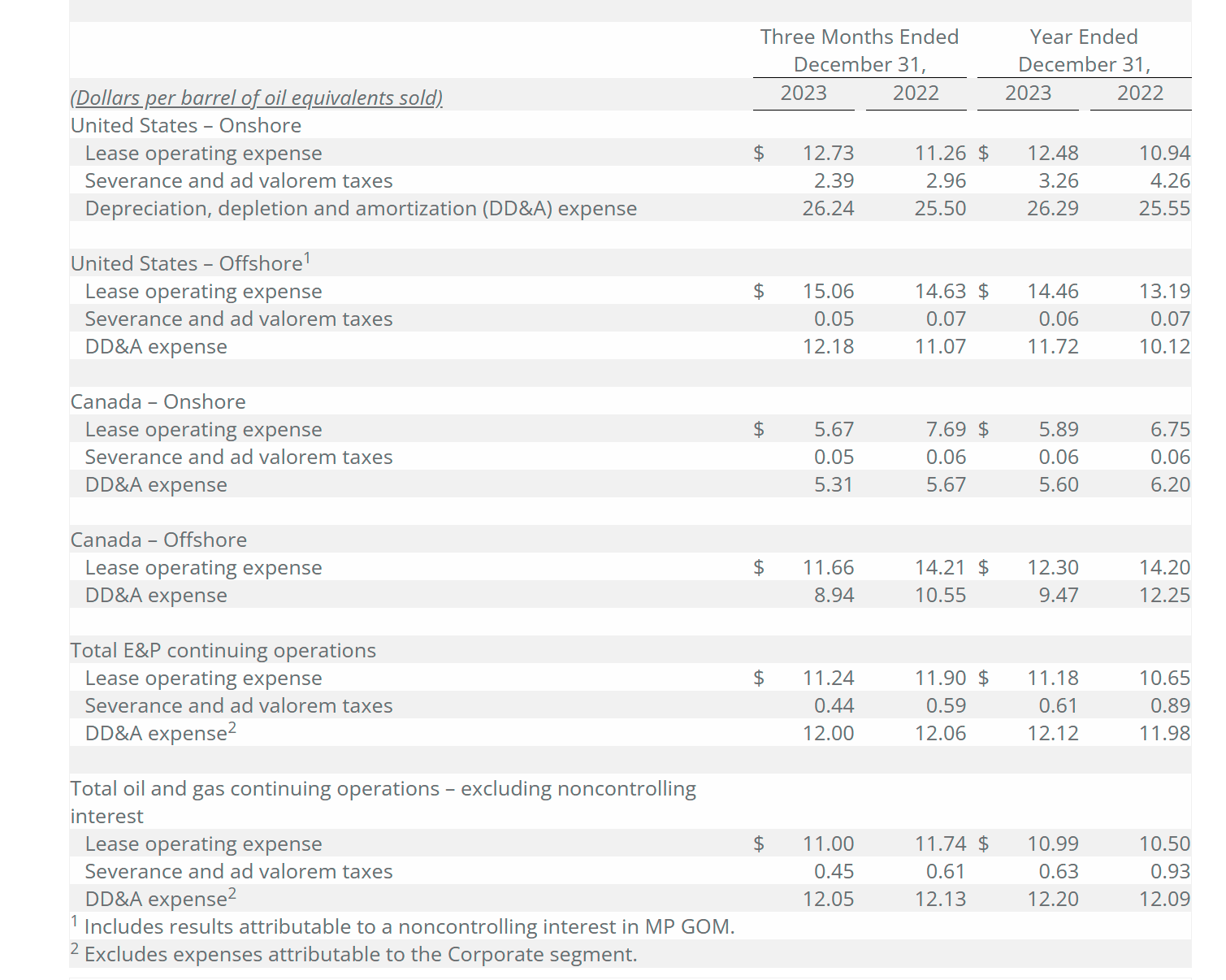

Murphy Oil Fourth Quarter 2023, Project Production Cost Comparison (Murphy "Oil Fourth Quarter 2023, Earnings Press Release)

As shown above, the offshore operations are extremely profitable. Management has been very adept at handling the offshore risks to obtain the low costs shown above. Once a successful project is underway, those projects have the very low costs shown above. Those costs imply a very low breakeven point and even generous cash flow when much of the industry is suffering losses and struggling through a time of weak prices.

Too many players "bet the company" with the result they end up with no cash. That means a lot of capital raises until there is a sufficient cash flow project or a lot of debt that often dilutes or wipes out shareholders.

Oftentimes, management does this by selling participation in the riskiest ventures while keeping a larger share of the later development wells that follow any success.

Murphy is a relatively small offshore player. The offshore projects generally require a lot of cash up front. Therefore, the strong balance sheet that is evident with this company comes from a far above average talent for minimizing that offshore risk.

This is one of very few companies I follow that breaks down the costs by project. Managements that do this often resolve cost issues because they acknowledge any cost issues to shareholders quarterly. There are plenty of other managements that hide high-cost production into the average cost reported because that average is the only cost reported. That will not be happening here.

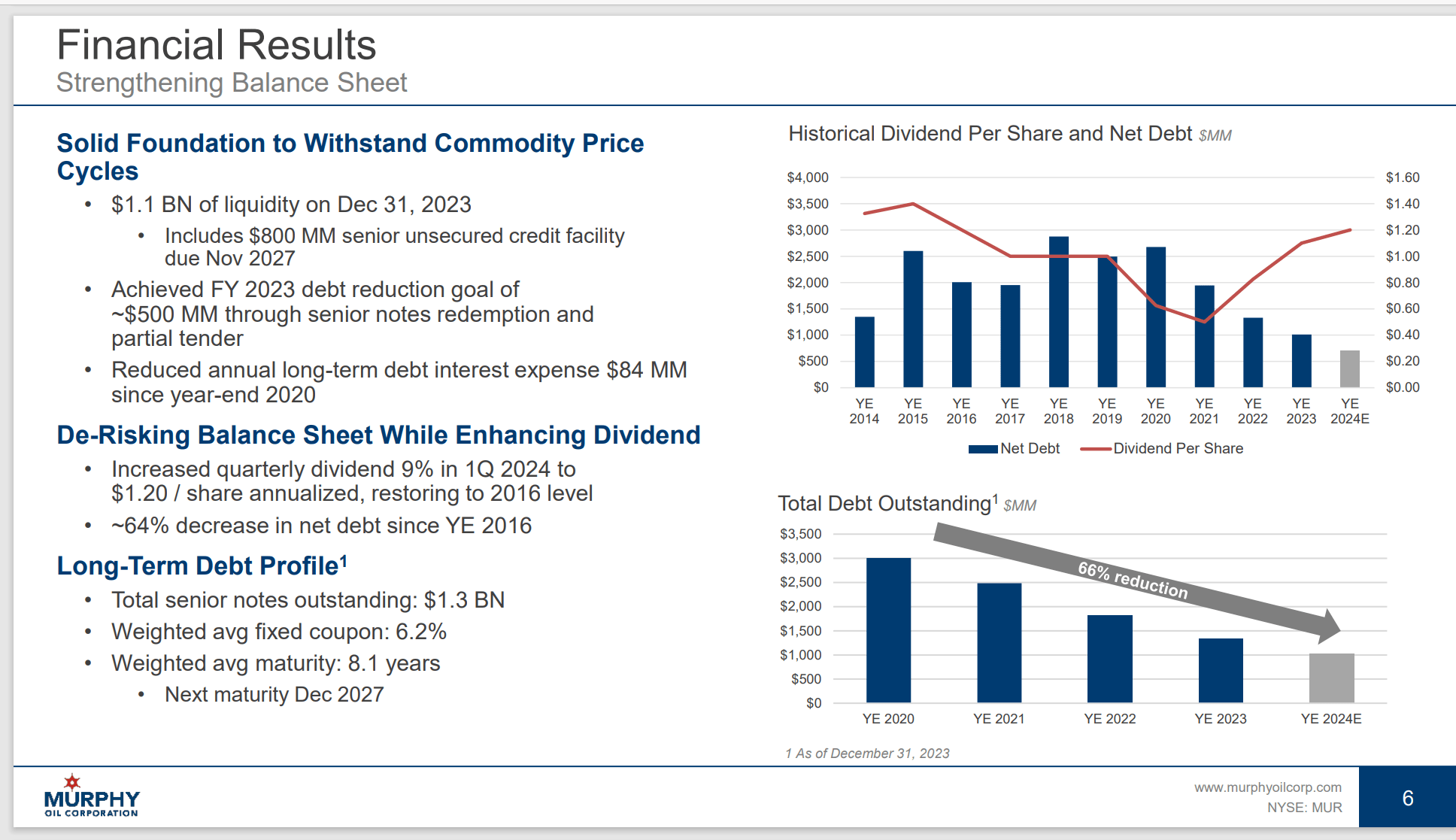

Murphy Oil has one of the lowest debt ratios in the industry.

Murphy Oil Debt Progress and Dividend Restoration Progress (Murphy Oil Fourth Quarter 2023, Earnings Conference Call Slides)

This company is extremely flexible when it comes to buying and selling chunks of the company. The finances need to have considerable room for any deal that may come along. Hence, the very low debt compared to the cash flow.

The other consideration is that should a major discovery happen offshore, it is often 5 to 7 years before that discovery produces cash flow. Such a major project needs financing ability. As shown above, this company clearly has that ability.

When I followed Hess Corporation (HES), that company for years sold assets until, the Guyana project produced sufficient cash flow to finance itself and later return some cash to the partners.

Murphy Oil appears to be in a financial position to finance such a project from its cash flow and credit line.

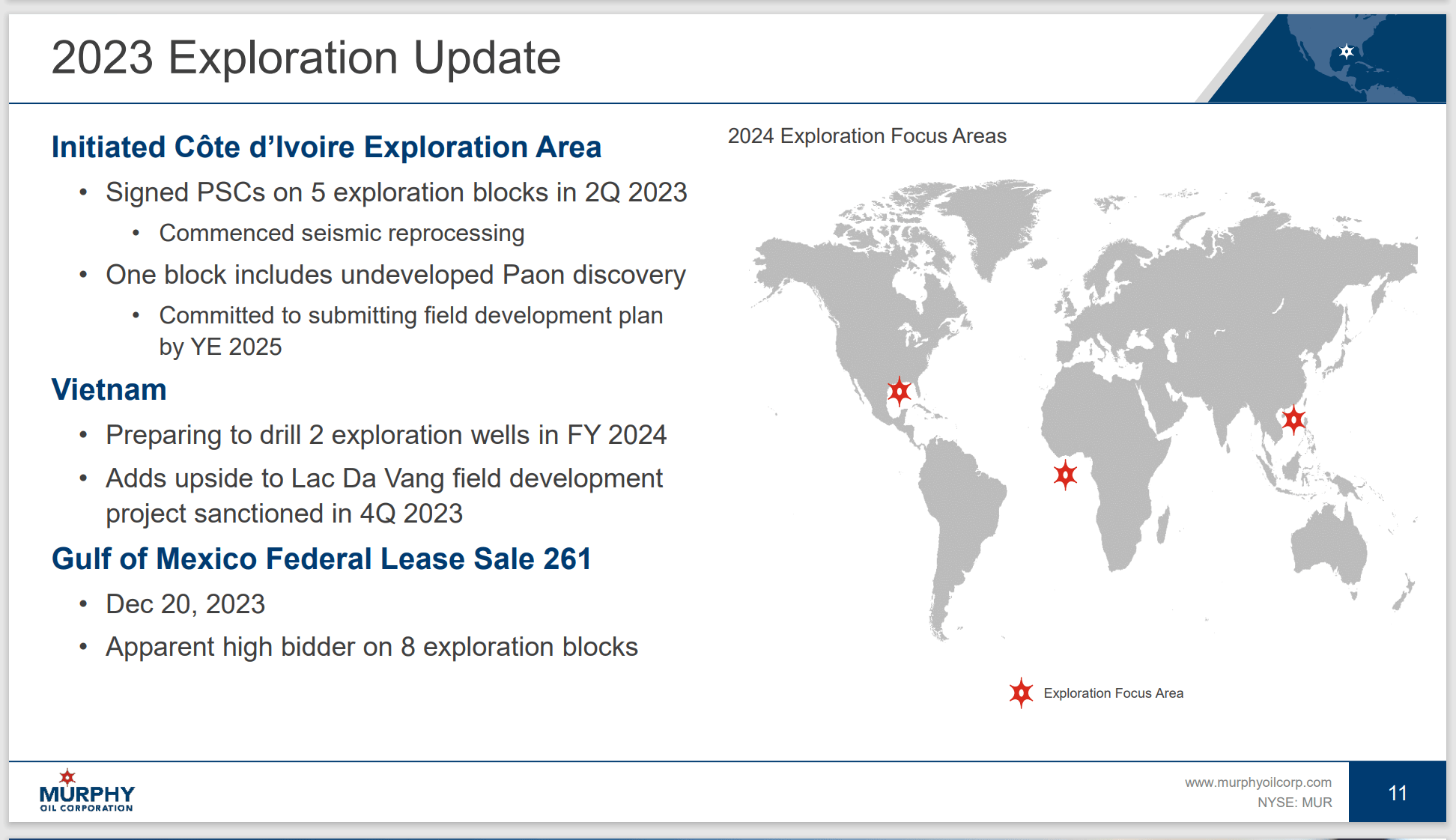

Murphy has several promising projects that have a drilled discovery. Investors should keep in mind that oftentimes a discovery by itself is not sufficient to justify production offshore. Instead, it often takes more follow-up wells to prove that there is sufficient oil to justify an offshore platform. Not all fields have as much development as the Gulf of Mexico. Therefore, many of these exploration places require considerably more oil in place to justify development.

Murphy Oil Exploration Projects Heading Towards Possible Development And Production (Murphy Oil Corporation Fourth Quarter 2023 Corporate Presentation)

Management was awarded some Gulf of Mexico leases. Those leases are likely lower risk than is the case with some of the other projects listed above. The reason is that the Gulf of Mexico has considerable production history. Therefore, leaseholders have a better record of finding production than is the case for pure exploration.

The Africa project already has a discovery well with production in a neighboring country. So, the strategy to lower risk is similar to the Gulf of Mexico. Explorers are a little more likely to find oil when there is already nearby production. This is yet another strategy to lower exploration risk when drilling costly wells.

Note that the latest presentation goes into more detail on both of these projects. There is not much change as both of the (Africa and Vietnam) projects will take some time.

Note that management did not update anything in Brazil. Much of what management holds in Brazil is in the very early stages of exploration. The wells are expensive and higher risk as well due to the lack of nearby operating history (though several leases do have nearby production or discoveries). Brazil is there going to take some time, even decades, before any tangible results are obtained.

Murphy Oil is a smaller offshore player (with onshore production to help finance the offshore business) that manages to reduce risk such that a strong balance sheet is maintained at all times.

Murphy recently announced the promotion of Eric M Hambly to Chief Operating Officer from his Executive Vice Presidentlal Position (Operations). At the same time, Mr. Ted Botner became an Executive Vice President while maintaining his roles of Corporate Secretary and Legal Counsel. Both people are career Murphy executives that likely will take on some tasks from Mr. Jenkins the CEO. Other than that, investors will not really see a major change.

This company offers the chance of finding an elephant while at the same time paying a dividend, reducing debt, and growing production from existing projects. That means the dividend will be smaller with this company. But the speculative and established upside potential is greater.

Investors probably can expect considerable variance in future dividend increases depending upon the timing of some of these significant projects. But that dividend is likely to grow at an above-average rate unless there is another 2015-2020 period (with all the challenges in that period).

This is a typical upstream company that is dependent upon oil and gas prices. Risks would include the loss of an essential senior manager or key employee. There is also a possible lack of exploration success or the miscalculation that leads to a large development project with insufficient profitability.

But overall, this company is an excellent risk manager so far (there is also a risk this can change in the future to the detriment of shareholders).

The stock remains a strong buy on good solid financials and growth prospects. There is also a reasonable chance that the company may find that "homerun" offshore find at some point in the future. That requires patience. But as the dividend increase shows, there is plenty else to like here while the investor waits.