AzmanJaka

AzmanJaka

In my previous coverage on Matterport (NASDAQ:MTTR), I recommended a hold rating as I wanted to wait for the real estate headwinds to be cleared before investing. My belief was that this headwind would turn into a growth tailwind as the economy recovered, which could drive valuations upward. Until then, I believed it was better to just monitor the business performance. This post is to provide an update on my thoughts on the business and stock. I am upgrading my rating from hold to buy as I turn bullish on the MTTR growth outlook and the fact that the real estate end market showed >20% growth, easing my previous concerns.

MTTR's total revenue for 4Q23 was $39.5 million, a 4% y/y decline that was slightly lower than the midpoint of guidance. The key driver was subscription revenue of $23.7 million, which was up 23% y/y. Net new ARR growth accelerated to 18% y/y growth vs. 15% y/y growth seen in 3Q23, and ARR came in at $94.7 million, up 23% y/y. Also positively, the NRR (net rental rate) increased to 109%, which is the greatest level in two years and near the 110% historical average for the company.

The equity narrative for MTTR is gradually shaping towards my expectations. According to management, the top-line strength is diverse, including an increase in new subscribers, an expansion of current subscribers, and the positive impact of the price increases implemented in mid-2023. Organic growth drivers—both paid and free subscribers—also experienced healthy y/y growth of 13% and 36%, respectively. ARPU also increased to $1.32k (annual pricing), up 9%, as a result of both an upmarket shift and the expansion of current subscribers. The strong demand was felt across all business sizes, where SMB and enterprise cohorts improved, both growing >20%, which signifies a healthy demand backdrop (and not one-sided to large enterprises, for instance, which would’ve suggested weakness persists in the SMB market). Importantly, one of the key concerns I highlighted previously was that residential real estate and non-residential real estate verticals were also both up >20%. On a more specific note, management highlighted the construction, facilities management, and travel and hospitality markets' ongoing strengths.

I am also becoming more optimistic on MTTR’s medium-term growth outlook. NRR increased for a second consecutive quarter, going up from 106% in the previous quarter and 103% in 4Q22, and half of the NRR expansion is due to natural expansion which sets a baseline expectation for NRR moving forward. In other words, NRR could sustain at mid-single-digits percentage (low-single-digits percentage from natural expansion + inflation-like pricing growth). In my opinion, natural expansion should not be an issue, MTTR has spent the last year honing in on its most valuable customers and developing deeper relationships with them. The company is now concentrating on making the same work for its smaller, long-tail customers. This should lead to more growth in NRR, bringing it closer to the historical average of 110% and maybe even beyond. Furthermore, MTTR has been establishing important partnerships with companies like Autodesk (ADSK), Amazon Web Services (AWS), and Procore (PCOR) over the last several quarters, and it appears that the company will soon be able to benefit from these relationships. Following a period of co-marketing that contributed to new business acquisition in FY23, the partnership relationships are now shifting to incorporate more co-selling this year. Management claims that they are witnessing robust pipeline development with these important partners, and that this channel will likely become an even more significant growth driver in FY24. As such, I see this as a key upside catalyst to growth acceleration. The release of AI features in FY24 is another encouraging aspect. Although the practicality of these features is debatable, I believe they will allow MTTR to increase prices and, perhaps, pave the way for additional add-on modules that could boost ARPU even further.

Profitability-wise, 4Q23 subscription gross margins increased sequentially once more as the business finished the current phase of cost optimizations for cloud hosting and customer service and took advantage of recent price increases. Although the actual 4Q23 EBIT margin was -43%, which was lower than the consensus estimate of -39%, the main reason for the discrepancy was the poor product gross margin, which was caused by the ongoing promotional pricing that began on Black Friday and Cyber Monday and continued all the way until the end of the year. Profitability should improve in the medium term, in my opinion, as MTTR continues to witness strong revenue growth and improve sales efficiency following the company's restructuring last year.

Own calculation

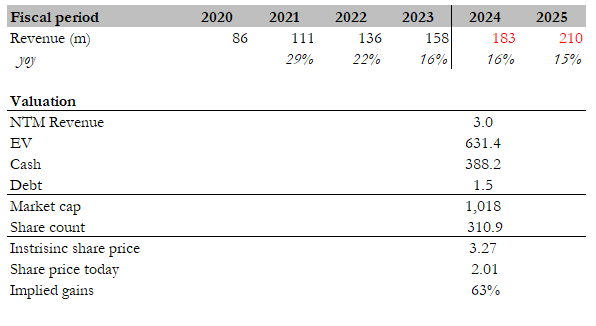

My target price for MTTR based on my model is $3.27. Relative to my previous model, my growth assumptions have gone up by 100bps in FY24 to reflect the high end of management guidance ($183 million). That said, as I discussed above, if the partnership with various key players results in more deals than expected and the rollout of features drives more adoption than expected, MTTR could beat this guidance. For FY25, I am sticking to my 15% growth assumption. I am also holding on to my 3x forward revenue assumption as the market is unlikely to rerate the valuation higher unless growth accelerates. With these assumptions, the upside remains attractive as the stock price has come down since last August (my last coverage).

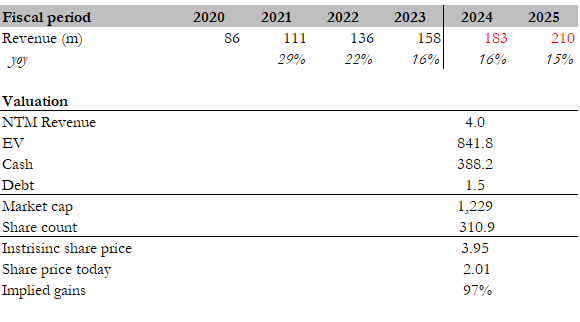

The interesting point that readers need to note here is that I am not assuming growth to accelerate in FY25, which could very well happen based on the catalysts I mentioned above and the fact that MTTR is going to turn their attention to penetrate the smaller customers to drive expansion. Any form of acceleration to the mid-teens or above 20% will very likely drive valuations upward. If we assume it goes up to 4x, the upside becomes a lot more attractive.

Own calculation

My worry is that the path to turning profitable might be delayed if management decides to reinvest in the business, and this is likely to happen if the economy recovers and management sees underlying demand accelerate. This could disappoint investors that are expecting the business to turn profitable (on an EBITDA basis); consensus is expecting this by FY25, causing them to sell their holdings and putting pressure on the stock. Another mini-red flag is that MTTR only saw 1K net additions to paid subscribers, down from 2K/2K/3K in 3/2/1Q23, which could suggest some form of headwinds that I am not aware of. If this deceleration turns for the worst, it could trigger a very negative narrative for the stock.

I am upgrading my rating on Matterport from hold to buy, driven by a more promising growth outlook and positive developments in the real estate end market. At the topline, organic growth drivers are healthy, indicating a strong demand environment. NRR should continue to sustain or potentially increase as MTTR shifts focus to capture opportunities from smaller customers, and also growth could see further upside as it reaps benefit from strategic partnerships and rolling out of new AI features. However, potential delays in profitability and unforeseen headwinds impacting subscriber growth remain risks to consider.