Materialise NV Just Beat Analyst Forecasts, And Analysts Have Been Updating Their Predictions

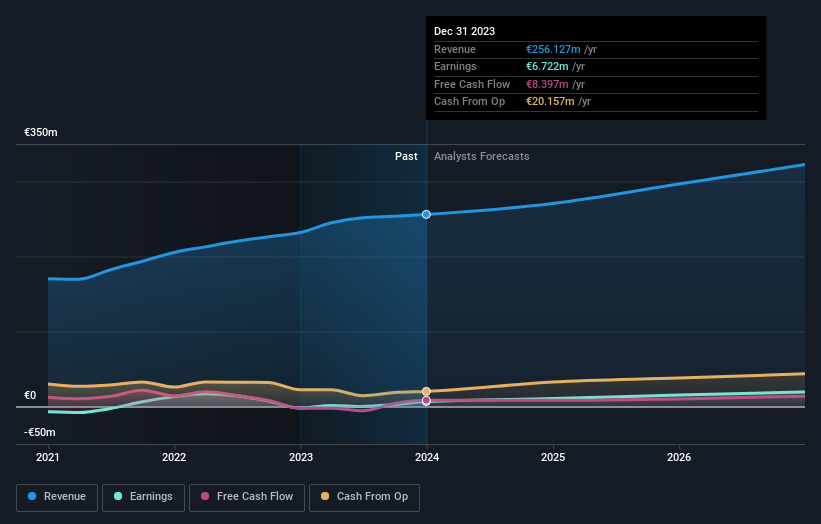

Shareholders might have noticed that Materialise NV (NASDAQ:MTLS) filed its yearly result this time last week. The early response was not positive, with shares down 4.1% to US$5.63 in the past week. Revenues were €256m, approximately in line with whatthe analysts expected, although statutory earnings per share (EPS) crushed expectations, coming in at €0.11, an impressive 267% ahead of estimates. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. With this in mind, we've gathered the latest statutory forecasts to see what the analysts are expecting for next year.

View our latest analysis for Materialise

After the latest results, the two analysts covering Materialise are now predicting revenues of €270.7m in 2024. If met, this would reflect an okay 5.7% improvement in revenue compared to the last 12 months. Per-share earnings are expected to bounce 58% to €0.18. Before this earnings report, the analysts had been forecasting revenues of €280.7m and earnings per share (EPS) of €0.10 in 2024. Although the analysts have lowered their revenue forecasts, they've also made a considerable lift to their earnings per share estimates, which implies there's been something of an uptick in sentiment following the latest results.

The analysts have cut their price target 9.0% to US$11.16per share, suggesting that the declining revenue was a more crucial indicator than the expected improvement in earnings.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. It's pretty clear that there is an expectation that Materialise's revenue growth will slow down substantially, with revenues to the end of 2024 expected to display 5.7% growth on an annualised basis. This is compared to a historical growth rate of 7.2% over the past five years. By way of comparison, the other companies in this industry with analyst coverage are forecast to grow their revenue at 12% per year. So it's pretty clear that, while revenue growth is expected to slow down, the wider industry is also expected to grow faster than Materialise.

The Bottom Line

The biggest takeaway for us is the consensus earnings per share upgrade, which suggests a clear improvement in sentiment around Materialise's earnings potential next year. On the negative side, they also downgraded their revenue estimates, and forecasts imply they will perform worse than the wider industry. Even so, earnings are more important to the intrinsic value of the business. Furthermore, the analysts also cut their price targets, suggesting that the latest news has led to greater pessimism about the intrinsic value of the business.