onurdongel

onurdongel

The last few weeks have been very difficult for shareholders of steel manufacturer United States Steel Corporation (NYSE:X). After seeing shares peak at $50.20 earlier in the year as optimism swirled around the prospect of the company being able to complete its transaction with Nippon Steel Corporation (OTCPK:NISTF, OTCPK:NPSCY) whereby Nippon has been expected to pay $55 per unit, or $14.1 billion on an equity value basis, to absorb the American steel behemoth, shares have since declined. As of this writing, they are trading at $38.87. That marks a 22.6% decline from their 52-week high.

This plunge comes as the company faces significant scrutiny. Not only is it going to have to contend with an antitrust investigation, but it will also face a national security review and it is facing pushback from politicians on both sides of the aisle in the U.S. While I still believe that it is likely the transaction will be completed more or less as agreed upon, there is certainly a probability, and a decent one at that, that the deal will fall through. For those who are long the stock like I am, this would be undesirable.

But given how far the stock has already fallen, it's difficult to imagine much further downside from where shares are priced at the moment. This creates a favorable risk-to-reward scenario that justifies, in my mind, an upgrade from the "buy" rating I assigned it back in the middle of December of last year to a "strong buy" today.

Even before United States Steel announced that it had struck a deal whereby it would be acquired by Nippon Steel in exchange for $55 per share, there were significant concerns that any major transaction might be impossible. Another major American producer, for instance, could prove to be a problem because of antitrust concerns. In addition to there being antitrust concerns when it comes to a foreign producer picking up the business, there are also concerns regarding national security. Sticking purely with the antitrust side of things, successfully absorbing United States Steel would turn Nippon Steel into the third largest steel manufacturer on the planet with around 65 million metric tons of output per annum and 86 million tons of production capacity each year.

Probably the biggest challenge to overcome on the antitrust front will be the 50% joint venture that Nippon Steel has with ArcelorMittal S.A. (MT) in Alabama. Located about 35 miles north of Mobile, Alabama, the two firms have had joint ownership of the steel processing facility since 2014. It boasts about 5.3 million tons of flat-rolled carbon steel products annually. To put this in perspective, United States Steel has a total annual steel production capacity of about 22.4 million tons, 17.4 million tons of which are in North America. Its total flat-rolled production capacity is about 13.2 million tons per annum.

So, the facility located in Alabama is truly massive. It is highly probable that if Nippon Steel were to divest its 50% ownership in the joint venture, the most significant barrier on the antitrust side of the equation would be resolved. And in February of this year, its partner in the venture, ArcelorMittal, hinted that an ownership change regarding that facility might be possible.

Historically speaking, or at least since the end of World War 2, Japan has been a friendly nation to the United States. If the acquirer were a Chinese business, the probability of a transaction occurring would be very close to zero. But that's not the case.

Having said that, this does not mean that the company can make a transaction occur without going through tremendous scrutiny. Even if Nippon Steel can avoid antitrust concerns, the transaction still has to undergo a CFIUS Review. CFIUS stands for Committee on Foreign Investment in the United States. Originally created in 1975 by means of executive order, a CFIUS Review is a process whereby a committee is formed of representatives from certain executive agencies and departments within the U.S. government. Over time, this committee has become more relevant and more powerful, resulting in potentially long investigations to see the extent to which transactions involving foreign parties might put national security at risk.

This process was further expanded by executive order in 2022 by President Joe Biden. Essentially, a CFIUS Review must now take into consideration several factors, including supply chain resiliency issues, technology, cybersecurity, data security, and more. Complete deal blockages are incredibly rare, but not unheard of, and the ones that do occur almost always involve Chinese firms. In the event that the CFIUS Review does recommend that the deal is killed, President Biden would be highly likely to follow through with the recommendation. I say this because, in a press release issued on March 14th, President Biden mentioned that "it is vital for it (United States Steel) to remain an American steel company that is domestically owned and operated." However, he did specify earlier in the statement that he has the backs of the steel unions.

On the same day that announcement was made, the United Steelworkers union applauded President Biden's statement on the matter. The union previously bashed Nippon Steel, accusing it of not operating in good faith and not formally incorporating promises that it had made into existing contracts. For its part, Nippon Steel has come out and said that they believe that they will pass all regulatory requirements in order to make this transaction occur. In the event that they are unable to pass a CFIUS Review, they even agreed to pay United States Steel a termination fee of $565 million (though there are some scenarios where United States Steel could be required to pay that fee to Nippon Steel).

Regarding union negotiations, they even made sweeping promises not to cut any jobs or close any facilities in the US. They have promised to make significant investments aimed at boosting shareholder value and have even said that they will uphold any contracts that exist with the unions. They even intend to keep the name of the company the same while also keeping the firm's headquarters in Pittsburgh while simultaneously moving the U.S. headquarters of Nippon Steel to Pittsburgh as well. At present, those headquarters are located in Houston. Despite these promises, the United Steelworkers does not believe that the company is being honest.

I am no lawyer, but I would make the case that if Nippon Steel can resolve the antitrust concerns by divesting itself of its 50% ownership of the aforementioned joint venture with ArcelorMittal, and if it can appease the unions that represent its employees, then a transaction is highly likely to proceed. This is in spite of pushback from both sides of the political aisle that has seen both Republicans and Democrats urge the deal to be scuttled. Even former President Donald Trump, who has developed the image as being business-friendly, has promised to destroy the deal as soon as he comes into office if he is elected in November of this year. But only time will tell what will transpire.

Back in the middle of August of last year, I started building what ultimately became a pretty substantial position in United States Steel. As with most of my positions, I gradually built it over time. The lowest price I paid for shares was $30.72, while the highest came from a batch that I bought on March 13th of this year for $41. All told my weighted average purchase price is $33.56. In theory, shares of the company could plunge to that point or lower compared to the $38.87 that they are currently trading at. So in that respect, there is a possible downside from here. I would argue, however, that such a downside is limited.

Author - SEC EDGAR Data

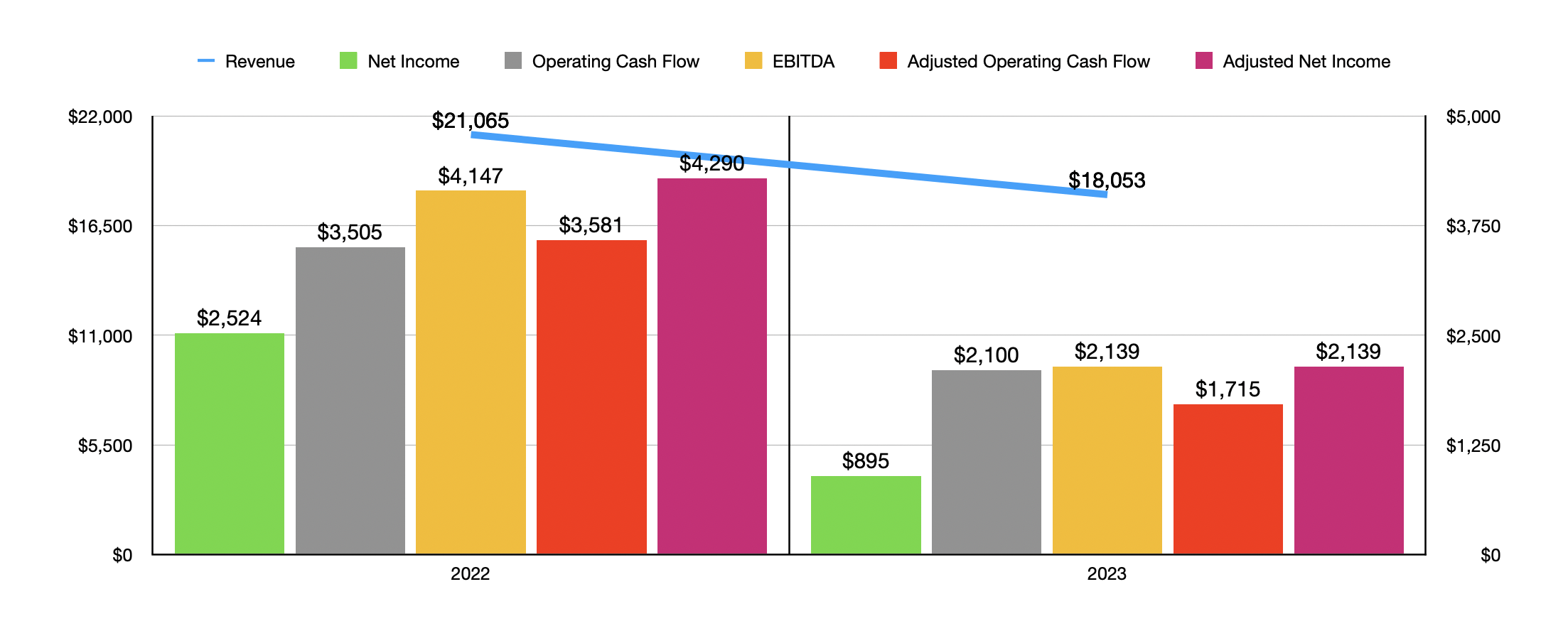

Obviously, the bullish scenario would see the transaction with Nippon Steel be completed as agreed upon. But if that does not come to fruition, the company looks rather attractive. In the chart above, you can see financial performance for both 2022 and 2023. Revenue, profits, and cash flows, all declined year over year. This was in spite of the fact that the overall volume for most steel products produced by the company increased year over year. Flat-rolled products saw volumes rise by 3%. Mini mill volumes shipped grew by 6%. And USSE products grew by 3%. Only tubular products saw a decline, totaling 9% year over year.

The company's problems from a revenue perspective largely centered around a decline in price. 2023 was not a good year for steel. A number of factors, such as supply chain constraints, the Russian invasion of Ukraine, strict COVID-19 policies, and the desire to pass on inflationary pressures to customers, all resulted in steel prices coming in rather high at one point. This seems to be a retracement to lower pricing as most of those factors die down considerably or as the market adjusts accordingly. Flat-rolled steel prices for United States Steel, for instance, dropped 15% in 2023. Mini mill prices fell nearly double that at 26%. And USSE prices plunged 20%. Only tubular prices increased, climbing about 5% year over year.

Author - SEC EDGAR Data

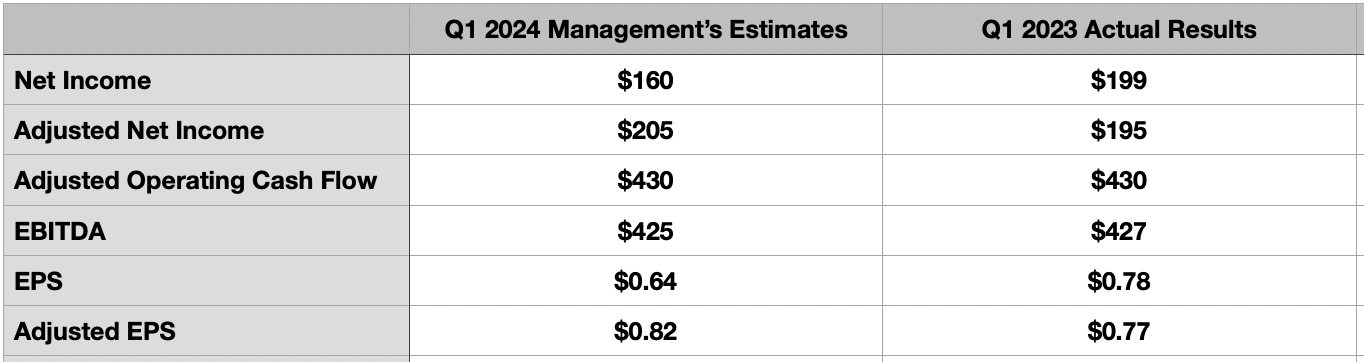

Naturally, bottom line results would worsen as the aforementioned chart illustrates. The good news is that there does appear to be some degree of normalization. Just recently, the management team at United States Steel announced some preliminary estimates for the first quarter of the 2024 fiscal year. They expect earnings of around $160 million, or $0.64 per share. That is down from the $199 million, or $0.78 per share, reported the same time one year earlier. But on an adjusted basis, profits are expected to be around $205 million, or $0.82 per share. That's up from the $195 million, or $0.77 per share, reported one year earlier. Based on other estimates provided by management, EBITDA should be around $425 million, while adjusted operating cash flow should come in somewhere around $430 million. For context, in the first quarter of last year, these numbers were $427 million and $430 million, respectively.

Author - SEC EDGAR Data

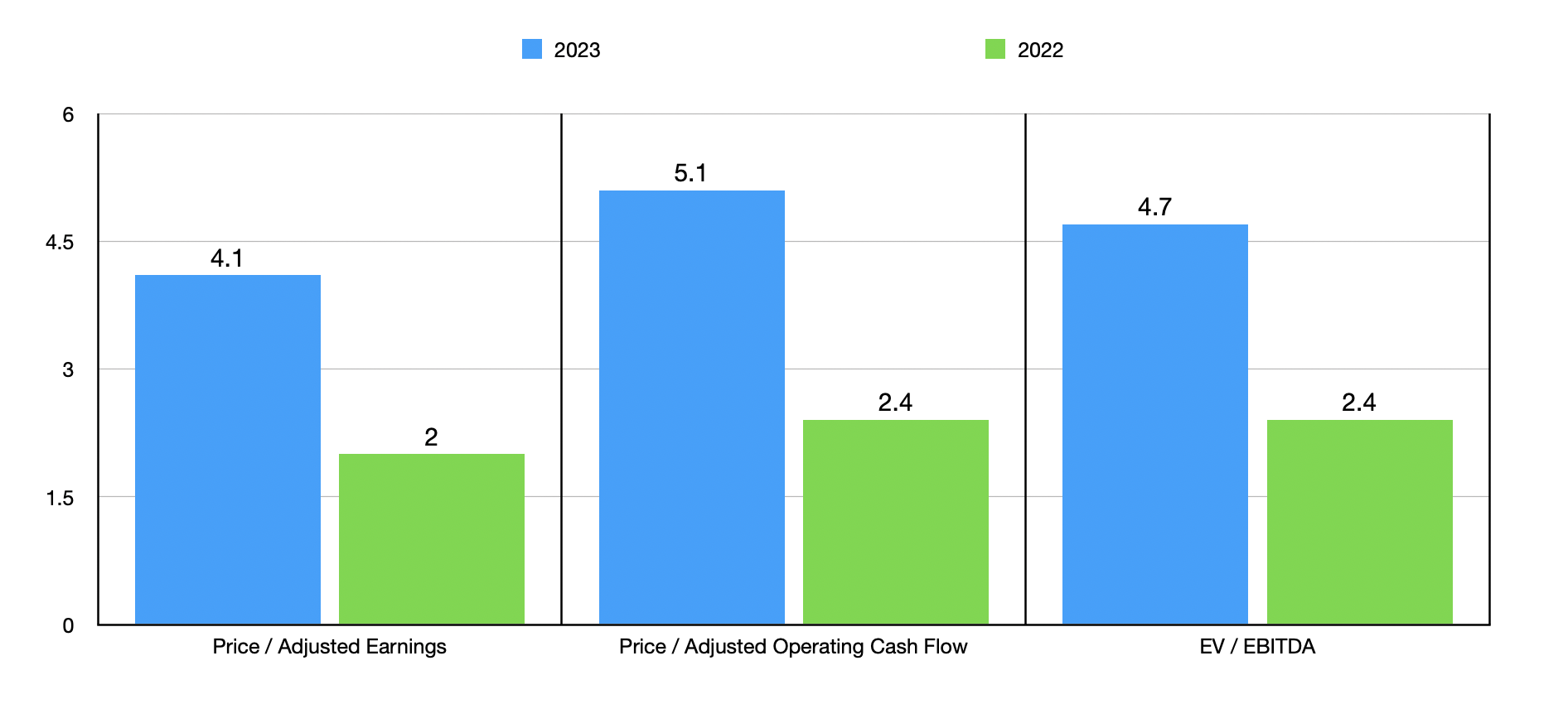

Assuming that the future looks very similar to the 2023 fiscal year, shares of United States Steel are trading at rather attractive levels right now. In the chart above, you can see precisely what I mean. I then compared the company, as shown in the table below, to six other steel producers. This list was inspired by the five companies I wrote about in a previous article that I thought would be the most likely suitors for United States Steel. Also added to the list is the current planned acquirer, Nippon Steel. If we use pricing as it stands today, then United States Steel is the cheapest of the group on a price-to-earnings basis. Only one of the six companies ended up being cheaper than it when it involved the EV to EBITDA approach. And when it comes down to the price to operating cash flow approach, three of the six ended up being cheaper. This all suggests to me that further downside, even in the event that the deal fails, should be short-lived and/or minimal at best.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| United States Steel Corporation | 4.1 | 5.1 | 4.7 |

| Cleveland-Cliffs Inc. (CLF) | 26.6 | 4.5 | 7.0 |

| ArcelorMittal S.A. | 26.5 | 2.9 | 5.2 |

| Nucor Corporation (NUE) | 10.6 | 6.7 | 5.9 |

| Stelco Holdings Inc. (OTCPK:STZHF) | 15.3 | 9.2 | 4.2 |

| Steel Dynamics, Inc. (STLD) | 9.6 | 6.7 | 6.1 |

| Nippon Steel Corporation | 5.8 | 4.2 | 5.5 |

Perhaps it's just wishful thinking, but I believe that there is a high probability that Nippon Steel will end up successfully acquiring United States Steel. The company has already promised almost everything that the unions could want. They just need to finalize that and perhaps add some sweeteners to the transaction. If they can resolve the aforementioned joint venture and perhaps make some other minor concessions, I see no reason why they won't receive approval from a regulatory perspective. This is especially true on the CFIUS side of things if they can make the unions happy.

Even if the Nippon deal does not get completed, United States Steel Corporation shares look very cheap at this point in time. There's also the prospect that some of the other suitors might be willing to pick it up for a slightly lower price. I know that Cleveland-Cliffs was the second-highest bidder at $54 in a stock and cash transaction. In recent days, the CEO of the company has said that if they reconsider, they would be looking to bid less than $30. But that sounds to me more like pouting than a realistic outcome considering the fact that there were multiple bidders in line for this. But regardless of that outcome, the fundamental attractiveness of shares today makes this a "strong buy," especially when factoring in the significant upside that could come from the deal being approved.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.