Ethan Miller/Getty Images News

Ethan Miller/Getty Images News

Motorola Solutions (NYSE:MSI) reported their Q4 FY23 result on February 8th with a robust growth. I initiated my ‘Buy’ thesis in my previous coverage, highlighting their strong growth in the public safety market. I anticipate their APX NEXT replace cycle persists into FY24, which will continue to drive their topline growth and margin expansion. I am also encouraged by their increasing business mix towards software/services. I reiterate a ‘Buy’ rating with a fair value of $360 per share.

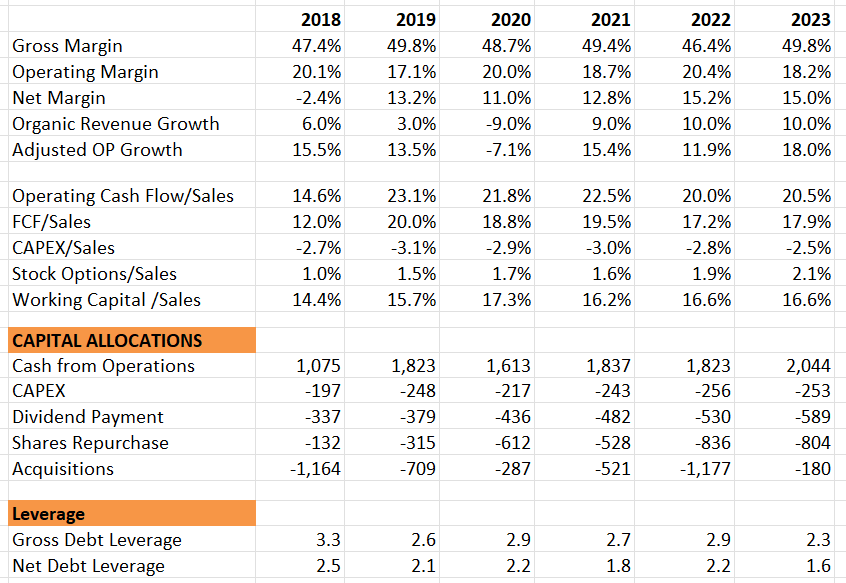

Motorola has witnessed strong margin expansion and FCF growth. They delivered 5% organic revenue growth and 5.8% adjusted operating profit growth in Q4 FY23, as shown in the tables below. For the full year, their adjusted operating profit was increased by 18%, and they delivered the record-high FCF of $1.8 billion.

Motorola ended the year with $1.7 billion in cash and 1.4x of net debt leverage, reflecting a robust balance sheet. They paid out $589 million dividends and repurchased $804 million of own shares, a quite consistent capital allocation policy.

Motorola Solutions Quarterly Results Motorola Solutions 10Ks

During the quarter, I am impressed by their strong growth stemming from the continued APX NEXT replacement cycle.

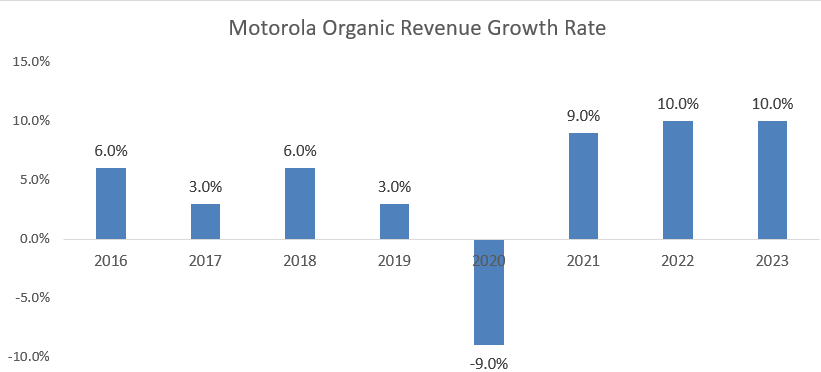

Motorola’s organic revenue rate has been around 10% in the post-pandemic period, as depicted in the chart below. As mentioned in my previous coverage, their APX NEXT launched in October 2019 was a huge success for the company’s growth in recent years. During the earnings call, their management anticipated that the APX NEXT replacement cycle would continue to progress and the end-market demands remain robust. Additionally, Motorola has developed related software attached to the device, enabling them to generate extra software and service revenue from these devices sales. The software and services could carry much higher margin for the company, being recurring in nature.

Motorola Solutions 10Ks

The revenue from software and services accounts for 37.4% of total revenue, marking a notable increase from 30.5% in FY18. In Q4 FY23, the software and services business grew by 7% year-over-year, led by growth in video, command center and land mobile radio (LMR). I favor a higher software and service mix in their business, which would lower the overall volatility of the company. I anticipate the growth momentum continuing in FY24.

The total backlog for software and services was up $800 million versus last year, as disclosed in the earnings call. The strong backlog would pave the way for their strong growth in the near term.

As mentioned earlier, Motorola has been building software for their APX NEXT devices, along with offering adds-on services. It worth noting that their software is widely used in the public safety and enterprise Command Center. These software and services constitute a quite sticky business.

Motorola announces to acquire IPVideo last December, the creator of the HALO Smart Sensor. The intelligent sensor system has been used for detecting real-time health and safety threats. The deal price was not disclosed, as such, it was considered a small tuck-in acquisition. IPVideo could complement Motorola’s strength in the public safety and video segment, and I presume it would be relatively straightforward for Motorola to integrate HALO Smart Sensor into their existing surveillance portfolio.

Motorola anticipates 6% revenue growth and 6.2% EPS growth in FY24, expecting to achieve growth in both volume and pricing. Considering their consistent organic revenue growth of 10% over the past two years, I view their guidance as quite conservative.

Firstly, their Video Security and Command Center business delivered double-digit revenue growth in Q4 FY23, and both segments ended the year with a record backlog. These backlogs would flow into the actual revenue in FY24, and I forecast the Video Security and Command Center to grow at double-digit in FY24.

Secondly, their software and service grew by 12.9% in FY21, 7.8% in FY22 and 10.4% in FY23, primarily driven by increasing attach rate with their device sales. Assuming another double-digit growth in FY24, the software and service could contribute 3%-4% to their topline growth.

Lastly, APX NEXT device refreshment cycle is expected to persist in FY24, as indicated by their management. Putting all together, I anticipate Motorola will deliver 7%-8% organic revenue growth in FY24.

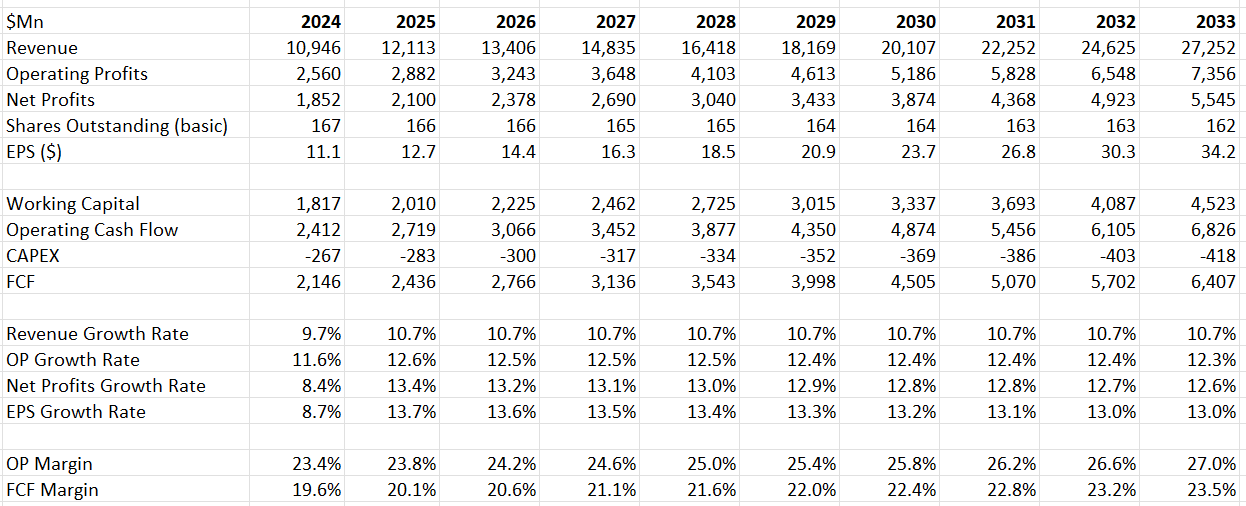

Regarding the DCF model, I assume 8% organic revenue growth in FY24 as discussed previously. Assuming Motorola allocating 5% of revenue toward acquisitions, M&A could add 1.7% of topline growth. For the normalized growth, I assume 9% organic revenue growth, reflecting the potential acceleration from software and service as their revenue mix gradually increases.

I calculate the operating expense growth to be 70bps lower than the topline growth, leading to 40bps margin expansion per year. Their margin expansion is driven primarily by operating leverage, pricing growth and increasing penetration of software component.

The following assumptions are used to calculate the WACC:

-Beta: 0.89 (Seeking Alpha)

-Risk-Free Rate of Return: 4.323 (10-year US government bond yield)

-Tax Rate: 20% (company’s guidance)

-Expected Market Return Premium: 7%. I am using the same assumption across my models.

-Cost of debt: 7%.

Using their current market cap and debt balance of $6 billion, the WACC is calculated to be 10%. The fair value is calculated to be $360 per share, as per my calculation. The current stock price is trading at 23x fwd. free cash flow, lower than high 20%s for most double-digit earnings growth companies.

Motorola Solutions DCF - Author's Calculation

As reported by Reuters last December, UK antitrust regulator won an appeal over Motorola’s Airwave network probe. In August 2023, the Competition and Markets Authority (CMA) ordered mandating price controls on Motorola’s Airwave network in UK, and the media reported that Motorola was projected to lose more than $1 billion in expected revenues over the next several years with the price control order. In Q4 FY23, Motorola has already been experiencing reduced revenue and backlog due to Airwave price controls. Motorola is still in court with the UK regulator, and the outcome is unknow at this point.

Motorola’s volume and pricing growth are more likely to sustain in the near future, and they continue to benefit from the APX NEXT replacement cycle, in my view. Their increasing mix towards software/services would make the company’s growth more recurring. I reiterate a ‘Buy’ rating with a fair value of $360 per share.