bjdlzx

bjdlzx

Baytex Energy Corp. (NYSE:BTE) management reported a significant increase in cash flow compared to what it would have been had the company not acquired Ranger Oil (ROCC). The fourth quarter cash flow represented more than half of the cash flow for the fiscal year. This is now a light oil upstream company. The market has yet to adjust to the transformational acquisition. But when the market does adjust, shareholders can expect a better stock price.

The Eagle Ford properties acquired are among the most profitable in the company portfolio. They also change the company from a heavy oil producer (subject to a discount from WTI pricing) to a light oil producer whose Eagle Ford production often gets a premium price to the local benchmark. It is not just the transformation to light oil that is important. It is instead the transformation to a light oil producer whose production gets additional return from the premium pricing of that production. This is something the market will value as well.

Management went into some immediate issues like stock overhang, and debt rearrangement as well as better cash flow that really first showed in the fourth quarter. All of this makes for a bumpier transition than the last article indicated. But it does not change the future outlook despite a lot of worries expressed in the conference call.

The market appears to have focused on the impairment charges. Impairment charges are generally a noncash charge that corrections noncash allocations of the past (undetermined number of) years. This is why cash flow is far more important as an indicator of company health.

(Note: This Is A NYSE-Listed Canadian Company That Reports In Canadian Dollars Unless Otherwise Stated).

Baytex Energy Summary Of Fourth Quarter Results (Baytex Energy Earnings Press Release Fourth Quarter 2023)

As shown above, free cash flow strengthened considerably in the current fiscal year despite generally lower commodity prices when compared to the previous fiscal year. The Eagle Ford properties are in a class all by themselves when it comes to free cash flow. Management mentioned this in the conference call.

The premium obtained for the production combined with great geology allow for low breakeven for wells drilled that is seldom matched in North America. Since oil prices are not exactly low right now, then cash flow is going to be generous.

The market was concerned about more debt in absolute terms. But the debt ratio was 1.1.

Since the company has United States dollar-based loans, there is some concern about currency issues. However, the Eagle Ford business appears to be able to support the loans (and that is likewise United States dollars). Therefore, despite the accounting reporting, the dollars earned to go for loans likely will result in no gains or losses.

The Canadian business essentially makes the loans safer.

In short, there is a lot changing about this company that Mr. Market has to get used to. But management does not have to do anything special for many of the things that are new for the market to like the upcoming reporting.

Before the latest acquisition, Baytex had acquired non-operated Eagle Ford properties back around 2014 just before the big oil price decline. The market tends to discount non-operated properties because Baytex could not really control the development pace, nor could it control the accompanying capital budget. For many years management stated that those Eagle Ford properties had "first call" on any capital because those properties were extremely profitable compared to the company heavy oil business at the time.

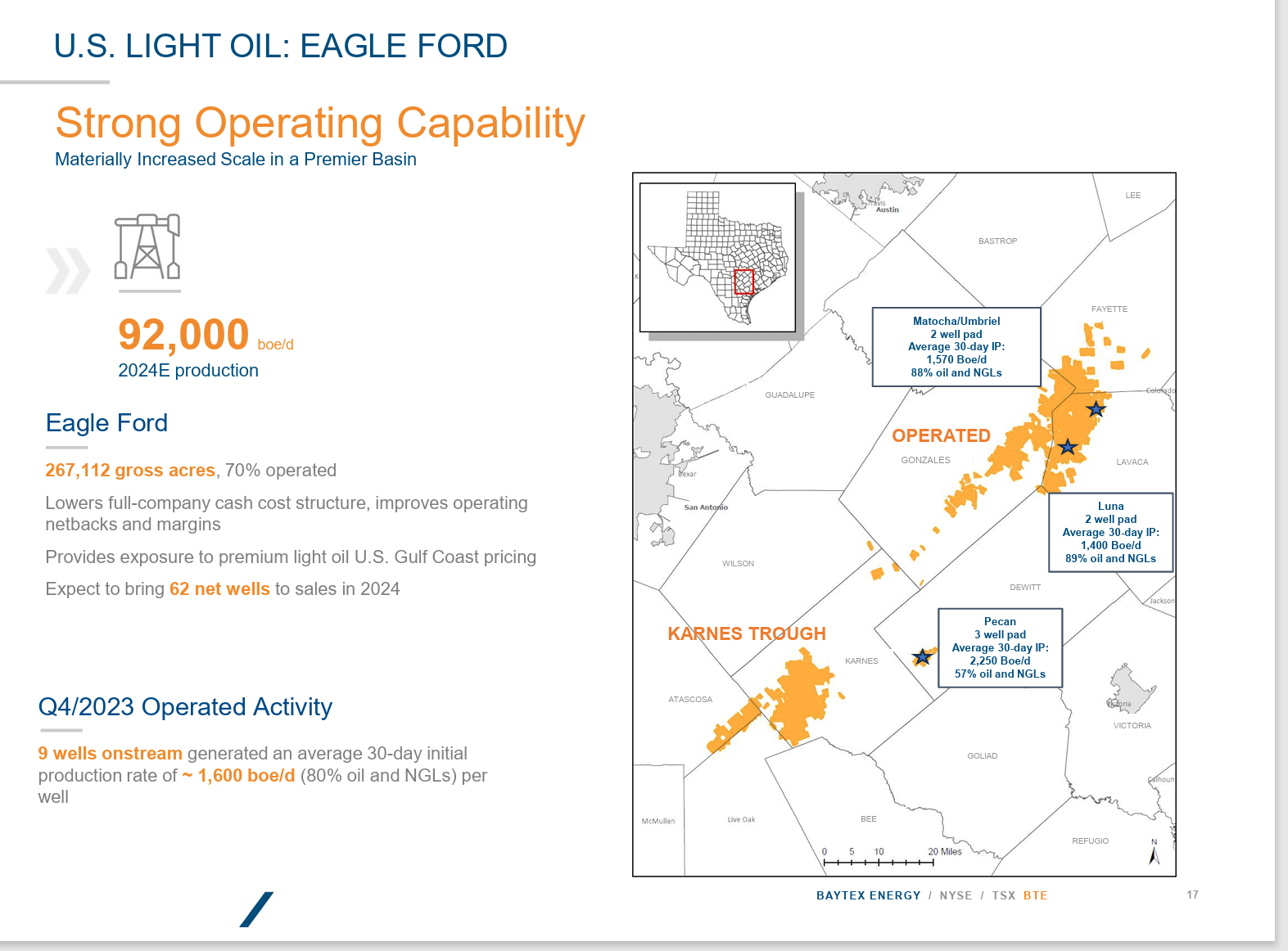

Baytex Energy Map Of Eagle Ford Operations (Baytex Energy Fourth Quarter 2023, Earnings Conference Call Slides)

That situation has now changed dramatically with the acquisition of Ranger Oil. Much of the production is now managed by Baytex. Baytex has access to a considerable amount of operator information from the non-operated properties. Long time readers know that Marathon Oil (MRO) is the operator of those properties. Marathon is known as one of the top operators in the Eagle Ford.

That partnership gives Baytex a lot of information that can be used to upgrade operations on the acquired properties. Already management is looking to cut back some key well costs. What is likely to follow is some increasing initial production numbers combined with better overall recoveries.

That will likely take more time to become apparent to shareholders because it takes time for more efficient wells to become a significant part of production. The existing production costs do not just "disappear" because Baytex made the acquisition and has a better idea of how to run things.

But already, the fourth quarter showed stronger free cash flow numbers (and the GAAP cash flow number was likely better as well for the prices obtained). Production and profitability could get a further future boost from the rapid technology changes sweeping the industry. Even mediocre deals or worse often look good thanks to those technology changes. This, though was a darn good deal for the company.

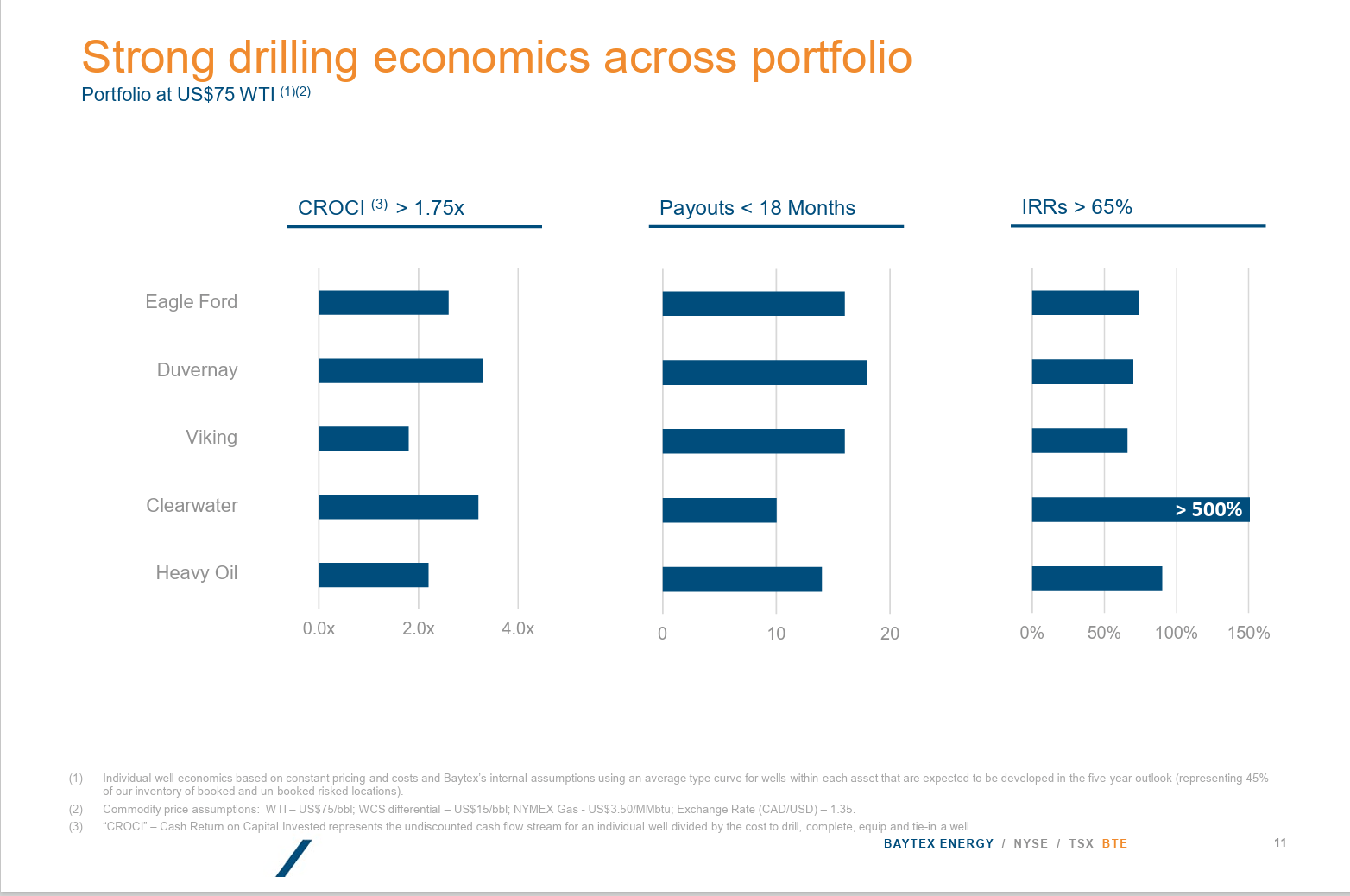

This acquisition will also benefit the Clearwater production. Clearwater (as shown below is unusually profitable).

Baytex Energy Summary Of Financial Characteristics Of Portfolio Projects (Baytex Energy Fourth Quarter 2023, Earnings Conference Call Slides)

The Clearwater play has long been the most profitable play in the company portfolio. But the heavy oil product has a selling price that is discounted to light oil pricing. That discount can widen to the point where heavy oil production is shut-in until a cyclical recovery begins.

Clearwater has costs that are low enough that the production might cash flow during most cyclical downturns. But that really has yet to go through a couple of business cycles for an actual experience.

The light oil production gives the company some safer cash flow in a cyclical downturn. This makes debt servicing in a downturn a much easier prospect. It also makes the Clearwater development a safer idea. Even with the fast payback shown above and the extremely good profitability, the company needs a cash source during cyclical downturns.

The new item here is that there is interest in the Bluesky and other intervals as the Clearwater Basin continues to come online. The costs in this particular basin are revolutionizing the heavy oil business. So, it is still an open question as to the production capability of this new basin.

In the meantime, the company now has two very highly profitable ways to grow in the future. The traditional heavy oil business is profitable right now. But that is not considered a reliable cash source for the reasons noted above. Instead, heavy oil is now an "extra" that is available during the good times. Clearwater may change that. But that is far from certain.

Clearwater has now largely relegated the rest of the heavy oil portfolio to maintenance or a lower growth priority. Because technology keeps advancing and (as a result) different basins have taken the cost lead at different times, it makes little sense to try to dispose of the legacy business. Another technology advance could see the company prioritizing a different area in the future.

Management mentioned during the conference call that they are far from satisfied with the stock performance. An additional consideration is the plans of Juniper (JNPR). Juniper was a major Ranger Oil shareholder who holds more than 10% of the outstanding Baytex stock. Should Juniper decide to exit its position, that could keep the stock price somewhat depressed for a bit.

Management mentioned that there may be other institutions as well that wanted to cash in the profits made by the merger. As such a stock price weakness is not unexpected.

Management does not view any of these as a long-term issue.

Management is replacing its US dollar-denominated debt due in 2027 with a slightly larger issue due in 2032. This does not mean the company will have a significantly larger amount of debt outstanding as a result.

The reduction in the effective rate of interest from 8.75% to 7.5% is likely one motivating factor. Management was able to upsize the offering to $575 million (United States dollars), which likely means more of the bank debt will be repaid.

Most companies will prioritize repaying any loans on the bank line first. This company appears to be no exception to that general rule.

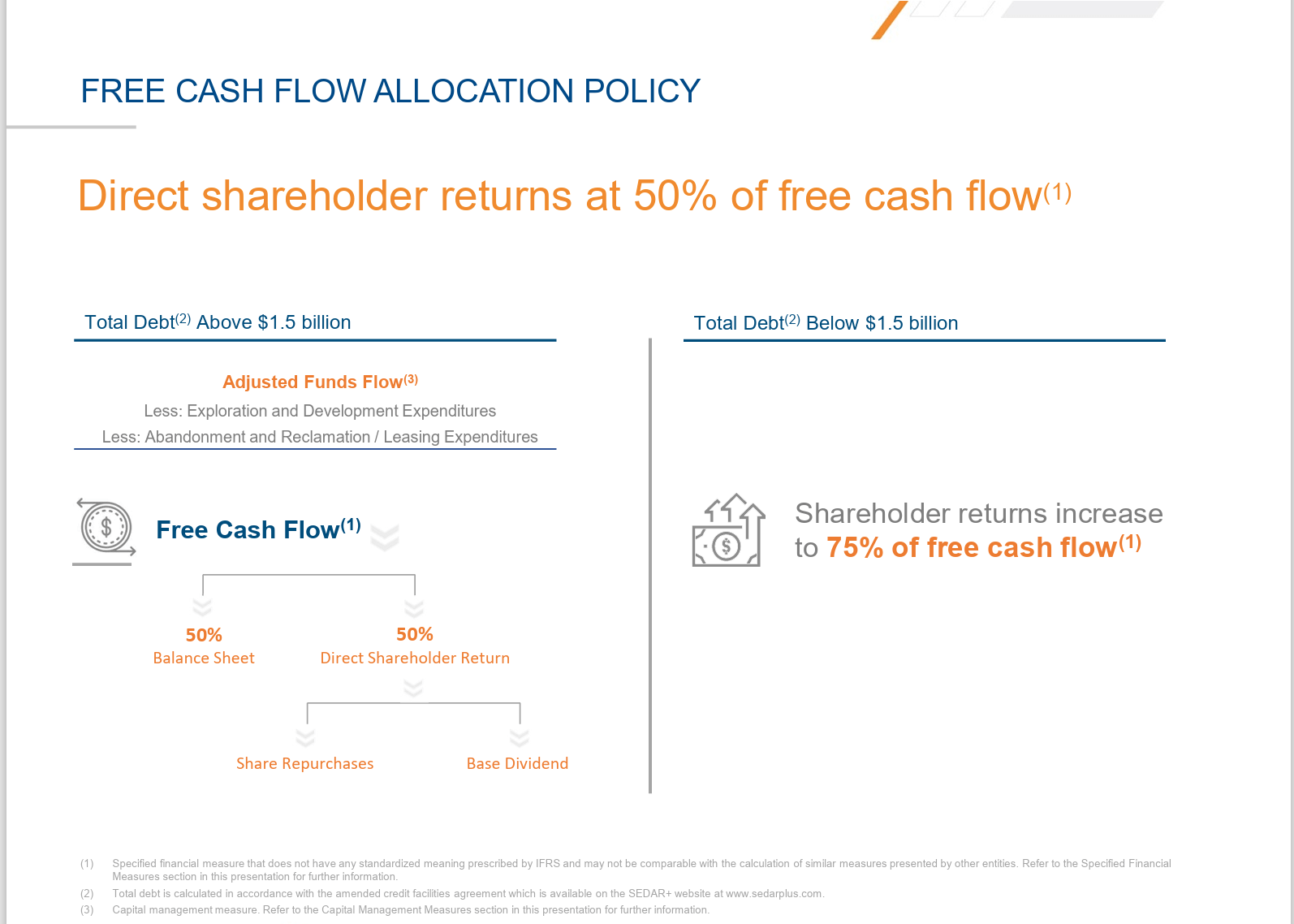

The company now has a dividend policy along with an updated shareholder return policy shown below. This policy takes into account the latest acquisition of Ranger.

Baytex Energy Shareholder Returns Guidance (Baytex Energy Earnings Conference Call Slides Fourth Quarter 2023)

Management has a goal for debt levels to increase shareholder returns. Clearly company profitability took a big boost. As a result, management is likely to get at least half-way to the goal shown above from the current financial position.

What is unclear is the effect of the exchange rate on the reported balance. The debt levels did get a benefit from the exchange rate in the current quarter. Whether that is something management will include in the reporting (or assume a fixed rate no matter what happens) is an open question. A continuing strengthening of the Canadian dollar could get the balance sheet into better shape sooner whereas a weakening would have the opposite effect.

In the meantime, the share repurchases almost assure dividend increases in the future. Management mentioned that about 4% of the shares outstanding were repurchased. That is a loud signal that management considers the stock cheap. It also increases the cash per share available for future dividends.

This issue is a strong buy consideration for investors interested in upstream. Remember that upstream is generally very volatile and very low visibility. Therefore, conservative investors can look elsewhere. For income investors, this would be for that small aggressive portion of the portfolio.

Once the market realizes that the main product of the company is now light oil. Then the market is likely to revalue this company accordingly. The cost structure changed with the acquisition. The worries about the discount widening for sales of heavy oil now are a lower concern in the past. This upstream player is likely to be worth considerably more in the future now that most of the business is in the United States and now Canada (were operation values are often lower than the United States).