Peshkova

Peshkova

Shares of biotechnology companies have been lagging behind the S&P 500 Index (SP500). Since we initiated our bullish view on the SPDR S&P Biotech ETF (NYSEARCA:XBI) with a "Buy" rating in December 2022, the S&P 500 Index has surged by a whopping 33.5% while the XBI has only risen by 13.7%.

TradingView.com, Stratos Capital Partners XBI) since we initiatied our bullish "Buy" rating 21 December 2022.' width="640" height="296" contenteditable="false" data-width="640" data-height="296">

XBI) since we initiatied our bullish "Buy" rating 21 December 2022.' width="640" height="296" contenteditable="false" data-width="640" data-height="296">

This underperformance in XBI appears to be mainly driven by dashed expectations for an early rate cut from the Federal Reserve (Fed). As evident in the chart above, XBI had initially begun to outperform the S&P 500 in November 2023 as the market was warming to the prospect of a rate cut by March 2024. However, XBI eventually lost momentum as expectations of an early rate cut began to wane following a hot February consumer price inflation (CPI) report and stronger-than-expected labour market data.

Because cashflows for growth companies tend to sit further away into the future, those cashflows are more heavily discounted when investors value growth companies. Thus valuations for biotechnology companies are more sensitive to the outlook for interest rates versus companies with evenly distributed cashflows.

This underperformance of XBI relative to the S&P 500, however, has only made the opportunity even more attractive to us.

Therefore, we are taking this opportunity to upgrade our rating for XBI from "Buy" to "Strong Buy". This is in line with our recent recommendations for investors to rotate equity exposure away from big-tech and artificial intelligence themes, and into laggard themes including biotechnology, healthcare, and residential real estate.

We are already beginning to see more evidence of improving fundamentals and rising mergers and acquisitions (M&A) activity within the biotechnology space. And these improvements have yet to be fully appreciated by investors, in our view.

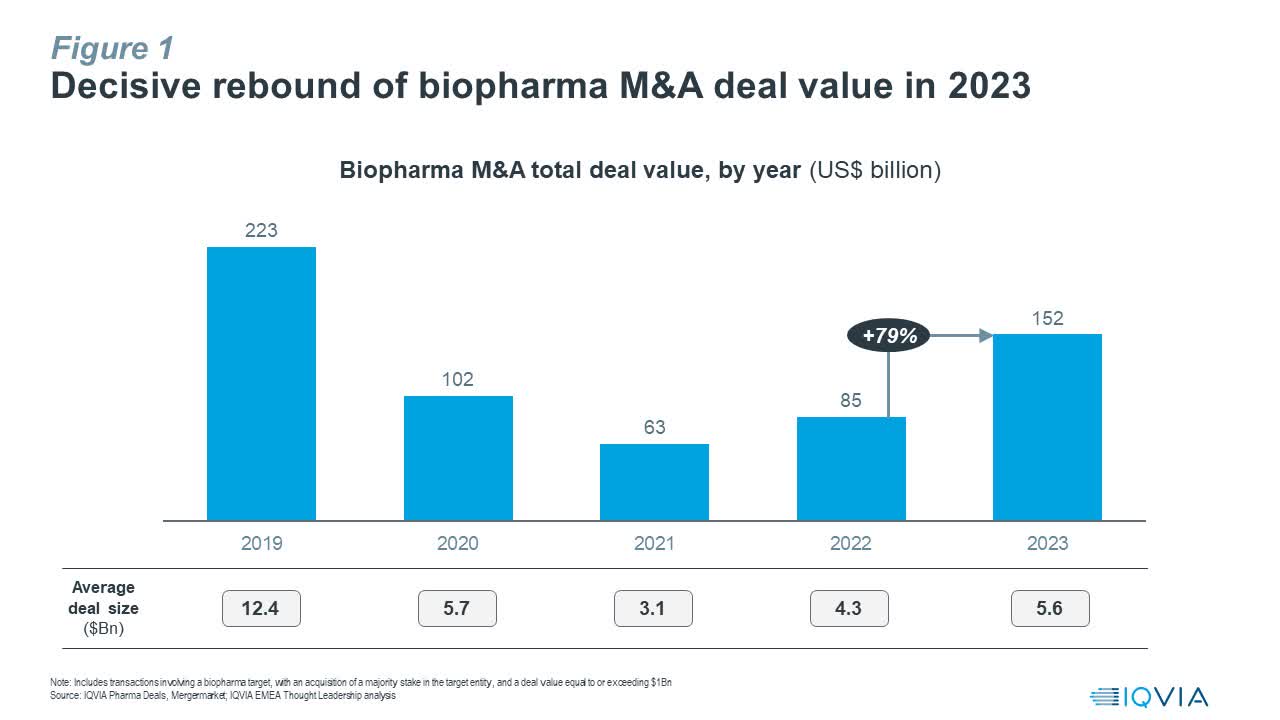

As the accompanying chart shows, the total value of biotechnology and pharmaceutical M&As has rebounded by 79% in 2023. At US$152 billion, the total value of M&A deals is still well below 2019 levels of US$223 billion, suggesting room for further upside in 2024.

IQVIA

Several factors are driving this recovery in M&A activity. Firstly, higher interest rates following a series of rate hikes by the Fed, economic uncertainties during and post-Covid19, and valuation mark-downs have all encouraged biotech investors to stay at the sidelines since 2020. Investment plans were temporarily shelved while hiring headcounts were frozen to preserve cash and assuage investors in this challenging business environment. Now that the prospect for rate cuts is clearer, and valuations for biotech have bottomed, investors are feeling more confident and willing to deploy their dry powder again.

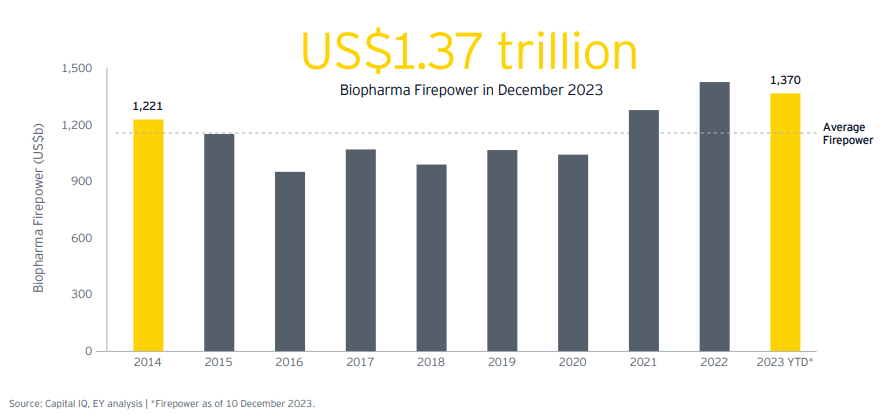

According to a recent report published by Ernst & Young, companies in the biotechnology and pharmaceutical sectors are estimated to have around US$1.37 trillion at their disposal for acquisitions, which is close to an all-time high. As these companies compete for deals, there has been an observed increase in aggressive acquisition offers with higher premiums.

2024 EY M&A Firepower report

Another factor driving this M&A recovery in biotech is the looming threat of a "patent cliff", where large pharmaceutical companies including Bristol Myers Squibb (BMY), Merck (MRK), Pfizer (PFE), and Johnson & Johnson (JNJ) are expecting blockbuster drugs to lose their patent and exclusivity protections. This "patent cliff" not only represents a threat to revenues and market shares for these companies but also presents a potential growth gap of over US$120 billion by 2028.

Although the prospect of a delayed rate cut by the Fed has risen significantly in recent weeks, we still see rate cuts as a matter of when not if. We are increasingly concerned that delaying rate cuts will only increase the risk of a recession, which means that the Fed may have to cut rates even more aggressively later on. Nonetheless, so long we do not see a deep recession, we still think biotechnology stocks will outperform in the next couple of years.

We see the potential for XBI to catch up to the S&P 500 in performance while providing some margin of safety due to modest valuations on biotech. All these should translate into the potential for alpha.

Crucially, we reiterate our strategy to invest broadly across large, mid and small-cap biotech names. This is necessary to manage the high idiosyncratic risks associated with the performance of biotech companies. We believe that our more passive approach to investing broadly across the biotech space will allow us to capture gains from a general recovery of the biotech sector and M&A activity while avoiding unnecessary idiosyncratic risks.

The XBI is ideal for our purposes. According to fund information provided by the issuer State Street Global Advisors, XBI seeks to provide investment results that correspond generally to the total return performance of the S&P Biotechnology Select Industry Index. The index is a modified equal-weighted index which provides the potential for unconcentrated industry exposure across large, mid and small-cap biotech stocks.

State Street Global Advisors SPDR

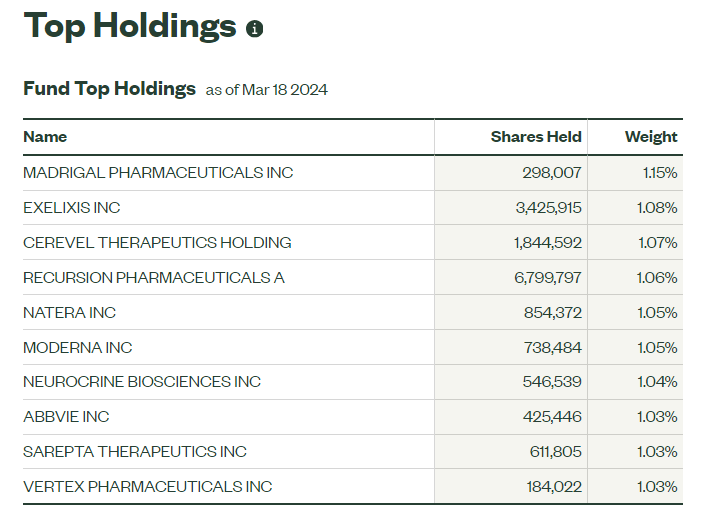

As the accompanying table shows, XBI's top ten holdings make up just under 11% of the fund's portfolio. Furthermore, each of XBI's top ten holdings makes up around just 1.03% to 1.15% of the portfolio individually.

In terms of valuation, the XBI is still trading at a compelling forward P/E multiple of 14.3x. This versus the increasingly expensive S&P 500 Index, which is trading at around 25x forward P/E, presents a compelling value opportunity to be bullish XBI in our view.

We like how despite improving fundamentals and M&A activity, XBI is still underperforming the S&P 500 Index. Furthermore, valuations on XBI is compelling at just 14.3x forward P/E.

We see the potential for XBI to catch up to the S&P 500 in performance while providing some margin of safety due to modest valuations on biotech. All these should translate into the potential for alpha.

Accordingly, we are taking this opportunity to upgrade our rating for XBI from "Buy" to "Strong Buy".

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.