aquaArts studio/E+ via Getty Images

aquaArts studio/E+ via Getty Images

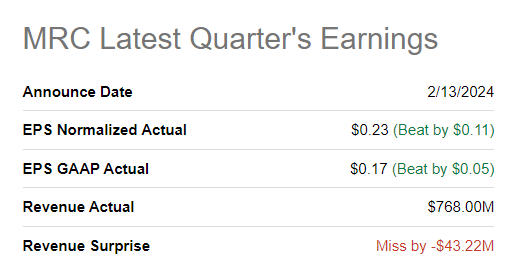

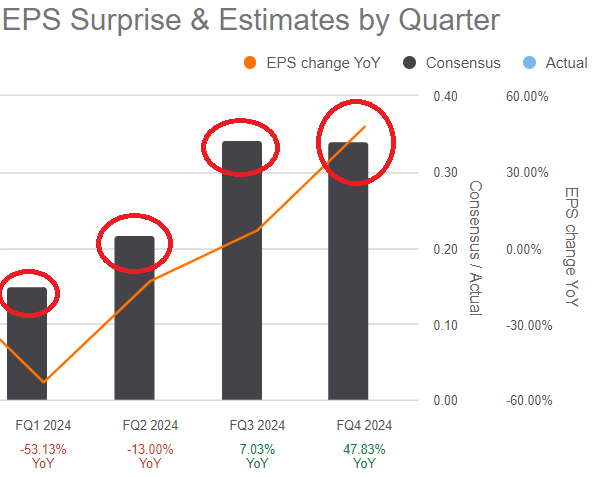

MRC Global Inc. (NYSE:MRC) recently reported better-than-expected EPS GAAP earnings and EPS growth, and positive FCF is also expected in 2024. With a diversified business model that includes many products and many clients, I believe that the largest net sales growth drivers include multi-year programs with gas utility customers and gas demand from the housing market. In addition, I would be expecting conscious demand from the need for replacement and maintenance of all gas infrastructure both in the U.S. and internationally. There are obvious risks from issues with suppliers, and volatility in the energy industry, however, I believe that MRC does trade quite cheaply right now at close to 5-6x cash flow.

MRC is the world's leading distributor of pipes, valves, and fittings and provides innovative supply chain solutions to the gas, power, and industrial services sectors.

With more than 100 years of experience and a global network of more than 8,500 suppliers, the company serves approximately 10,000 customers through digital commerce applications and 214 service locations. They offer over 300k SKUs, including PVF, oilfield supply, valve automation, metering and instrumentation, serving diverse end markets. Given the total number of clients, and products offered I believe that MRC appears significantly diversified. As a result, I would be expecting lower net sales volatility than what other peers with less diversified business activity could report.

They specialize in serving key companies in the gas Utilities, DIET and PTI sectors, where product reliability and quality are crucial due to the demanding operating conditions and associated risks. With a base of approximately 10,000 customers, no one accounts for more than 10% of revenue.

For many major customers, they are their main PVF supplier, providing reliable products and services. They seek to build long-term relationships by maintaining a strong reputation and offering value-added solutions. They anticipate that consolidation in the energy industry will benefit their business as companies look for larger, more comprehensive distributors like MRC Global.

With the business model being defined, I think that the recent earnings including better EPS GAAP than expected, and EPS expectations for 2024 are beneficial reasons for having a quick look at the future of MRC.

Source: Seeking Alpha Source: Seeking Alpha

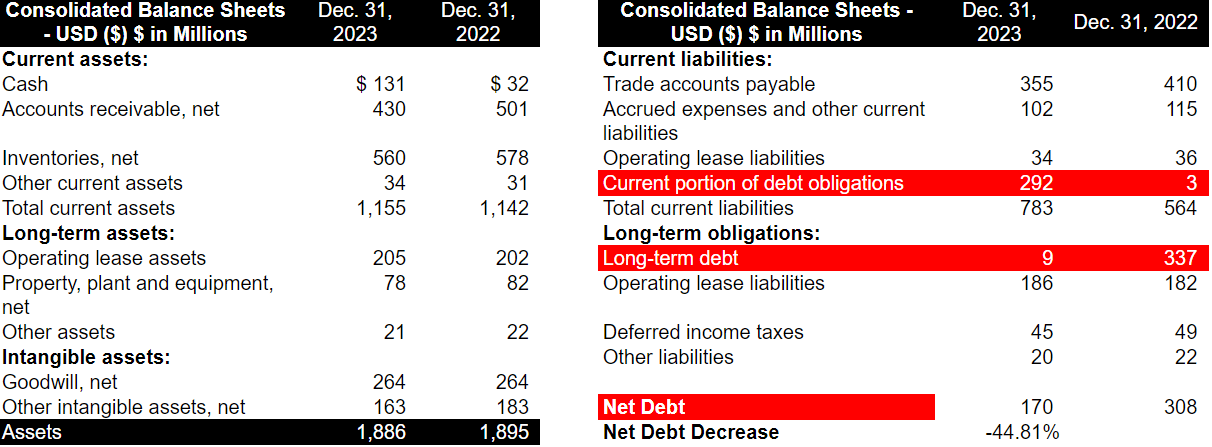

As of December 31, 2023, the company noted cash worth $131 million, which was significantly larger than in 2022. With this increase in cash, net debt decreased substantially from about $308 million in 2022 to close to $170 million in 2023. I think that the recent increase in liquidity could enhance the Ev/FCF in the coming quarters as soon as investors learn about it.

Also with accounts receivable of $430 million, inventories of about $560 million as well as total current assets of $1155 million, the current ratio is larger than 1x. In sum, I believe that MRC does not seem to have a liquidity issue.

Finally, with property, plant, and equipment of about $78 million, and goodwill worth $264 million, total assets stand at about $1886 million, which implies an asset/liability ratio close to 1x. In sum, with these figures, I believe that the balance sheet appears quite stable.

Source: 10-k

I studied carefully the company's long-term obligations. The company has a $400 million senior secured term loan B due September 2024. The interest rate, linked to the term SOFR, varies depending on the base interest rate. MRC and its affiliates guarantee the loan, backed by asset liens. Prepayments are required for asset sales and certain insurance proceeds. The $750 million global ABL facility, with specific guarantees and borrowing bases, provides additional flexibility. Given the total amount of inventory and assets, I am not really concerned about the total amount of obligations.

Source: 10-k

I believe that we will most likely see net sales growth given the agreements with gas utility customers, which require replacement and maintenance. Considering the total amount of old infrastructure in the United States, and elsewhere, I believe that we can expect a lot of work from MRC. According to The Pipeline and Hazardous Materials Safety Administration 35% of the gas distribution line miles are over 40 years old.

The majority of the work we perform with our gas utility customers are multi-year programs where they continually evaluate, monitor and implement measures to improve their pipeline distribution networks. Source: 10-k

The Pipeline and Hazardous Materials Safety Administration or PHMSA estimates approximately 35% of the gas distribution main and service line miles are over 40 years old or of unknown origin. This infrastructure requires continuous replacement and maintenance as these gas distribution networks continue to age. Source: 10-k

In the last annual report, MRC noted that most of their customers coming from the housing market continue to sign agreements with Gas Utilities, which will most likely bring steady growth in the coming years. The expectations of MRC are also in line with the expectations of market experts, who expect the Household Natural Gas Distribution Global Market to grow at close to 6.2% CAGR from now to 2028. I believe that market growth will most likely accelerate the company's net sales line.

It will grow to $240.62 billion in 2028 at a compound annual growth rate of 6.2%. Source

Based on market fundamentals and new market share opportunities, we expect the Gas Utilities sector to continue to have steady growth in the coming years. Source: 10-k

The company seeks to increase its market share through preferential contracts with clients. I believe that MRC's business strategy focused on growth, and developing long-term relationships will most likely bring larger FCF margins.

In addition, I think that offering products and services already tested in the United States in the global markets could bring significant net sales growth. Keep in mind that the target market expands significantly when MRC enters a new jurisdiction. In this regard, I believe that it is worth mentioning recent increases in backlog in 2023, and 2022 as well as average rig count.

Source: 10-k Source: 10-k

With the company's investments in technology and infrastructure, I think that the company could experience significant efficiency acceleration inside the organization. More in particular, the company's efforts with regard to detailed client account planning, digital integration, and lower overall cost to serve could bring FCF margin growth in the coming years. In this regard, the annual report included the following statements about investments in IT systems, and digitalization.

We invest in information technology systems and service center infrastructure to achieve improved operational excellence and customer service. Our digital transformation strategy is a key component of operational excellence and is designed to add further differentiation to our product and service offerings with an objective to maintain and grow our business with new and existing customers. Source: 10-k

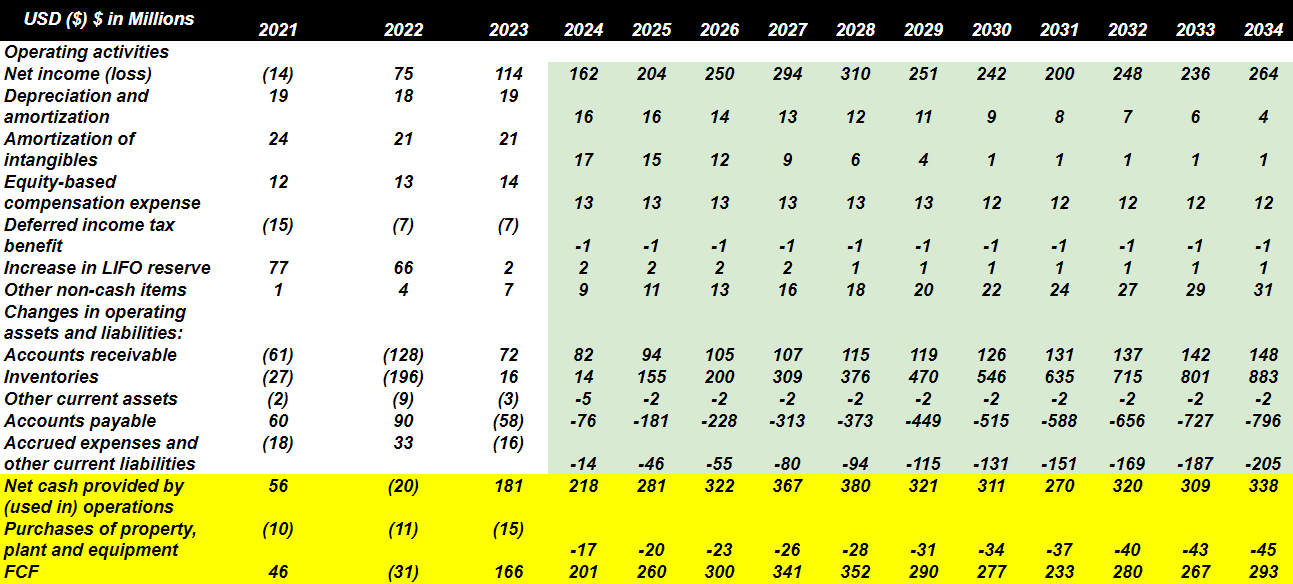

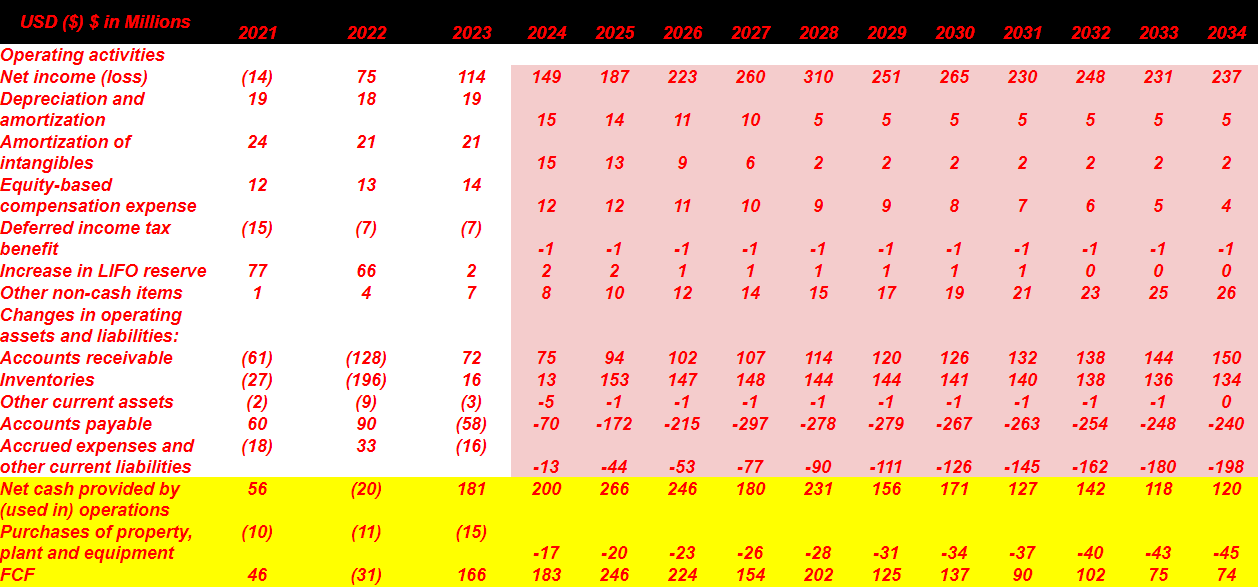

For the design of my cash flow forecasts, I took a look at previous changes in working capital, changes in inventory, as well as capital expenditures, and other items included in the cash flow statements. I believe that my figures are quite conservative.

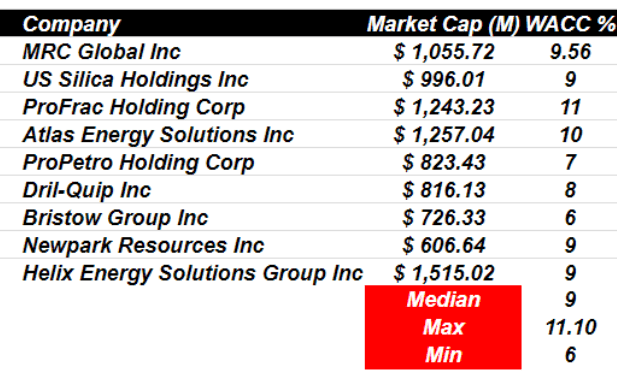

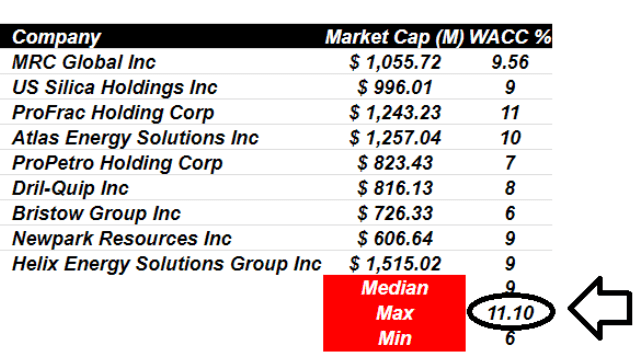

For the assessment of the cost of capital, I took a look at the cost of capital reported by other competitors. I obtained a peer list with a maximum WACC of 11%, a minimum WACC of 6%, and a median WACC of 9%. Under my best case scenario, I used a WACC of 9%, and under my worst case scenario, I used the maximum WACC of 11%.

Source: Gurufocus

MRC Global reports a weighted average interest rate of 8.98%, so I believe that cost of capital is close to 9%, and 11% would be conservative. The following table is from the last annual report.

Source: 10-k

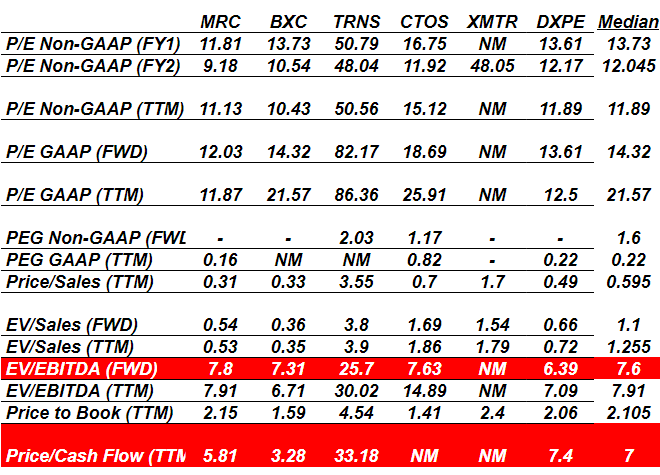

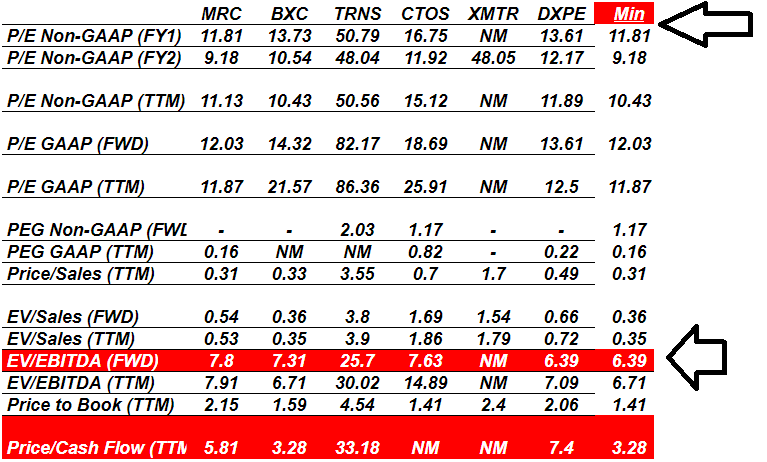

For the exit multiple I took a look at the list of competitors reported by Seeking Alpha, which includes a median EV/EBITDA of 7.6x, and price/cash flow of 7x. With these figures in mind, I assumed a valuation of 9x, which I believe is conservative.

Source: Seeking Alpha

With the previous assumptions, I also assumed 2034 net income of about $263 million, with depreciation and amortization of about $4 million, and also with amortization of intangibles close to $1 million.

In addition, I also assumed equity-based compensation expense of close to $11 million, and changes in other non-cash items of $31 million, Besides, I also took into addition changes in accounts receivable of $148 million, 2033 inventories of $883 million, and changes in other current assets of -$3 million.

Also assuming changes in accounts payable worth -$797 million, changes in accrued expenses and other current liabilities of -$206 million, 2033 CFO would stand at $338 million. If we also include 2033 purchases of property, plant and equipment of -$46 million, 2033 FCF would be close to $293 million.

Source: My Cash Flow Expectations

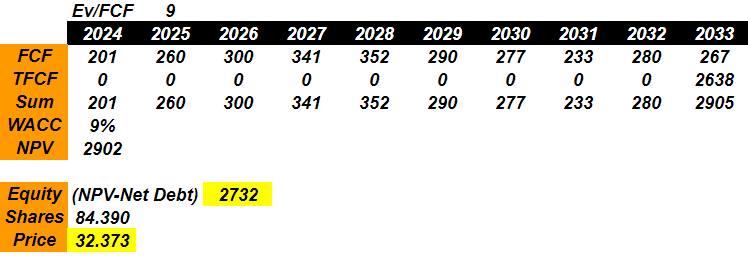

Now, putting everything together with a WACC of 9%, and terminal Ev/FCF of 9x the implied enterprise value would be $2.9 billion, and the implied price would stand at about $32-$33. Given the current market capitalization, I believe that there is upside potential in the stock price.

Source: My Cash Flow Expectations

Under my bear case scenario, I assumptions with respect to changes in working capital, capital expenditures, and other items that are a bit more pessimistic than in the previous case scenario. I also included the maximum WACC observed in the list of peers offered by Gurufocus. In addition, my EV/FCF is close to the minimum EV/EBITDA, and price/cash flow multiple reported by Seeking Alpha.

Source: Gurufocus Source: Seeking Alpha

With the previous assumptions, I also assumed 2033 net income of $237 million, with depreciation and amortization of about $5 million, 2033 amortization of intangibles close to $2 million, and with equity-based compensation expense of $4 million.

In addition, I assumed changes in operating assets and liabilities including accounts receivable of $150 million, with changes in inventories worth $134 million, and changes in other current assets of -$1 million.

Finally, with changes in accounts payable of -$241 million, changes in account accrued expenses and other current liabilities of -$198 million, which implied 2033 CFO of $119 million. With 2033 property, plant and equipment of about -$46 million, I obtained 2033 FCF $74 million.

Source: My Cash Flow Expectations

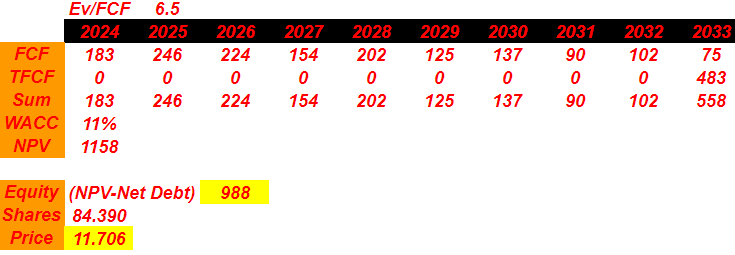

With the previous assumptions, I obtained a total enterprise value of $1.1 billion, equity valuation of about $988 million, and an implied stock price of close to $11.

Source: My Cash Flow Expectations

MRC's revenues are tied to the levels of capital and operating expenses in the industries it serves. Demand for products and services is sensitive to capital expenditure in sectors such as gas utilities.

Fluctuations in oil and gas exploration, production and refining activity affect demand. U.S. and global economic conditions negatively impact whether clients reduce capital expenditures due to recessions, interest rates, inflation, among other factors beyond our control.

As a global leader in PVF distribution for operated markets, they compete in a fragmented industry with well-known national distributors, major regional competitors and numerous local distributors. They stand out through agile local service, compliance capacity, a wide range of products and services, price competitiveness and total costs for the client. They face competition from large PVF distributors, regional and specialty competitors, as well as numerous local distributors. Furthermore, competition is intensifying as many of the suppliers also sell directly to end users.

I believe that MRC Global presents a solid strategy focused on growth, diversification, efficiency, and long-term relationships. Given the amount of old infrastructure, MRC will most likely have a lot of work offering maintenance and replacement to utility companies. In addition, I believe that the housing market and the demand for gas will most likely represent a net sales driver for MRC. In my view, I think that risks associated with dependence on economic activity and changes in capital expenditure must be monitored. Besides, competition and pressure from direct suppliers add complexity and may drive down FCF margins. With that all being said, MRC does look significantly undervalued at the current valuation of 7x EBITDA.