JazzIRT

JazzIRT

Medical Properties Trust (NYSE:MPW) is a company where I previously noted that I sold the stock. The reason is that the stock entered a period where I did not believe that the stock price would "run away" from me. So far that has been the case. I wanted to get past the 30-day wash sale and have clearly done so. A credit on the taxes for the loss does not eliminate the loss but it is better than nothing. But having followed other companies in a situation like this, it is very likely that the company gets most if not all of what it is owed as long as management evaluated the security properly and did the liens correctly. That, in and of itself is not a big risk. But knowing that the market waits for certainty gives me time to do more investigation of the current situation so that I will be ready to get back in when the time comes.

Clearly the situation got a little more complicated than I anticipated. But having been through this with Evolution Petroleum (EPM) because (at the time) main asset manager Denbury (DEN) filed bankruptcy. Evolution got every single penny and for the most part there really was no delays. But Mr. Market ignored those details to keep the stock price low until after Denbury emerged from bankruptcy. Before the Evolution situation there were others.

But the key idea is that if management has "their ducks in a row" from the start and has been very careful, then whatever happens with Steward will likely see Medical Properties Trust come out on top because it has a superior debt position to others that Steward owes money to.

However, just like with Evolution Petroleum (which was debt free with a considerable cash balance), the market cared little about the position of Evolution Petroleum while caring a lot about the perceived weaker partner. In this case Steward is not a partner but the owner of an asset or assets that the company has a lien on. That is an even better position to be in. But you would not know it from the actions of the market.

The biggest risk right now would be a negotiating team that gives away some or all of that superior position through negotiations without obtaining adequate collateral or decent chances of getting the money at risk back. There is also the risk of a lease rejection at some point.

Generally, a company like Steward, with a lot of secure loans, has no advantage in filing bankruptcy. Instead, an out-of-court solution is highly likely. The reason is that in a bankruptcy situation, secure lenders can and often do take the properties back with no hope for Steward itself. Whereas an out-of-court solution may well prove to have a viable solution for Steward. Usually, any lender first goes for a viable entity like Steward as they don't want to operate the properties themselves.

From the price of the stock, one would think that Medical Properties Trust has issues itself. But the financial rating is still high enough that it is not in an area of high bankruptcy probability. It will likely be monitored though and there certainly could be a credit rating drop at the height of negotiations followed later by a restoration once it is clear the solution works. However, there is likewise some risk there as well as sometimes solutions do not work.

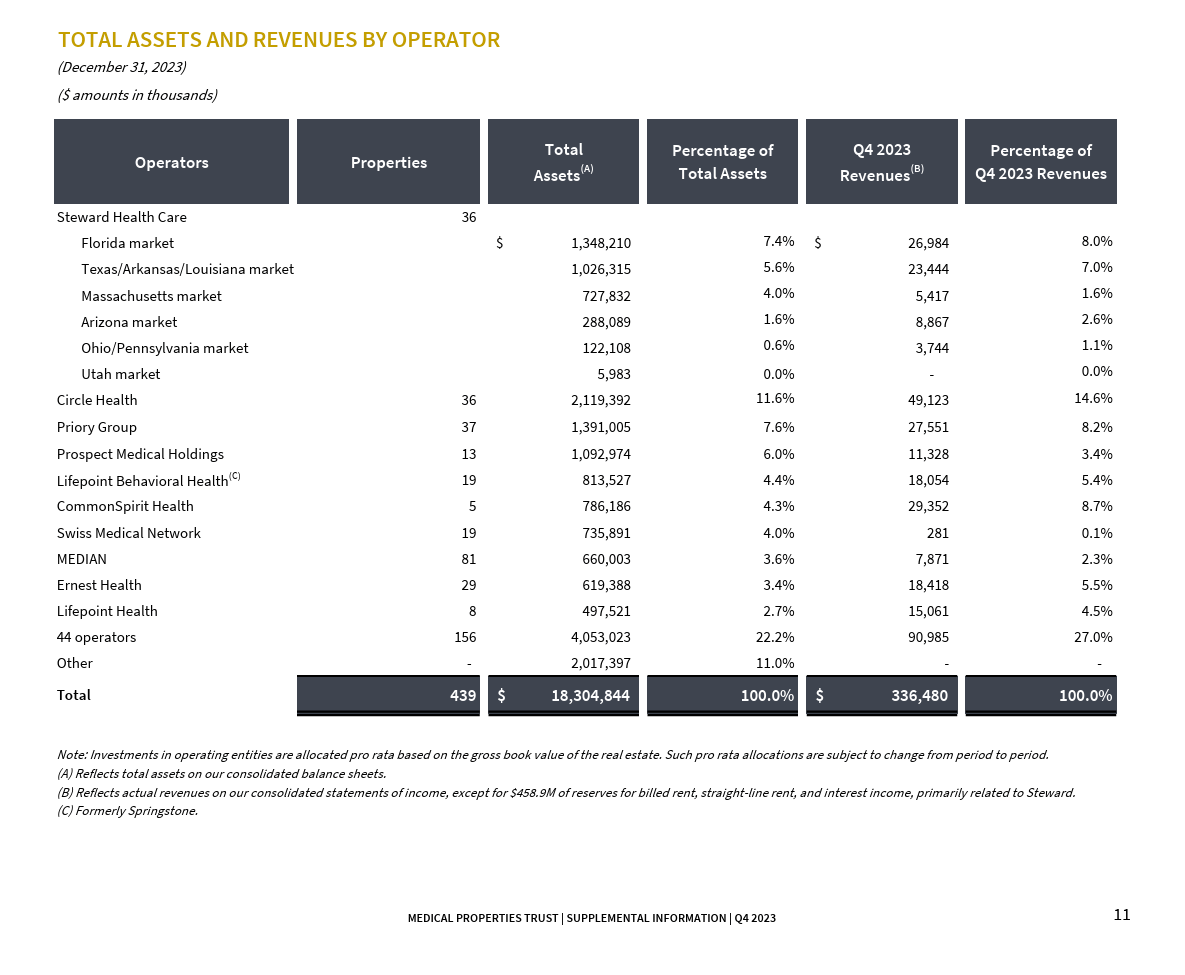

Medical Properties Trust Asset And Revenue By Debtor (Medical Properties Trust Supplemental Information Fourth Quarter 2023)

Steward is very roughly 20% of the business which is important no matter how you want to measure it. However, the risk of loss here would mean that properties have changed unfavorably in value significantly since the appraisals were done. With real estate, that is not likely as long as management did the proper due diligence.

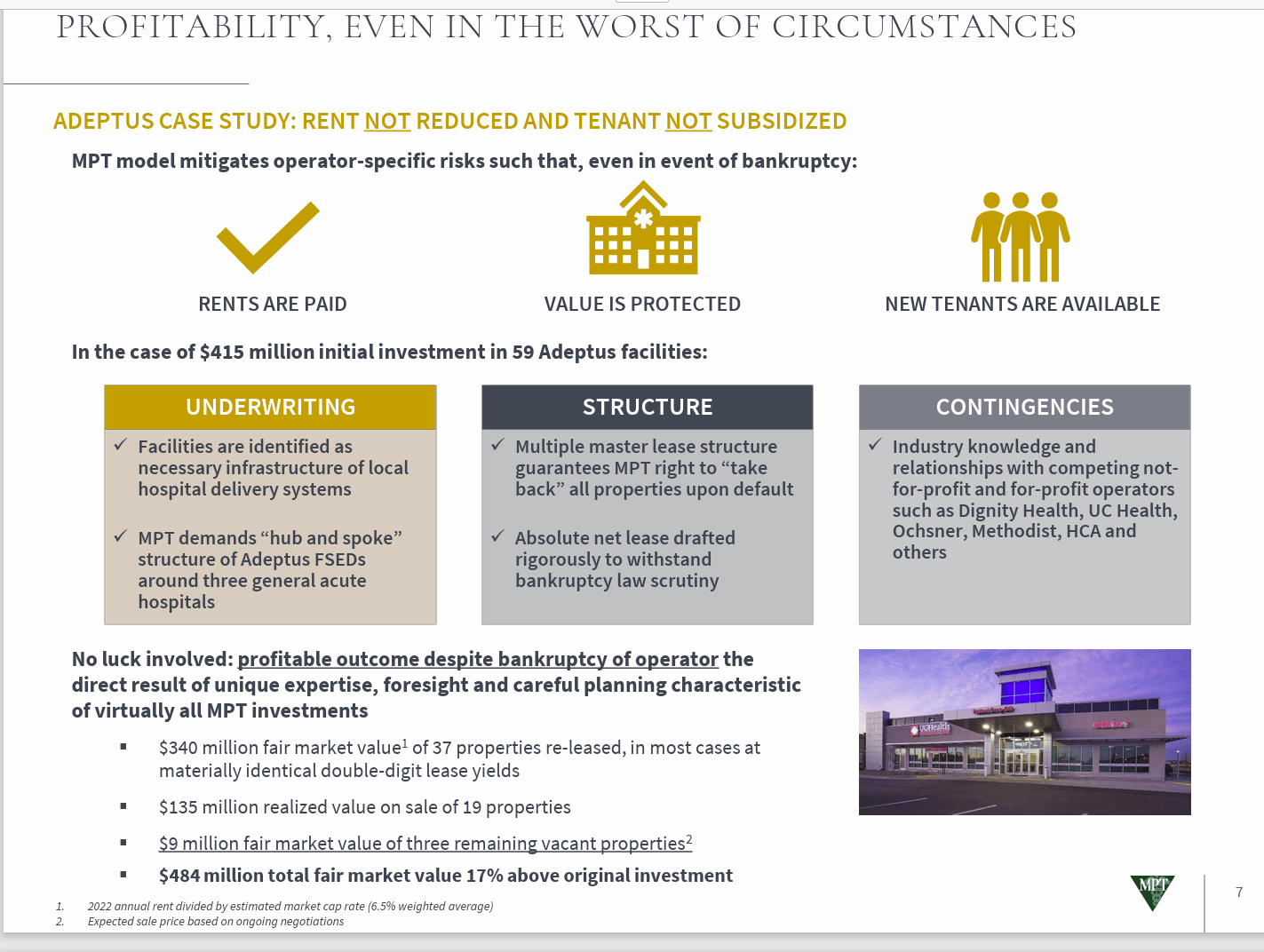

Medical Properties Trust Worst Case Scenario Example (Medical Properties Trust Investor Update April 2022)

Management has demonstrated that in the past, they did fine when the worst case happened (as shown above).

The difference between then and now was that "worst cases" involved smaller operators "once in a while".

But then came the pandemic with some long-delayed after-effects. Investors were spooked when a stronger entity acquired Steward's Utah properties while paying less interest in the lien payment calculation. Left out of that "spooked" was the idea that a stronger entity will not have the challenges Steward has and therefore in the long run could prove to be more profitable even with a lower interest rate used in the calculation.

Also mentioned was that Steward would pay the difference in new payments. That of course, is now up for discussion and negotiation.

This is where the bear case has a field day. Statements about overpayments and overvaluations abound. That goes against the history of the company where the company typically recovers at least all of the value lent. However, should there be enough coronavirus aftereffects, there could be enough properties on the market to cause a value sag. Put that down as another risk (even if it is unlikely to happen).

Worst case scenario would likely be a 25% loss in value as long as the appraisers did their job and management paid attention to market price changes (as well as future risks at the time of the transaction). But that loss would be only 5% of the whole portfolio shown above (as a rough estimate). Most companies can survive something like that and keep going. It would also be unlikely to happen all at once.

Most of the time, if any value impairment happens, it would likely be less than 5% of the assets involved. That would especially be true for real estate assets.

Most companies with leases hope for lien rejection because they can then negotiate higher lease rates during times of higher interest rates. Higher interest rates usually come with inflation. If Steward were to reject every single lease, then there would definitely be a transition period where management would have to scramble, and it could be rough in the short-term. But with inflation coming down, that past inflation should bode well for any new leases that need to be done.

Probably the worst case in the mind of Mr. Market is high interest rates and a need to refinance the debt with inflation coming down. But with a decline in inflation, there is usually a decline in interest rates. The market can be messy about this. But the relationship is well established.

Medical Properties Trust management has long demonstrated that they have "inflation proofed" the leases to the extent possible.

To summarize, here are some of the main risks going forward:

Management did not do its job when creating the lease. Therefore, the leasing conditions and security provide inadequate protection.

The negotiating team either endangers or gives away the superior lien position in negotiations without adequate compensation.

Management was lax about "mission critical assets". The location of the assets is not what management has advertised. Therefore, the assets are in for a big price decline should Steward reject all of the leases. Combine this one with Steward will reject all the leases and there will not be another buyer out there for anything close to the original price. Keep in mind that the company history argues against both of these. But the market seems bent on these, and it has affected the stock price. Any indication that management is correct during the future settlement could send the stock price soaring.

Steward is about 20% of the business. The market is clearly looking for big losses. But typical losses in the 5% of the assets involved is about 1% (if that) of the total portfolio. Most companies can handle that.

There is also a chance of an extended reorganization. Out of all the market worries, this one can turn out to be realistic.

For me, there is no rush right now to jump back into the stock. I may initiate a small (very small) position in the near future as this unfolds. But I will likely wait for more certainty. As the Evolution Petroleum incident proved, the stock price is going nowhere until there is more clarity. Even after Denbury emerged from bankruptcy, Mr. Market was still worried. Of course, Denbury was acquired by Exxon Mobil (XOM), so there are no partnership worries anymore.

While this whole thing was unanticipated, the stock is somewhere between a hold for many and a strong buy for a few in this specialized situation. The risk is clearly elevated, and the stock should be part of a basket of stocks so that one can still sleep at night even if this one blows up. For me, the original holding was barely under 2%. Therefore, the next round of dividends clearly made up for any "losses" while the wash rule allows for the taxes to eliminate some of the losses.

However, the chances of the company getting out of this situation in decent shape are pretty good. So, there is good recovery potential. Some, like me will choose to wait, while others will establish positions because they are comfortable with that additional risk and know how to handle it.

For that reason, I will cover this until the situation ends to see where we all end up. In the meantime, it is time to do some more work as the Steward situation unfolds. I like management's chances. But Mr. Market needs to be dealt with and I am dealing with Mr. Market.