Richard Drury

Richard Drury

Legendary investors Warren Buffett and Peter Lynch have both used versions of the quote:

Selling your winners and holding your losers is like cutting the flowers and watering the weeds.

This quote is so true and - as a value investor - can be quite difficult for me to apply consistently. If a stock runs up rapidly in price for me, I tend to want to sell it and when a stock collapses, I tend to want to buy more. While sometimes that makes sense, it is always essential to look below the hood first to see if there is a good reason why the market is bidding up one stock and dumping the other. Moreover, Mr. Market has an uncanny ability to predict the "random" breaking of both good and bad news with its pricing movements. Many times when a stock makes a sharp move higher or lower, it seems like a previously unknown positive or negative catalyst comes to light (though of course, this is not always the case as sometimes sharp market moves are spawned by nothing more than excessively bullish or bearish sentiment).

As a result, it is generally prudent to hold on to a winning business model as great businesses and great management teams tend to create their own "luck" and it is generally prudent to dump a losing business model as bad businesses and bad management teams tend to create their own "misfortune."

Here are two examples of winning stocks that I believe are worth holding on to despite recent sharp moves higher in their stock prices and two examples of losing stocks that I believe are worth dumping despite recent sharp moves lower:

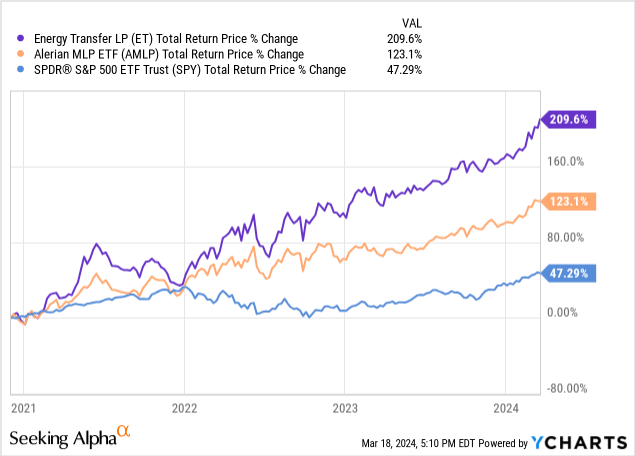

Midstream energy infrastructure giant ET units have soared higher over the past three and a half years as management has successfully accomplished its objectives of:

As the chart below illustrates, ET has been a massive outperformer since I added it to my portfolio on December 3, 2020:

However, the common equity still yields 8.4% on a next twelve-month basis and is very well covered by distributable cash flow, the balance sheet continues to grow stronger, and management has guided and is delivering on a 3-5% distribution per unit CAGR range, continues to invest aggressively in growth projects, and has also dangled the potential for unit repurchases in the future depending on market and industry conditions.

As a result, we continue to see ET compounding at a double-digit CAGR moving forward, and - while we may occasionally trim our position slightly as needed to unlock capital for reinvestment in other opportunities - we plan to continue holding a substantial position in ET moving forward. To read my latest in-depth thoughts on ET, click here.

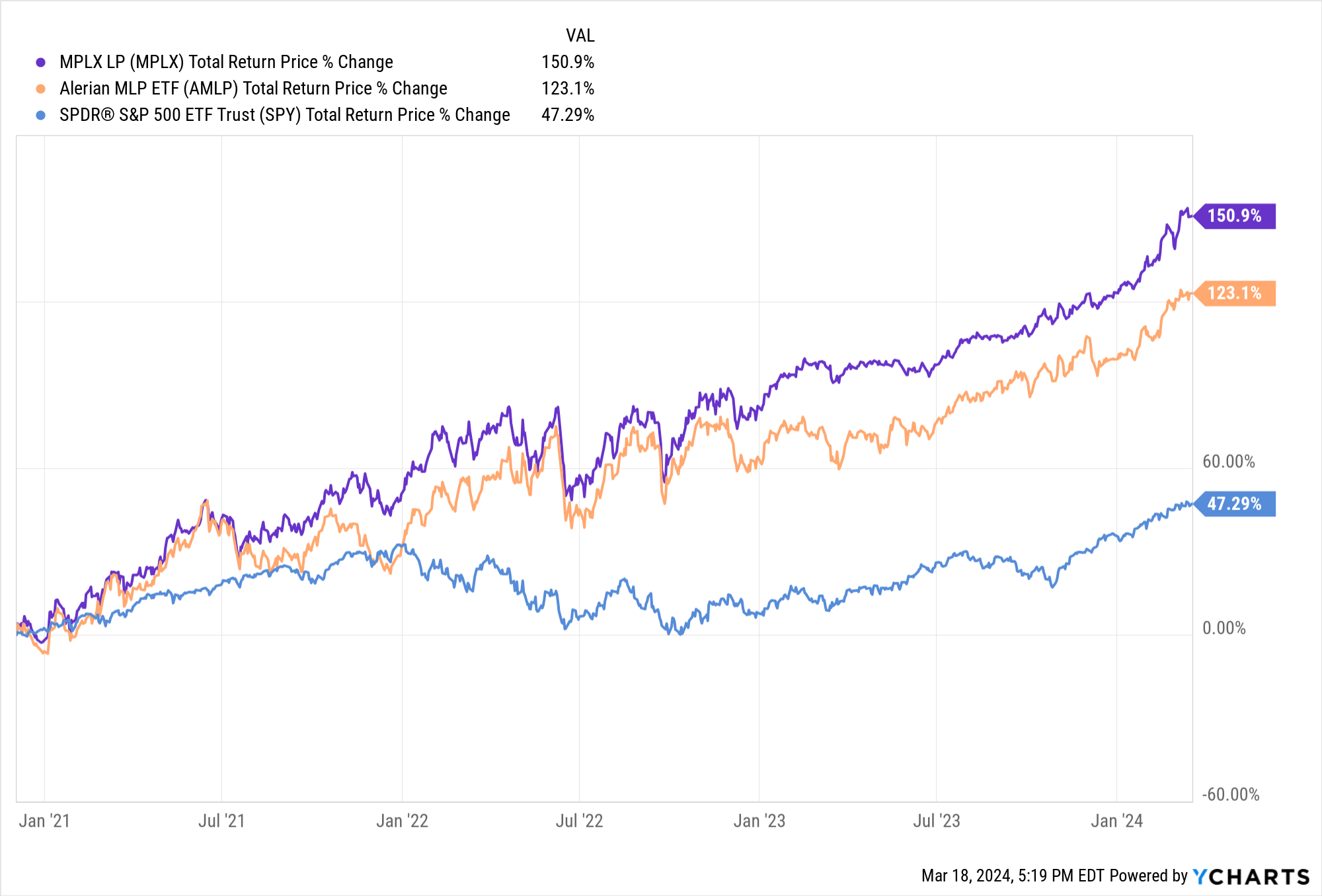

MPLX - like ET - has been a significant outperformer since we launched our portfolio on December 3, 2020:

While I have not added it to my portfolio because I chose ET instead (and am glad I did) if I held it right now, I would likely continue to hold at least some of my position because MPLX - like ET - has a very strong balance sheet, a thriving and defensively-positioned business model, pays out an 8.7% next twelve-month distribution yield that is very well covered by distributable cash flow, and the growth outlook for both cash flows and the distribution remains attractive at a low to mid-single digit CAGR for the foreseeable future.

As a result, it remains positioned to deliver double-digit compounded annualized total returns alongside fairly low risk, making it an attractive holding in a total return-focused income portfolio. To read my latest in-depth thoughts on MPLX, click here.

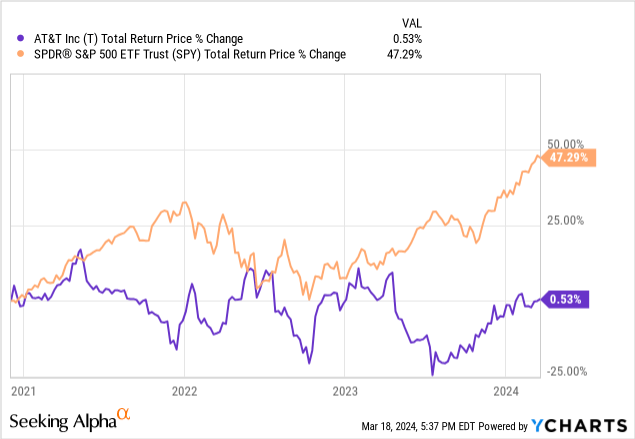

While ET and MPLX are attractive long-term compounders that appear poised to continue delivering attractive risk-adjusted total returns despite their recent strong run-ups in equity valuation, T is a stock that I would avoid buying and would even sell if I held it, despite its significant total return underperformance since I launched my portfolio on December 3, 2020:

While the stock price has been beaten down and its 6.6% dividend yield may look attractive to some investors, its EV/EBITDA valuation actually remains above its long-term average despite interest rates sitting at elevated levels.

Moreover, management remains largely constrained in its ability to return capital to shareholders as it is feeling the need to allocate most of its free cash flow net of the dividend to pay down debt and is also having to invest aggressively in its capital-intensive, low-ROIC business model in order to sustain its competitive positioning against the likes of Verizon (VZ) and T-Mobile (TMUS). As a result, its dividend growth outlook is very poor, with analysts forecasting a meager 1.1% dividend per share CAGR through 2028. Moreover, even its earnings per share outlook is very weak, with analysts guiding for just a 2.8% CAGR through 2028.

When combining its heavily leveraged balance sheet, management's horrible track record, the stock's unappealing valuation, and very weak earnings per share and dividend growth outlook, its 6.6% dividend yield is not high enough to compel me to want to have this stock in my portfolio right now.

Another stock that is not worth keeping right now despite weak recent stock price performance is NYCB. While as recently as two months ago it was considered to be a boring and fairly stable high-yield regional banking stock, the sudden emergence of underlying issues at the bank, including a large increase in loan loss reserves, regulator pressure that likely forced the company to slash its dividend, and material weakness in its internal risk control processes that led to huge write-downs in book value, a significant restructuring of the management team and board of directors, massive declines in the stock price, and eventually a significant change in the company's ownership structure.

While the stock currently trades at a meaningful discount to its tangible book value (which is likely in the $6-$7 per share range right now) and the bank appears to be on firmer footing, the fact that it pays little to no dividend, continues to be plagued by considerable uncertainty in the quality and future performance of its loan book, shareholders have recently gotten massively diluted through the deal to bring in $1 billion in outside equity, and the new CEO is making a very hefty salary, all signal that this remains a very speculative investment at best and does not indicate a company that is positioned to be a dependable long-term compounded.

As a result, it would take a much larger discount to book value to entice me to consider buying shares right now. You can read more details on my thoughts on NYCB here.

Buffett and Lynch are both some of the greatest stock market investors in history and a big part of that is because they knew when to cut their losers and let their winners run.

While the high-yield space is not quite as conducive to the buy-and-hold investing strategy (and I do not practice strict buy-and-hold investing for that very reason), there are still times when it makes sense to hold on to your winners. ET and MPLX are two classic examples of this given their fundamental strength and continued attractive yield plus growth profiles. Meanwhile, there are always cases where seemingly "cheap" high-yield stocks actually look like they could very possibly get even cheaper. As a result, I try to make a point of avoiding these stocks or selling them if I hold them. While it is always painful to sell a loser and lock in permanent losses, it is a far bigger mistake to hang on to perennial underperformers when that capital would have been much more prudently allocated to winners.