Photofex

Photofex

MP Materials Corp. (NYSE:MP) is a leading producer of rare earth elements. This mining facility is located in Mountain Pass, California, which is near the Mojave National Preserve. The rare earth elements that it produces are used in so many products that are critical for our modern life. They are used in clean energy, automotive, military, and many high-tech products. What makes this situation unique is that MP Materials is one of the few producers in the Western world. These elements cannot be sourced effectively in most countries and the ones that have significant rare earth resources are countries like Russia and China, which may not be willing to export these materials now or in the future. These rare earth elements include lanthanum, NdPr Oxide, and Cerium.

Because of China's weaker-than-expected economy and other factors, the prices of rare earth elements have been declining, and this has put some margin pressures on MP Materials for the past year or so. However, prices seem to have stabilized and are expected to rise going forward. This should drive earnings higher for MP Materials, as well as the stock price, which is now trading near 52-week lows.

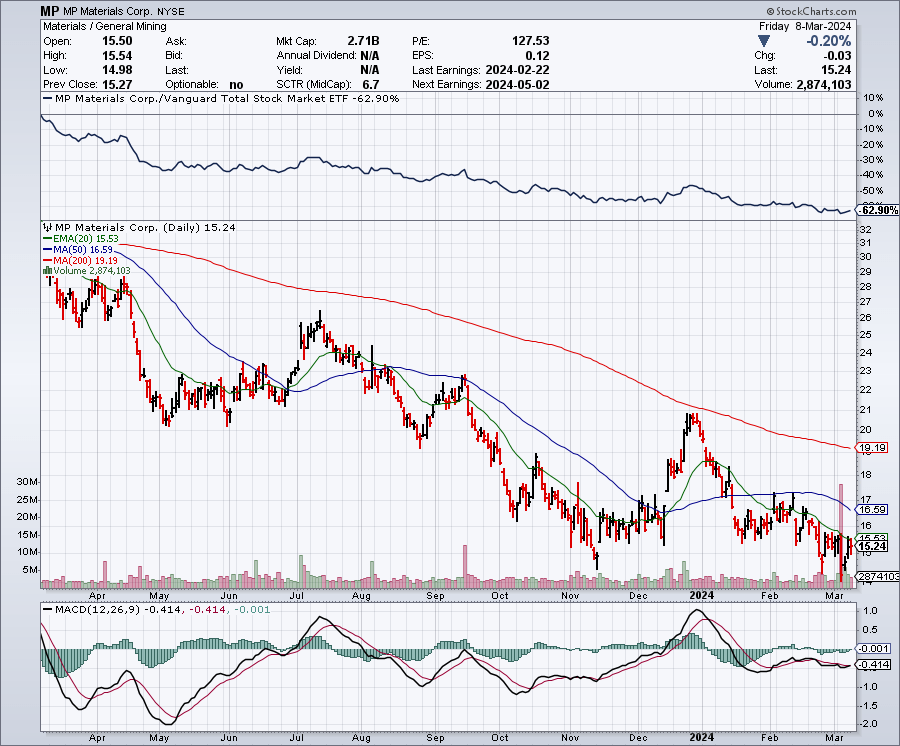

As the chart below shows, this stock bottomed out in the $14 range in November, and it recently tested that level again and has bounced back over $15. It is too early to say for sure, but if this holds, this could be a very bullish double-bottom formation on the chart. The stock is trading slightly below the 50-day moving average, which is $16.59 per share. The 200-day moving average is around $19.19 per share. The 200-day moving average has been steadily drifting lower over the past few months, which is putting it closer to the 50-day average. This could be setting this stock up for a very bullish golden cross formation in the not-too-distant future.

StockCharts.com

Analysts expect MP Materials to earn about 11 cents per share on revenues of $260 million in 2024. However, earnings and revenues are expected to surge going forward. For 2025, estimates are at $1.02 per share, with revenues coming in around $635 million. For 2026, earnings estimates are at $2.49, with revenues potentially at $1.16 billion. This suggests MP Materials is trading for just about 15 times estimates for 2024 and only 5 times earnings for 2026. This is a dirt cheap valuation, especially for a company that is growing as fast as this one.

As shown below, demand for rare earth elements is expected to grow significantly over the years. In addition, the supply will remain constrained and this could lead to a surge in prices. Based on this, it appears that now is a great time to invest in this industry. I think this is an ideal opportunity to buy and hold on to your shares, letting these supply/demand dynamics run their course and benefit your portfolio in the process.

Adamas Intelligence, "Rare Earth Magnet Market Outlook to 2040", (Q2 2023)

The geopolitical developments in the past couple of years have created a trend for onshoring and making sure that critical supplies are not cut off inadvertently by a war, for example, or by adversaries. Countries are becoming more protectionist, especially when it comes to goods that are used in high-tech products. In December 2023, China announced a ban on rare earth technologies, and this makes the need for a Western world supplier like MP Materials even more important.

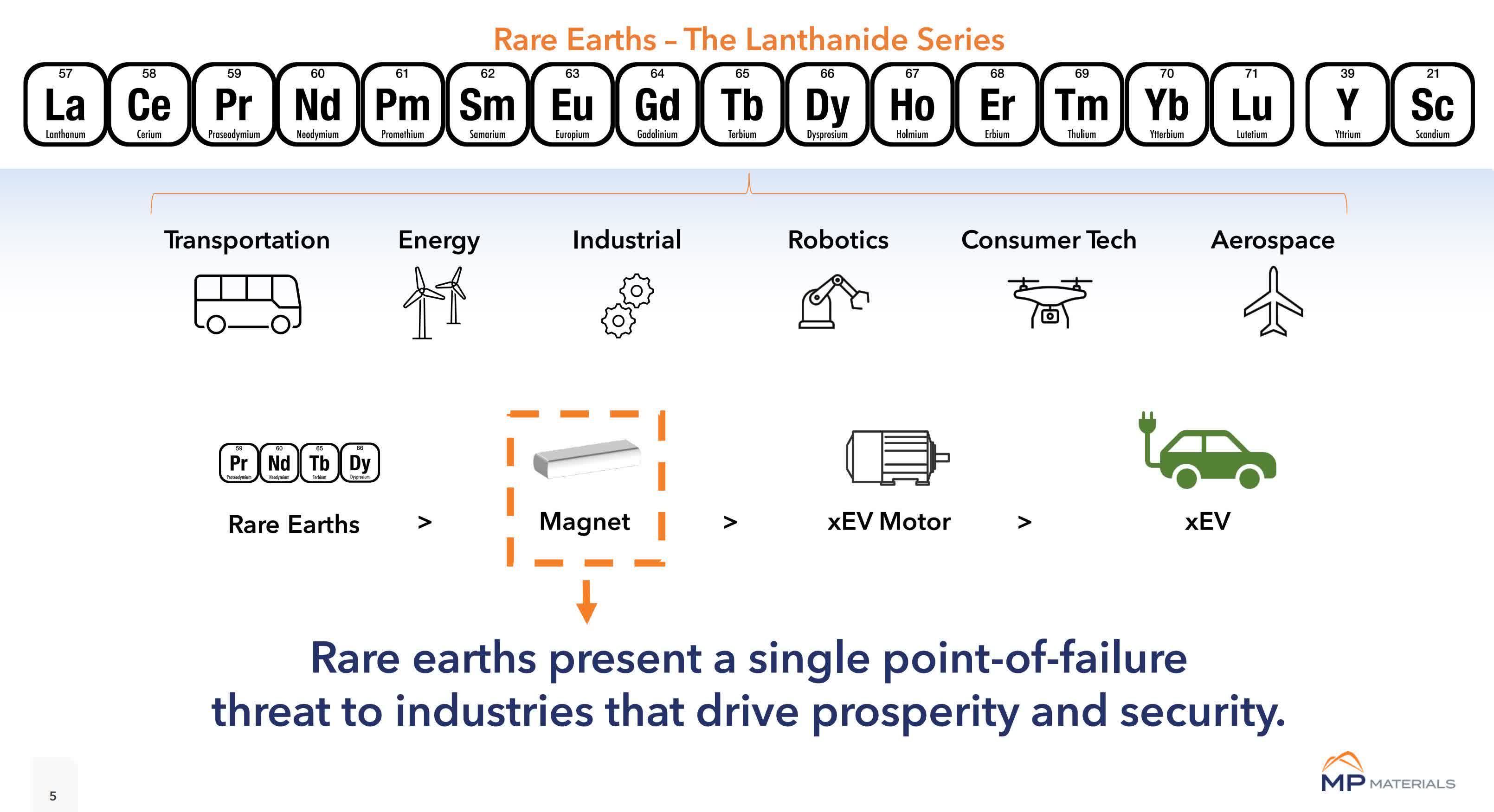

Although most people probably never spend time thinking about rare earth elements, this industry is critically important to just about everything we take for granted in our daily lives. The graphic below shows many industries that use rare earth elements such as robotics, military, aerospace, consumer technology (such as smartphones, drones, etc.), electric vehicles and so many more. As this graphic points out, the lack of supply of rare earths could represent a point of failure for many industries and the Western economy. We have seen an increase in bans on certain exports, including chips and rare earth elements, which makes MP Materials a critically important supplier.

M P Materials

This stock topped out at around $60 in 2022 (when rare earth prices were higher) but has declined significantly since, and now trades for just about $15. This could be an opportunity to buy at or near cycle lows, and there could be a lot of upside even if this stock just trades for half of its 2022 high. Analysts expect rare earth element pricing to strengthen in the second half of 2024, and this should lead to improved profit margins for MP Materials. On March 4, 2024, this company announced a $300 million share repurchase authorization. MP Materials has a strong balance sheet, with nearly $1 billion in cash, and around 694 million in debt. This company is clearly important to national security and in 2022, it was even awarded a $35 million contract from the Department of Defense.

The price of rare earth elements can be volatile and the share price of this stock is also very volatile. In recent trading, there have been days where this stock moves 5% or more intraday, so be prepared for wide swings if you buy this stock. This industry can be heavily impacted by China, which is a leading producer, and this is a potential risk factor. The mining industry comes with many safety and regulatory risks. According to Shortqueeze.com, about 17.6 million shares are currently short, and this represents about 12% of the outstanding shares. Obviously, the shorts have been capitalizing on the weaker prices for rare earth elements, and they have ridden this stock down to 52-week lows recently, so there is a bear case to be made. (However, the trend for lower rare earth pricing seems to be ending and shorts could fuel a big rally in the stock from these low levels.)

This stock looks attractive around the 52-week lows, and the trend for lower rare earth prices seems to be coming to an end soon. The long-term outlook for this industry looks very bright based on the supply/demand ratio in future years. This company has a strong balance sheet-it recently announced a $300 million share buyback, and the stock looks cheap based on forward earnings estimates. I think this stock could be trading at much higher levels in the near future, just as it was a couple of years ago. I would not make a big allocation to this stock, but I believe buying some shares makes sense. I am adding on weakness and buying in stages. I am also selling put options in order to benefit from the very strong option premiums that this stock offers.

No guarantees or representations are made. Hawkinvest is not a registered investment advisor and does not provide specific investment advice. The information is for informational purposes only. You should always consult a financial advisor.