izusek/E+ via Getty Images

izusek/E+ via Getty Images

It's February, and love is in the air. For the biotechnology sector, that means M&A activity. In line with this, Novartis (NYSE:NVS) announced yesterday its intention to become one with MorphoSys (NASDAQ:MOR), a Germany-based biopharmaceutical company that develops medicines for cancer, for EUR 68 per share, or an aggregate of EUR 2.7 billion in cash. The acquisition is expected to be completed before July.

Novartis had recently been rumored to be in late talks with cardiomyopathy drug developer Cytokinetics (CYTK) in a deal valued over $10 billion, but the duo later broke up, per reports, and Novartis has since stated their commitment to "bolt-on" deals under $5 billion.

MorphoSys and Novartis have a history together. They had been partnering on the development of ianalumab for the treatment of autoimmune disorders such as lupus nephritis.

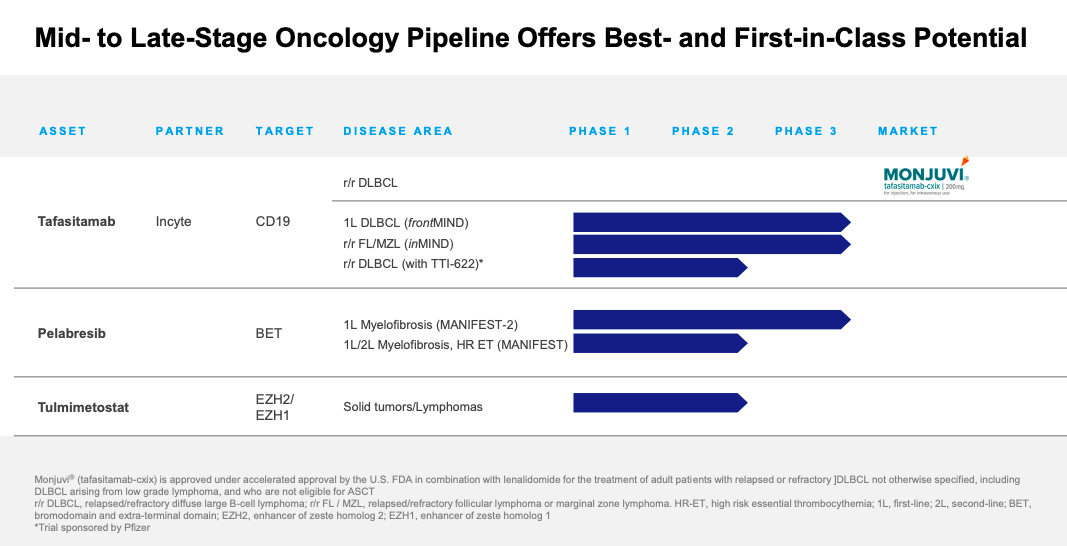

This bolt-on deal will grant Novartis access to MorphoSys' extensive oncological pipeline.

MorphoSys' investor deck

Pelabresib, a first-in-class oral inhibitor of BET proteins, is a potentially game-changing treatment option for myelofibrosis; it was well-tolerated when combined with ruxolitinib, and in the Phase 3 MANIFEST-2 study in patients who had not yet taken a JAK inhibitor, the combination showed encouraging trends in symptom improvement as measured by the important secondary endpoints of absolute and 50% change in total symptom score at week 24 relative to baseline. This is probably the most intriguing asset and will likely be a part of the treatment arsenal for addressing myelofibrosis.

Interestingly, Novartis owns the drug pelabresib was paired with in MANIFEST-2; this drug is known by the trade name Jakafi. Therefore, MorphoSys is probably a strong fit for Novartis, as it expands their cancer portfolio and gives new impetus to their research.

Per Seeking Alpha, Novartis' financials, featuring $14.07 billion in cash and a robust operational cash flow of $14.46 billion TTM, alongside a total debt of $26.44 billion, highlight its capacity to fund the MorphoSys acquisition comfortably. With a debt-to-equity ratio of 56.55% and liquidity ratios—current ratio at 1.16 and quick ratio at 0.88—indicating sufficient short-term asset coverage for liabilities, the company's balance sheet reflects a reasonable financial stance. The levered and unlevered free cash flows of $12.13 billion and $12.67 billion TTM, respectively, further underscore Novartis' ability to pursue strategic investments without compromising its liquidity or solvency. Given the acquisition cost of approximately $3.1 billion, Novartis’ ample cash reserves, coupled with its effective cash generation and manageable leverage, affirm its financial readiness to enhance its oncology portfolio through this acquisition. The strategic expenditure on MorphoSys aligns with Novartis' long-term objectives, demonstrating a judicious allocation of capital that supports both immediate financial health and sustained industry leadership.

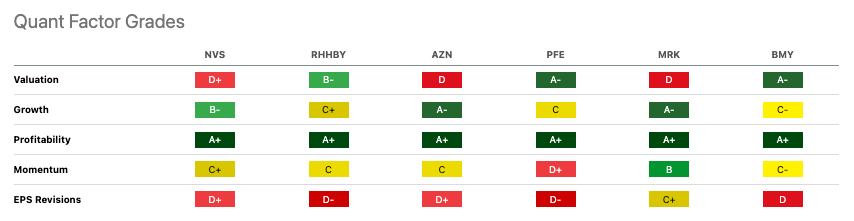

When comparing Novartis with its industry peers—Roche (OTCQX:RHHBY), AstraZeneca (AZN), Pfizer (PFE), Merck (MRK), and Bristol Myers Squibb (BMY)—using Seeking Alpha's Quant Grades, the financial and operational metrics offer a detailed perspective.

Seeking Alpha

Novartis excels in profitability, securing an A+ alongside all peers, underscored by a superior gross profit margin of 74.24%, reflecting its operational efficiency. Despite a valuation grade of D+, suggesting a less favorable market perception compared to Pfizer's A- and Roche's B-, Novartis' revenue growth of 7.36% is commendable, outpacing Merck's 4.51% and indicating robust sales expansion.

In terms of growth, Novartis' B- grade, although surpassed by AstraZeneca (A-) and Merck (A-), still signifies strong future earnings potential, especially with a revenue figure of $46.66 billion. Momentum, marked at C+ for Novartis, suggests some challenges in stock performance but remains ahead of Pfizer’s D+. EPS revisions for Novartis at D+ reflect industry-wide analytical adjustments, with its EPS diluted TTM at $7.10 suggesting a resilient profit per share.

The net income of $14.85 billion, with a net income margin of 31.83%, emphasizes Novartis’ profitability. Its revenue per share of $22.47 further positions it as a formidable competitor within the sector.

To summarize, Novartis' bold bid for MorphoSys, cumulating in a EUR 2.7 billion investment, marks a deliberate foray into oncology, enriching its collection with assets like pelabresib. Such a move not only cements Novartis' market stature but also mirrors its fiscal prudence, using strong financial reserves and cash flows for growth and keeping liquidity intact.

My recommendation on Novartis is "hold" as the firm blends MorphoSys' pipeline into its cancer arsenal. Watch closely for pelabresib's clinical journey and market positioning, alongside Novartis' tactics to fortify its biotech standing. While financials and efficiency speak to a robust base, valuation hesitancy calls for measured hope.

Risk mitigation for investors hinges on Novartis' integration efficacy, regulatory nods, and oncology additions' performance. Sector diversification, a sharp focus on Novartis' post-deal strategy and operations, and awareness of industry shifts and regulatory dynamics will guide investor adjustments, promoting a well-guarded, diversified investment stance.