Oscar Wong/Moment via Getty Images

Oscar Wong/Moment via Getty Images

Hello Group's (NASDAQ:MOMO) continuous focus on cutting costs and efficiency improvements yield promising results for the bottom line despite declines in revenue and users. Management continues to be very savvy in milking the cash cow business that is Momo, and profits continue to show despite macroeconomic headwinds in China. Assuming a stable user base and modest revenue declines, I believe Hello Group's profits will likely be substantial going into the future which gives investors an opportunity to buy earnings on the cheap. Future growth will likely come from the new apps they've started which has seen significant traction and can contribute to the bottom line going forward.

Hello Group owns two core apps that make up most of their business at the moment: Momo and Tantan.

Momo started in 2011 as a dating platform but eventually evolved into a social networking tool which allows users to find and connect with people nearby based on their location. This meetup model was popular as lots of young people are looking to make new connections and expand their social circle, which really appealed to Momo's unique value proposition. It was real-time, based on location, and had that freshness to it that made people want to try it out. Management capitalized on user growth and monetized it through livestreams, memberships, online games, and other paid features for users.

Tantan was acquired in 2018 for over $600M by Hello Group, formerly called Momo, and is commonly referred to as the "Tinder" of China. It quickly gained traction, as it copied many features from Tinder that had a proven track record of success. Like Tinder, Tantan also features swipe-based matching, location-based preferences, and the opportunity to build an attractive profile. It is currently one of the most popular dating apps in China. Like Tinder, Hello Group has monetized Tantan through in-app purchases, membership subscriptions, virtual gifts, and livestreaming.

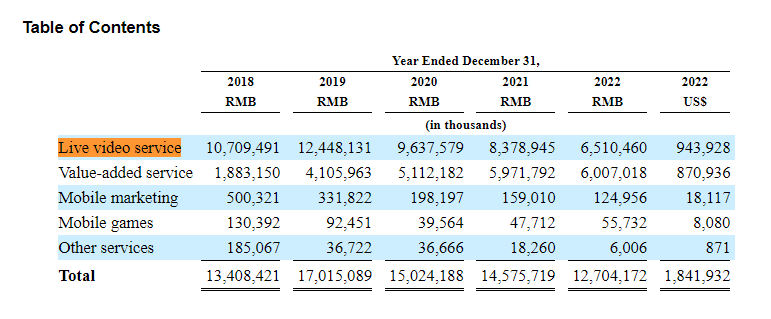

All in all, Hello Group makes money primarily through live video services and value-added services. Live video services make up 51.2% of revenues for 2022, and the money mainly comes from virtual gifts and splitting the income broadcasters get from livestreaming on the platform. Value-added services make up 47.3% of revenue for 2022, and it mainly comes from membership subscriptions and virtual gifts. Paid members get benefits such as advanced search options, discounts in the emoticon store, and ability to see recent visitors on your profile.

Annual Report 2022

Many young people in China are already familiar with the app "Momo" as it blew up in popularity back in 2012-2013, when user growth almost quadrupled. MAUs went from 22 million to 84 million in just a year, explosive growth for any social media app. However, since then Momo has had its issues retaining and growing its user base as the freshness and coolness of the app no longer remains. MAUs declined from 114 million to 95 million from 2021-2022, and that trend is continuing downwards. Management attributes this to COVID 19, citing lockdowns and social distancing measures. However, since the pandemic in China, young people haven't returned their activity on Momo. According to Hello Group's Q3 2023 Press Release, "For the Momo app total paying users was 7.8 million for the third quarter of 2023, compared to 8.4 million for the same period last year."

The same goes for Tantan. According to the Q3 2023 Press Release, "Tantan had 1.4 million paying users for the third quarter of 2023 compared to 2.0 million from the year ago period." Even more, Tantan has had its own host of issues such as a major imbalance of male-female users on the app. As of 2022, 85% of Tantan's users were males, which is a big problem because it creates a hyper competitive environment that diminishes value for all users on the platform. Furthermore, it seems that spammers and fake accounts are everywhere on the app, according to user reports on the internet. Management has indicated they are fixing the spamming problem, according to their recent earnings transcript, "On the product and operational front, the biggest achievement in the third quarter is that we managed to maintain spamming activity to a low level significantly, and therefore, the community returned to normal."

Ultimately, the backdrop for Hello Group is that paying users continue to dwindle on both apps as revenues decline. It seems that for the most part management is trying to keep the user base steady, and acknowledges the matureness of Momo. But, macroeconomic challenges create a difficult environment as the paying user base continues to be under pressure.

Despite revenues and user decline, management's cost cutting efforts should be applauded for keeping the bottom line in good shape.

According to the press release Q3 2023 management states, "The group level profitability continued to grow from the prior year period, thanks to our effective cost optimization and efficiency improvement initiatives." Management has been ruthless in cutting costs related to staff efficiency, cutting features and activities that create little value, trimming marketing expenses, and lowering unit acquisition costs. As a result, bottom line numbers showed remarkable improvement despite revenue declines, "Net income attributable to Hello Group Inc. was RMB1,505.1 million (US$206.3 million) for the first nine months of 2023, compared to RMB1,086.3 million during the same period of 2022." This nearly 40% increase for the first nine months ended Q3 2023 is quite impressive and has boosted profit margins to "22.4%, up 3.7 percentage point year-over-year and down slightly, 0.2 percentage point quarter-over-quarter" according to the earnings Q3 2023 transcript.

My main point for this thesis boils down to my belief that these cost cutting measures will continue to hold profits up long enough until management can turn around the top-line to stability. Until then, even with modest declines in revenue the earnings will likely be substantial. Furthermore, buybacks can continue to drive EPS growth as management has stated they still have $110 million ready to deploy in the earnings call.

Hello Group can likely restore top-line revenue through taking the cash from Momo and redeploying it into Tantan and some of the other newer apps they have launched overseas. It is unlikely that Momo will return to its former glory, so the growth story has shifted to these newer apps Hello Group has launched.

In particular, apps like Hertz, SoulChill, Duidui, and the newest one inSpaze all have unique value and are seeing traction. According to management in the earnings transcript, "And as a result, revenue from these new endeavors in 2022 increased around 1.5x compared with the previous year. The incremental revenue not only offset the decline in VAS revenue from Momo and Tantan, but also drove a slight increase in our group's VAS revenue despite several unfavorable external factors."

Honing in on the newest app, inSpaze was recently announced as an immersive social app for the Apple Vision Pro. Users can immerse themselves in a world of their own, and it reminds me of the Metaverse when looking through its features. While still in early stages, it proves that management is innovating and thinking about the new era of social networking in the virtual space. I believe new initiatives such as this can offset the decline from the older Momo that is losing a bit of its freshness.

Furthermore, Tantan is still untapped in terms of potential. Myriad issues exist as previously mentioned, from fake accounts to an imbalance of males to females, yet I still believe management can fix these problems. If they can succeed, Tantan alone can be as valuable as Tinder, which made $1.79 billion of sales in 2022. Tantan currently makes sales of ~$200 million in 2022, so there's potential for increase if management can get the app working well again.

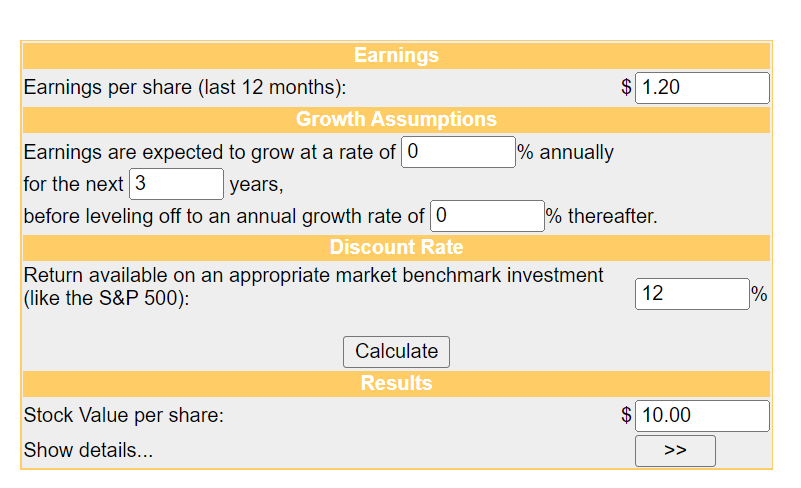

For valuation, I estimate earnings power and apply usually a conservative multiple. Starting with TTM revenues of $~1.7 billion, I expect the revenues to decline around 7% year over year for 2 years and then stabilize at around $1.5 billion. Given the decline in paying users for both Tantan and Momo, a weak macroeconomic environment, and management guidance of a decrease in revenues of around 6-9%, I picked 7% as a midpoint.

Eventually, I think after 2 years the top-line growth from new apps and Tantan should start to offset the decline of Momo, reaching a stabilizing point of $1.5 billion in revenue. I highly doubt revenues will go below $1.5 billion because I feel that management can eventually stop additional paying users from leaving their legacy apps, while simultaneously growing paying users on the newer apps. I expect net margins to remain strong due to cost cutting initiatives, around 15%. 15% is actually below the current profit margin of 22%, which is realistic as the business may see some additional overhead grow with the development of their new apps, cutting into the net margin. Based on these calculations, earnings should range around $200 million to $250 million for the next few years. ($1.5 billion x 0.15 = $225 million)

Divide $225 million by 190 million shares outstanding and you get EPS of ~$1.2. Apply a very conservative earnings multiple of 8, and $1.2 x 8 = ~$10.

I applied a low multiple to account for the sheer uncertainty of the business. Management may not be able to fix Tantan, and Momo's decline could be worse than imagined. So, upon accounting for modest revenue declines, EPS still remains pretty attractive given cost cutting and share buybacks from management.

MoneyChimp DCF Calculation

Risks involved in buying stocks in China are mostly geopolitical and macro. The main concern right now is the impending real-estate crisis, which is affecting a lot of consumer wealth and spending in China.

Historically, Chinese people loved buying real estate as prices kept going up annually since the 1998 housing reform. In the beginning, people may have been skeptical, but after years of watching home prices go up they threw in the towel and prices continue to elevate year after year. Thus, most Chinese households have a lot of money tied up in real estate for investment purposes. Because of real estate prices declining, Chinese people are seeing their wealth being wiped out steadily.

Logically, the last thing someone thinks about is purchasing virtual gifts for their favorite broadcaster when they've seen their wealth disappear overnight. So, the macro backdrop is tough and little virtual gifts and in-app purchases are likely the first expenses to be cut for individuals living in China.

Furthermore, regulation from the PRC can always be trouble for Hello Group. In the past, the Chinese government has ordered Tantan to be removed from app stores due to a violation of policies. Hello Group's apps have also dealt with a past reputation as a place for prostitution, which has seen bad press and intense government scrutiny.

Competition in the social networking space is intense, as many international players have entered like Tinder and Bumble that are all competing for young people's attention. These companies have proven track records and apps that are currently functional, which poses a major risk to Tantan as users may switch without that much difficulty.

And finally, don't forget about tensions between US and China which could escalate and decrease investor confidence and trust in Chinese markets, leading to price declines regardless of fundamentals.

CEO and Chairman Yan Tang has a founder's mentality, being one of the co-founders of Momo since inception. He has been there from the start, which I believe makes him motivated to keep his business afloat and profitable. Notably, he owns 21% of shares outstanding, and most of his net worth can be tied to his company. His knowledge and expertise in the social networking business is very strong and I believe his track record of growing Momo gives him the experience necessary to turn his business around.

Since his tenure in 2011, revenues from literally $0 to over $1.7B today. Users went from nothing to around 100 million MAUs today. A true entrepreneur with the ability to start from scratch, businessmen like him are very rare to find, as most CEOs are hired guns and have no experience starting companies. Some of his innovations was to start location-based instant messaging and a core focus on creating value for young adults in China.

I believe his talent is noticing gaps in the market, and driving aggressively to create value for young adults with products that serve an unmet need. Although Momo is slowing down, international markets outside China present compelling opportunity for Mr. Tang to do it again outside China. If he did it once, I think he may be able to do it twice.

In conclusion, I still believe that Hello Group presents a buying opportunity because of its cost-cutting initiatives, top-line stabilization and growth from new apps, and the potential for a revamp of Tantan creates significant upside. However, this stock is a little more uncertain and murky as the revenues and users continue to show weakness. Still, the earnings are there miraculously, and I'm impressed enough to give this one a chance given its low valuation. My $10 price target presents 50% upside to investors who are willing to give love and social connection a chance in China.