Bim/E+ via Getty Images

Bim/E+ via Getty Images

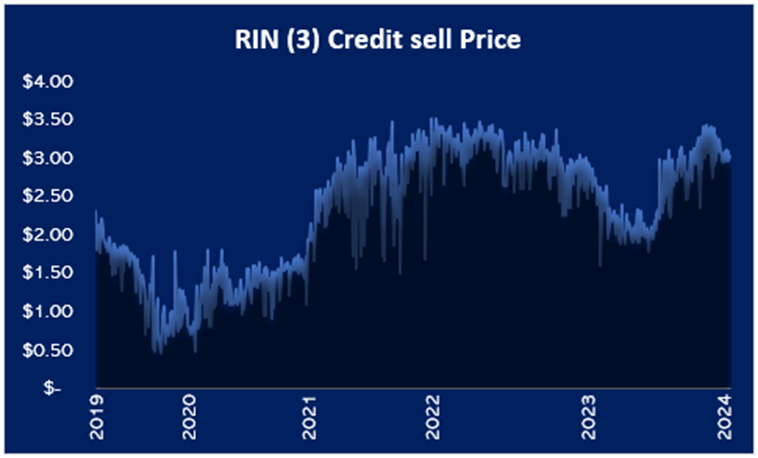

Montauk Renewables (NASDAQ:MNTK) is one of the leading U.S. companies in RNG (renewable natural gas) production and sales, with a share of around 10% of the entire RNG landfills market in the United States. The stock has declined more than 75% from its high in September 2022, mainly due to the volatility in the price of RIN(D3).

RIN(D3) is partly caused by an oversupply phase that is likely to have negative effects on 2024 prices as well. In the long run, however, the MNTK's business has a solid foundation for growth, supported by federal and state incentives that aim to increase the share of RNG to 3% of total gas used in the U.S. by 2050, up from 0.5% in 2023, implying at least a 6-fold expansion of the entire industry. At the same time, the environment appears to be very competitive, seeing the participation of both specialized companies, waste management giants as well as some companies involved in gas production and sales. In addition, Montauk's business model has considerable concentration in terms of both suppliers and customers, a factor that although it can be positive and capable of creating synergies, can also represent a major risk in an environment of increasing competition. Considering this, other risks reported during the analysis, and following the results of my DCF, I currently assign MNTK a Hold rating. If interested in the world of renewable energy, on EuroEquity Research you'll find several analyses of companies operating in it.In 2023, with an output of 5499 MMBtu Montauk emerges as one of the leaders in RNG obtained from landfills. FY22 data show a market share of 9.1%. The landfills segment is the type of RNG characterized by the highest annual production, far surpassing livestock, and food waste, allowing MNTK to position itself with a 6.2% share in the entire RNG market, without considering renewable electricity production.

However, most of Montauk's production sites are owned by companies such as Republic Services (RSG) and Waste Management (WM), which in exchange for the sale of operations receive a royalty based on the company's revenues. As of Dec23, 37.3% (vs. 38.9% as of Dec22) of its projects are placed in Waste Management operated landfills while 22.2% (vs. 25.1% as of Dec22) at Republic Services operated landfills. This business model creates a great dependence on other companies that may even choose to do in-house what is entrusted to Montauk. A possibility that is already looming in part, with WM's decision to create its own portfolio of RNG projects and the creation of a Joint Venture between RSG and BP, through Archaea Energy, aimed at building new proprietary plants. The trend toward verticalization of waste management companies, coupled with the growth of competitors already in the market among Clean Energy Fuels (CLNE), OPAL Fuels (OPAL), Gevo, Inc. (GEVO), and AMP Energy are likely to weigh negatively on the development of new projects, with serious repercussions on MNTK's future economic and financial performance.

MNTK SEC Filings and Author's Analysis

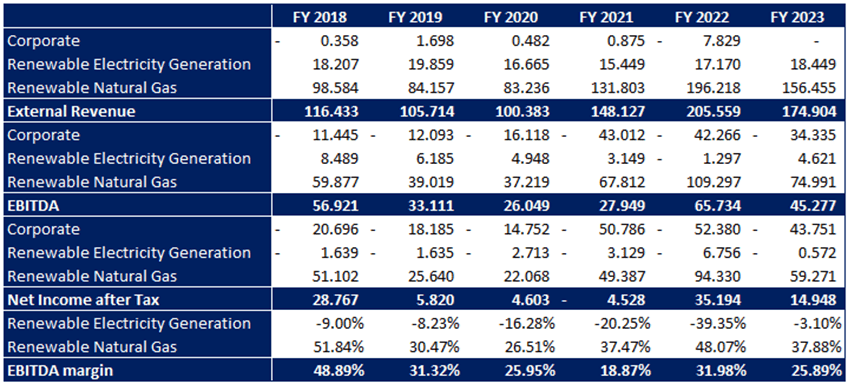

In FY23, Montauk generated 89% of revenues from the RNG segment and 11% through the segment dealing with power production through gas. Both segments are governed by long-term contracts with an average maturity of about 15 years, PPAs (Power Purchase Agreements) for electricity and GSA (Gas Sales Agreements) for RNG sales. Turning to details, 76.2% of FY23 revenues (vs. 70.3% FY22) were derived from the sale of credits such as RIN(D3) and RECs (Renewable Energy Certificates), with only 23.8% coming from the sale of RNG and electricity. These credits are monetized through sales to third-party companies that need them for compliance reasons. Although demand in the market tends to be high, the price is very volatile and very close to the highs of the last 5 years touched in FY22. In addition, the sharp decline already experienced by some RIN classes (D4-D5-D6) has alerted many investors to future RIN(D3) price expectations, which are expected to decline moderately during FY24, but to improved levels compared with FY23. Due to their large impact on revenues, proper management of these receivables, and an increase in their value, could be two important pillars of MNTK's success. At the same time though, a drop in the price can turn into an element of risk with concrete repercussions on both revenues and marginality.

www.epa.gov

Finally, this organizational structure has the problem of usually being associated with high revenue concentration. It is no coincidence that in FY23 the top 5 customers of Montauk account for 71% of revenues (vs 69% in FY22). The top 3 customers include Valero Energy (VLO), George E. Warren and HF Sinclair (DINO) in FY23.

During FY24, Montauk is planning 2 investments, for a total addition of 2400 MMBUtu/day, about 6.34% of revenues according to my estimates. The increase is mainly attributable to the expansion of the Apex plant, currently operated by APEX Environmental LLC. Two more plants are planned in FY26 in South Carolina and California, adding 4500 MMBUtu/day, about 11.9% of revenues. Such an increase in revenues and their effect on operating results though, will heavily depend on the price changes of RINs (D3) over the period. Nevertheless, I consider this a positive development, due to the resulting reduction in the dependence on WM and RSG sites.

MNTK Annual Report FY23

Finally, one last project that holds great importance is the Montauk Ag Renewables, through which the company will seek to develop a plant from an estimated output of 45000-50000 MWh equivalent annually, increasing its electricity production by 25%. The entire new project will be based on the use of a new company-owned technology acquired in FY21. The site will be in Turkey, North Carolina, after being moved from Magnolia, and is expected to start generating revenues as early as FY25, although full completion is expected by FY27.

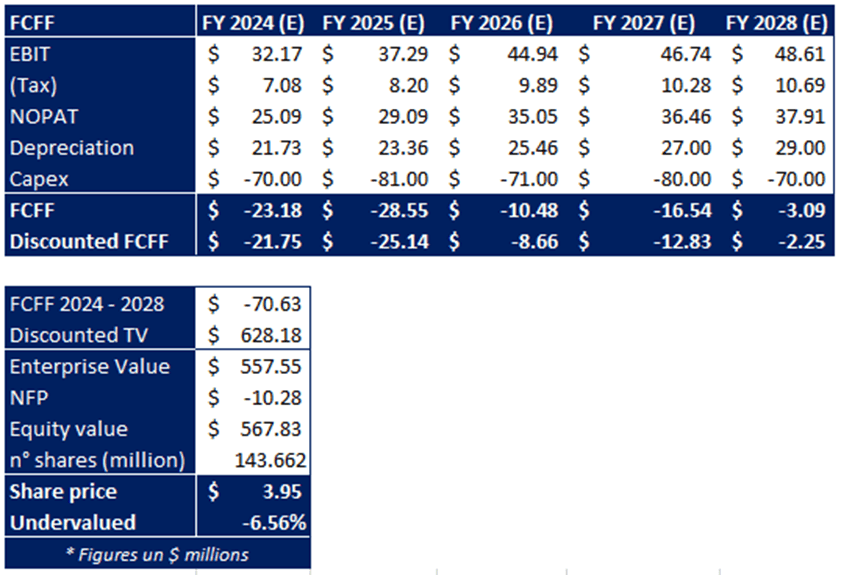

The amount of Capex needed to complete the projects is expected to be around $295-345m, $155-185m for the 4 RNG projects and $140-160m for the Turkey project. It should be financed through cash on hand, OCF production obtained between FY24 and FY26, and from a $50-60m increase in debt, which is of no concern given the net debt of -$10m as of Dec23. Barring further developments, a capital increase in the period is therefore not required.

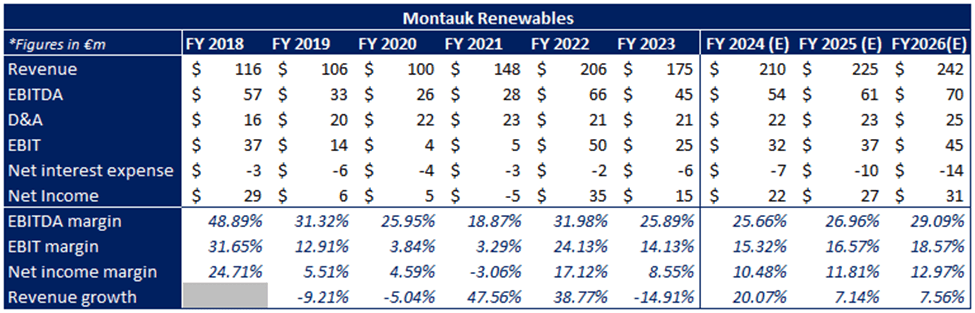

Montauk's revenues are closely correlated with the selling prices of RINs and RECs and were extremely volatile within the reporting period. In FY23, they reached $175m, down 14.9% YoY, due to record prices of RINs (D3) during FY22. In FY24, management issued guidance estimating production between 5.8m and 6.1m MMBtus, as well as electricity production between 190,000 and 200,000 MWh equivalent, for total revenues between $208m and $219m. In FY24, EBITDA and EBIT margins are expected to improve compared to FY23 results, due to better RIN price dynamics which, however, might turn out to be worse than expected considering the price trend in early 2024.

MNTK SEC Filings and Author's Estimates Author's Estimates

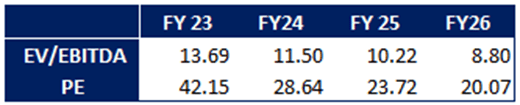

In FY23, MNTK made a profit of $15m, vs. $35m in FY22, confirming the strong sensitivity of profits to changes in the price of RINs. As of March 2024, the PE is 42.15x, a very high value for a company characterized by gradual and moderate growth. Moreover, even the prospective numbers return a forward FY26 PE of 20x, a value that I consider high considering all the unknowns related to the volatility of earnings results and the implementation of all projects. The same can be said for the EV/EBITDA ratio.

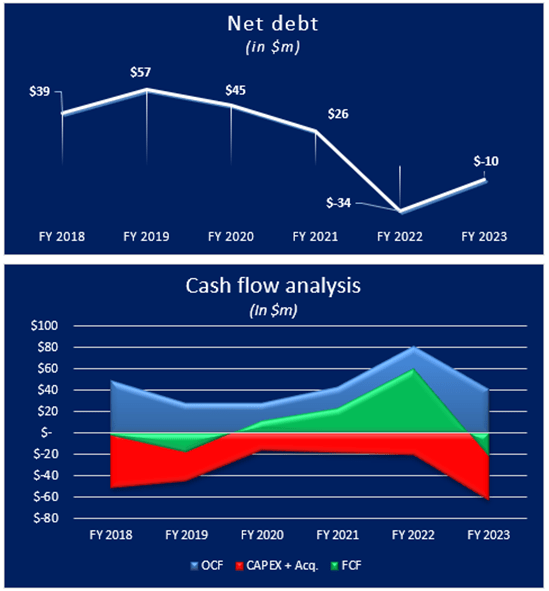

Despite much uncertainty regarding the economic data, balance sheet figures are strong, with negative net debt of $10m further strengthened by $218m of PP&E. These results were achieved through the production of high FCFs between FY20 and FY22, allowing MNTK to raise some of the capital needed to finance its new expansion program. FCF is likely to travel into negative territory over the next 3 years, because of the projects under construction. This could lead to raising external capital, probably through debt which, as seen in the previous point, could increase by about $50-60m by FY26. This would not be a particularly red flag though, with the Net Debt/EBITDA ratio being still just above 1x.

MNTK SEC Filings and Author's Analysis

In addition to the risks reported earlier during the business analysis, I believe there are 3 others of significant importance:

A large portion of the production sites are outdated and were built before 2007, except for 5 plants built between 2018 and 2020. Slightly better situation regarding renewable electricity generation sites.

Montauk's revenues are highly dependent on credits such as RIN(D3) and RECs. A change in regulations regarding these two instruments may therefore have a significant impact. In addition, the industry in which the company operates is heavily regulated and must follow certain guidelines that may change over time.

Over the next 2-3 years, MNTK will carry out a significant investment campaign, with the total Capex expected to exceed $300m. Although these projects represent an opportunity for growth, they will also require a significant expenditure of economic resources causing debt to increase. Although I do not think this is currently plausible, it may also be necessary to raise capital from investors.

I conducted a DCF analysis to assess Montauk's intrinsic value, returning a valuation of €3.95 per share, slightly below current market price. The following assumptions were used to determine the fair value:

Beta: since the Montauk beta turned out to be negative, I decided to use the average industry beta obtained from Stern NYU equal to 0.93.

MRP (5.7%) and Risk-Free rate (3.8%) were obtained by using 2023 Fernandez's data, weighted by the geographic breakdown of the company's revenues. A cost of equity of 5.57% was obtained.

WACC = 6.57%, increased by 1% to consider the risk associated with the MNTK's small market cap.

g = 2% in line with the inflation target in the US.

Author's Analysis & Estimates

I consider Montauk to be a financially sound company capable of producing high FCFs in recent years, without requiring any capital increase from shareholders. Over the next 2 years, it will be busy finalizing major projects that will lead to continued growth in RNG, and electricity generated. However, I consider within the business model and industry possible risks that weigh heavily on my valuation: first, the dependence of its business on both WM and RSG, as well as the high concentration and volatility of revenues, which are too dependent on the price trend of RIN(D3). Finally, my DCF returns a fair value slightly below the current price, highlighting a fair valuation of the stock. In my opinion, MNTK should price 20-30% below current levels to start becoming attractive from a risk-return perspective.