Jack Taylor

Jack Taylor

Following my coverage of Monster Beverage’s (NASDAQ:MNST), for which I recommended a buy rating due to my expectation that the business can continue to sustain earnings growth over the foreseeable future, thereby enabling it to continue trading at 32x forward PE, this post is to provide an update on my thoughts on the business and stock. I reiterate my buy rating for MNST as earnings growth continues to be strong, and I expect the strength to persist in the near term. Notably, there are upside catalysts (pricing growth in the US and gross margin expansion) that could drive earnings growth back to >20%, which could cause its valuation to go above my current assumption of 32x forward PE.

MNST performed in line with my expectations. In the recent 4Q23 quarter, MNST reported top-line growth of 14.4%, driving FY23 growth to 13.1%. Gross margins expanded 270bps to 54.5%, which was very positive as management cited a positive pricing environment and also favorable freight and input costs. As such, 4Q23 saw adj net income of $367.7 million, equating to adj EPS of $0.38, relatively in line with consensus. To just quickly sum up the 4Q23 earnings, I think the headline figure suggests that fundamentals continue to track well against my expectations.

Looking ahead, I think MNST will continue to do well in FY24, as the business saw a strong start to FY24, where January saw gross sales growth of 20.5% (16% if we adjust for the additional selling day). I believe January gross sales performance is very impressive in light of the sticky inflation environment, which I thought would dampen consumer demand, and also the poor weather. My view is that this suggests that MNST's newly launched products continue to see very positive adoption. Per management comments, last year January saw new product launches, which were 1 month later than the year before. As such, I think the strong January performance could imply the restocking of this new product, which suggests underlying demand is strong (if not, there is no need to restock). Moreover, there is likely ongoing benefits from building back Bang distribution in the U.S. as MNST works to regain distribution rights to a number of retailers that have disconnected with the brand. I expect this to happen in 1Q24, as the timing of the trade reset is expected to occur between January and 2Q24. Given that management has shifted its innovation pipeline to February’24, I think there is a good chance that it will be able to capture more shelf space given that consumer demand for MNST products remains healthy and retailers want to capture this demand.

Also, I might add that we have a number of important resets coming up, the trade reset from January on through the early part of the second quarter. So -- and we're anticipating big gains in shelf space, not only for our legacy brands, not only for the SKUs that we're about to launch but also for the Bang brand, where a number of retailers that had hitherto really discontinued Bang because of all the litigation and all of the issues are now taking it back. 4Q23 earnings results call

Aside from a healthy topline growth outlook that supports my earnings growth outlook, further gross margin expansion should also continue to drive earnings growth. In my opinion, there are multiple drivers to support a higher gross margin outlook. Firstly, input costs (aluminum) and logistic costs (freight) are trending favorably for MNST. Secondly, MNST should reap positive operational leverage from strong volume growth and a price increase program internationally. Note that these price increases have not really impacted consumer demand (international growth continues to be strong), which means there is still more room for ARPU expansion. Also, note that MNST has not started price increases in the U.S. market yet; if it does, these additional profits will flow into the P&L at high incremental margins. Thirdly, given that MNST is going to start producing some monster energy drink volume in house, it should be margin-accretive as well.

Obviously, we're working on margins. I'm proud to say that the Midwest premium and aluminum, which was one of my big bugbears, are coming down. But against that, we've said that we have increases in other commodities and other pricing.

And I don't know what's going to happen with freight, for example, we had a good benefit from freight in this quarter, this last quarter, and I'm not sure what's going to happen as we look forward into 2024 and the implications of the election and everything else.

The company has implemented price increases in the first quarter of 2024 in certain international markets. We're continuing to monitor opportunities for further pricing actions in both the United States and internationally. 4Q23 earnings results call

Own calculation

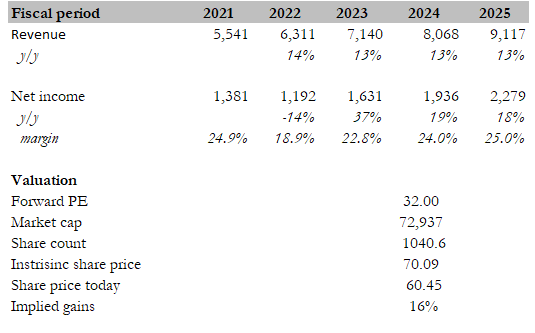

My target price for MNST based on my model is $70. My model assumptions are that MNST can continue to grow topline at 13% over the near term, an upgrade to my previous assumption as FY24 started off really strong and I see multiple growth drivers that can continue to support similar growth levels. I have also increased my margin expansion expectations given the positive tailwinds that should lead to a higher gross margin in FY24, which will set a higher base for FY25 to grow upon. With my revised assumptions, I now expect MNST to generate $2.28 billion in FY25 earnings, ~$180 million higher than what I expected previously. As MNST continues to drive high-teen earnings growth (with the possibility of growth going back to >20% if it raises prices in the US), I think the stock should continue to trade at its current multiple of 32x (which is its historical average). If I were to compare it to other beverage companies in the US, it also suggests that MNST should trade at a premium as it has a higher growth profile than peers.

Peers include: PepsiCo (PEP), Coca-Cola (KO), Celsius (CELH), Keurig Dr Pepper (KDP), and National Beverage Corp. (FIZZ). The median forward PE multiple peers are trading at is 22.4x, and the expected 1Y revenue growth rate is 5%. Based on my outlook above, MNST is expected to grow 13%, which is an 800bps premium to peers’ average.

A potential headwind to growth is that MNST's new innovation might not see the same traction as it usually does historically. Although the track record is good so far, there is no guarantee that the new product will do just as well. If that is the case, it would impact this year’s growth and also the next 1Q as retailers choose to restock less of this new product.

In conclusion, my rating for MNST is a buy rating due to continued strong earnings growth. FY24 started well, and I expect the momentum to continue from the new products expected to launch in 1Q24 and Bang distribution recovery. Notably, further gross margin expansion and pricing growth in the US could potentially push earnings growth to >20%. My revised target price of $70 reflects higher topline and margin expectations.