Urupong

Urupong

monday.com (NASDAQ:MNDY) points to solid guidance together with its Q4 2023 results.

Essentially, this is the bear and bull case. The bear case notes that monday.com is facing consistent deceleration in its revenue growth rates. While the bull case highlights that notwithstanding its decelerating revenues, the business is rapidly becoming increasingly profitable so that its valuation is cheaper than it appears at first glance.

This insight, when taken together with the fact that just over 10% of its market cap is made up of cash, means that paying 35x forward free cash flows is a fair entry point for investors.

Back in November, in a bullish analysis, I said:

My analysis of monday.com leads me to maintain a positive outlook on the company's future, despite facing challenges such as decelerating revenue growth rates and competitive pressures.

Author's work on MNDY

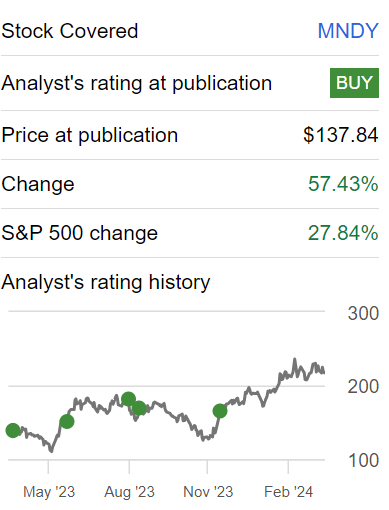

monday.com is a stock that I've been unwaveringly bullish on in the past year. The stock is up 57% y/y versus the S&P500 which is up 28% in the same time period. And as I look ahead, I remain bullish on this stock.

monday.com is a platform for teams to manage their work efficiently. Its platform helps users organize tasks, collaborate with team members, and track project progress. They offer various features, including CRM tools, to enhance productivity.

In the near term, monday.com is positioned for growth, buoyed by several factors. Its robust performance in fiscal year 2023, marked by a 41% revenue growth and record non-GAAP operating margin and free cash flow, demonstrates its market strength. With a focus on innovation and product enhancement, including the launch of mondayAI, monday workflows, and mondayDB, the company continues to solidify its position as a Work OS platform.

Additionally, the introduction of monday code provides developers with a secure environment to create apps, further enriching its ecosystem and enhancing its value proposition for customers. Also, its updated pricing model should contribute to further revenue growth in the near term.

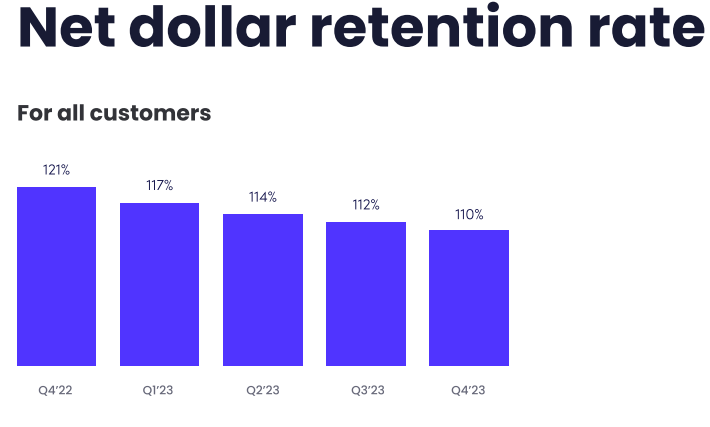

However, monday.com also faces near-term challenges. For one, the overall macro environment continues to impact customer spending behavior, which is reflected in its net dollar retention rates, see below.

MNDY Q4 2023

As you can see above, for its trailing twelve months ended Q4 2023, monday.com's net retention rates reached 110%, which is the lowest point of 2023.

Moreover, the competitive landscape in the Work OS platform market is intensifying, with established players vying for market share, for example, from Atlassian (TEAM). Given this consideration, together with monday.com's price hike, one has to wonder, whether this could ultimately lead to a level of customer churn in 2024.

Altogether, monday.com has to balance many different elements, from striving to increase its revenue growth rates, while ensuring top customer satisfaction, all the while increasing its product pricing.

Given this context, let's now delve into its financials.

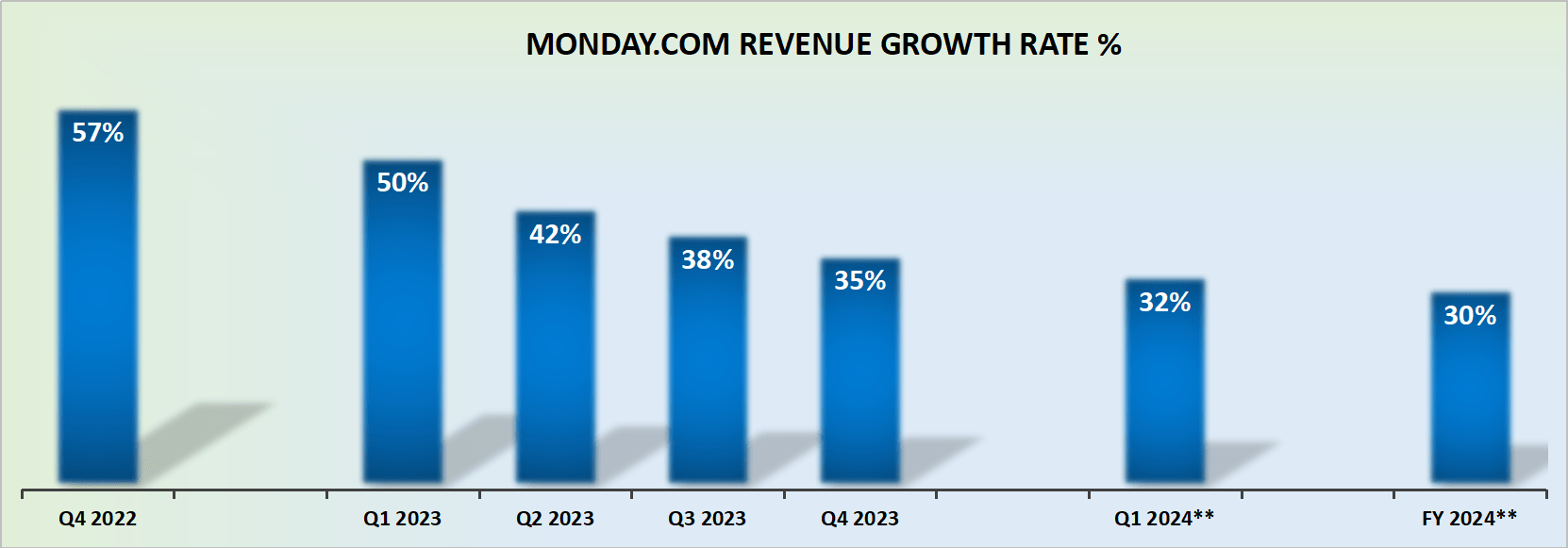

MNDY revenue growth rates

monday.com guides for approximately 30% CAGR for the year ahead. On the one hand, this slowdown is largely to be expected given the strength of the prior year.

On the other hand, this will be the 4th consecutive year of decelerating growth rates. How much of this deceleration is due to a saturated market? How much of it is due to the competition? And how much is due to customers tightening up their spending this year?

And lastly, if monday.com could stabilize its revenue growth rates at this pace into 2025, this would imply that these strong 30% CAGR rates may be here to stay for a while.

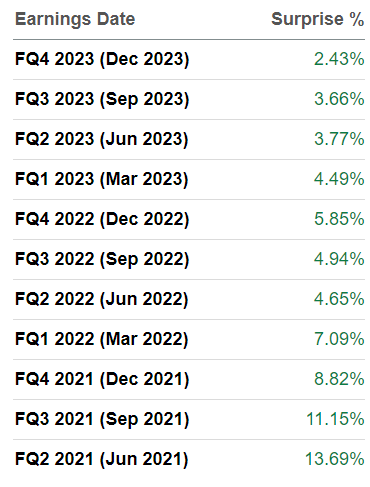

However, consider this table.

SA Premium

As you can see above, the size of monday.com's revenue beats has become progressively smaller with time. Therefore, it's not possible to conclude that this management is being highly conservative with its guidance to allow for easy beats in the quarters to come. In fact, I believe that what you see here with the 30% CAGR for 2024 might be all there is.

However, I believe there's more to this investment thesis. And that's what we discuss next.

Since 2023 ended with free cash flow margins of 28%, when monday.com guides for its free cash flow margins to compress down to 22%, investors largely expect management to be using 2024's excess profit margin to invest in its future growth.

Nevertheless, there appears to be sufficient juice left in this young business for it to end up delivering approximately 30% free cash flow margins as a forward run rate at some point in 2024.

Even if the year as a whole doesn't quite reach 30% free cash flow margins, there's enough momentum in the business that it could deliver 30% free cash flow margins at some point in 2024 or early 2025.

Consequently, I believe that monday.com could at some point in 2024 be on a forward run-rate of delivering $300 million in free cash flow. This puts the stock priced at 35x forward free cash flow, a figure that is easily justifiable given its strong growth rates of approximately 30% CAGR.

I remain bullish on monday.com despite facing challenges like decelerating revenue growth rates and competitive pressures. The company's solid guidance alongside its Q4 2023 results indicates resilience.

Despite concerns about slowing revenue growth, monday.com is becoming more profitable, making its valuation seem cheaper than perceived. With over 10% of its market cap in cash, paying 35x forward free cash flows appears compelling.

Looking at monday.com's near-term prospects, I see promise driven by robust performance in fiscal year 2023, with a 41% revenue growth and record non-GAAP operating margin and free cash flow.

Additionally, an updated pricing model is expected to contribute to further revenue growth in the near term. Despite challenges like macroeconomic uncertainties and intensifying competition, I believe monday.com remains poised for growth and profitability, making it an attractive investment opportunity.