JHVEPhoto

JHVEPhoto

Marsh & McLennan (NYSE:MMC) released their Q4 FY23 results on January 25, showing strong topline and earnings growth. I highlighted Marsh & McLennan’s growing portfolio across economic cycles in my recent article. I believe the company is well-positioned in FY24, and I reiterate my 'Buy' rating with a target price of $230 per share.

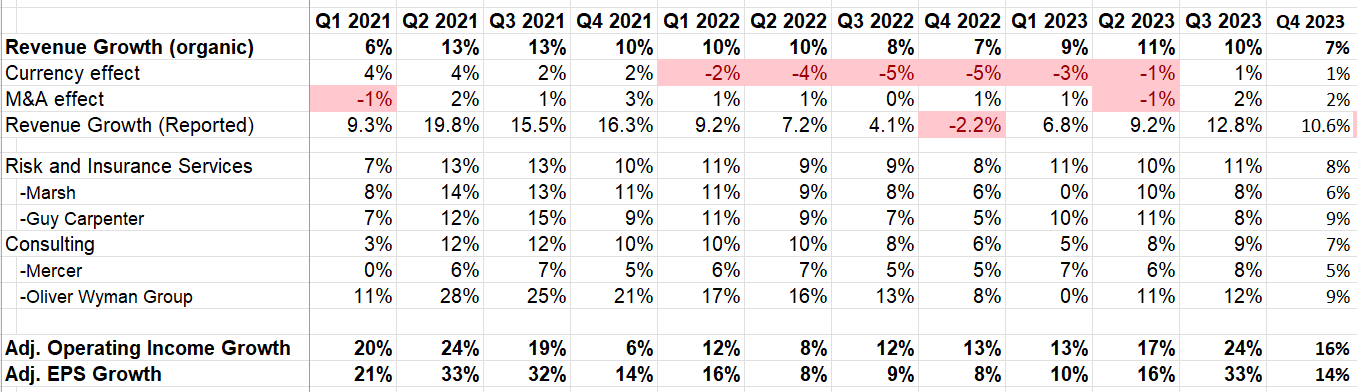

In Q4 FY23, they delivered 7% organic revenue growth and 16% adjusted operating income growth, both exceeding market expectations. This growth extends across all business segments, including risk and insurance services, as well as their consulting business, as illustrated in the table below. Regarding capital allocation, they generated $3.8 billion in free cash flow in FY23, paid out $1.3 billion in dividends, and repurchased $1.15 billion of shares, reflecting a consistently strong shareholder return policy. Their net debt leverage ended at only 1.7x at the close of the fiscal year, indicating a robust balance sheet.

Marsh & McLennan Quarterly Result

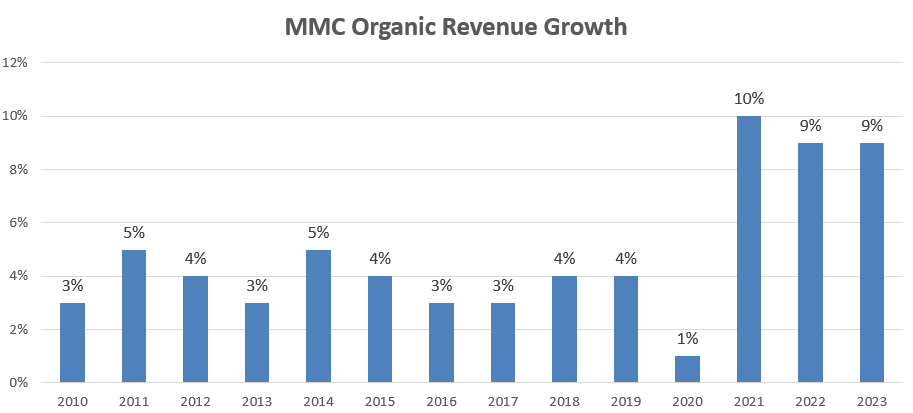

As shown in the chart below, their growth rate has accelerated since FY21, delivering almost 10% annual organic revenue growth. I believe there are several reasons for this growth acceleration.

Marsh & McLennan 10Ks

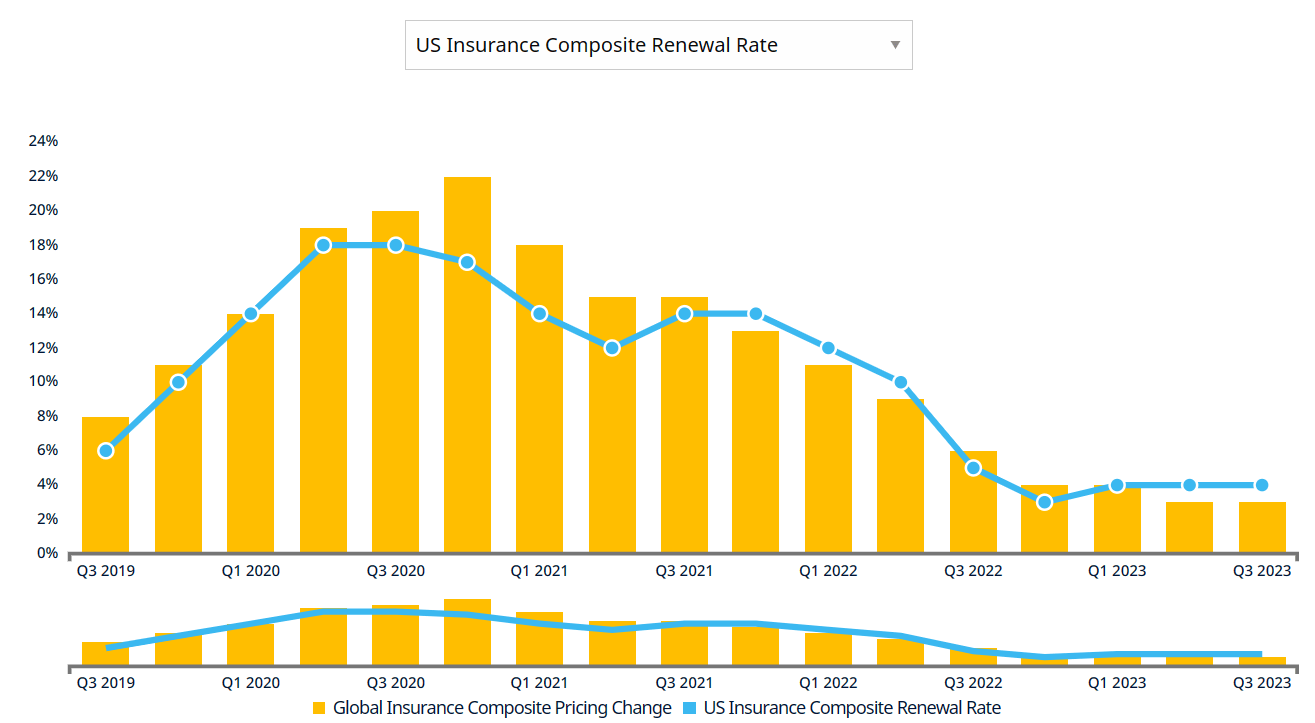

Firstly, their business is benefiting from the insurance rate increases observed in the past few years. During the Q4 FY23 earnings call, their management indicated that overall insurance rates have increased for the 25th consecutive quarter. Property rates increased by 6%, compared to 7% in the third quarter, and casualty pricing continued to be up low single-digits. According to the Marsh Global Insurance Market Index, the U.S. insurance composite price increased by 3% in Q3 2023. The overall high inflationary environment, I believe, makes insurance price increases inevitable.

Marsh Global Insurance Market Index

Secondly, Marsh & McLennan has actively shifted its business portfolio into high-growth areas, including digital, climate resilience, sustainability, cyber, and affordable healthcare, among others. These high-growth areas are expected to provide revenue growth acceleration and margin expansion over time.

Finally, their acquisition strategy has consistently added value for shareholders. Marsh & McLennan has a long-term track record of successful tuck-in acquisitions and integrations. They prioritize attractive acquisitions over share repurchases, as indicated by their management during the earnings call. I believe their historical acquisitions have been focused on their core insurance and risk management businesses, thereby adding significant value to the company.

For FY24, they are guiding for mid-single-digit or better underlying revenue growth with margin expansion and strong growth in adjusted EPS. Additionally, they anticipate spending $4.5 billion on dividends, share repurchases, and acquisitions. Looking ahead, I believe Marsh & McLennan could continue to grow above the insurance market growth rate, although not as robustly as in the past three years.

The primary factor influencing this is the insurance premium rate. While the overall insurance rate has increased significantly since the global pandemic, historically, insurance underwriting and pricing have experienced cycles. As illustrated in the previous chart, the overall rate continues to move higher, but the growth rate has started to moderate.

Considering this, I expect Marsh & McLennan to deliver 5-6% underlying revenue growth in FY24, aligning with their historical average level. Over the past seven years, they have achieved an average of 6% organic revenue growth. On the margin side, their primary drivers are operating leverage and high-growth businesses. During the earnings call, their management expressed confidence in delivering another year of margin expansion in FY24.

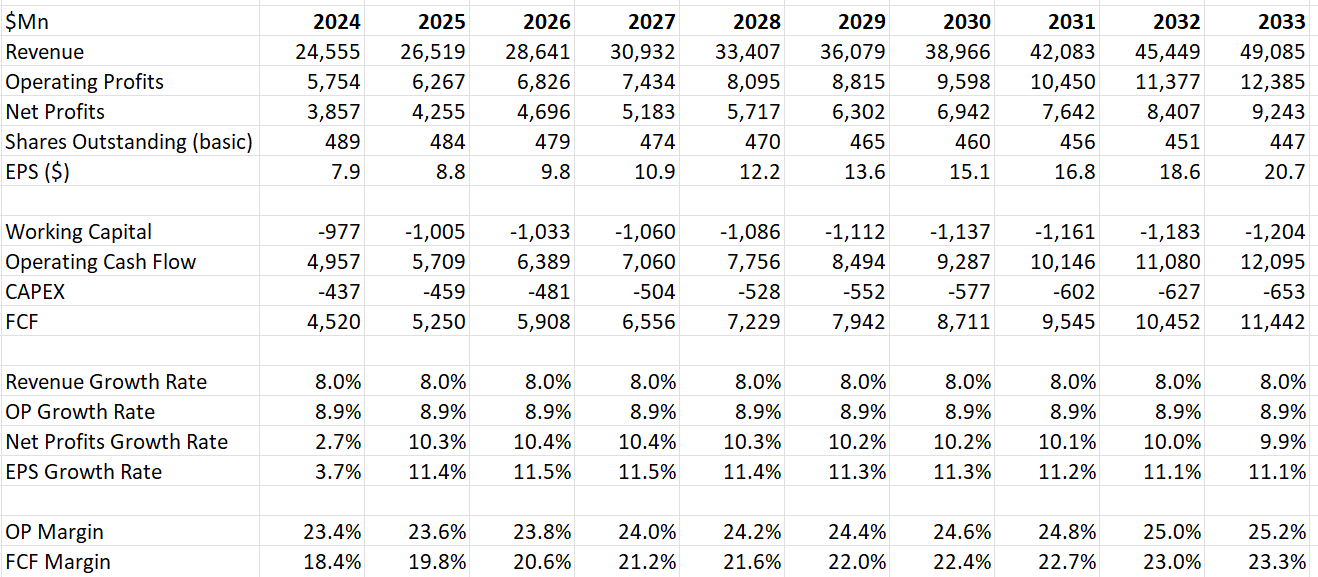

As discussed previously, I anticipate the company delivering 6% organic revenue growth. I assume they are allocating 4% of revenue to acquisitions, and these acquisitions could contribute another 2% to topline growth, aligning with their historical average. On the margin side, I expect the company to generate operating leverage and improve gross margins, driven by high-growth business lines. Based on my calculations, they should be able to achieve a 20 basis points annual margin expansion.

Marsh & McLennan DCF - Author's Calculation

Keeping all other assumptions intact, the fair value is estimated to be $230 per share. Currently, the stock price is trading around 21x forward free cash flow, which is quite cheap for a double-digit earnings growth company.

Marsh & McLennan is undergoing corporate restructuring to reduce overhead costs. They reported $131 million in total restructuring costs, covering severance, lease exits, and technology streamlining initiatives. During the earnings call, they indicated that total charges are anticipated to be approximately $475 million, with expected savings of roughly $400 million. As shareholders, it's important to monitor the actual financial benefits derived from these restructuring programs, as all expenses are excluded from the non-GAAP margin calculation.

Despite anticipating a moderation in the insurance rate increase in the near future, Marsh & McLennan continues to be a high-quality growth company. I reiterate my 'Buy' rating with a target price of $230 per share.