Diy13

Diy13

The Global X MLP ETF (NYSEARCA:MLPA) is a targeted yet passively managed ETF invested in some of the largest US domestic midstream Master Limited Partnerships (MLPs). MLPs can offer investors higher yields because they do not pay corporate taxes, but rather offer investors pass-through distributions that are taxed at the investor level. By investing in MLPs via an ETF wrapper, individual investors can reap the benefits of high yields MPLs provide but can avoid the nightmarish K-1 tax reporting. MLPA provides 1099 reporting. There are several macro and global tailwinds we believe will support midstream energy for decades, and believe investing in the energy sector through MLP ETFs could make sense in a value and income portfolio. The question is: Is MLPA the right ETF in this space?

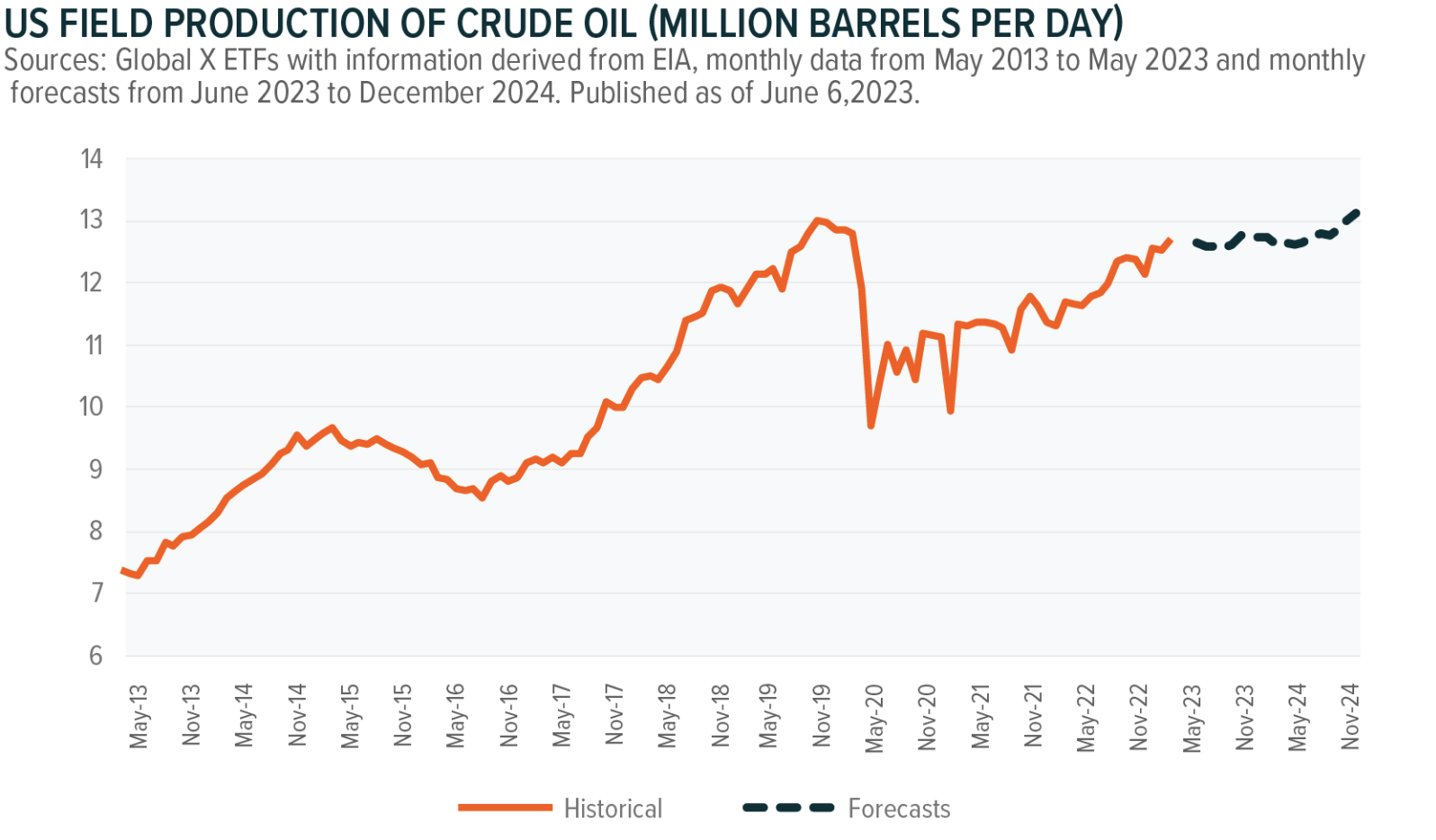

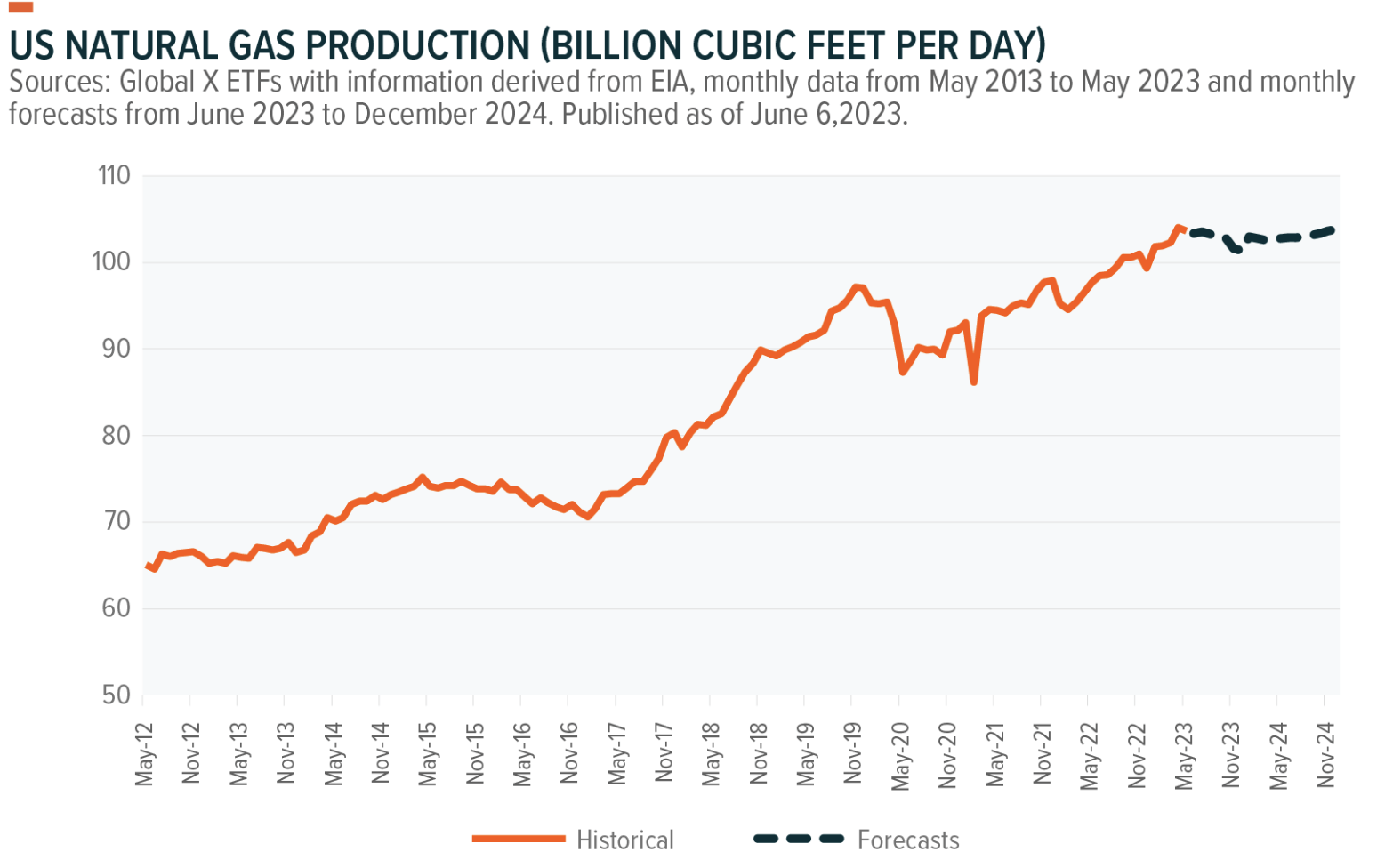

US domestic oil and natural gas (NG) production are at all-time highs and projected to grow. OPEC has cut oil production and the US has become a production power house to offset the lower supply. In addition, the world increase in consumption of liquified natural gas is at an all-time high. The International Energy Agency (IEA) reported in its 2023 IEA Outlook that natural gas represented 23% of the world's energy consumption and coupled with projected new liquified natural gas (LNG) projects, LNG consumption is expected to increase by another 45% by 2025. The rise in US domestic oil and NG production supports the role midstream operators play and will continue to underpin with growing demand for midstream infrastructure. The graphs below demonstrate US oil and natural gas production since 2013 with forecasts through the end of 2024. It's not slowing down, folks!

US Oil Production (Global X Energy & MLP Insights)

US Natural Gas Production (Global X Energy & MLP Insights)

The 2022 Inflation Reduction Act (IRA) gives generous decades-long tax incentives to utilities and midstream operators in the effort to build out US infrastructure. This would buttress the woefully inadequate domestic electric grid, as well as provide much-needed infrastructure for renewables.

Europe is also in need of energy capacity, not just the US. Recently, the European Union reclassified natural gas projects and nuclear energy as "green renewables". US producers have tremendous capacity to export liquified natural gas, and these processes flow through midstream pipelines. Additionally, since the Russia-Ukraine conflict began, US exports of (LNG) have increased significantly to wean EU countries off the Nord Stream pipelines. While the White House has put a pause on many (LNG) exports recently, it is still supporting exports to the EU for the time being.

MLPA is comprised of 21 MLP holdings, but its top 10 represent over 85% of its constituents. This is what we call a targeted focus ETF, and we generally like that over an ETF comprised of 800 stocks following an index. There is risk involved with both: concentration risk with the former and "blind luck" diversification with the latter. By blind luck, we mean taking the good with the bad or perhaps the beauties with the beasts for the sake of diversification.

The competing ETFs we follow closely are AMZA, AMLP, EMLP, and XLE. There are close similarities between all of them, but a few important differences. We note there is high concentration risk with the top 6 to 10 holdings in all the ETFs with the exception of EMLP which has a large utility exposure. Utilities are much more prone to interest rate risk than pure MLP players. MLPs are typically run with long-term contracts, considered almost toll-like. They also have built-in inflation escalators, so their earnings are not exposed to inflation and the often wild swings of commodity pricing.

Another significant difference is market cap construction. XLE is the bellwether ETF for the energy sector; its composition is 73% large-cap and no small-cap exposure. The rest of our closely followed industry competitors have comparable market cap exposure of 12ish% large-caps, but 20-40% small-cap composition, with MLPA having the largest small/microcap exposure.

| MLPA | AMZA* | AMLP | EMLP | XLE | |

| Top 10 Holdings % Representation* *AMZA Top 6 holdings | 85% | 85% | 93% | 50% | 76% |

Market Cap Exposure: Large Cap | 12% | 12% | 12% | 15% | 73% |

Market Cap Exposure: Mid Cap | 46% | 62% | 52% | 66% | 27% |

Market Cap Exposure: Small/Micro Cap | 42% | 26% | 36% | 19% | 0% |

Energy Sector Exposure | 97% | 99% | 97% | 57% | 100% |

Industrial Sector Exposure | 0% | 0% | 0% | 4% | 0% |

Utility Sector Exposure | 3% | 1% | 3% | 39% | 0% |

*Source Seeking Alpha & Internal Database |

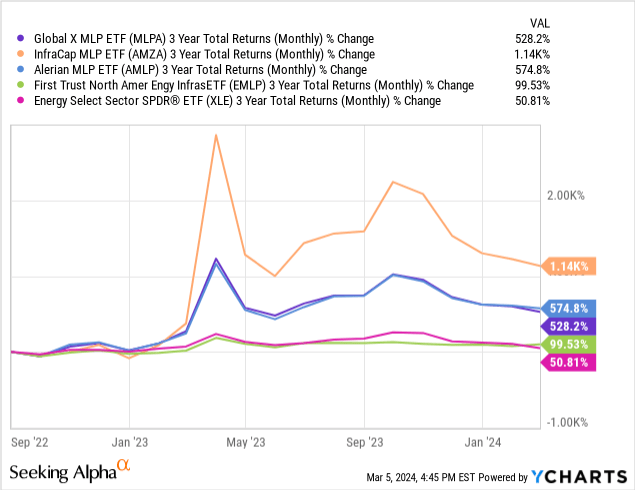

While past performance is not indicative of future performance, the chart below summarizes the normalized 3Y rolling total returns of MLPA and its competitors we closely follow. We believe industry concentration, market cap concentration, and active vs. passive management drove the returns and these same factors could impact potential future returns. We recently wrote an article on AMZA, which is still our favorite with a buy rating. AMZA is actively managed, leveraged, and has a seasoned management team. Note, AMZA has outperformed all these MLP ETFs by double or more over the last 3 years.

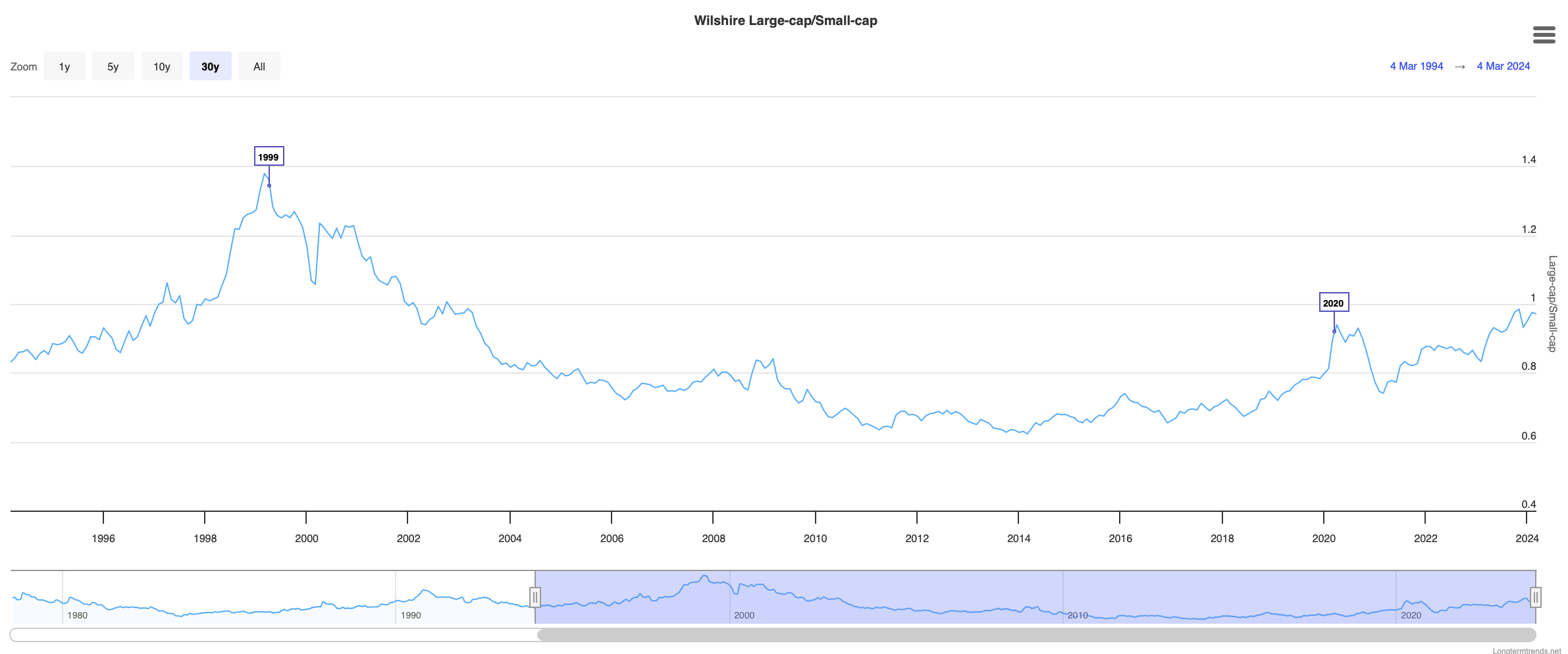

Going forward, we are neutral on MLPA. Our views on MLPA might change should 2024 a) we see a reversal of the large valuation gap between large-cap and small-cap stocks as shown in the chart below or b) we see lower interest rates later in the year as many predict. The ratio of large-cap valuations to small-cap valuations is plotted below. The higher the ratio, the more undervalued small-caps are relative to large-caps. You'll note the time periods around the dotcom bubble in the late 90s/early 2000s and the 2020 COVID-19 shutdown were the last times other than now we see such a large valuation gap. Also, many economists and market strategists predict an ever-delayed lowering of interest rates by the Fed this year as inflation moderates. High interest rates disproportionally affect smaller cap stocks, as they often rely more on floating rate interest rates and private equity to fund their businesses than larger cap stocks. Hence, MLPA with its more small-cap-focused strategy could provide outsized returns in 2024 should interest rates eventually fall during the year or the valuation gap between large and small-cap stocks moderate to the mean.

Ratio Large Cap Valuation to Small Cap (Longtermtrends.net)

Geopolitical and Macro Risk. Should OPEC begin producing more oil for export, US production could fall with potentially falling oil prices. Also, LNG processing and transportation could be put on an indefinite hold in any other country, which would lower MLP infrastructure expansion.

Concentration risk. MLPA is highly concentrated, with 85% of its portfolio in its top 10 holdings. Should any company have poor performance, the overall ETF performance could be negatively impacted.