GOCMEN

GOCMEN

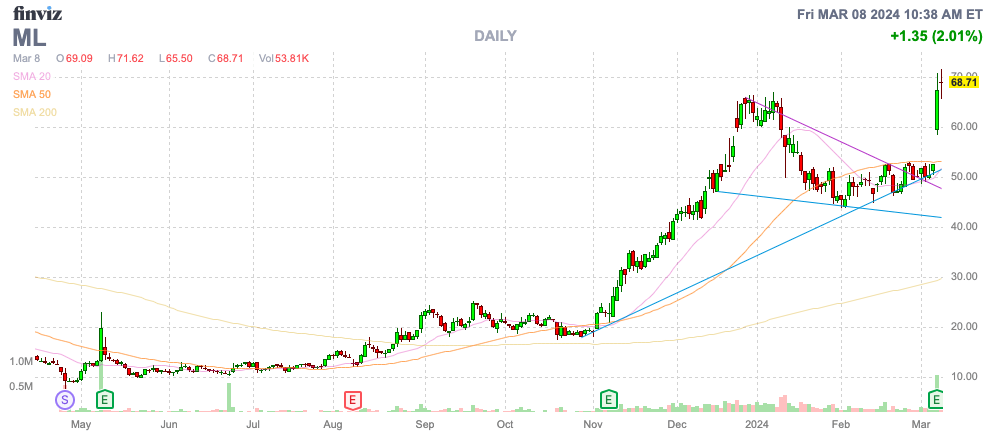

MoneyLion Inc. (NYSE:ML) has become the gateway for financial products on the Internet, but the stock still trades like a SPAC that performed a reverse split. The fintech remains in massive growth mode and has turned highly profitable while the stock still trades at a split adjusted $2, though MoneyLion has already had a big rally off the lows. My investment thesis remains ultra Bullish on the stock based on financial metrics, not how much MoneyLion has rallied off the lows.

Source: Finviz

MoneyLion hit a tough stretch at the end of 2022, when financial services firms pulled back on selling products via their marketplace. The fintech is back to growth mode as platform partners return to investing in growth.

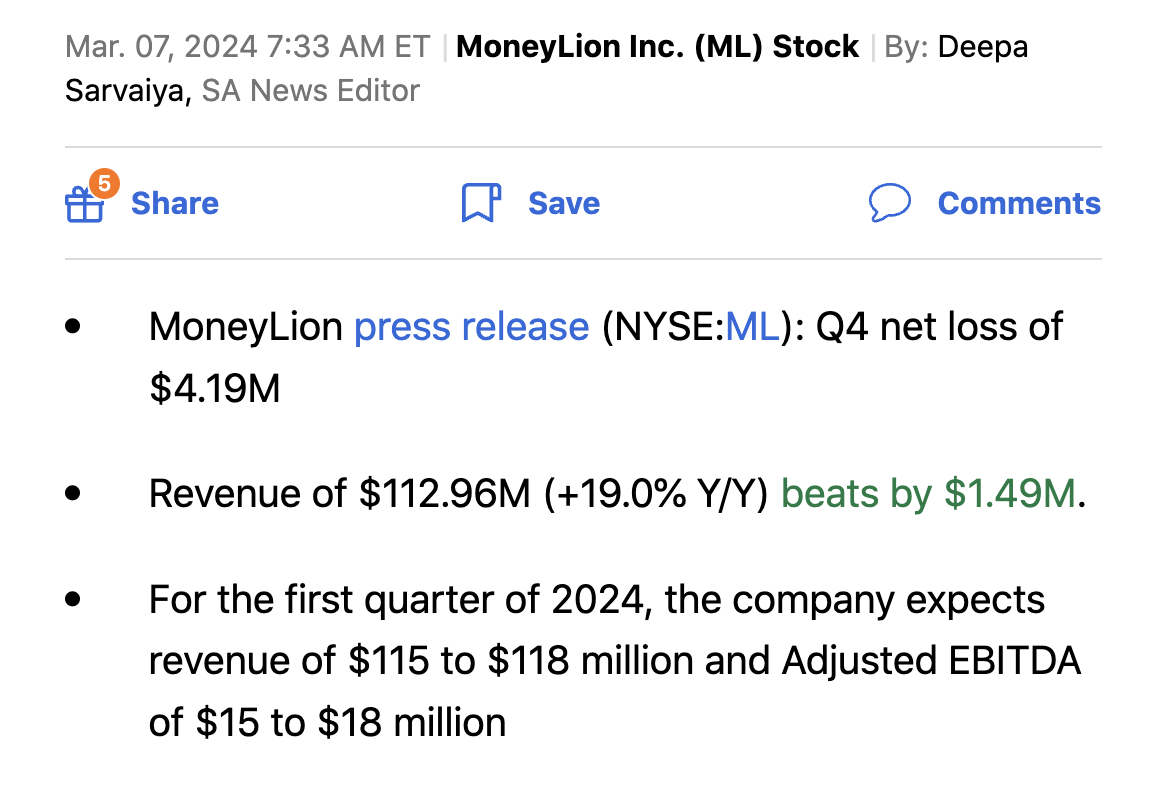

The fintech reported a solid Q4 to end 2023, with results beating targets as follows:

Source: Seeking Alpha

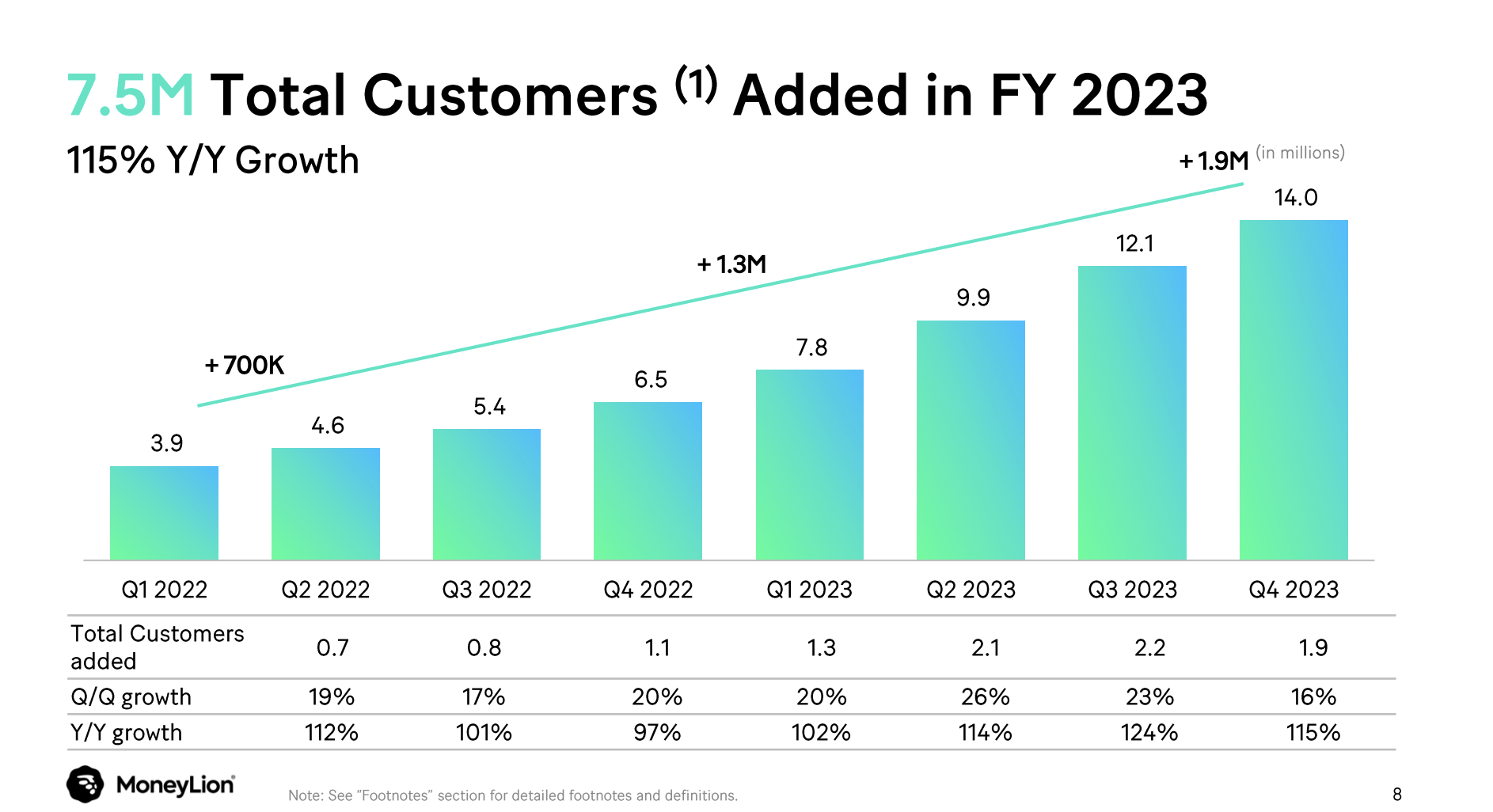

MoneyLion added 1.9 million new customers during the quarter to reach 14.0 million, up 115% YoY. These new customers are the key to accelerating growth in 2024 and beyond, with a combined 4.1 million new customers in just the last 2 quarters alone.

Source: MoneyLion Q4'23 presentation

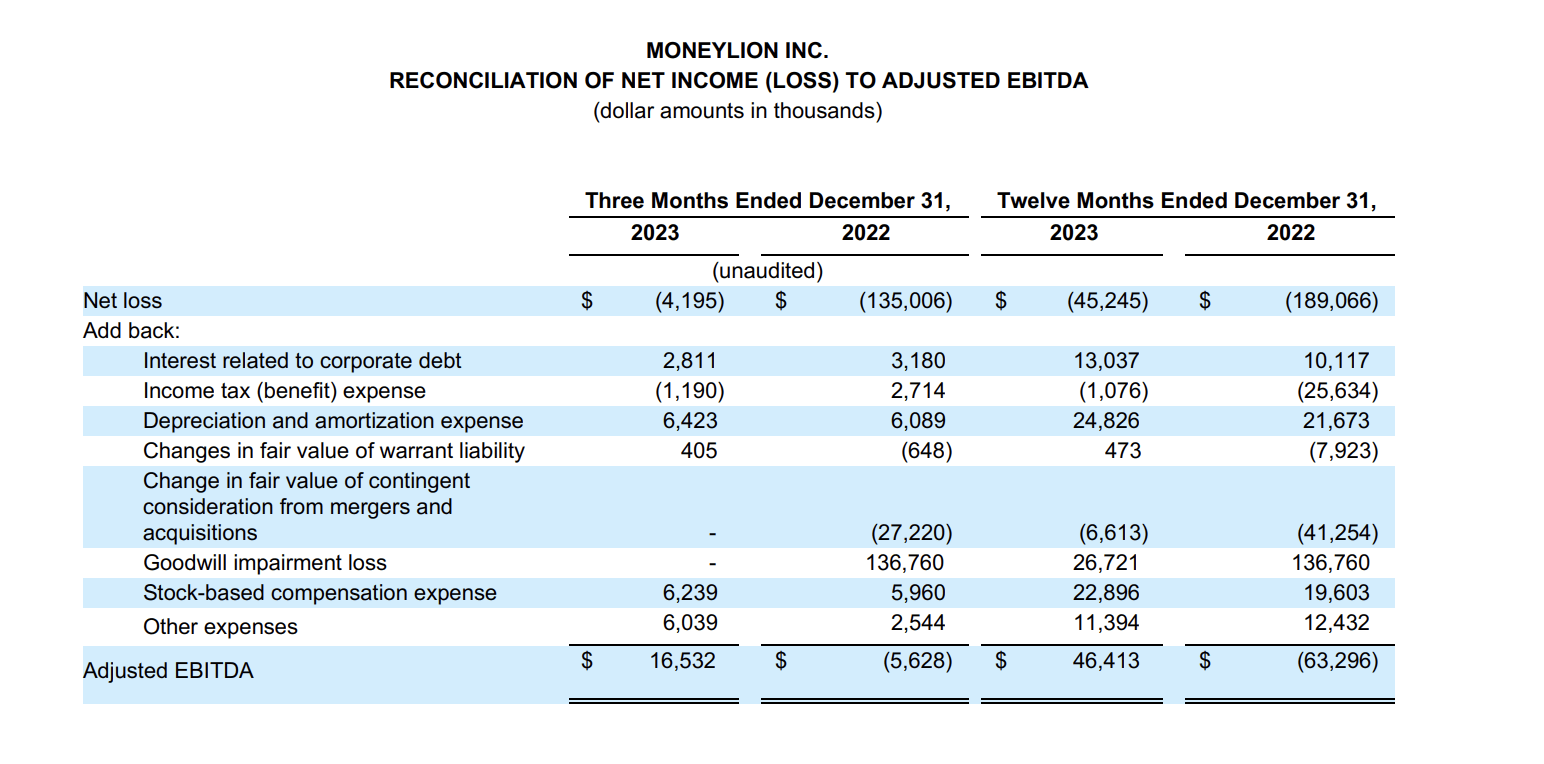

Despite onboarding all of these new customers, the fintech continues to become more profitable, with adjusted EBITDA hitting $17 million. The company was reporting large losses in mid-2022 and the turnaround has occurred via MoneyLion flipping the switch on profits to the tune of a $105 million improvement in adjusted EBITDA YoY in 2023.

A prime reason for the profit improvement is the vast reduction in CAC. The fintech has reduced the cost to acquire a new customer to almost nothing at only $15, requiring MoneyLion to sign customers up on limited products to generate a quick return on investment now estimated at an only 3 month payback period. The company only spent $28 million on marketing during Q4, with the cost down from $37 million in the prior December quarter.

The company plans to continue expanding their financial marketplace with more content and a push further into insurance, credit cards and mortgages. The marketplace has substantial growth opportunities to move beyond a current focus on lending partners.

MoneyLion traded below $10 last year and soared to $70 on the strong Q4 results. With all of the stocks soaring on AI hype, the initial thought is likely that the stock is expensive now.

The actual truth is that MoneyLion only trades at ~10x EBITDA targets for the year. A fintech with adjusted EBITDA set to soar this year would normally trade at a far higher multiple, though the current multiple is far above the level at the stock lows where MoneyLion only had a market cap of $100 million company for a business running at a $60+ million annual EBITDA rate now.

Even more important, adjusted EBITDA is actually close to adjusted profits. In fact, the only real charge is to exclude the $2.8 million interest expenses on corporate debt along with the offsetting tax benefit.

Source: MoneyLion Q4'23 earnings release

The company focus on GAAP profits probably doesn’t help the stock view. The biggest costs excluded from EBITDA, stock-based compensation and amortization, are normal costs stripped out of adjusted profits by techs and fintechs alike.

MoneyLion should trade at far higher multiple with signs EBITDA could grow by 50% rates over the next couple of years. If the company can generate accelerating growth, as forecast, and obtain a further boost from the EY partnership to further boost revenues.

The company didn’t provide any financial estimates on the EY alliance, but the CEO was clear a lot of work has been done with the companies. MoneyLion combines the technology, data and AI capabilities, content and product knowledge to help banking partners easily acquire, grow and importantly, monetize consumers at scale while EY provides the banking platform for small, traditional banks to operate a digital banking platform.

Per management on the Q4 '23 earnings call, the EY partnership attacks a large fee pool amongst the regional and traditional banks and should contribute significantly to the business as follows:

CEO Diwakar Choubey

the idea here is really to co-build turnkey digital solutions alongside EY. And as you can imagine, that we didn't stumble upon this relationship by mistake, and that there's been a lot of time spent by both companies, multiple quarters, really setting us up for success.

So it's early innings, but we do expect it to be fairly meaningful to our contribution later this year and certainly in 2025.

CFO Richard Correia

Yes, I think we love this question because we didn't make a big splash with EY, because this is going to be small. And so when we think about the fee pools that are available, it's in the $20 billion range. And as you know, when MoneyLion sets its sights on a fee pool, we take market share. And so we're going after the digital transformation of the regional banks, the national banks, the credit unions with our marketplace technology.

Guidance for Q1 suggests growth already starts off at up to a 26% rate, while a major upside catalyst exists from lower interest rates. The fintech might drive higher growth rates for a stock trading below market multiples.

The key investor takeaway is that MoneyLion Inc. stock remains exceptionally cheap. Investors shouldn't pay attention to where the stock traded last year, but rather value the fintech based on growth rates and adjusted profits.