SOPA Images/LightRocket via Getty Images

SOPA Images/LightRocket via Getty Images![]()

As a high-quality-seeking dividend growth investor, the pickings recently have been pretty slim. The market has been on a role, which from a net-worth perspective, makes me feel good, but as an active investor looking to put money to work in compounding dividend growth, there have been fewer opportunities. This is why I regularly track a list of around 100 of the highest-quality dividend growth stocks, so that as valuations come into fair range, I can take advantage. I don’t always time purchases perfectly, but over the long term, I have been very happy with the results. After more than 20 years of investing ups and downs, the one thing I know is that you really can’t go wrong with quality.

If you’ve been following along, you know that one of my favorite ways to look for value in this high-quality dividend growth space is to screen for those stocks trading near 52-week lows. I decided to filter my watchlist by companies that are trading at less than 30% of their 52-week range (52-week low being 0% and 52-week high being 100%).

Using this first pass criteria, we will be looking at the following list of companies:

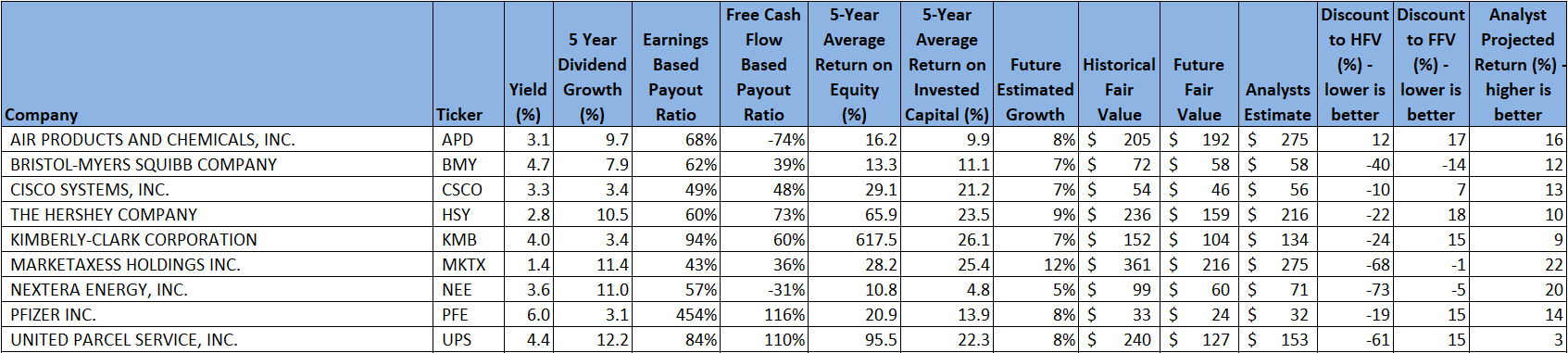

Finbox, Seeking Alpha, Author’s Analysis

As I’ve described in previous articles, I like to calculate a fair value in two ways, using a Historical fair value estimation, and a Future fair value estimation. The Historical Fair Value is simply based on historical valuations. I compare 5-year average: dividend yield, P/E ratio, Schiller P/E ratio, P/Book, and P/FCF to the current values and calculate a composite value based on the historical averages. This gives an estimate of the value assuming the stock continues to perform as it has historically. I also want to understand how the stock is likely to perform in the future, so utilize the Finbox fair value calculated from their modeling, a Cap10 valuation model, FCF Payback Time valuation model, and 10-year earnings rate of return valuation model to determine a composite Future Fair Value estimate.

I also gather a composite target price from multiple analysts, including Reuters, Morningstar, Value Line, Finbox, Morgan Stanley, and Argus. I like to see how the current price compares to analyst estimates as another data point, and as a sanity check to my own estimates.

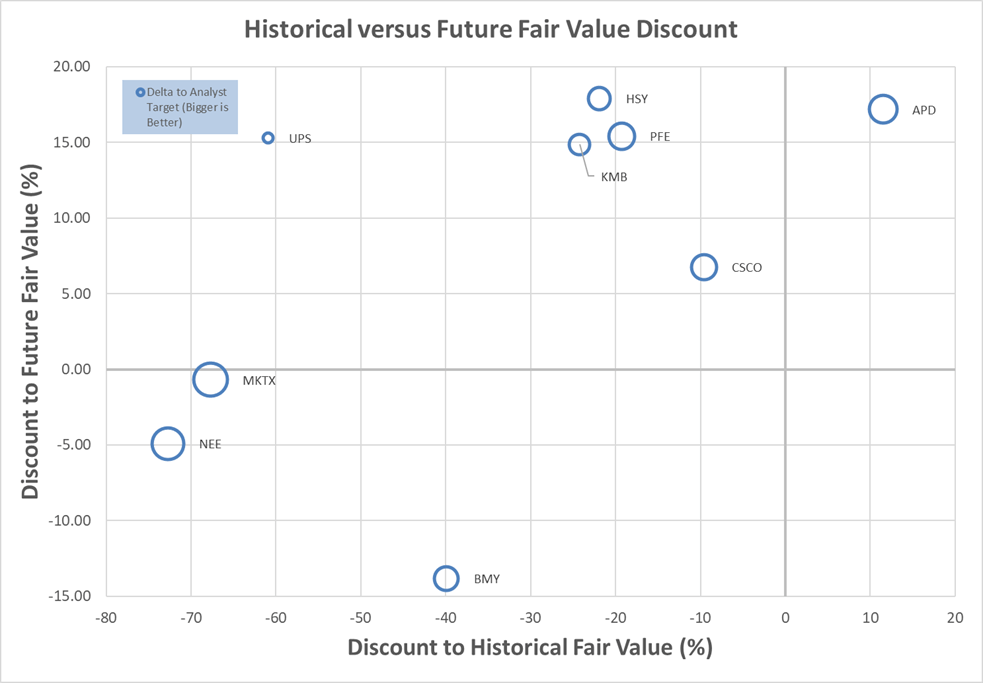

Plotting three variables on one plot is tricky, but using a bubble plot allows us to visualize three variables by plotting the Historical fair value versus the Future Fair Value on a standard x-y chart, and then use bubbles to represent the size of discount relative to analyst estimates.

Author calculation of Historical and Future Fair Value, analyst estimates

This chart is insightful once you understand how to interpret it. What we are looking for are stocks that are trading at a discount to both the Historical Fair Value and the Future Fair Value. So, those stocks that are farther to the left, and farther to the bottom, are potentially the stocks trading at the largest discount to fair value. This would be the bottom left quadrant of the graph. Additionally, those stocks with the biggest bubbles are the stocks that are trading at the largest discount to analyst estimates, so in theory, stocks in the lower left quadrant that also have large bubbles, should be decent candidates for investment.

The chart suggests that MarketAxess (NASDAQ:MKTX), NextEra Energy (NEE), and Bristol Myers Squibb (BMY) are all trading at discounts to their Historical and Future Fair Values, as well as favorably compared to analyst estimates.

I own all of the stocks in the list / chart except for Kimberly-Clark (KMB). I have recently initiated a position in Air Products and Chemicals (APD) at $226 and added to my positions in MarketAxess at $217 and in NextEra Energy at $56. I already have a full position in Bristol-Myers, but still believe it to have good potential as a long-term investment. If there is a theme to my investing, outside of high-quality dividend growth, it is the out-of-favor, beat down, but high-quality stocks that I believe have unappreciated potential. That works more times than it doesn’t.

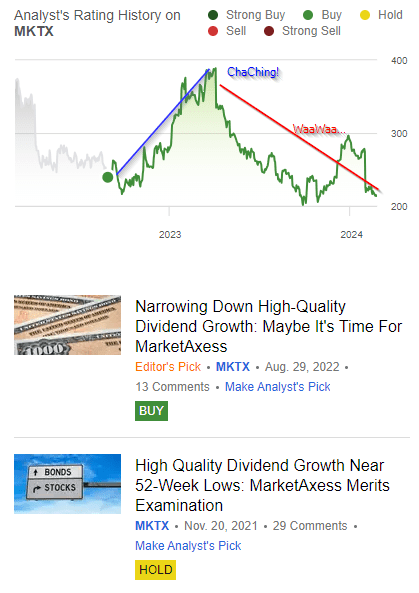

MarketAxess and I are still figuring each other out. I’ve written a couple articles in the past about it and am still excited for the future prospects, but to this point, the results have not been good. I want to take another look, since it has been a while, to see the rationale for my recent purchase.

Since I’m not trying to sell anything on Seeking Alpha (trust me, I don’t do it for the money) but more to encourage me to dig deeper and be a better investor, I like to be as transparent as possible. I wrote my first article on MKTX at the end of 2021. Overall, I rated it as an interesting hold at that point, but also noted that I was looking for a target price around $330. I ultimately initiated a position several months later at $307. I wrote another article in August of 2022 where I updated my rating to Buy. I have purchased MKTX several times since that initial purchase at $307 - $244, $246, $225, and $217. I have a long, time horizon, and I like dollar cost averaging when valuations look fair.

Even averaging down, I am underwater on this investment. If I was a trader, my initial “hold” rating in 2021 should have been a “sell”. It is also interesting to see that had I sold before mid-2023, I would have had a really nice capital gain. Maybe I should be a trader…

Seeking Alpha

Since I’m not a trader, let’s start with the basics. MKTX has a 5-year average Return on Equity of 28.2%. However, its most recent ROE is 21.7%. The 5-year average Return on Invested Capital is 25.2% but its most recent ROIC is 19.4%. In both cases, I like that ROE is so close to ROIC, since this suggests management isn’t playing games with debt to increase the ROE, however, even though the numbers are still very good, there is some deterioration against the average that is a minor warning flag. A quick look at ROIC versus the Weighted Average Cost of Capital (around 10%) shows healthy margin, which should be a good growth indicator. With the initial yield being low, we need growth to be strong to support strong future dividend growth.

The earnings-based dividend payout ratio of 43% and free-cash-flow-based dividend payout ratio of 36% are both excellent. They have paid a growing dividend for over 14 years now. The most recent raise of 2.8% is disappointing against the backdrop of the low initial yield. Morningstar rates MKTX as wide moat, with exemplary capital management, and currently has a 4-star valuation rating.

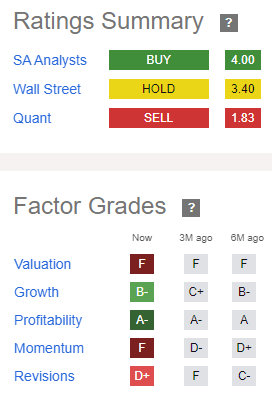

Seeking Alpha makes available a summary of ratings, as well as factor grades. These make for another nice, first pass filter for investment timing.

Seeking Alpha

Starting with the top stop-light chart – you can take your pick between Buy, Hold, and Sell. My only argument here is that Quant and Wall Street tend to be short-term focused, and I like to think the analysts on Seeking Alpha are more sophisticated, and therefore longer-term focused – apologies to those traders out there, I’m a very long-term investor, hence of course I am sophisticated (laugh).

The Factor Grades are relative, and therefore very dependent on the peer comparisons. MKTX doesn’t have a lot of direct competition, so these relative comparisons need to be taken in context. Two things that are important to the investment thesis in MKTX are growth and profitability though, and it scores well here. These are important to the sustainability and high growth expectations we have for the dividend. Otherwise, the momentum and revisions suggest it might be out of favor, which conveniently, falls right into my wheelhouse.

I want to be really simple about how I think about MKTX.

On the one hand, revenue continues to increase nicely, amidst increased adoption and volumes. On the other hand, market share has been coming down amidst strong competition from key competitors that are also growing, like Tradeweb and Trumid. This is the fundamental source of investor frustration with the stock – is the growth story intact, and will MKTX continue to grow even in the face of strong competition?

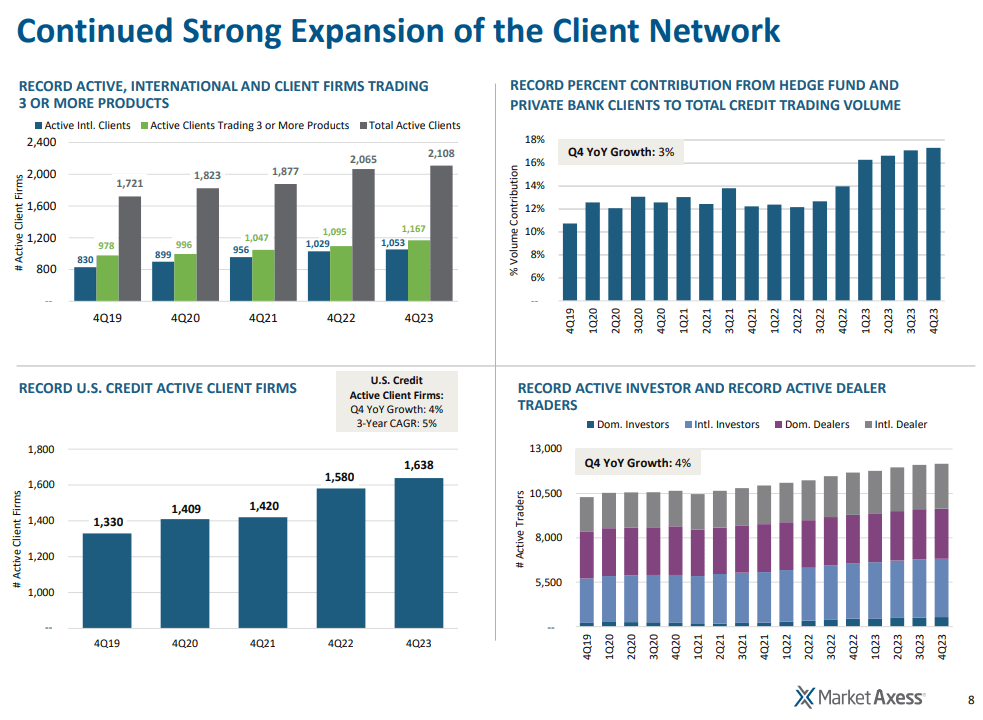

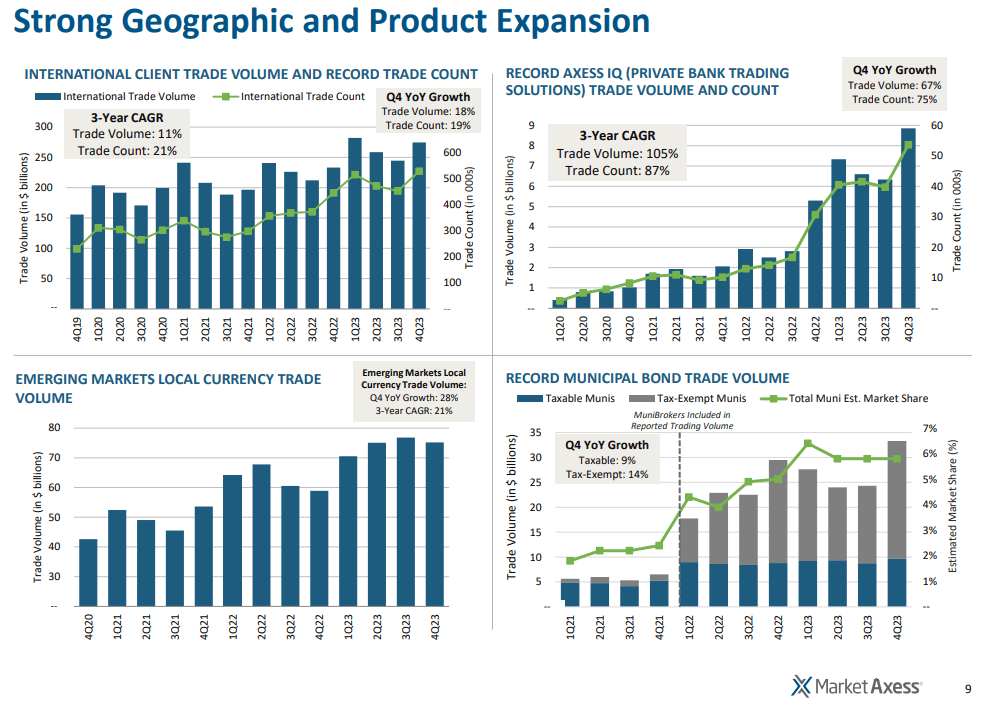

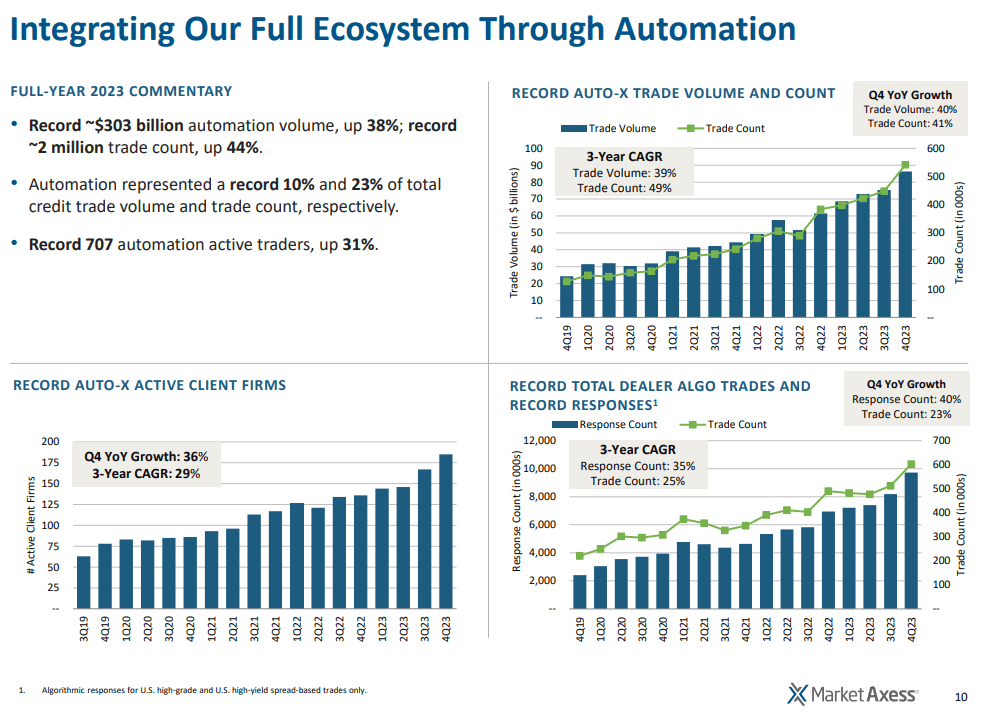

Just a few graphs of results from the recent MarketAxess FY 2024 Earnings Results show that there is a lot to be excited about.

MarketAxess Full Year 2023 Results Presentation MarketAxess Full Year 2023 Results Presentation MarketAxess Full Year 2023 Results Presentation

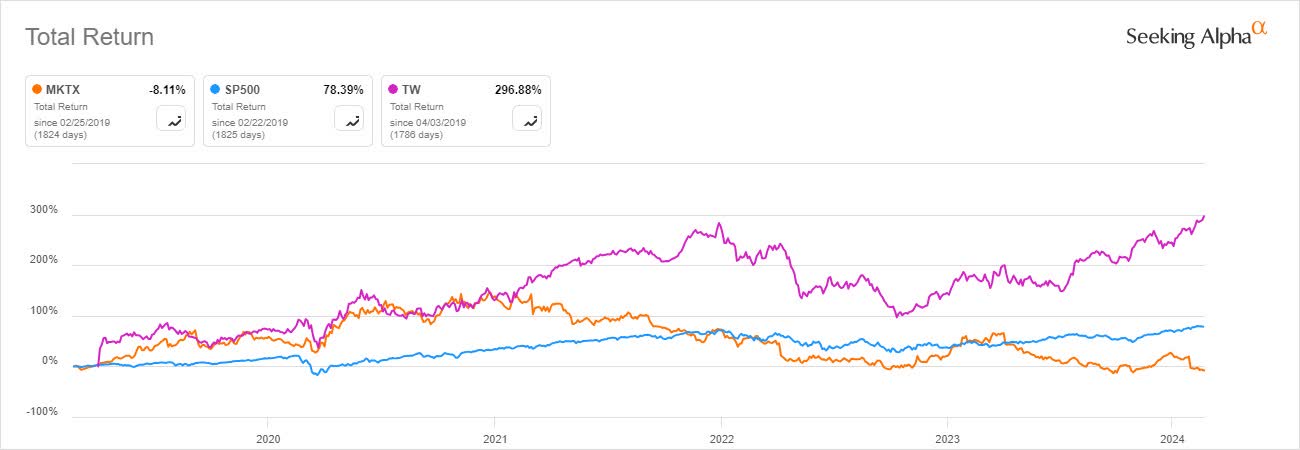

Before we dig deeper into the growth, I do like to look where things have been in the past. I think we realize that past performance can be somewhat indicative of the quality of the company. Obviously, it’s important to understand the key drivers for that past performance, to see if you believe anything has changed that could impact that. So, let’s start with how MKTX has performed for shareholders in the past:

Seeking Alpha

First, MKTX has drastically outperformed the S&P 500 in the past, including a brief period last year. Recently, however, MKTX has given up all of its out-performance and is now under-performing. Of interest, Tradeweb is one of the key competitors we mentioned above. It has significantly outperformed the market as well as MKTX. I can’t help but notice that some of MKTX’s under-performance seems correlated to some of Tradeweb’s outperformance, and this is one of the key foundations for the bear case – Tradeweb is taking a lot of that new and addressable market that MKTX is supposed to be getting. MKTX isn’t growing as much because Tradeweb is taking market share. Taking the counterpoint, if the total addressable market is growing, MarketAxess has been able to continue to grow, even with a total market share decline, and Tradeweb is performing very well, could MarketAxess be undervalued relative to the performance potential of the total addressable market?

Let’s now see if valuations have improved relative to history with the decline in price, or if we are seeing overall degradation. Let’s reference P/E and yield for this.

Finbox Finbox

Maybe a positive note is forming with this view – the P/E is still relatively high, but compared to its historical valuation, is at a low compared to the 5-year average of 55.8. This suggests that the business has not degraded to the extent that the price has. Additionally, the yield is also at a 5-year high compared to the 5-year average of 0.8%. From this historical-based view, MKTX may be attractively valued.

MKTX continues to do a nice job of maintaining shares outstanding, not letting shareholders get diluted. However, it doesn’t look like share buy-backs should be counted on to add to future earnings per share growth. This could still suggest that they believe they have better ways to grow earnings for shareholders through strategic investment than just relying on share buybacks or could suggest they are preserving capital due to concerns about growth.

Finbox

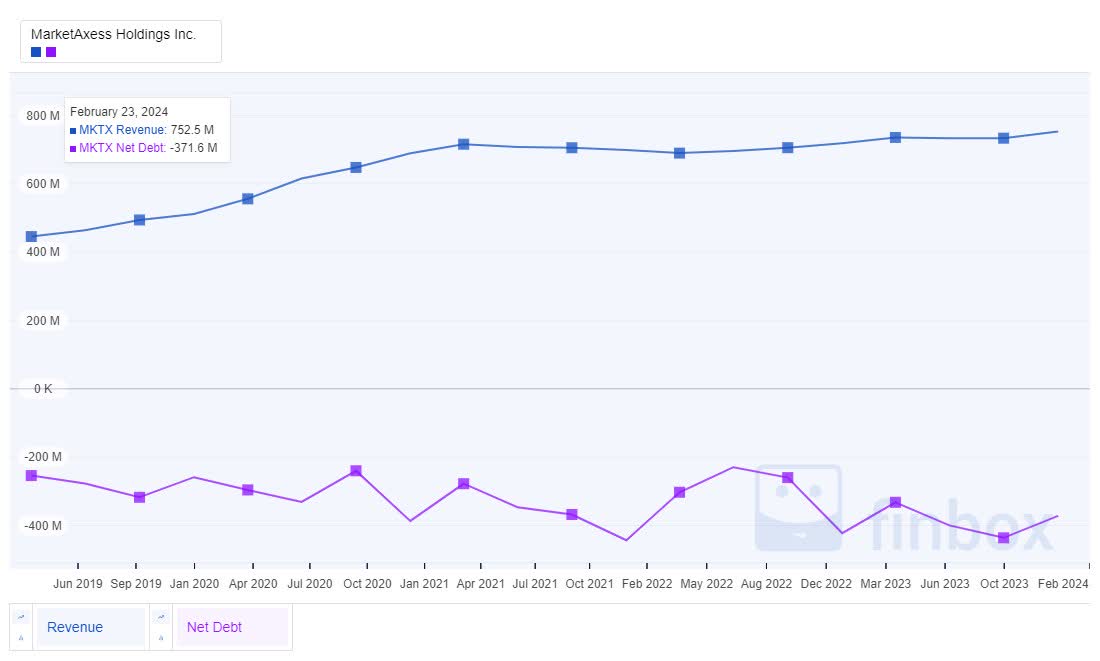

I still really love the revenue versus net debt story. MKTX is debt free and has a strong net cash position. This is not very common in today’s day and age, and something I like seeing as a long-term investor counting on that compounding dividend growth far into the future. Even with the historical acquisitions that have added to business results, maintaining this debt free status is impressive.

Finbox

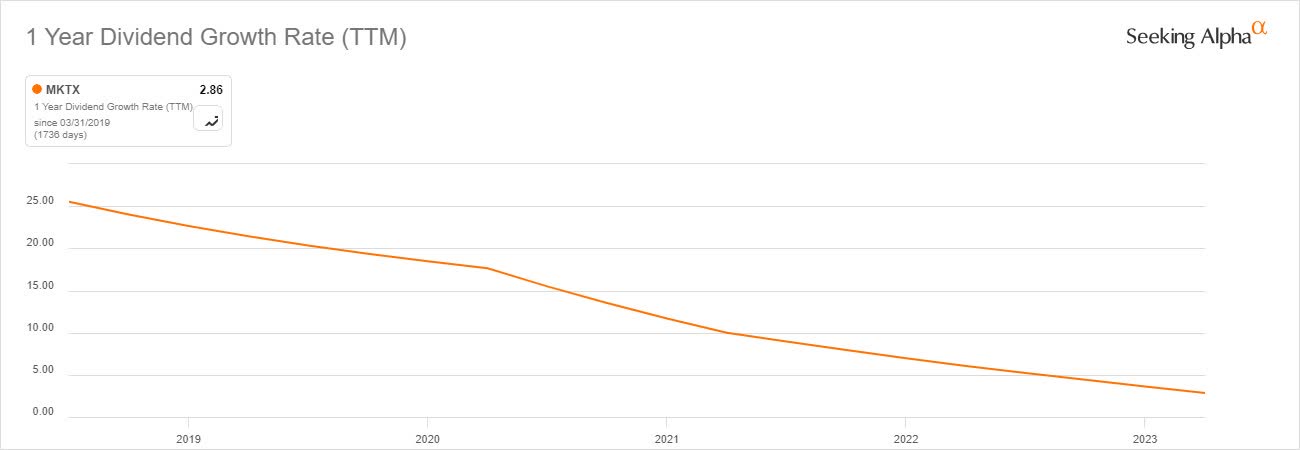

MKTX has paid a growing dividend for over 14 years and has historically demonstrated very strong dividend growth. The growth is tapering significantly recently, with the most recent raise being under 3%. I look at this as an indirect indicator of management’s confidence in future growth, so when I see dividend growth pulling back, it could indicate management is not convinced of their growth prospects. Likewise, it could also indicate that they have other plans in mind, such as strategic M&A or internal R&D, or it could just indicate that the high rate of growth in the early years was to get the dividend to a target level, and now that target level has been achieved, the growth will be more throttled by fundamentals (still tied to growth).

Seeking Alpha

The earnings and free cash flow-based payout ratios are healthy and relatively stable. Based on free-cash-flow, which is how dividends are paid, it looks like a higher level of growth could be sustained. This leads us back to our above question looking at the growth – does management lack confidence, or is this a sign of conserving cash for other strategic investments?

Finbox

Moving on to our future looking analysis, it seems like the story hasn’t changed a lot since we last looked at MKTX. The question still boils down to that future growth. Let’s take a look at some of the future indicators to see if anything significant has changed in that story.

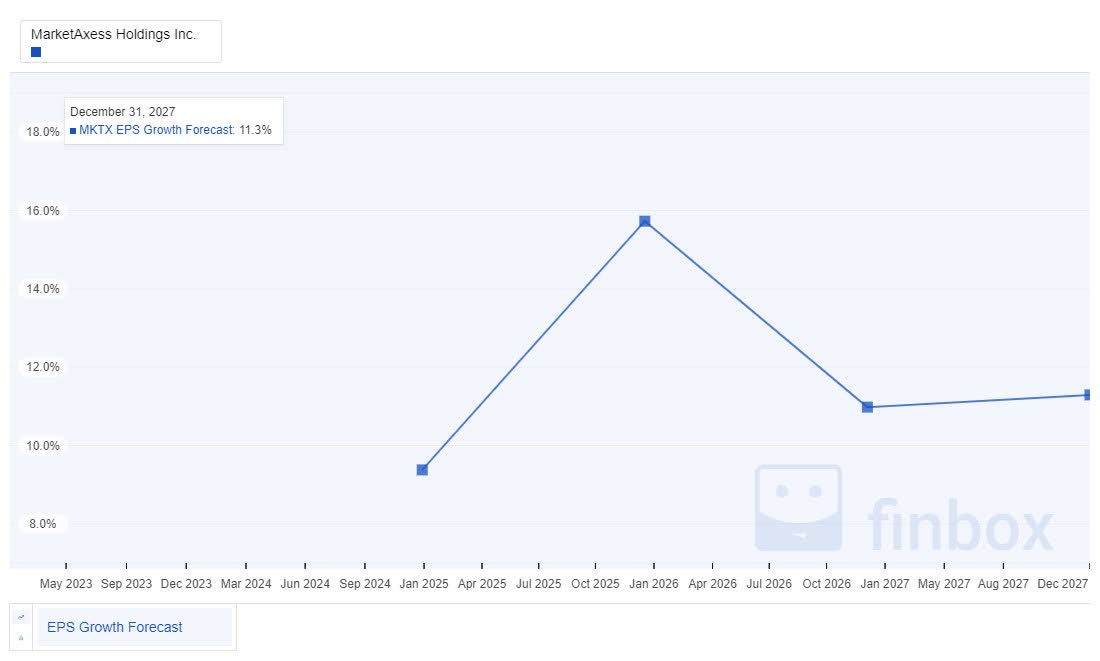

Let’s start with projected earnings growth. Frankly, I like what I see. Far from being a no-growth / low-growth story, at least from an EPS perspective, the growth projections are solid.

Finbox

The future growth projections align well with the past estimates for long-term growth. Sometimes, with companies that are out of favor, there is a big discontinuity between the expected future growth and past estimates for long-term growth. That doesn’t appear to be the case here.

Finbox

My own estimate for MKTX’s forward growth is around 12%. I derive this from a combination of various growth projections and growth models. I personally feel like an average, low double-digit growth expectation is reasonable for MKTX, and expect the growth to continue on a fairly stable trajectory, as we’ve seen with the historical growth results. Those levels of sustainable growth do nice things for compounding over time.

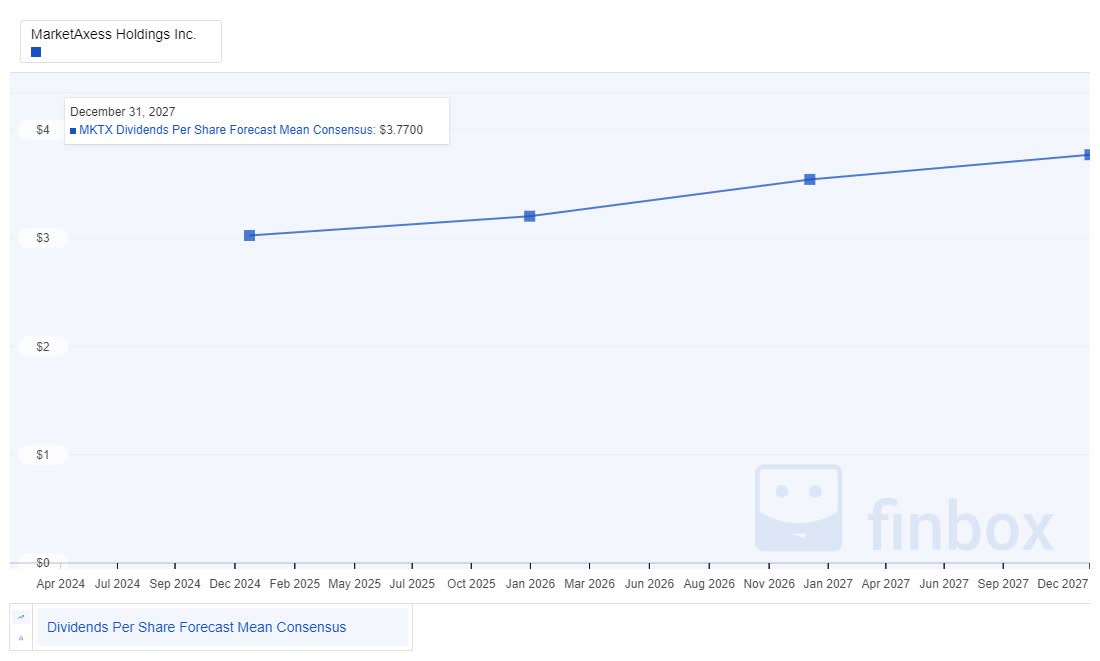

For a dividend growth investor, understanding future dividend growth potential is also important, especially in as much as it is sustainable. Here are the long-term dividend growth projections for MKTX. The forecast growth looks consistent. I do wonder if the recent deceleration in dividend growth is short-term, or more of the new standard. I don’t like 3% dividend growth from such a low yielder. My hope is that short-term sacrifices in dividend growth will allow for strategic investment, which MKTX has proven to be adept at, allowing longer-term growth in the future. As a more growth-oriented stock in general, that growth should likely also result in attractive capital appreciation.

Finbox

The future projections for payout ratio show the opportunity to grow the dividend in-line with other growth projections, without increasing risk. Even if the low growth of late calls into question future growth, it appears the capacity will be there.

Finbox

Since EPS is not a full indicator of growth, the other thing to tie out is revenue. Revenue is expected to continue on a healthy growth projection, in a stable way.

Finbox

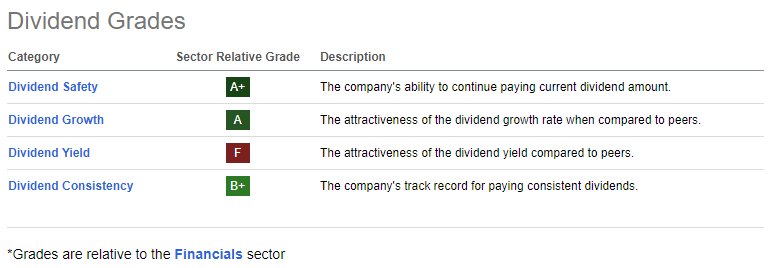

The Seeking Alpha Dividend Grades show the potential in this investment, with strong relative scores for safety, growth, and consistency – all things we like to see. We know the yield is low, and relative to the financial sector, this low grade isn’t a surprise.

Seeking Alpha

Let’s end our journey with a brief discussion on risk. At the end of the day, the story with MKTX is a growth story. If the opportunity for growth is less than expected, or if MKTX is unsuccessful in capturing its share of the growth, which I believe is the biggest concern the market has, then the stock is likely overvalued.

From a financial and quality perspective, there does not appear to be much risk here. Due to its debt-free status, MKTX doesn’t actually have credit ratings from the major agencies, however, the Value Line Financial Strength rating is A. As we discussed previously, Morningstar rates it as Wide Moat with Exemplary Capital Management. The Altman-Z score is currently a very healthy 11.39. The biggest risk is likely valuation, and as we’ve discussed, the valuation looks attractive currently.

MKTX and I have had a colored history. Had I sold shares at certain points, I would potentially be much wealthier, at least on paper, however, I do believe in the quality of this company, like the growth history and prospects, and think the addressable market they serve is attractive. To an extent, this is a picks and shovels type of company for the bond market, and they are doing something that, though not entirely without competition, is disruptive. The strategic work they are doing to create a more liquid market, which itself generates stickiness, as well as driving customer value through the liquidity, and lower costs, seems to me like a pretty sound strategy. They have also shown a good ability to execute strategic acquisitions in an accretive way, while still maintaining a very solid balance sheet.

I don’t know what will happen short term, but I am a strong-buy for the long-term investor, even given my storied history with this stock. I think the stock is attractively valued at the current price, and as I noted earlier, recently put my money where my mouth is and added to my position at $217.

The initial analysis for this article also identified other good candidates for further consideration. NextEra and Bristol Myers Squibb look to be attractively valued based on Historical and Future valuations, and have decent upside to analyst estimates.