LdF

LdF

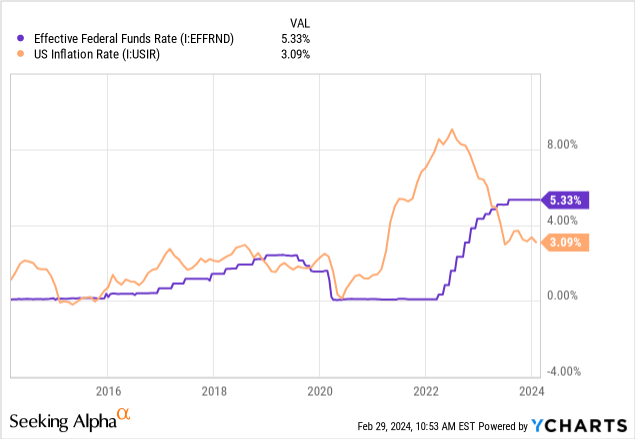

Over the past decade, low interest rates have defined fixed income investing. With persistent rock bottom rates, many households and retail investors found themselves in an uncomfortable situation. Interest earned on savings accounts, cash equivalents, and other short term investments was close to zero, let alone the rate of inflation.

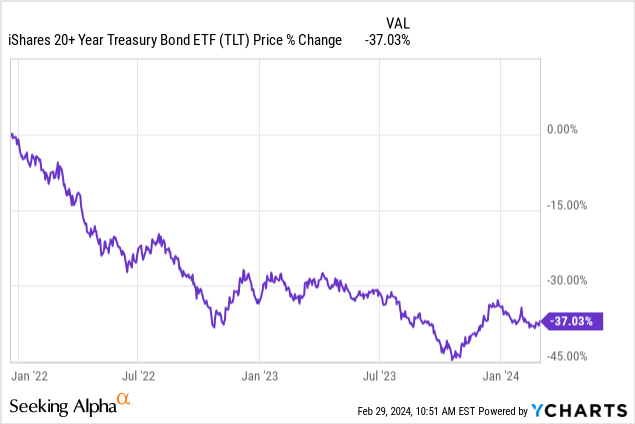

As rates remained low, the yield curve was relatively flat. It was flat enough that even long duration bonds couldn’t hedge inflation. To make matters worse, the interest rate risk on these bonds left material downside exposure for anyone willing to stretch for the yield. As interest rates have since increased, the pain has materialized for anyone holding long term fixed rate securities.

The pain shown above has opened an opportunity. We can boldly proclaim that “cash is no longer trash”. An increasing federal funds rate means short term, cash equivalents like treasury bills or short term certificates of deposit now have material yield. With the Fed Funds target rate now sitting at 5.25% to 5.50%, interest earned on most interest bearing instruments is above inflation.

The reversal in spread has contributed to massive inflows to money market and short term fixed income funds. With limited volatility, these investments now earn enough to beat inflation and surpass many other income producing assets like dividend stocks or many REITs. As the category quickly gains popularity, it becomes increasingly important to be selective. There are a variety of short and ultrashort exchange traded funds available.

Today, we are going to circle back on the PIMCO Enhanced Short Maturity Active Exchange-Traded Fund (NYSEARCA:MINT). With nearly $11 billion in assets under management, MINT is a popular option for those seeking a cash alternative with extra juice. We are going to take a critical look at MINT and explore areas where the fund falls short.

The PIMCO Enhanced Short Maturity Active Exchange-Traded Fund is a short term bond fund sponsored by PIMCO, a Newport Beach based asset manager. MINT invests in fixed income securities across the world, focusing mainly on the United States. The fund invests in bonds and other securitized credit instruments.

MINT invests in debt targeting a portfolio maturity inside of three years. The fund seeks to benchmark the performance of its portfolio against the FTSE 3-Month Treasury Bill Index.

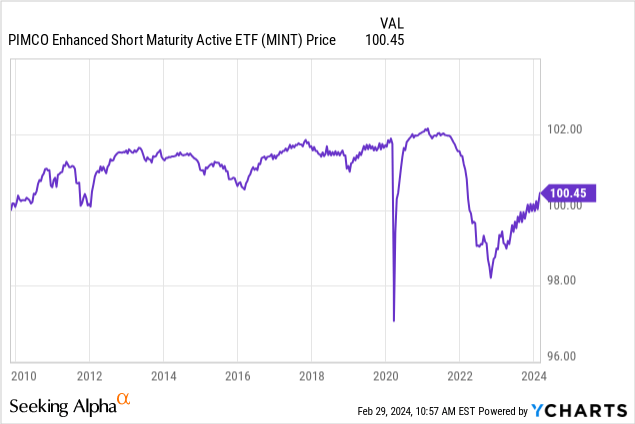

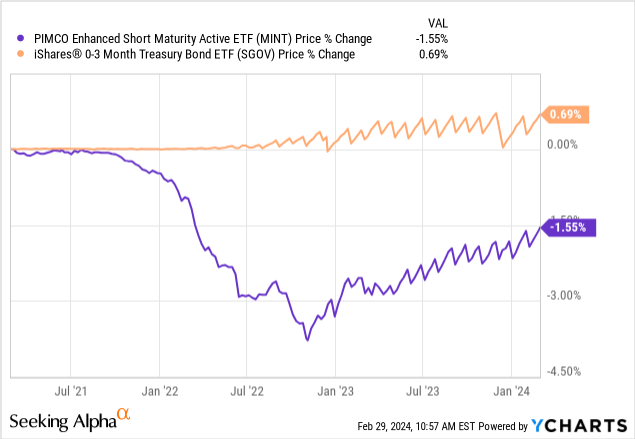

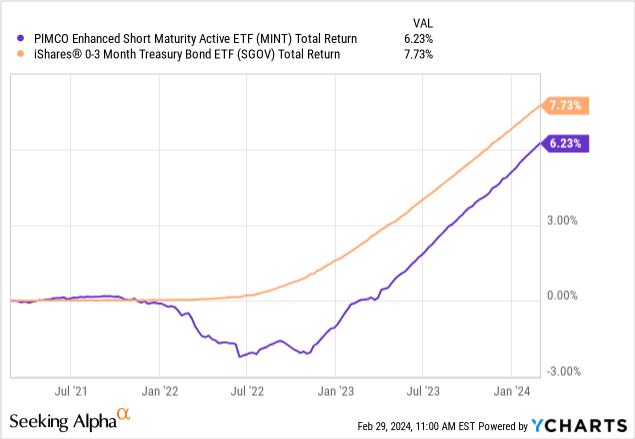

MINT is often compared to a money market fund or equivalent. That said, there are important differentiators. The largest of which is MINT’s floating share price. Traditional money market funds guarantee principal value at $1.00 per share, whereas MINT’s share price changes as with any other stock. The choppiness in MINT’s monthly share price stems from the monthly distribution of interest income earned by the fund’s investments. However, beyond the ex-dividend related share price disruption, we see that MINT is significantly more volatile than other competing funds, such as the iShares 0-3 Month Treasury Bond ETF (SGOV)

To understand why, we should explore the strategy and understand what MINT is working to achieve. A key component of MINT’s name is Enhanced. What does PIMCO exactly mean by enhanced? Although MINT is touted as a cash equivalent fund, the portfolio is anything but. While SGOV invests in short term treasury bills, MINT invests in more complex, longer term investments.

PIMCO

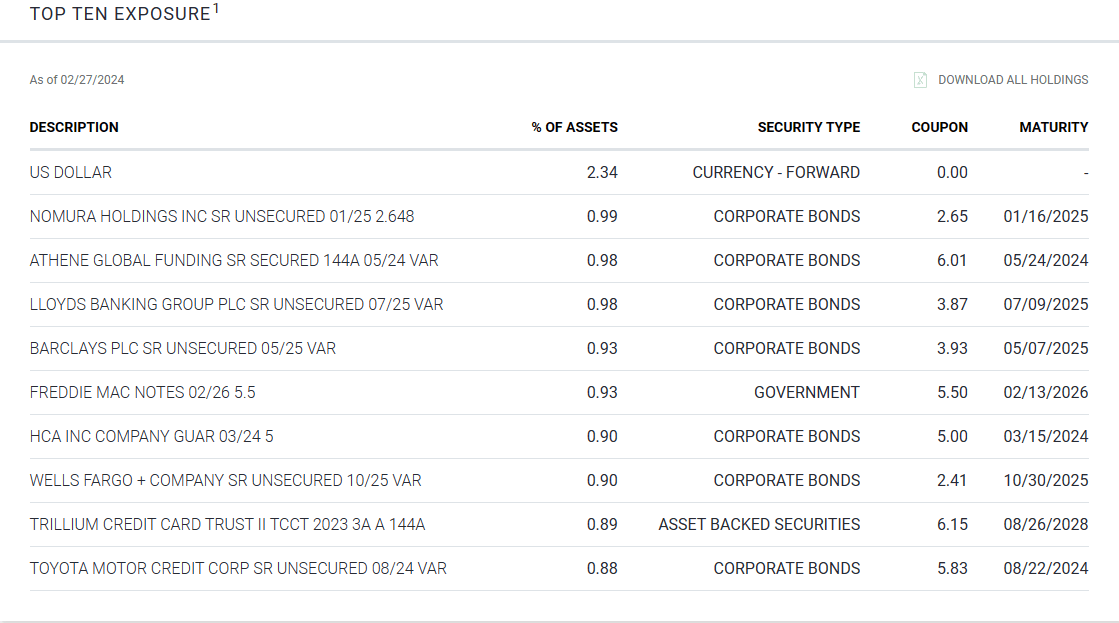

The fund’s top ten investments represent riskier names including Nomura (NMR), Barclays (BCS), and some ABS exposure. If we look deeper, we will learn that MINT has complex securities in the portfolio such as collateralized loan obligations. As of the most recent semiannual report, MINT’s management team noted the following as contributors to performance.

Overweight exposure to select securitized credit, particularly collateralized loan obligations, contributed to relative performance, as spreads tightened.

Overweight exposure to investment grade corporate credit, specifically financials, contributed to relative performance, as spreads tightened.

Underweight exposure to U.S. duration contributed to relative performance, as the inverted U.S. yield curve provided a carry advantage versus the benchmark, the FTSE 3-Month Treasury Bill Index, as short term U.S. rates rose.

This is a vastly different portfolio and strategy than those of SGOV or other cash equivalent ETFs. Worryingly, MINT has not outperformed SGOV in terms of total return, stability, or interest earned.

MINT’s index creates a fundamental issue for the fund. MINT is indexed against the three months treasury index, which is essentially a cash equivalent. As shown in the top ten holdings, MINT has exposure to bonds maturing far outside of twelve months, generating additional duration exposure for the fund.

PIMCO is effective at managing fixed income risks such as duration exposure, however these added risk factors mean MINT creeps further and further away from a true cash equivalent. I believe using an index of three month treasury bills is misleading as to MINT’s real strategy.

I think a more comparable index for MINT investors compare against is the Bloomberg U.S. 1–5 Year Government/Credit Float Adjusted Index. Rather than short term treasuries, this index tracks the market for investment-grade, U.S. dollar-denominated, fixed-rate treasuries, government-related, and corporate securities. The maturity range is slightly longer, reaching out to five years.

Despite holding securities with more risk, SGOV has been comparable in terms of yield. The primary driver here is the expenses charged by each fund. SGOV currently charges just 0.07% as an expense ratio, while MINT charges 0.35%. The 28 basis point spread comes directly from the interest earned by the fund. For MINT to match SGOV’s yield, management must find an additional 28 basis of yield to offset the added expenses.

Long story short, management is underearning their fees in my view. Despite saddling shareholders with additional risk, MINT lacks the stability of shorter term funds and fails to deliver a meaningful yield spread that would make the extra risk worthwhile.

SGOV or a traditional money market mutual fund may be cheaper options for cash management solutions than an actively managed fund like MINT.

Cash has staged a heroic reemergence as an attractive asset class. Following a protracted period of bottomed interest rates, we can now earn a return on our cash. This sets the stage for a paradigm shift in how investors approach their portfolios.

Ultrashort bond and treasury ETFs have become increasingly popular as their dividend rates have steadily climbed. As yield reaches higher, assets under management continue to increase as investors pile into interest bearing securities.

MINT is a popular cash equivalent ETF. However, more risk lies under the hood than investors often give credence to. While competing funds like SGOV invest purely in cash equivalents, MINT takes a more active approach investing in more complicated securities. However, the fund fails to deliver a meaningful yield premium that would overcome the added risk. With those factors considered, SGOV or a traditional money market is likely better suited as a cash equivalent.