kschulze/iStock via Getty Images

kschulze/iStock via Getty Images

M/I Homes, Inc. (MHO), together with its subsidiaries, engages in the construction and sale of single-family residential homes in Ohio, Indiana, Illinois, Minnesota, Michigan, Florida, Texas, North Carolina, and Tennessee.

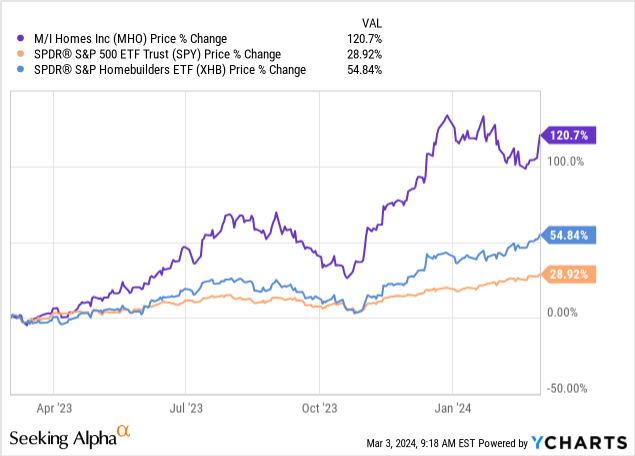

The firm’s stock price has seen an extraordinary, more than 120%, increase over the past 12 months, significantly outperforming the broader market, which has "only" gained 29% in the same period.

While we have covered other firms in the homebuilding industry before, e.g. we just recently published an article on D.R. Horton (DHI), this is going to be our first writing on MHO. Today, our focus will be on both macro- and microeconomic factors that are expected to have a material impact on the company’s share price in the coming quarters. We will start our discussion by looking at a set of economic indicators, like consumer confidence, home sales, building permits and inflation rate. In parallel, we will also be examining the impact of these macroeconomic factors on the firm’s latest earnings results to gauge, whether the recent rising trend in share price is likely to continue in the near term or not. We will also make several references to our article on DHI for completeness.

When writing about a company in the homebuilding industry, it is crucial to understand the broader trends of the housing market. Let us look at three indicators here, namely the new home sales, the existing homes sales and the building permits in the United States.

New home sales (tradingeconomics.com) Existing home sales (tradingeconomics.com) Building permits (tradingeconomics.com)

Based on the three graphs above, we can say that the housing market is not in its healthiest state. Existing home sales are hovering close to their historic lows, while both building permits and new homes sales are around their pre-pandemic levels. This relative weakness of the housing market can be largely explained by the Fed’s recent actions with regards to interest rates. As inflation started to raise concerns in 2021 and 2022, the Fed has started to increase the interest rates to protect the economy from overheating. As a result, the effective Fed funds rate has reached almost 5.4% in the second half of 2023. Such high interest rate levels lead to more expensive mortgages, which essentially makes housing less affordable, causing a decline in demand for housing units.

U.S. Inflation rate (tradingeconomics.com) Effective Fed funds rate (tradingeconomics.com)

These macroeconomic headwinds are clearly visible in MHO’s latest earnings report, released in January 2024. First of all, the company has significantly missed both top- and bottom-line estimates. EPS in Q4 came in at $3.66, $1.28 lower than expected and significantly lower than the 2022 Q4 figure of $4.65. Revenue in Q4 declined by 20% year-over-year, totaling in $972.6 million, $217.4 million lower than earlier expected. For the whole year of 2023, the number of homes delivered, the revenue and the pre-tax income have all decreased compared to the prior year. The return on equity and the contract backlog have also been trending downwards. The decrease in the contract backlog is especially concerning, because it is an early indication of future revenue declines.

Highlights (MHO) Summary (MHO) Backlog (MHO)

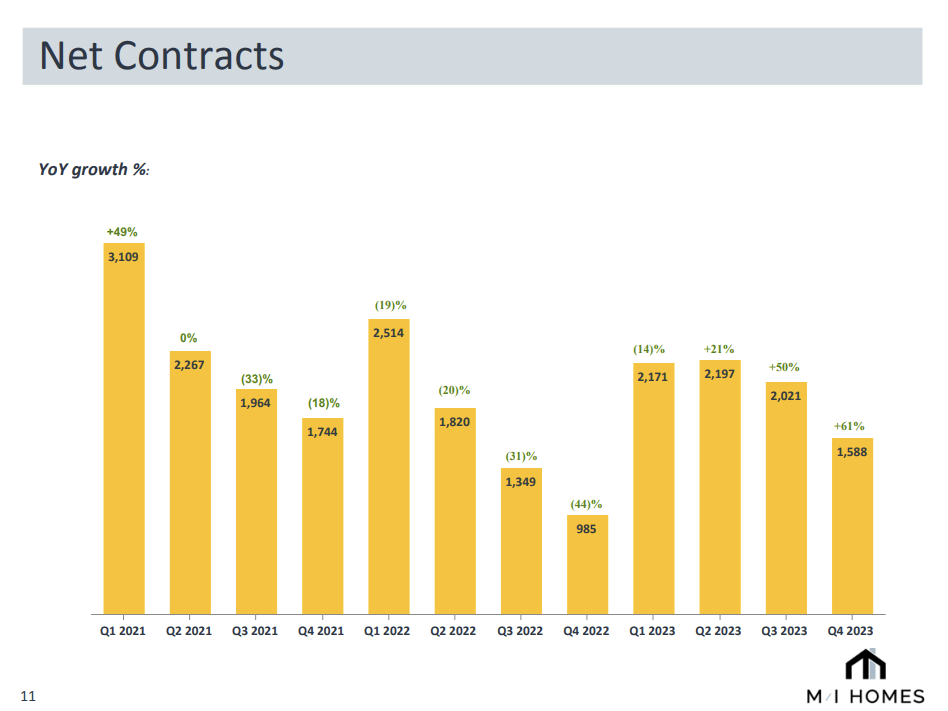

The number of new contracts in Q4 have increased by 61% YoY, which gave us a slight hope. However, when we looked closer, we realized that the situation is not as good as it seems. Actually, net contracts are showing a downward trend, but due to the extremely poor Q4 in the prior year, the last quarter comparison appears to be attractive.

Net contracts (MHO)

We believe that these results are not surprising, considering the state of the economy in general and the state of the housing market. Furthermore, the tailwinds of the housing market driven by the work-from-home trends after 2020 seem to have diminished by now. And, with all these headwinds, in our opinion, the recent run-up in share price is not justified and not sustainable in the longer term.

On the other hand, the Fed is expected to cut interest rates gradually, starting this year, which could generate significant tailwinds for MHO and other firms in the homebuilding industry. This tailwind in likely already priced in, and therefore we do not see significant upside from these price levels. At this point, however, due to the significant macroeconomic uncertainty, we would be more comfortable with investing in a firm, which can demonstrate more robustness and more resilience even during times of market stress. If you are looking for a firm like this in the homebuilding industry, take a look at our recent writing about DHI, which discusses the key points of their latest earnings results and also highlights why they have managed to achieve relatively strong results and increase their market share, despite the headwinds.

To discuss the company’s valuation, we will take a look at a set of traditional price multiples. The following tables compared MHO’s figures with those of the respective sector median, with those of its industry peers and with its own historic averages.

Valuation (Seeking Alpha) Valuation (Seeking Alpha)

While MHO appears to be trading at a discount compared to the industry peers, it is trading at a significant premium compared to its own 5Y averages. At this point, however, we need to consider that the firm’s latest financial results compare relatively poorly to those of DHI, for example. Further, MHO does not pay any dividends, while DHI does, with a current quarterly dividend rate of $1.20 per share. DHI has even managed to keep paying and grow these dividends over the past 9 years in each year. Most of MHO’s profitability metrics are also less appealing than those of DHI’s, including the EBITDA margin, the net income margin, the return on equity and the return on assets.

Comparison (Seeking Alpha)

As we do not see the housing market improving significantly in the coming quarters, we believe that we cannot justify a new investment in a firm in the homebuilding industry, which does not demonstrate robustness and resilience, and which in turn exhibits decreasing sales, decreasing home deliveries and decreasing EPS.

The challenging macroeconomic environment, including elevated interest rates, elevated inflation levels and low consumer confidence, creates significant headwinds for MHO’s business. The state of the housing market is also relatively weak, with existing home sales hovering around historic lows.

As a result, MHO’s latest earnings have shown a decrease in revenue, a decrease in the number of homes delivered and also a decrease in EPS. The return on equity has also contracted, and contracted backlog has also kept decreasing.

While MHO is selling at a discount compared to its industry peers, we believe that in these uncertain times it is more justifiable to invest in an industry leader, like DHI, that can demonstrate robustness and resilience and has better profitability metrics even during turbulent markets.

For these reasons, we rate MHO’s stock as “hold” now.