The Wisconsin State Capitol building in Madison.

CharlieTong/iStock via Getty Images

The Wisconsin State Capitol building in Madison. CharlieTong/iStock via Getty Images

Those who know me personally and through following my work here on Seeking Alpha know that I especially appreciate statistical trends. Each day, I am blessed to research new trends that stay with me. Those who also know me may be aware of the fact that I was born, raised, and have lived in the Badger State my whole life.

Those who know me personally and through following my work here on Seeking Alpha know that I especially appreciate statistical trends. Each day, I am blessed to research new trends that stay with me. Those who also know me may be aware of the fact that I was born, raised, and have lived in the Badger State my whole life.

There's nothing better than combining my love for data with the appreciation that I have for my state (especially with the winter we've been having so far this year). Over the years, I have had the privilege of covering some great Wisconsin-based utilities like Alliant Energy (LNT) and WEC Energy Group (WEC) on SA.

Today, I am going to initiate coverage with a buy rating on shares of Madison Gas and Electric Company or MGE Energy (NASDAQ:MGEE). As I will expand on as the article progresses, I believe MGE Energy is a quality electric and gas utility. However, the appeal extends beyond this statement of fact alone. Demographic trends within its Madison, Wisconsin-based service area are also firmly on its side.

Dividend Kings Zen Research Terminal

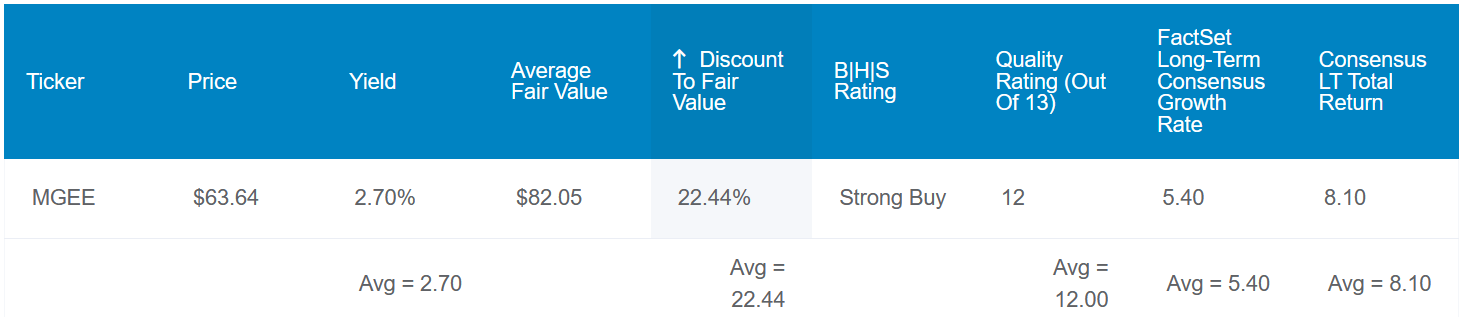

MGEE's 2.7% dividend yield is well below the utility sector median of 4% according to Seeking Alpha's Quant System. That's why the stock earns a D- grade for yield relative to its peers. However, this is still almost double the 1.4% yield of the S&P 500 (SP500) index. Not to mention that with 48 consecutive years of dividend growth, the company earns an A+ from Seeking Alpha's Quant System on dividend consistency.

There are also plenty of reasons to believe that MGEE's dividend can keep moving higher over time. For one, the company's 49% EPS payout ratio is far below the 75% EPS payout ratio that rating agencies believe is safe for the electric and gas utility industry. MGEE's 38% debt-to-capital ratio is also considerably less than the 60% debt-to-capital ratio that rating agencies prefer from the industry. This suggests the company's balance sheet is capitalized quite well.

For these reasons, the probability of MGEE cutting its dividend in the next average recession is just 0.5% or one in 200. Even in a severe recession, the likelihood is only 2% or one in 50. For perspective, these are both the lowest allowed values in the Zen Research Terminal.

Dividend Kings Zen Research Terminal

MGEE's valuation also appears to be another factor that supports my buy case. The five-year average dividend yield for MGEE is 2.1% according to Dividend Kings' Automated Investment Decision Score Tool spreadsheet, which implies an $83 fair value. Averaging that out with the $80 fair value using a P/E ratio of 21.9, shares could be worth $82 each. That would indicate the electric and gas utility's shares are 22% undervalued.

If MGEE returns to fair value and grows as anticipated, here are the total returns that it could produce over the next 10 years:

When investing in publicly traded utilities, I like to dive into the demographics of the service area and the regulatory environment in which a utility operates. That's because I view these factors as just as important as other factors, such as a company's financial position.

If a company operates in an economically prosperous service area and the regulatory environment is optimal, great results are much more likely. This is why MGEE is of such interest to me.

As of Dec. 31, 2023, the company served 163,000 electric customers in a 264-square-mile service area within Dane County, Wisconsin. MGEE's electric operations accounted for roughly 71% of the $690.4 million in total regulated operating revenue in 2023.

At the end of 2023, the company's natural gas business served 176,000 customers. This 1,684 square-mile service area was spread throughout seven south-central Wisconsin counties, including Madison and the surrounding areas. MGEE's natural gas operations contributed to the remaining 29% of the $690.4 million in total regulated operating revenue in 2023 (all details in the previous two paragraphs were sourced from pages 7-8, 11, and 59 of 120 of MGEE's 10-K filing).

MGE Energy Q4 2023 Investor Presentation

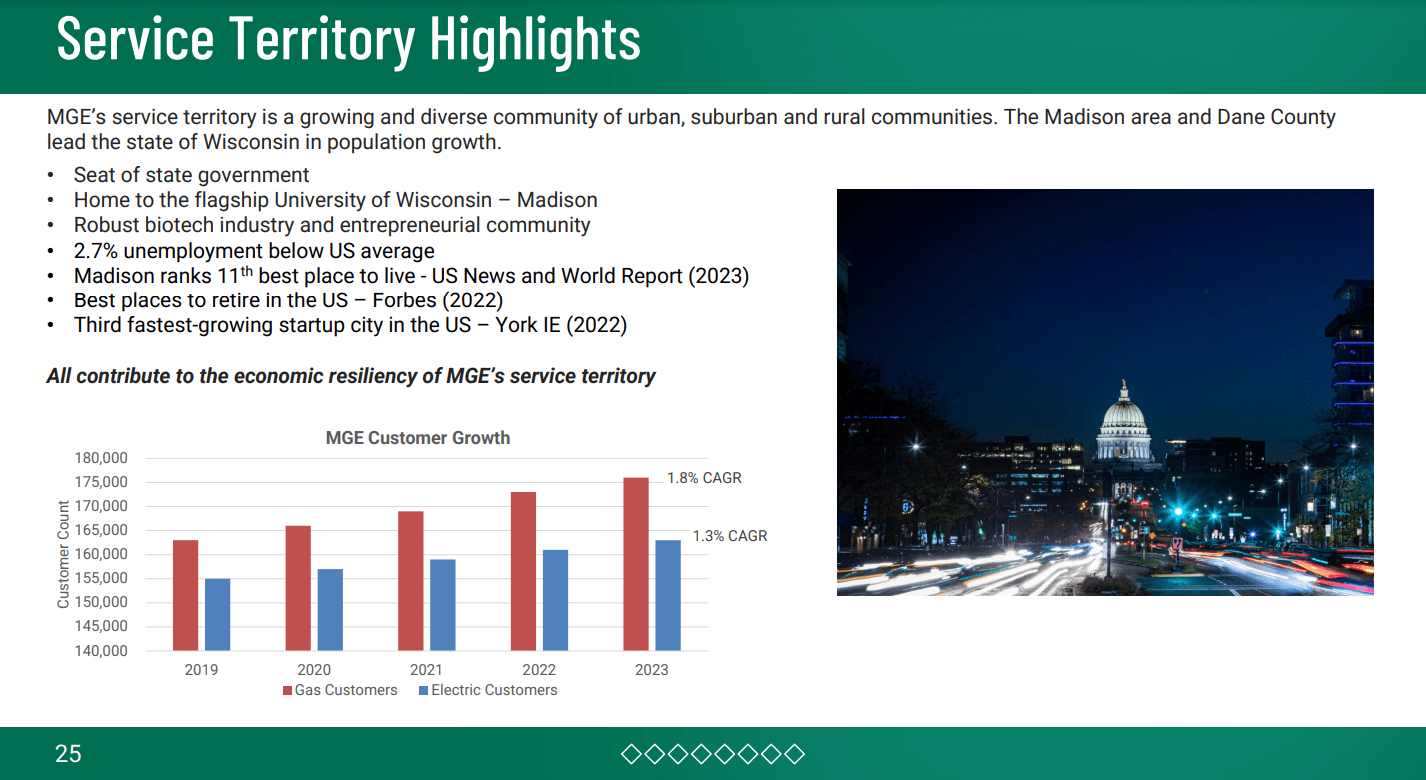

In my view, the appeal of operating in the Madison area is obvious. In the last five years, the Madison metropolitan area has grown at an average rate of 1.4% annually to 507,000 as of 2023 per data from Macrotrends. For context, that's about triple the 0.5% average annual growth rate of the U.S. population to 340 million as of 2023 according to Macrotrends.

As a result, this level of growth leads the entire state of Wisconsin. Several factors are underpinning these favorable demographic trends. That includes one of the best public universities in the country, UW Madison. The area's world-class university is also attracting some of the best and brightest minds in the country and the world. Thus, it shouldn't be a surprise that Madison benefits from a vibrant economy. This is led by top employers, such as UW Madison, UW Health, and healthcare software giant Epic Systems. This economic environment helped to keep the unemployment rate at just 2.7% - - below the U.S. average.

These demographics have allowed MGEE's natural gas customer base to compound by 1.8% annually in the past five years. Electric customers have compounded by 1.3% annually during that time (unemployment rate and natural gas/electric customer growth rates according to slide 25 of 33 of MGEE's Q4 2023 Investor Presentation).

MGE Energy Q4 2023 Investor Presentation

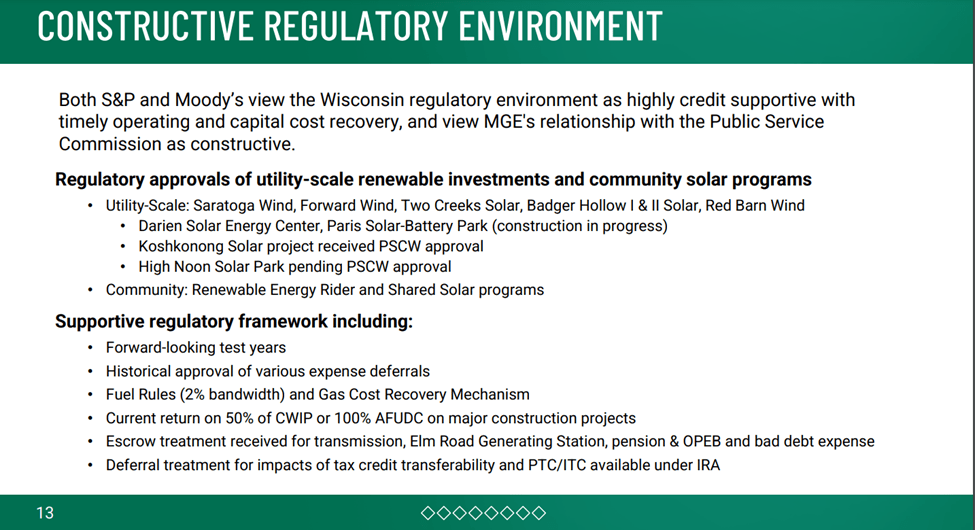

As if this wasn't enough, the company is the beneficiary of what S&P and Moody's consider constructive regulatory environments. That's because the Public Service Commission of Wisconsin allows operating and capital cost recovery mechanisms in a timely manner per the rating agencies.

Coupling that with the strong balance sheet that I noted at the beginning, S&P rates MGEE's corporate credit an AA- on a stable outlook (slides 13 and 27 of 33 of MGEE's Q4 2023 Investor Presentation).

These elements explain how MGEE has been able to generate 6% annual diluted EPS growth over the last five years, with diluted EPS reaching $3.25 in 2023 (slide 6 of 33 of MGEE's Q4 2023 Investor Presentation and MGEE's Q4 2023 Earnings Press Release).

In better news, diluted EPS growth should be even better in the next couple of years. The FAST Graphs analyst consensus is for diluted EPS to rise by 13.2% to $3.68 in 2024. In 2025, the FAST Graphs consensus is that MGEE's diluted EPS will climb another 8.7% to $4.

There will be at least a few factors in play that are expected to contribute to this growth, which is why I agree with these forecasts. First, annual customer growth should remain between 1% and 2% in these years due to the demographic trends that I highlighted above. More customers equals higher operating revenue.

On top of that, higher electric and natural gas rates should also be a boost to the top line. The PSC of Wisconsin authorized 1.54% higher electric rates in 2024 and 2.44% higher natural gas rates. In 2025, electric rates will grow another 4.17%, and natural gas rates will increase by 1.32% (slide 15 of 33 of MGEE's Q4 2023 Investor Presentation).

Finally, the company is becoming more efficient operationally. For instance, operating expenses relative to total operating revenue fell from 80.7% in 2022 to 78.8% in 2023 (calculations made from data sourced on page 59 of 120 of MGEE's 10-K filing). As MGEE makes additional investments to drive efficiency, this should further improve margins. That will drive bottom-line growth for the company.

As I alluded to earlier, MGEE has upped its quarterly dividend per share for 48 consecutive years. In the last five years, the payout has grown by 26.7% cumulatively - - a 4.9% compound annual growth rate.

Moving forward, I anticipate that dividend growth will be at least as strong. That's because the analyst consensus for 2024 diluted EPS is $3.68 per FAST Graphs. Against the $1.71 in dividends per share that will likely be paid this year, that would be a diluted EPS payout ratio of just 46.5%.

MGEE is a superb utility, which is evidenced by its track record of earnings growth and industry-leading AA- credit rating from S&P. However, the company still faces risks.

One of the more noteworthy all-around risks to MGEE is its geographic concentration. The Madison area is an ideal service area for a utility to operate. But if that doesn't continue to be the case (e.g., the local economy deteriorates and residents start leaving the area), it could weigh on the company's results.

Wisconsin tends to be friendly toward utilities with rate cases, although there is no guarantee that will remain the case. If MGEE can't recover costs promptly, this could also hurt its results.

Finally, there is the risk that the Madison area could be hit hard by natural disasters. If that happened, the company's operating results could be disrupted. Even worse, damage could be inflicted on MGEE's infrastructure beyond its insured amounts. That may end up breaking the investment thesis.

FAST Graphs, FactSet

MGEE is a top-notch electric and gas utility. Yet, the current situation with elevated interest rates is weighing on its valuation right now. As interest rates eventually make their way back down, I believe the market's perception of MGEE will improve. This is because the fundamentals are arguably as strong as they have been at any point in the last decade or two. Accordingly, I see no reason why the stock won't re-rate from its present blended P/E ratio of 19.2 to the normal P/E ratio of 21.4.

If MGEE's earnings growth matches the consensus and it returns to fair value, 40% cumulative total returns could be in store between now and the end of next year. That's precisely why I'm starting coverage with a buy rating.