Tomohiro Ohsumi/Getty Images News

Tomohiro Ohsumi/Getty Images News

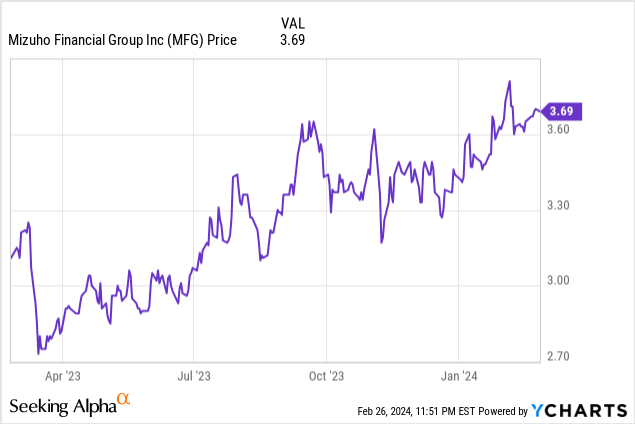

It’s been a great time to be long Japanese megabank Mizuho Financial Group (NYSE:MFG), and since my last coverage (see here), which outlined the upside case in the aftermath of a sector-wide selloff this time last year, the stock has moved up and to the right.

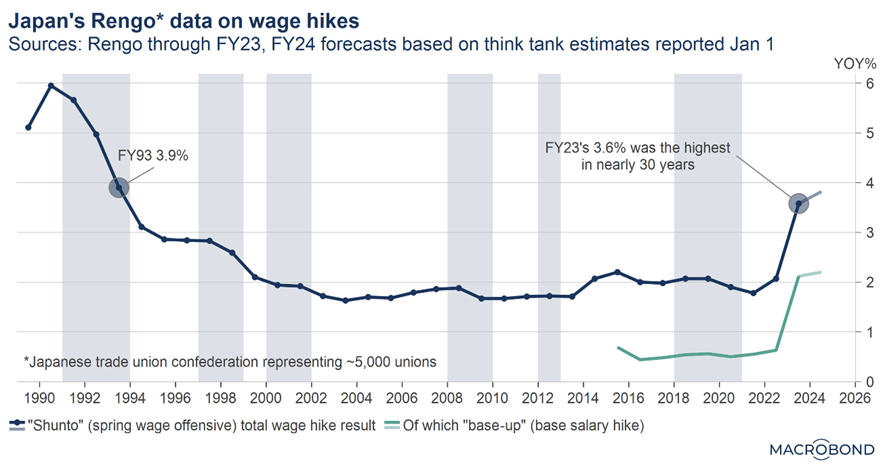

MFG hit all the right notes again in its latest quarter (fiscal Q3 2023), even pacing ahead of full-year guidance numbers (which management only just raised in fiscal Q2). Though domestic banking remains a tough business amid Japan’s negative interest rate regime, wider loan spreads overseas, as well as growth in fee-related income, have helped. So has investment income, which added further bottom line cushion in the face of the latest round of "shunto" wage hikes. With core margins holding firm, though, the decision to reiterate, rather than raise guidance looks increasingly conservative and bodes well for big upside surprises at full-year results later this year.

Under President Masahiro Kihara, who took the helm in early 2022, MFG also is undergoing some interesting mid-term reforms. If successful, expect profitability improvement and a good deal of value unlocking down the line, all of which bodes well for the bank’s return on equity - ROE - profile. Even if reforms don’t pan out anywhere near as successfully as planned, the low payout ratio means there’s still ample capacity for shareholder returns, particularly as MFG also shores up its capital base. The catch for the US listing is that currency fluctuations can erode the payout slightly (hence the negative SA dividend scorecard), though the yield should still remain a very solid one.

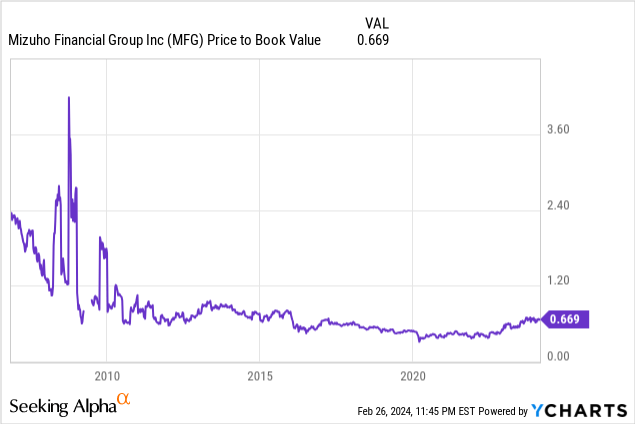

Plus, there’s the wide 30%-40% book value discount, which implies very cheap optionality if either MFG management delivers on reforms or the BoJ delivers on monetary policy normalization in April. In line with the trifecta of "buy" ratings across Seeking Alpha’s Quant, Analyst, and Street scorecards, I see ample room for the stock to head higher from here.

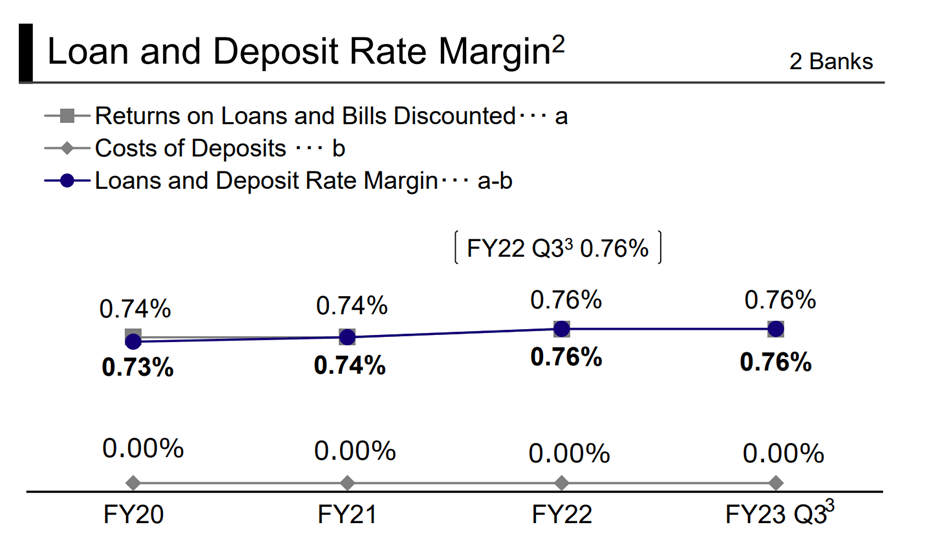

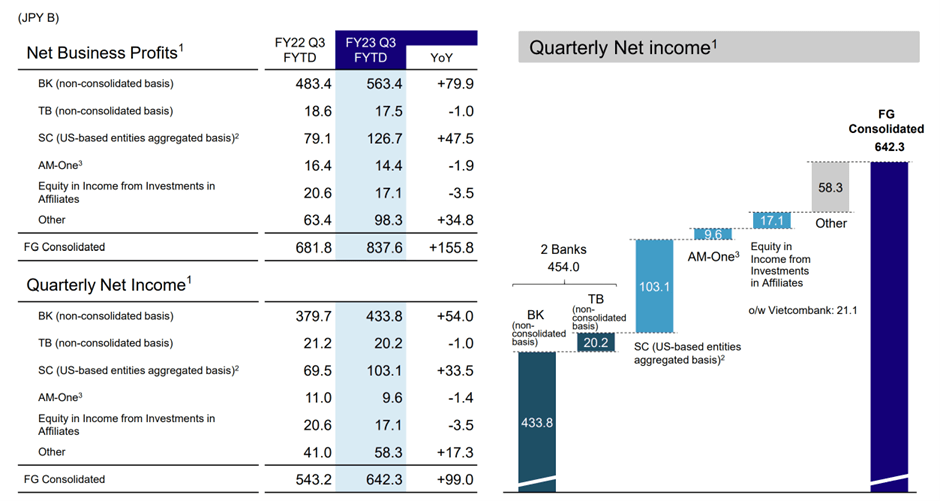

MFG was out with a very solid fiscal Q3 to-date report earlier this month, with total profits attributable to owners of JPY642bn already above management’s full-year guidance of JPY640bn. Doubly impressive was that the bank achieved this result with little help from domestic interest rates or a Japanese economy that has technically slipped into recession. Of note, MFG's loan spreads in Japan have been resilient despite competition and rate headwinds, while lending activity also has been healthy.

Mizuho Financial Group

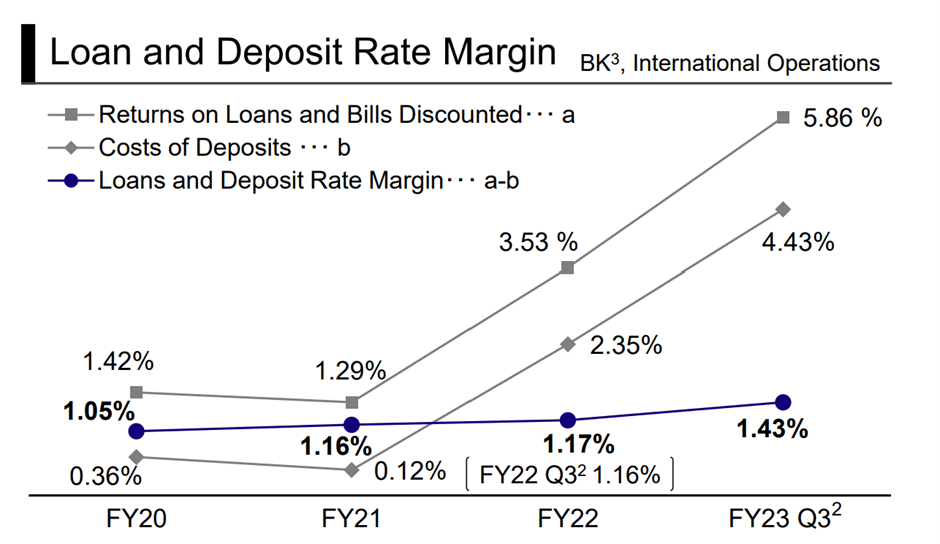

But MFG’s diversified earnings base also has helped massively - not only in fee-related businesses like corporate and investment banking (major positive swing factors to book value growth thus far) but also in its foreign banking operations, where loan and deposit spreads have seen good expansion.

Mizuho Financial Group

The only real blemish, albeit a very modest one, was costs, as heightened wage pressures amid a weaker yen and higher inflation backdrop dragged on margins. Management also has been deploying capital into growth areas, mainly overseas, which has nudged up the cost/income ratio slightly. But expense growth paled in comparison to top-line gains and one-offs from unrealized gains elsewhere in the securities portfolio, driving consolidated net business profit growth of >20% YoY on a fiscal year-to-date basis.

Mizuho Financial Group

And with net income attributable to shareholders, the key guidance metric, already ahead of full-year guidance, the mid-term guidance bar may be due for a raise sooner rather than later. For now, though, management hasn’t altered its guidance, which leaves good buffer against any unforeseen credit costs or investment-related one-offs down the line.

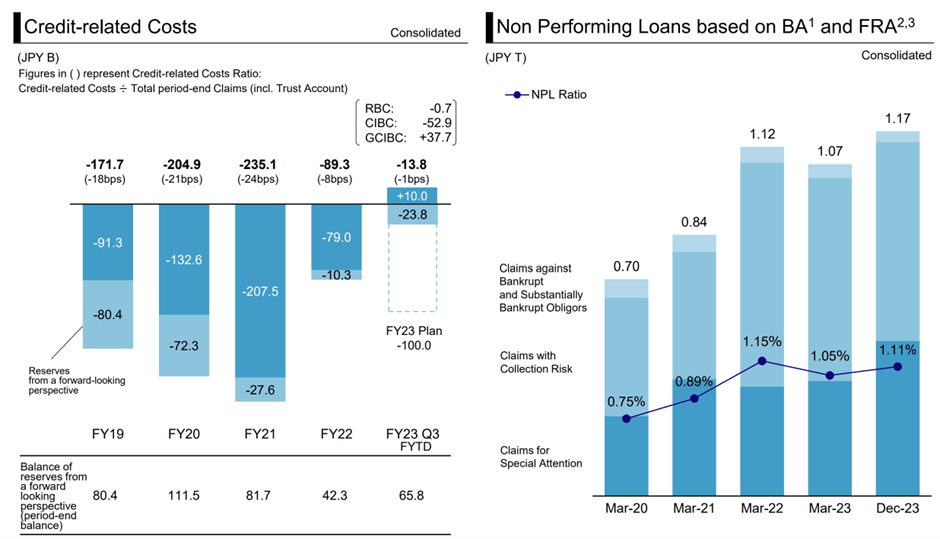

As for the balance sheet, it’s been so far, so good. Non-performing loans are running slightly higher, though at 1.1% in fiscal Q3, it remains well under control. Meanwhile, credit costs are trending favorably, even after including some big reversals from retirement benefit trusts, so unlike Aozora Bank (OTCPK:AOZOY), there’s been no indication of real estate contagion here. In any case, MFG’s capital ratio is adequate at the current ~11.5%, ensuring good headroom relative to the bank's 9%-10% minimum.

Mizuho Financial Group

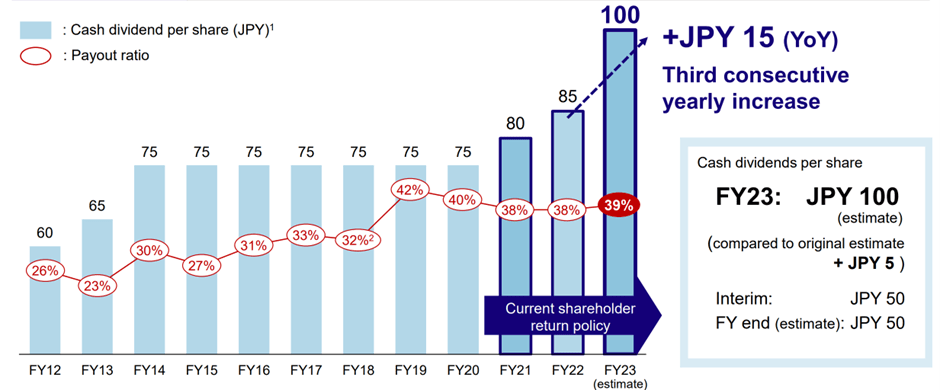

The bank’s other liquidity and funding metrics also screen very strongly, and alongside a relatively low payout ratio, I see its current dividend growth path (up to JPY100/share per fiscal 2023 guidance) as very sustainable. There's a risk that the yen depreciation eats into the dollar-denominated payout (a factor SA’s dividend screen has picked up on), though at an implied 3%-4% yield, MFG investors should still get a nice income bonus here.

Mizuho Financial Group

Besides income, MFG’s balance sheet headroom is key to enabling the planned reforms outlined by President Masahiro Kihara. In particular, the bank’s management team has shown encouraging intent on unlocking value from its eclectic mix of portfolio assets – key to improving overall ROEs and narrowing the stubborn book value discount. In addition to shedding "higher risk/lower return" assets, efforts to protect profitability, particularly on the cost side, will be key in light of renewed pressure from recent "shunto" wage negotiations. In any case, reform success doesn’t appear to be priced in at the current 30-40% book value discount, so the re-rating optionality adds to an already favorable risk/reward.

Mizuho Financial Group

Reforms may take time and a lot of will from management, but the biggest needle-mover lies in the hands of the BoJ, in my view. Governor Ueda has been signaling monetary policy normalization for a while, though the timing of an exit from negative interest rates has been continually pushed back - to the chagrin of bank investors. The upcoming monetary policy meeting in April could mark a notable policy shift, as the combination of robust wage growth, corporate earnings, and labor market tightness over the last year threaten to reinforce a “virtuous cycle between wages and prices.” Also on the agenda are exits from asset purchases by the central bank and "Yield Curve Control" (i.e., a policy to cap government bond yields), both of which would finally lift Japan out of a negative rate regime.

Macrobond

Higher interest rates, even if gradual, bode well for the megabanks, all of which have lagged the broader index since Japan implemented ultra-loose monetary policy. MFG is no different, as though it doesn’t have the highest interest rate sensitivity, each 10bps policy rate hike still adds a hefty JPY50bn to net interest income (per fiscal Q2 2024 estimates).

Perception also is key. Unlike prior years when Japanese banks suffered from a negative rate overhang, normalized rates would allow investors to underwrite Japanese banking stocks in line with global norms. In combination with reforms (internal and external, as imposed by the TSE), MFG has a clear path to both ROE improvement and improved shareholder returns over time. Yet, the market is skeptical on both counts as its current 30%-40% book value discount and below-peer valuation shows. Thus, MFG arguably offers more upside than its megabank peers, particularly if it also supplements its dividend hike with a buyback at the upcoming full-year results.

Bloomberg

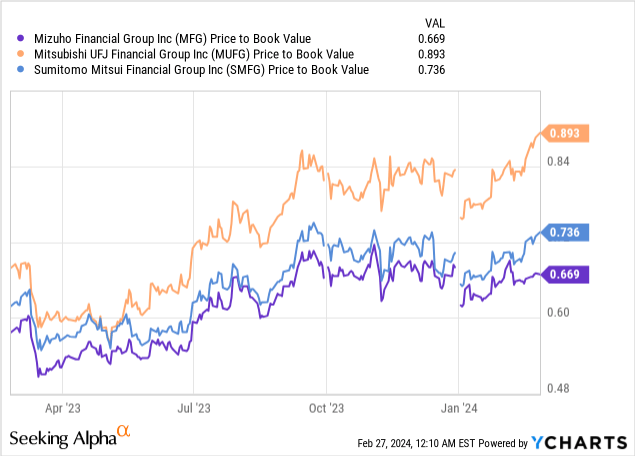

Coming off another strong quarter and with multiple catalysts in the pipeline, MFG appears poised to extend its run into 2024 and beyond. The reform angle will continue to be one to watch, with new management making good headway both on earnings growth and shareholder returns. Most importantly, though, for MFG’s domestic banking business is the BoJ following through with monetary policy normalization at its April meeting. After years of ultra-loose policy and consistent delays to exiting, the market isn’t pricing in very much at the current ~0.67x P/B (cheapest among the Japanese megabanks), implying very cheap optionality on offer. Alongside a well-covered low-single-digit percent yield (subject to currency fluctuations), MFG’s high Seeking Alpha ratings are well deserved, in my view.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.