fcafotodigital/E+ via Getty Images

fcafotodigital/E+ via Getty Images

Historically, Medifast (NYSE:MED) has successfully ridden the wave of the ever-growing health & wellness industry. Boasting continuous growth, impeccable ROIC metrics, and a pristine balance sheet in a secular growth market, it may seem folly to argue against buying shares and partaking in the company's seemingly unstoppable success. While the company clearly has had a successful past, it is important not to turn a blind-eye to the dynamism of the industry in which it operates - and the implications this could have for the company's future. I thereby give this investment opportunity a 'Hold' rating due to the disruptive market forces causing uncertainty around the business's fundamentals, while also considering the undeniably cheap valuation of the company's shares.

Medifast, founded in 1980 and headquartered in Baltimore, is a health and wellness company primarily known for its OPTAVIA brand. OPTAVIA is a weight-management program that utilizes independently contracted coaches to sell the company's products and guide customers on their weight-loss journeys. These coaches are not employed by Medifast, but earn money through bonuses and commissions based on their sales of the company's products.

Medifast's main product line is their Fuelings - food made by the company that is integrated into the various monthly meal plans available to the customer. These Fuelings consist of a wide variety of different food items: bars, shakes, cookies, mashed potatoes and more. Additionally, OPTAVIA offers Lean & Green meals, a selection of recipes designed for easy-to-make, homemade meals that are designed to fit seamlessly into the above mentioned meal plans.

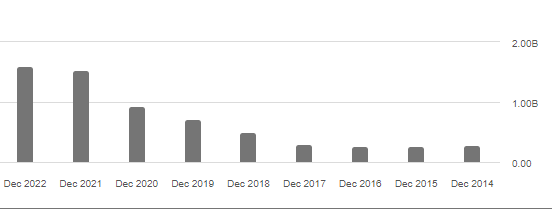

Until recently, Medifast has performed exceptionally well. Revenues have grown from approximately $285 million in 2014 to $1.598 billion by the end of 2022 - a compound annual growth rate (OTC:CAGR) of 24%:

Seeking Alpha

What's even more impressive is the consistency in the company's free cash flow (FCF) generation during the same timeframe. With FCF of $21.4 million in 2014 and $154 million in 2022, they achieved an even larger CAGR of approximately 28%:

Seeking Alpha

Furthermore, according to Morningstar, Medifast achieved an average return on invested capital (ROIC) of over 50% between the years 2014 and 2022 - an astounding rate of return especially when considering the industry average of about 20%.

Based on the following metrics from the most recent earnings report, the balance sheet is similarly impressive:

| Current ratio | 2.42 |

| Debt to equity | 0.53 |

| Debt | $0 (As of Q4 2023) |

| Net cash | $150 million |

The company has also been consistent with maintaining a net cash position over the past ten years, using operating cash flows to fund their business expansion:

Seeking Alpha

Medifast has successfully ridden the coattails of the health & wellness industry, as is clearly evident from the robust financials discussed above. The health & wellness industry as a whole, according to Precedence Research, is projected to grow from $5.24 trillion at the end of 2022 to $8.945 trillion by 2032 - a CAGR of 5.5%.

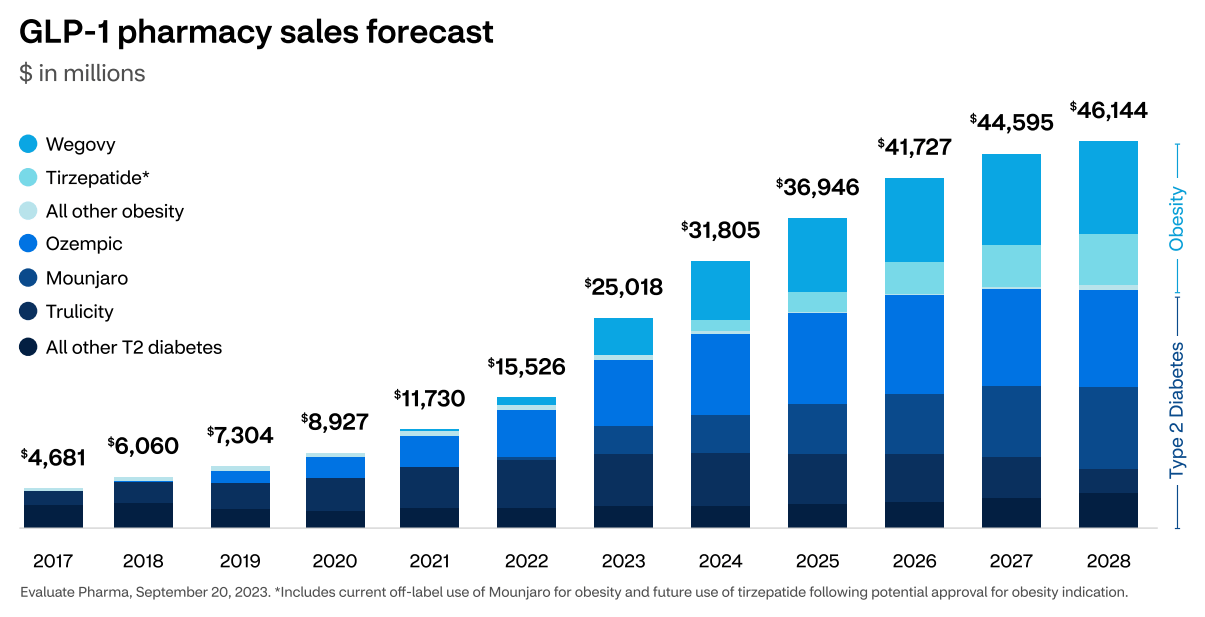

This industry is, however, a notoriously dynamic one, necessitating business agility and foresight to capture the latest market trends and developments. Take the sudden and rapid rise of GLP-1 medications for the treatment of obesity, for example. GLP-1s, which were originally developed for type II diabetes, were found to also encourage weight loss in patients by suppressing appetite and slowing digestion. Once the versatility of this drug was realized, pharmaceutical giants such as Eli Lilly and Norvo Nordisk began seeking approval from the FDA for the use of GLP-1s in obesity treatment. A recent CVS Caremark report succinctly illustrates the potential of this opportunity:

CVS Caremark

While the business opportunity in the GLP-1 space is vast, it may spell bad news for traditional weight loss companies such as Medifast. This is apparent in the precipitous drop in revenues experienced in 2023: from just under $1.6 billion in FY 2022 to $1.072 billion in FY 2023, a decline of over 30%. The company lists this as a risk in the 2023 annual report, describing GLP-1s as "favorably perceived" and "easier to use" than the OPTAVIA program, causing a "[reduction in] demand for [their] products and services". Looking ahead on a quarterly basis, for Q1 2024 Medifast is estimating revenue to be between $155 - $175 million, a massive drop from the $349 million achieved in the same quarter of 2023.

In tandem with plummeting revenues, Medifast is also rapidly losing coaches, who "remain firmly at the center of [their] efforts". At the end of 2023, Medifast's coach count was 41,100, a 32.5% decrease from the prior year, and quarterly revenue per coach dropped over 16% to $4,648 - "the first time quarterly revenue per coach was below $5,000" since 2017. In the Q4 2023 earnings release, the company attributes these deteriorating metrics to "continued pressure on customer acquisition" as a result of the "growth of GLP-1 medications in the marketplace".

While the ascension of GLP-1s could indeed be dire for Medifast, they are not taking the death knell lying down. In their FY 2023 annual report, Medifast makes clear their aspirations for "business transformation" by expanding into the "medically supported weight loss and sports nutrition markets".

Medifast is attempting to break into the medically supported weight loss industry by entering into a strategic partnership with telehealth provider LifeMD. This partnership with LifeMD (LFMD) will give OPTAVIA customers "access to board-certified affiliated clinicians and medications, such as GLP-1s" to provide a comprehensive health solution instead of focusing solely on weight loss. Based on an internal study conducted by Medifast, it was determined that 96% of those using weight loss medications also desire lifestyle changes to maintain a holistic approach to health - a statistic that Medifast hopes to leverage by partnering with LifeMD.

Medifast is also entering into the $30 billion sports nutrition market with its new line of OPTAVIA ACTIVE products. The initial products in this new line are essential amino acids and whey protein powder. In the 2023 annual report, the company claims that entry into this new category will '"[triple] its addressable market.". With these in place, the company can continue to bring related products to market such as the OPTAVIA Nutrition Kit for Medically Supported Weight Loss and the OPTAVIA Muscle Health Kit for Medically Supported Weight Loss.

Of course, none of this is free. While Medifast does indeed have a fortress-like balance sheet, the company is taking drastic measures to redirect capital towards these new initiatives. First off is the ceasing of international operations. Medifast is almost entirely a domestic company, however they do concede that international expansion is an "important component of [their] long term growth strategy". The company entered into the Singapore and Hong Kong markets during the summer of 2019. As a result of the recent market disruption however - Medifast, as of year end 2023, will cease operations in these countries to "optimize the Company's spending and investments to prepare for and catalyze sustainable future domestic growth.".

In addition, and perhaps most painful for investors, is the discontinuation of dividend payments. Prior to this announcement, the company sported a highly attractive quarterly dividend of $1.65, a CAGR of over 25% since 2015. These dividends were positively correlated with the flourishing cash flows Medifast experienced during the same timeframe - making the discontinuation all the more inauspicious. As with the halt of international operations, Medifast retracted their dividend so capital can be redirected to "grow the business through marketing and technology initiatives that are expected to increase customer acquisition and the lifetime value of customers".

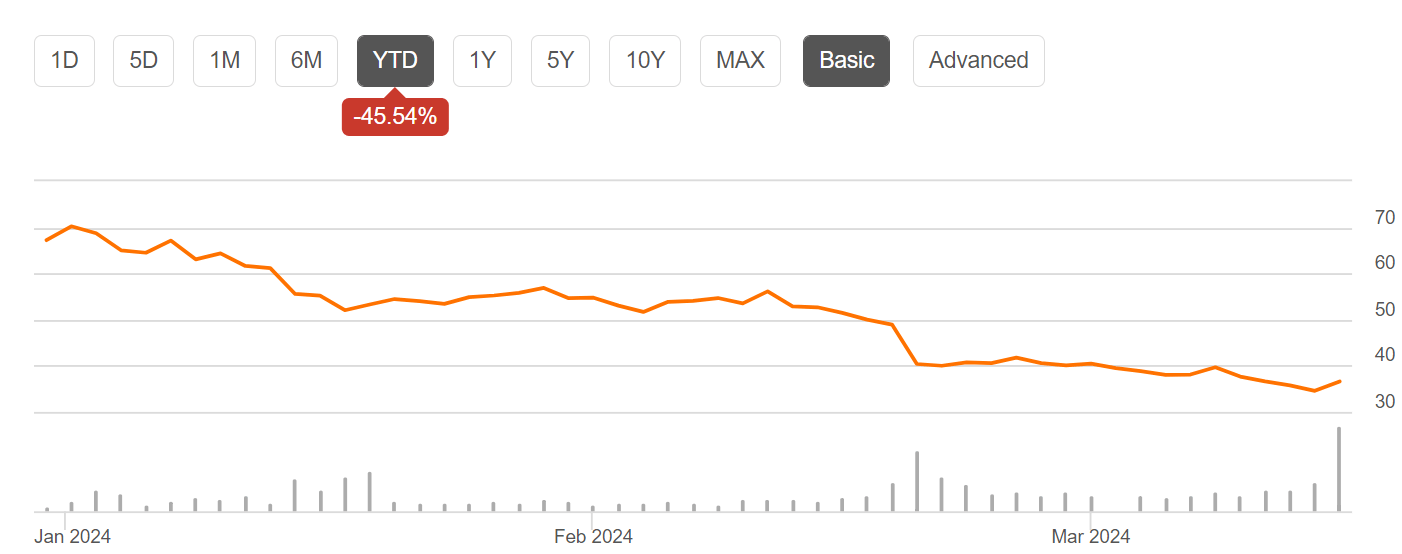

Unsurprisingly, Medifast's stock price has cratered massively. YTD the MED ticker has plummeted almost 50%:

Seeking Alpha

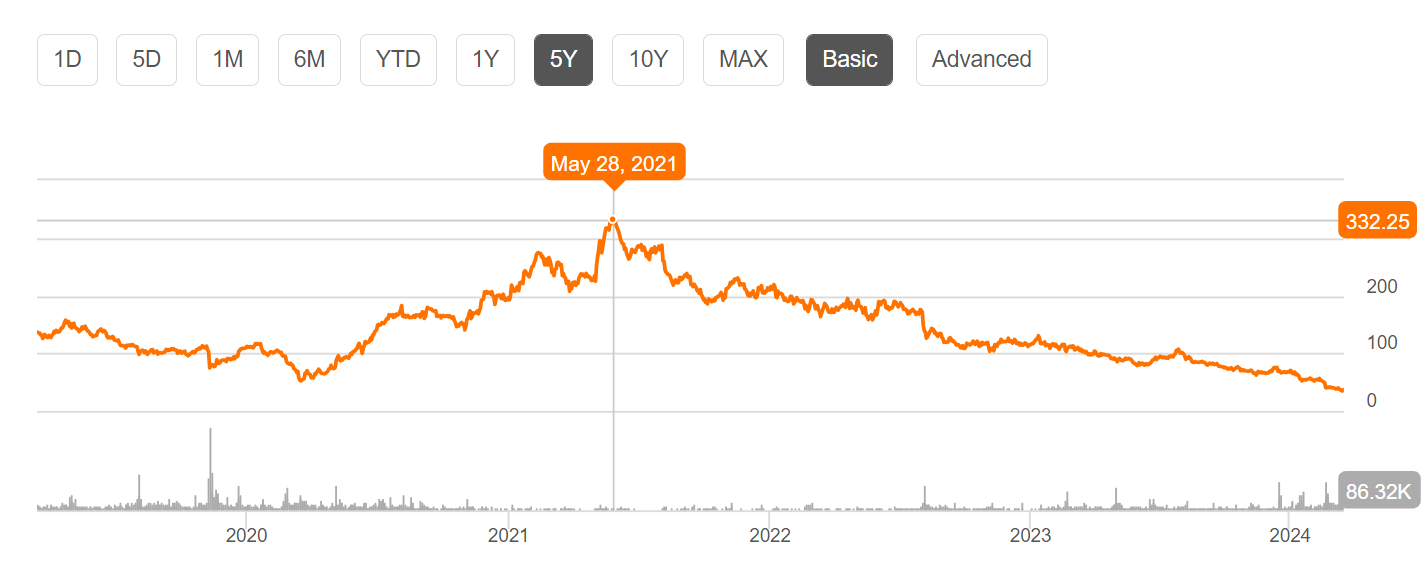

Furthermore, the stock reached an all time high of approximately $330 in May of 2021, and currently sits at a share price of about $35 in March of 2024 - a crash of roughly 90%:

Seeking Alpha

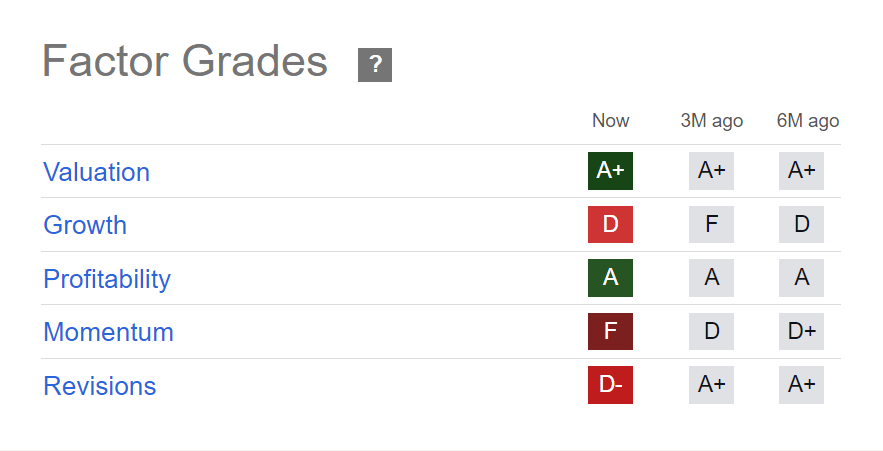

Medifast's stock, by almost all measures, is dirt cheap. This is immediately apparent when skimming over the MED Seeking Alpha page and noticing the A+ grade in the valuation category:

Seeking Alpha

Despite the horrific growth profile, investors should not hesitate to also take note of the impressive profitability grade, as this will prove extremely important in our valuation of the company's shares.

Let's dig a little deeper and look at some traditional 'back of the napkin' valuation metrics:

| Non-GAAP P/E | 3.79 |

| P/S | 0.37 |

| P/B | 1.96 |

| P/CF | 2.67 |

From a cursory glance, this indeed seems like an unequivocally cheap investment. It is important, however, to analyze the qualitative situation and future expectation of any prospective investment and incorporate that into the valuation. Taking MED's forward metrics into consideration, the picture is not quite as rosy:

| Non-GAAP FWD P/E | 19.22 |

| FWD P/S | 0.57 |

To get a more detailed valuation, let's perform a 10 year discounted cash flow (DCF) analysis. This will allow us to make assumptions on the company's future cash flows over the next 10 years and discount them back to today using our required rate of return.

A salient thing to note in the case of Medifast is the resilience in profitability/cash flow despite the cratering revenue. As mentioned above, MED's annual revenue fell by approximately 30% from $1.6 billion in 2022 to $1.072 billion in 2023. Their free cash flow (FCF) generation remained strong, however, reporting $155 million in 2022 and $106 million in 2023; a margin of 9.7% and 9.9%, respectively. In this case, the FCF margin actually slightly increased despite the calamitous drop in revenue over the same period.

To provide ourselves with an inherent margin of safety in our DCF calculation, let's assume Medifast will not overcome its woes and extrapolate the financial performance of the last year to the next 10 years in the future. In other words, let's assume MED's FCF will sink 30% per year in tandem with its revenue over the next ten years. Let's also use a required rate of return of 20% per annum over the same period:

| Year | FY FCF (millions) | Discounted FCF (millions) |

2024 | $74.20 | $61.83 |

| 2025 | $51.94 | $36.07 |

| 2026 | $36.36 | $21.02 |

| 2027 | $25.45 | $12.29 |

| 2028 | $17.81 | $7.15 |

| 2029 | $12.47 | $4.17 |

| 2030 | $8.73 | $2.44 |

| 2031 | $6.11 | $1.42 |

| 2032 | $4.28 | $0.83 |

| 2033 | $3.00 | $0.48 |

| Sum = $151.54 |

Now, when we add the net cash position of $150 million to the sum of our discounted cash flows, apply a reasonable FCF multiple of 8x, and divide the result by shares outstanding of 10.9 million, we get an intrinsic value of $27.66.

Theoretically, this means that if the business's FCF retracts by 30% per annum over the next ten years, and we can sell our shares for an 8x FCF multiple at the end of that period; if we desire a 20% annual return on our investment, the most we would pay for a single share of the company today is $27.66 (this also assumes that shares outstanding remain constant).

There can be no doubt that Medifast is facing an urgent existential threat from the rise of GLP-1 medications. With rapidly decreasing revenues and a dramatically uncertain future, one would expect an investment in this company to be hopeless. However, as was illustrated above, even in a shrinking company there is value to be extracted given the right price. The decision to purchase shares in a company such as this depends largely (if not entirely) on the investor-in-question's philosophy.

On the one hand, Medifast is a company that is facing extreme pressures from disruptive market forces, causing revenues to collapse and investors to flee. In a highly concentrated portfolio built around a select few positions, it would perhaps be wise not to swing on this particular pitch - unless there is high immunity to market volatility and unwavering conviction on the prospects of the company.

Conversely, in a value-conscious and diversified portfolio, buying shares of MED could offer a speculative opportunity to pick up a soggy cigar-butt and add it to a wide collection of similarly cheap opportunities. Unless cash flows dry up completely, the company's shares might be trading at a low enough price to achieve an adequate return on capital despite deteriorating fundamentals.

In light of this, it is unreasonable to give this investment opportunity a definitive 'Buy' or 'Sell' rating; I rate this as a 'Hold'.