Intuitive Surgical's flagship da Vinci system

3alexd/E+ via Getty Images

Intuitive Surgical's flagship da Vinci system 3alexd/E+ via Getty Images

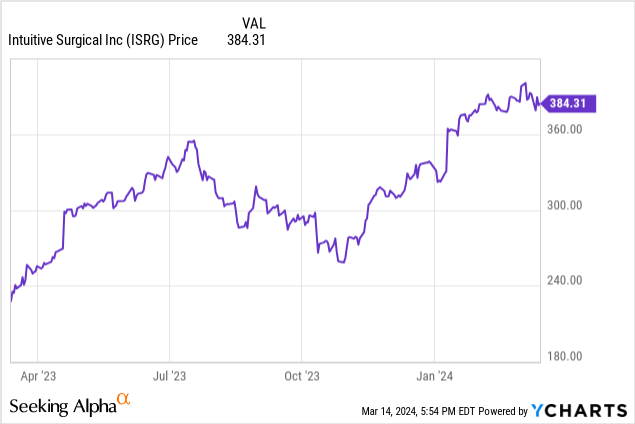

Intuitive Surgical, Inc. (NASDAQ:ISRG) has been on a tear over the last 12 months, up 61% since March last year. Revenues rebounded in 2023 to $7.1bn with 14% YoY growth, driven by a 21% increase in procedure volume of their flagship da Vinci system. The company is also in an excellent financial position with $5.2bn in cash and zero debt. However, with a P/E of 78.8 and an EV/EBITDA of 62.4 it may be looking expensive, and there are a few warning signs that may not justify the high price-tag. I believe Intuitive Surgical is a hold at current prices, but I will be looking to buy if there is a pullback.

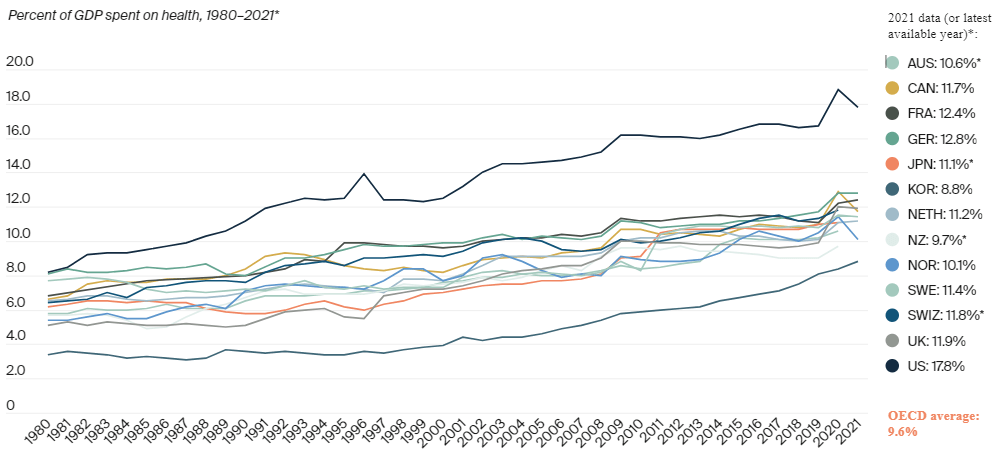

Healthcare, just like everything else, is being revolutionised by technology. Transformations in healthcare through mass automation, standardization and digitization of processes will increase efficiencies and reduce costs on a large scale, and economies are increasingly spending more worldwide. The US is the global leader in healthcare spending, with 17.8% of GDP spent in 2021, and every other major economy is following trend.

The Commonwealth Fund - % of GDP on Healthcare

With the increased spending comes great opportunities for businesses to capitalise, and Intuitive Surgical, Inc. is one at the forefront of evolution. Their da Vinci system is the pioneer of robotic-assisted surgery, a fully unified ecosystem with surgical systems, learning simulations and data intelligence all in one package. The da Vinci system was the first of its kind, and Intuitive Surgical have been on top ever since it was released. They provide hospitals in over 70 countries with surgical equipment and command a 80% market share worldwide.

In 2012 there was an estimated 200,000 surgeries performed with the da Vinci system, in 2023 there was 2,286,000, representing a CAGR of 22.5%, and this trend is only going to continue as more types of surgeries are approved for robotics, which allow for fewer complications, faster recovery times and less scarring.

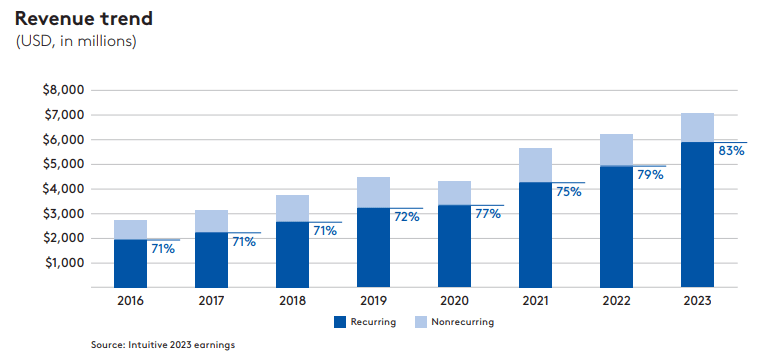

What makes Intuitive Surgical such an attractive investment is the nature of the revenue. When a hospital buys a da Vinci system they also buy into the unified ecosystem that comes with it. There is the built in learning platform called Intuitive Learning, 24/7 maintenance and technical support, and My Intuitive software allowing access to data and AI analytics of every surgery ever performed with a da Vinci. There is also lots of single use and surgery specific instruments and accessories, all of which you need to pay for.

It is estimated services agreements cost between $80k - $190k per year and each individual surgery costs $600 - $3,500. As more systems are placed around the world, recurring revenues increase, with 83% of total revenues recurring in nature in 2023.

Taken from Intuitive Surgical's 2023 Annual Report

Revenue growth has averaged 11.5% since 2014 and this was on a steady upward trajectory of increasing growth before COVID lockdowns delayed all non-essential surgical operations. This growth is only going to continue well into the future, with robot assisted surgery predicted to grow at a CAGR of 9.5% to 2030, led by procedures such as joint replacements and neurosurgeries.

Amazingly, Intuitive Surgical has zero long-term debt obligations, meaning there is no significant interest payments, a particularly valuable quality in this high interest rate environment. They have also had exceptionally stable margins over the last 10 years, with gross profit margins between 66% - 70% every year, and net income always hovering around 25% of revenues year in year out. These stable margins are a sign of a competent management who are reserved and calculated with spending, allowing great cash conversion and we saw this with a free cash inflow of $1.6bn in 2023. As stated, they now have $5.22bn in cash, so there is no chance of bankruptcy any time soon.

With such high levels of cash, it is important Intuitive Surgical puts some of this money to good use, and thankfully this seems to be the case. Their newest da Vinci system, the da Vinci 5, has just received FDA clearance in the US. This new generation system has been 10 years in the making, and has more than 150 enhancements on the current da Vinci Xi, including improved accuracy, a new 3D display and first-of-its-kind force-sensing technology. This is an important next step in their journey, as more and more companies try to break into the market, Intuitive Surgical need to show why they are the top dog. I will be keeping a close eye on the first peer reviewed articles on the new system, however, with access to the largest pool of data on robotic-assisted surgery and past triumphs in releasing new generations, it is safe to say Intuitive Surgical have an edge in development.

Intuitive Surgical are also using their bulky cash piles to widen their reach on the healthcare technology industry with Intuitive Ventures. This is the groups own venture capital fund with AUM of $250m, supporting independent initiatives in the direct and adjacent fields of minimally invasive care, and has 9 startups in the portfolio. Neocis, leaders in robotic-assisted dentistry and Kela Health, an advanced surgical AI platform are some notable holdings in the portfolio. This is a great step in the right direction, expanding and diversifying their global reach in the healthcare sector.

It is clear Intuitive Surgical is a great company, with a near monopoly on a rapidly expanding growth market and excellent financial management. However, this doesn't come without a price. With a P/E of 78.8 and an EV/EBITDA of 62.4, it is extremely expensive when compared to others in the robotic-assisted surgery space. Some notable players with systems already in the market are Stryker (SYK), Medtronic (MDT), Boston Scientific Corporation (BSX) and Abbott Laboratories (ABT).

| Company | ISRG | SYK | MDT | BSX | ABT |

| P/E | 78.8 | 42.7 | 25.3 | 61.9 | 35.6 |

| EV/EBITDA | 62.4 | 27.5 | 14.8 | 29.4 | 20.0 |

Valuations taken from SA Valuations page.

Importantly, Intuitive Surgical only sell robotic-assisted surgery systems and the products that go with it, whereas the others have much wider product catalogues, so this valuation could be justified by the fact they currently sell more robotic surgery systems than all of the other four combined. However, I think this puts them at a much higher risk, especially when considering how the market dynamic is currently changing.

The biggest risk to the high valuation is market share. Intuitive Surgical were the first on the scene when the da Vinci system was released in 2000, and have been on top ever since. However, most of their original patents have expired in the last few years, and this could mean some trouble for the competitive advantage they have long enjoyed. When the great investor Warren Buffett talks about a competitive advantage, the key word he uses is durable, so how durable is Intuitive Surgical's?

One of the key emerging players to challenge the da Vinci system is Medtronic (MDT). Their Hugo RAS has received regulatory approval in Europe, Canada and Asia, and is undergoing clinical trials in America. When looking into the peer reviewed articles comparing the Hugo RAS with the da Vinci system there were some very interesting results. Firstly, in every comparison there was no significant differences in functionality between the two systems, see here, here and here. A leading robotic surgeon, Alex Mottrie, said the Hugo RAS may more suitable than the da Vinci for general surgery due to the four independent arms, and the open console is a big plus as it allows other surgical staff in the room see what the surgeon sees, allowing conversations and improved procedure.

One preconceived counter to the implementation of the Hugo RAS is that most surgeons trained in robotics have trained primarily on the da Vinci, meaning it would be impractical to be retrained on the Hugo RAS. However, it seems surgeons who are proficient on the da Vinci had little problem switching to the Hugo RAS - think of it like switching from a PlayStation controller to an Xbox one, a little getting used to but it's the same process in the end. Mottrie believes, in the future, large surgical centres will have access to multiple different machines and it will ultimately come down to the procedure type what each surgeon prefers.

The fact the Hugo RAS performs just as well as the da Vinci is significant, as its reported the Hugo RAS is 25% cheaper than the da Vinci. One of the biggest gripes of robotic-assisted surgery is justifying the price and cost effectiveness, and this is the reason many places outside of the US have been slow to adopt the technology. A cheaper system that performs the same will take future market share from Intuitive Surgical and Medtronic already have strong connections across Europe. Medtronic aren't the only competitors either, and more cost effective systems on the market means less on Intuitive Surgical's top line. This threat to market share is the main reason I can't justify such a high valuation right now.

Of course, Intuitive Surgical aren't going to just let competitors take all their market share. The next-gen system, da Vinci X, is their answer to all the competitors, and it will be very interesting to see how this performs. If the system is truly revolutionary and is worlds ahead of the current gen, this would cement them as the best robotic surgical system maker and I could fully justify the high valuation, however this just isn't something we will know for at least a year.

One thing we know is the impact the rollout of the new system will have on the companies financials. CFO Jamie Samath said the operating margins are likely to come under pressure in 2024 due to the upcoming launch of da Vinci 5. On top of this, due to new competition, Intuitive Surgical's R&D costs have been steadily increasing since 2015, going from 8.3% of revenues to 14.0% last year. This is a trend I see continuing into the future, as they need to ensure they still have the best products on the market. This is the second reason I'm weary of the high valuation, because if operating margins take a larger hit than anticipated, the stock would come down.

Overall, Intuitive Surgical is an excellent and revolutionary company, with an amazing product that will benefit millions of people. They are the market leaders in a rapidly growing market, and have been there for a very long time. Unfortunately, the market has already priced this in and it looks too expensive to me. The next couple years is critical to determine if they keep their position as the best on the market, and to me it seems the stock already has all the upside priced in, without any of the potential risks considered. However, if there is a significant pullback in the general market, this would be one of the first I add to my portfolio.