DanielBendjy

DanielBendjy

From my perspective, while Mondelez (NASDAQ:MDLZ) is a business that dominates the biscuit category and looks like it is going to take Mars's spot as the number one player in the chocolate category, the DCF analysis estimates an annual return of 11.5% over the next five years, making MDLZ a hold as I aim for 15% annual returns. This stock could still be of potential for a defensive play in a diversified portfolio or for an investor happy with an 11.5% annual return. Growth in emerging markets, especially Latin America is a positive for MDLZ, showing solid double-digit revenue growth in the previous few years. Debt levels are something for investors to monitor as the debt is currently about six times its annual free cash flow.

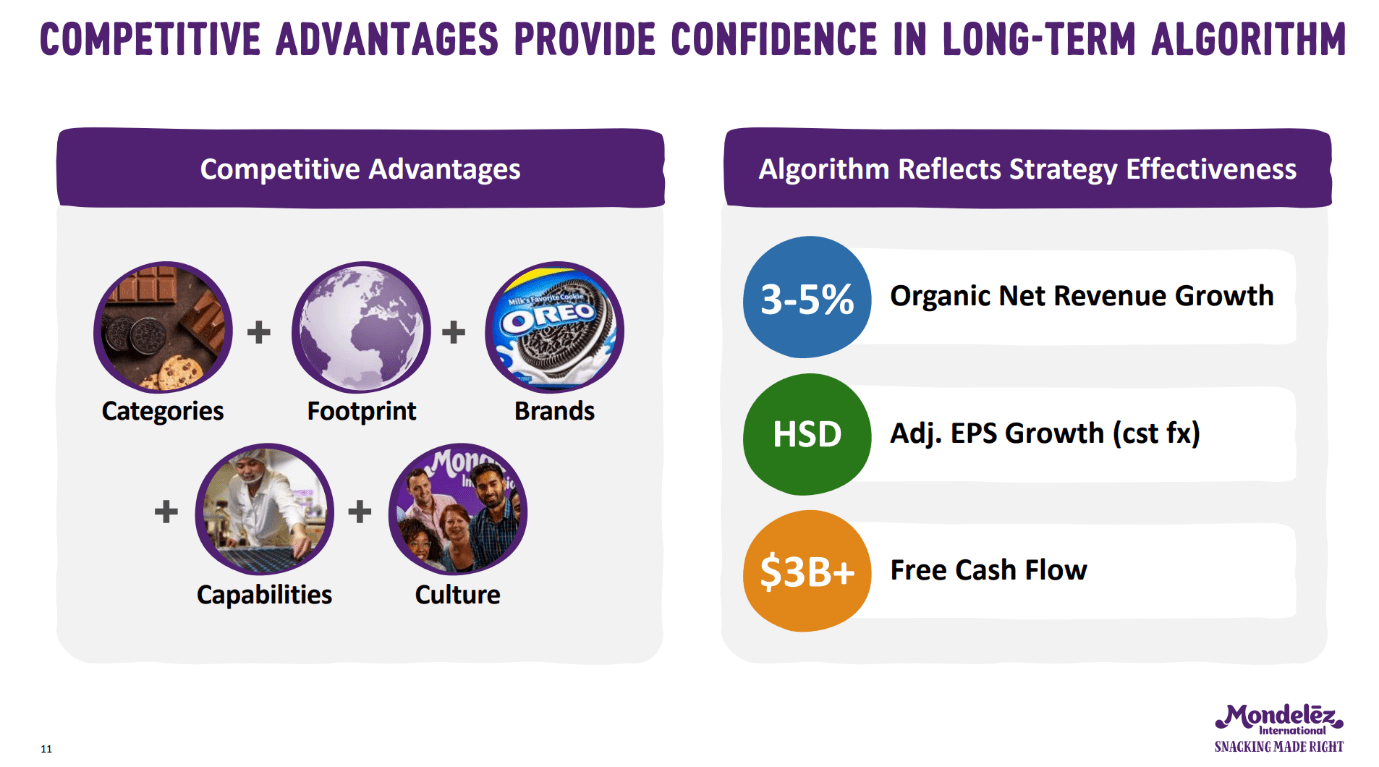

Mondelez is one the largest players in the snack food and confectionery space, it owns well-known brands such as Oreo, Cadbury and Toblerone. The business itself is a defensive slow grower with stable revenues which it makes through the sale of its snack and drink products. The company is well diversified geographically with a global presence in over 150 countries. I see their competition as other food global conglomerates like Nestlé, Hershey and Mars in which Mondelez is currently gaining market share.

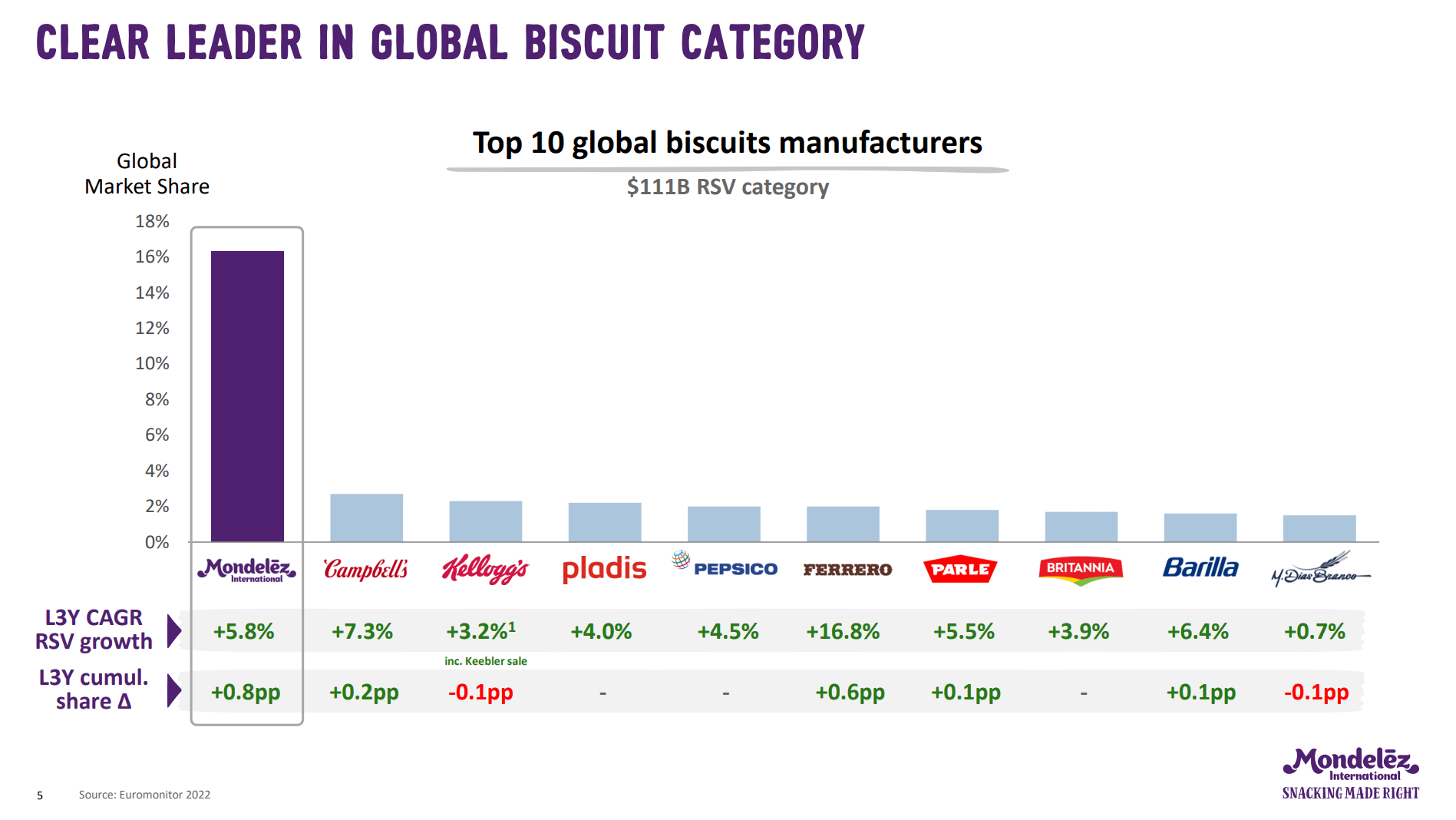

Mondelez is currently a global leader in many of its core categories in particular the biscuits and chocolates segments. MDLZ currently are a clear cutout leader in biscuits capturing a 16% market share, while the nearest competitor has about 3% market share. The gap continues to widen where in 2023 Mondelez gained a further 0.8% market share in the biscuit category driven by strong brands such as Oreo and Ritz.

Mondelez 2023 Investor Presentation

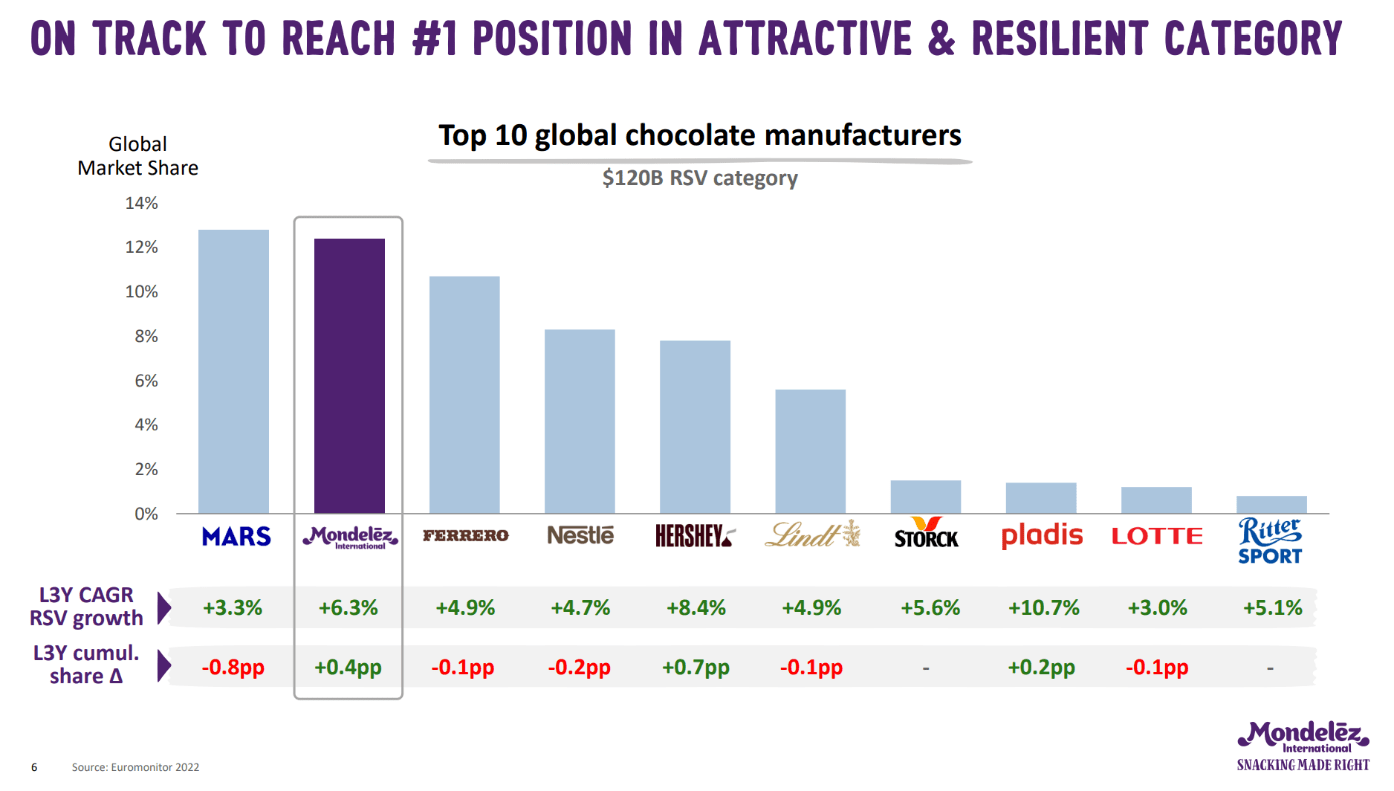

In the chocolate category, Mondelez is in second place globally with around 12% market share, only behind Mars with about 13% market share. However, I believe Mondelez will close the gap between themselves and Mars over the coming years as Mondelez is gaining market share against Mars. In 2023, Mondelez gained 0.4% in market share, while Mars lost 0.8% market share in the $120 billion dollar chocolate category.

Mondelez 2023 Investor Presentation

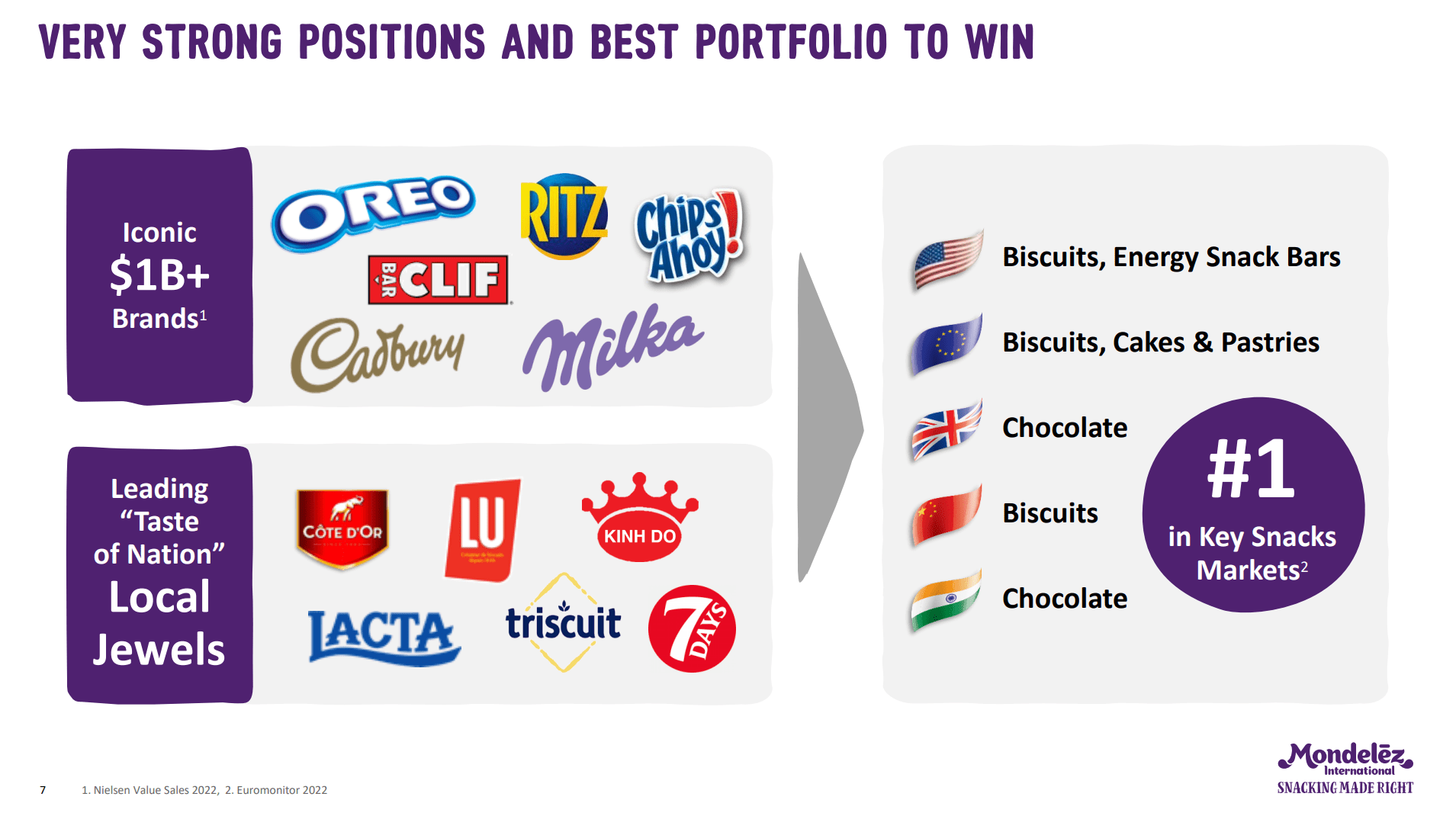

This is evidence that points to the idea that Mondelez’s brands are performing well. As we can see below, they have six different brands that alone are worth more than $1 billion each while leading in key snack markets across various geographic regions.

Mondelez 2023 Investor Presentation

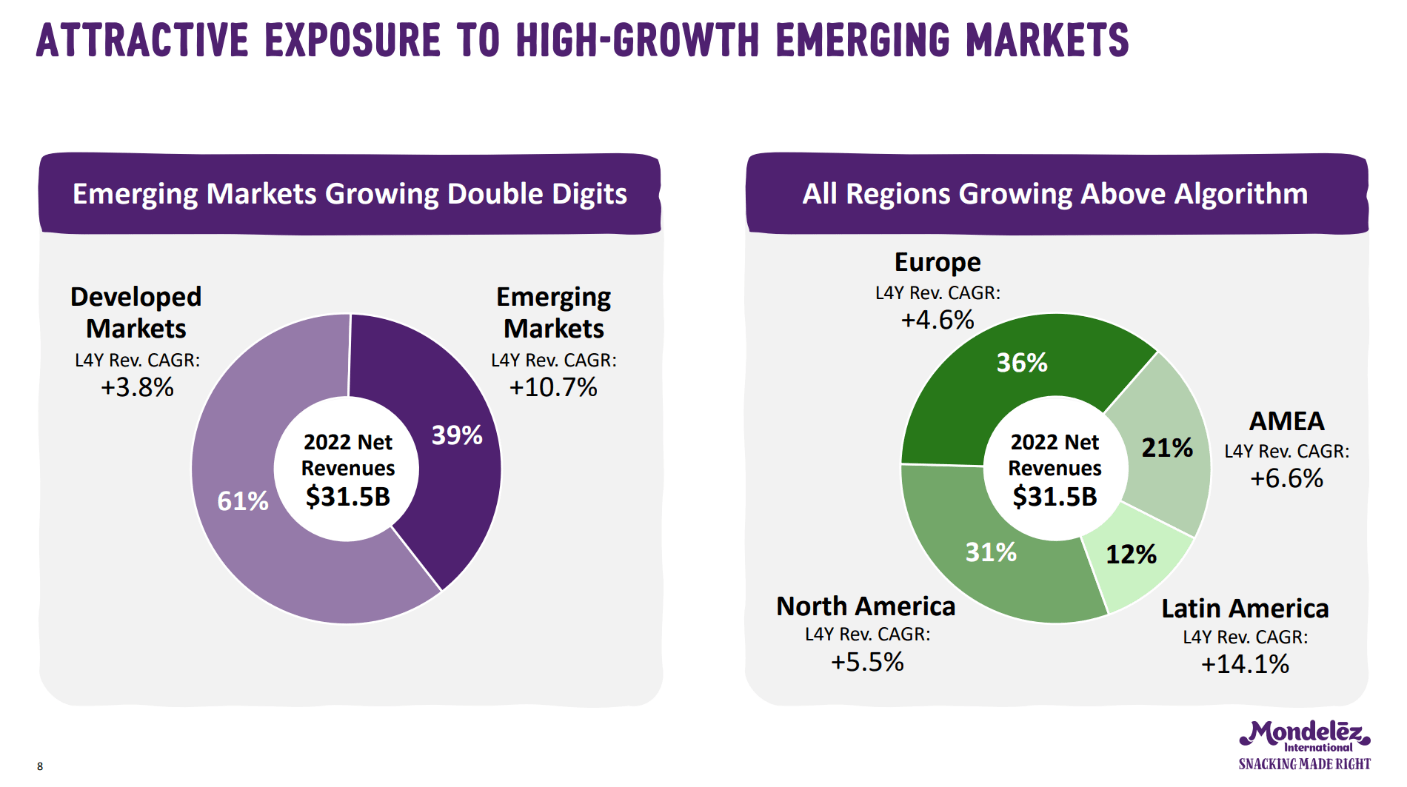

MDLZ is definitely a company that is well diversified not only in terms of its brands but also within the geographic regions in which their brands are offered. This helps protect the company from geographic risk and geopolitical risk. As we can see, the largest two regions for MDLZ are Europe and North America with 36% and 31% of the revenue coming from these regions, respectively. We can also notice Latin America is only 12% of the total revenue, however it is the fastest growing region for Mondelez where last four years revenue CAGR for Latin America was 14.1%. Moving forward I expect emerging markets to drive most of the revenue growth for MDLZ where over the last four years emerging markets collectively grew at a CAGR of 10.7%. Over time I also think emerging markets will become a larger part of the overall business.

Mondelez 2023 Investor Presentation

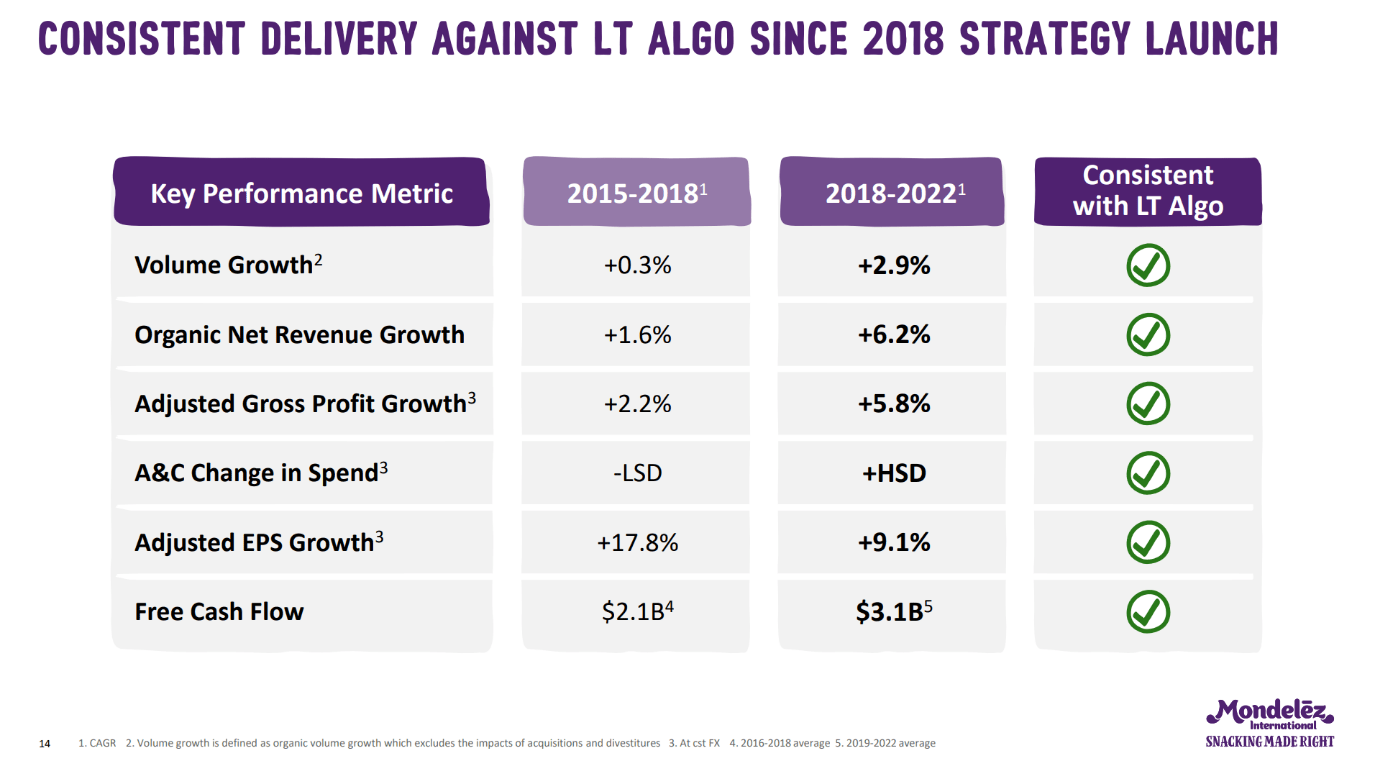

MDLZ made good progress on its overall long-term goals and have made a strong turnaround in their business since 2018. As a part of this we have seen volumes increase at a considerably higher rate from 0.3% to 2.9%. This has helped drive organic revenue growth improvement where MDLZ have improved growth in this area from 1.6% to 6.2%, a vast improvement. This has also led to higher free cash flow which is now above $3 billion which is then used by the management team to increase the dividend, repurchase shares and reinvest back into the business for future growth. Compared to 2018, for me it is undeniable that Mondelez have improved their focus which has led to better overall business metrics.

Mondelez 2023 Investor Presentation

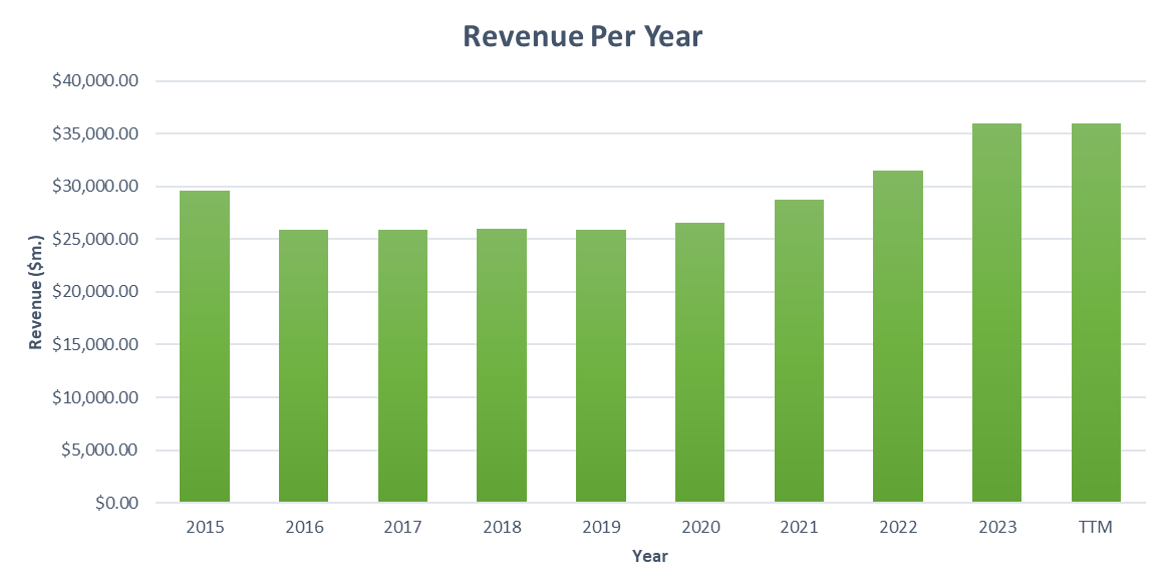

From 2018 to 2023 MDLZ has seen slow but steady revenue performance with the pace of revenue growth picking up in the recent couple of years, largely due to the growth seen in Latin America and as a result of the companies more narrow focus on the core categories of biscuits and chocolate. We have seen revenue increase from $25,868.00 million in 2018 to $36,016.00 million in the last 12 months, which is a CAGR of about 7%.

Created by Author, Data From Tikr Terminal

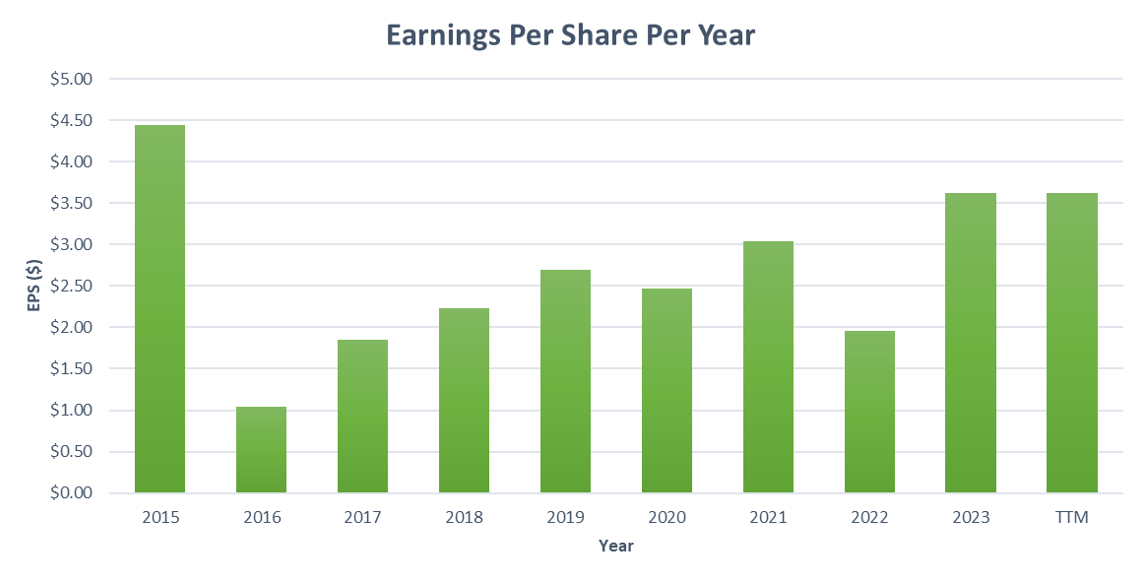

The EPS also improved with revenue moving from $2.23 in 2018 to $3.62 in 2023, a CAGR of 10%. The fact that EPS grew faster than revenue is a sign that the business improved net income margins. EPS also grew faster due to share buybacks.

Created by Author, Data From Tikr Terminal

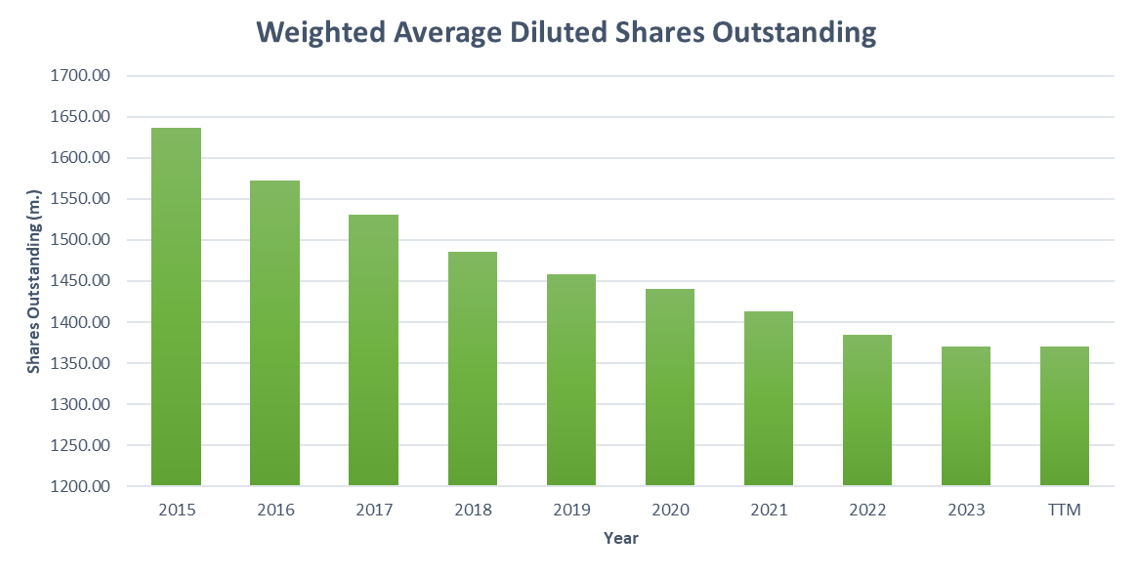

As we can see below, the company consistently repurchased their shares over the last five years, decreasing the share count from 1486.00 million in 2018 to 1370.00 in 2023, a decrease of 1.5% per year. This shows the company’s commitment to delivering free cash flow back to shareholders.

Created by Author, Data From Tikr Terminal

The management team expects that in the long term, the company will maintain a consistent annual free cash flow of at least $3 billion per year. Given the momentum the business has within its core segments such as biscuits and chocolate as well as the growth expected in emerging markets like Latin America, I believe the company can achieve this conservative target. In the short term, even with potential recession risk as a result of a weakening macro environment, I see the stock as defensive, protected by a stable revenue model. Even in a recession, consumers will still purchase Mondelez brands.

Mondelez 2023 Investor Presentation

As for liquidity, the latest quarterly report shows cash and cash equivalents of $1,810.00 million. The company's total debt is $19,945.00 million, which seems quite high given that the company expects to produce at least $3 billion in free cash flow over the coming years. This means that in a conservative scenario, it may take six years' worth of free cash flow to repay the rest of the debt. I think the debt level is something to watch, though since the business is defensive, I see the debt as manageable and a common theme among large food conglomerates.

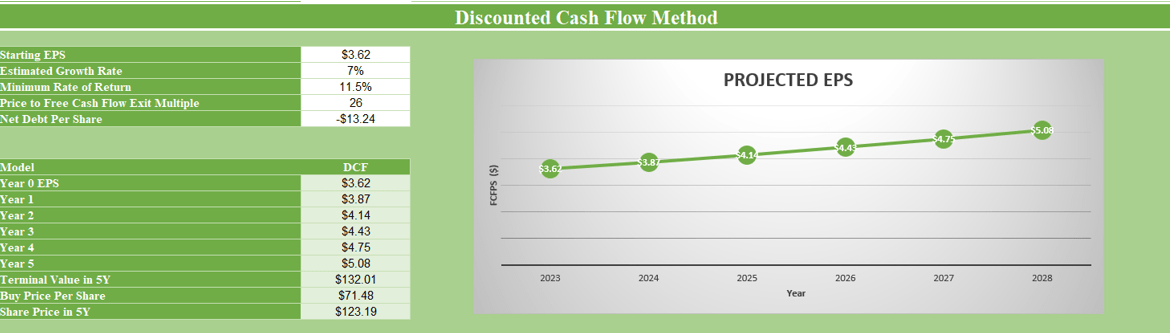

As of Q4, MDLZ's current EPS is $3.62. Given the strong brands, the opportunity to gain further market share and the growth expected in Latin America, I anticipate a conservative annual growth rate of 7% for MDLZ's EPS over the next five years. Taking this growth into account, the projected EPS for MDLZ by Q4 2028 would be $5.08.

Using an exit multiple of 26, which is based on MDLZ's average price to earnings ratio over the past decade, the estimated price target for the stock in five years would be $123.19. Therefore, if you invest in MDLZ at its current share price of $70.75, the expected CAGR would be 11.5% over the next five years, based on these calculations.

Created by Author, Data From Tikr Terminal

Therefore, for me I see Mondelez stock as a hold since I aim for a 15% or higher annual return. Though I do see Mondelez as undervalued compared to historical valuation where it currently trades at a PE of 19 as compared to the 10-year historical valuation of 26. Hence, dividend investors or value investors who don’t mind an 11.5% per year return may like this stock.

To wrap up, Mondelez has a plethora of strong billion-dollar brands that place it amongst global leaders within the snack and confectionery industry. MDLZ dominates the biscuit category and by far has the largest market share at about 16%. They are also ranked second in the world within the chocolate category, only behind Mars though it seems like MDLZ will overtake Mars as the number one player in terms of market share in the coming years. The business is geographically and politically diversified regarding the regions in which they operate where they also have exposure to emerging markets which I see being the key growth driver for the company. The business’s financials are stable and would likely suit more defensive-styled investors, nonetheless I do think investors should keep a close eye on the debt levels as the debt load is around about 6 years worth of free cash flow. Overall, I see Mondelez as a hold, as my DCF analysis anticipates an annual return of 11.5% over the next five years where I personally aim for a 15% return. However, for investors looking for a stable defensive play, offering double-digit returns, this could be your play.