ArtistGNDphotography

ArtistGNDphotography

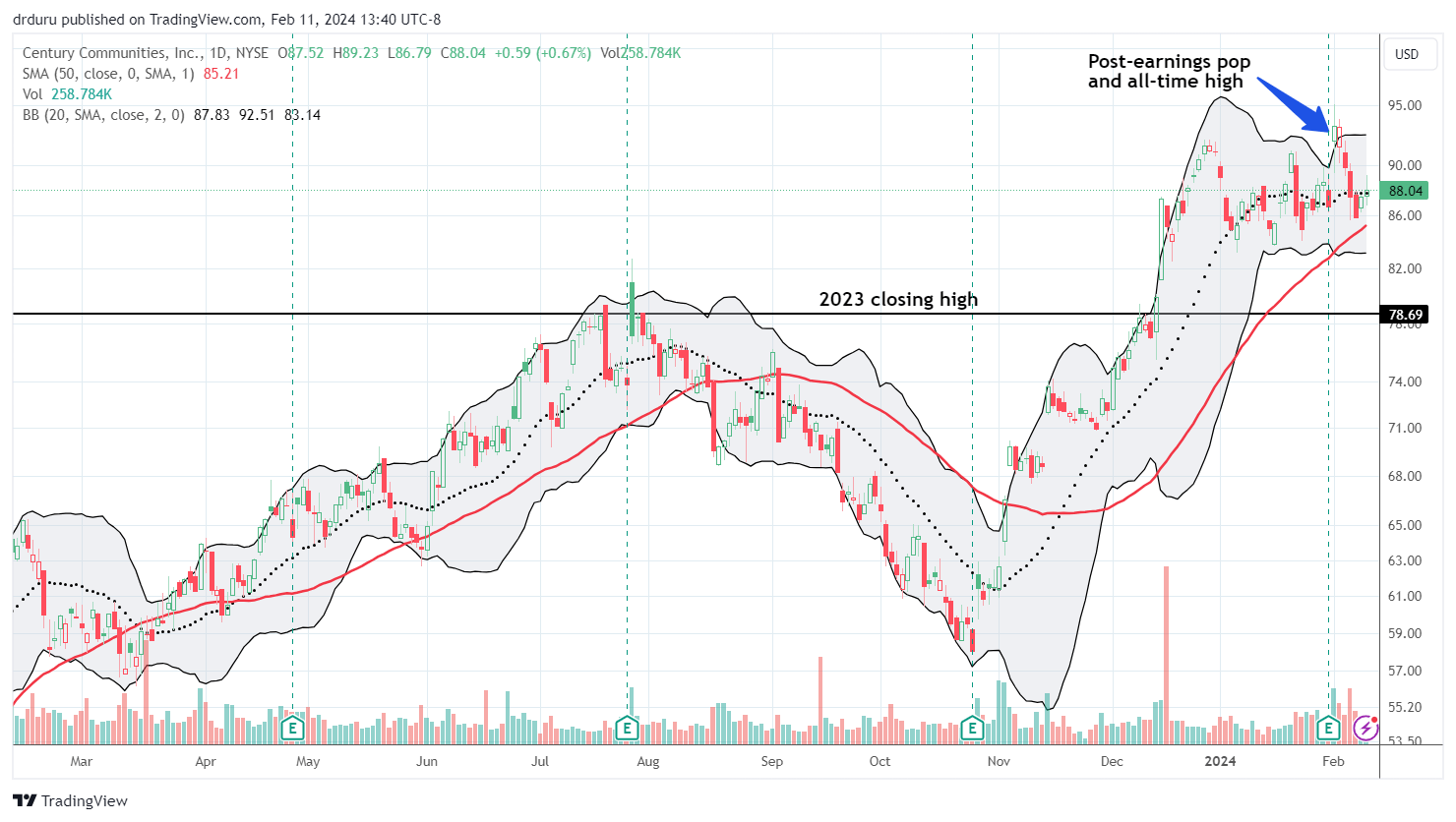

Although I recently declared an end to the seasonal trade on builders, buying opportunities in the stocks of home builders should still appear from time to time as the year unfolds. Century Communities, Inc. (NYSE:CCS) offered up one of those opportunities last week. The home builder gained 7.6% on February 1, after reporting earnings. Sellers proceeded to wipe out those gains over the following four trading days. The selling ended right above a technical support level at the 50-day moving average (the red line in the chart below), creating what looks like the bottom of a developing trading range. CCS's earnings seem to support a case for this bottom more or less holding in the short term. Eventually, the stock should rebound to the top of the trading range and perhaps even breakout by the next seasonal trade on home builders.

CCS pulled back sharply from a post-earnings pop and all-time high. (TradingView.com)

CCS has an attractive valuation with a price/book ratio of 1.17. The 1.0 level is the conventional recession valuation for builders. The current price/book ratio is around the middle of CCS's 10-year range; it hit 2.0 in 2021. The forward P/E of 8.8 further gives room for downside operational risks. The price/sales ratio is also barely above 1.0.

Even better, CCS earned a strong buy quant rating after reporting earnings. The quant rating pegged CCS mainly as a hold since September 2022. While I am surprised by the D+ valuation grade, the A EPS revision grade and the A- momentum grade are encouraging. CCS also carries a #1 quant ranking in its industry. Since Wall Street rates CCS as a hold, the stock could enjoy an upside from upgrades in the near future.

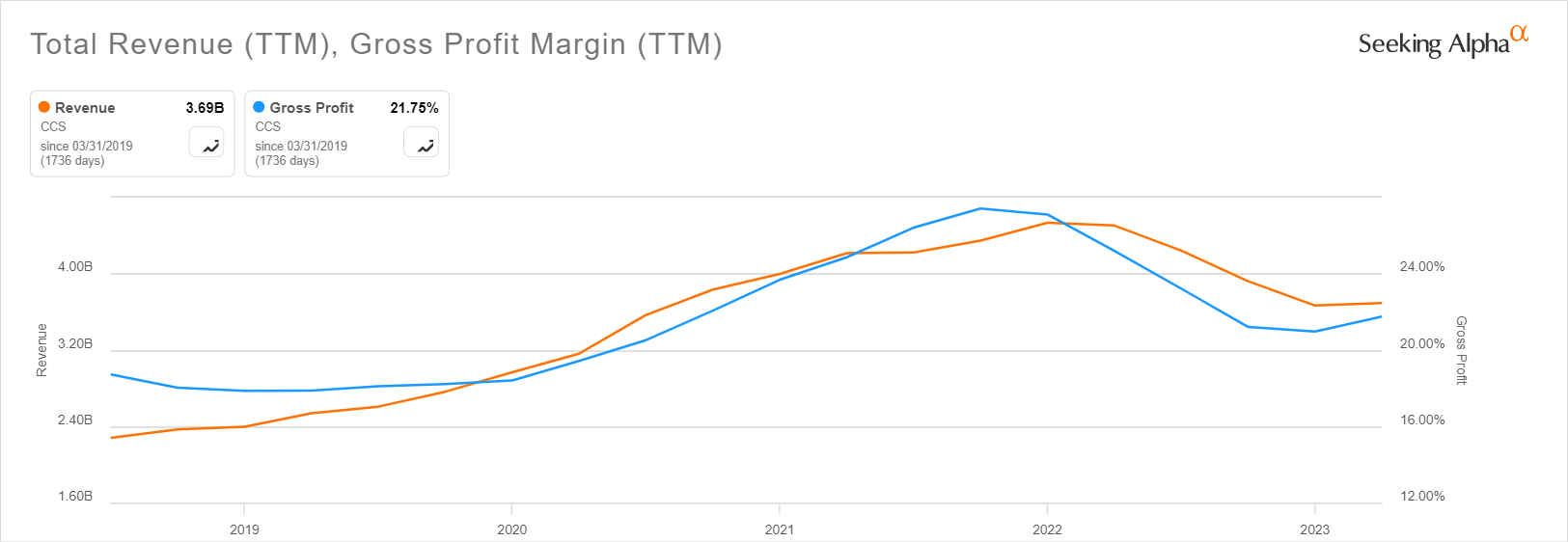

The hold rating from Wall Street is consistent with the rating model I proposed last year. Based on revenue TTM (trailing twelve months) CCS is a "revenue peaker" and the gross margin TTM is below 25%. Both characterizations put CCS in the bucket where analysts are prone to hand out a hold rating. While the gross margin will not likely break the threshold in the coming year, CCS should become a "revenue grower."

CCS is a "revenue peaker" and under the 25% margin threshold. Thus, analysts are more likely to rate the builder as a Hold. (SeekingAlpha.com)

In the transcript of the earnings conference call, Century Communities guided to full-year 2024 deliveries from 10,000 to 11,000 homes, generating $3.8B to $4.2B of revenue. This guidance represents 2.7% to 13.5% revenue growth from the $3.7B in 2023. This growth is not all organic given the recent acquisition of Landmark Homes of Tennessee, Inc., which will expand Century's footprint in Greater Nashville.

Century Communities did not guide on margins. Instead, management said, "we're obviously thinking that as incentives are getting pulled back, we think there's some stability to that gross margin line. And heading into the year, I don't think you're going to see - we're not anticipating it falling like it did from Q4 to Q3." So assuming CCS holds the line at 2023's 21.2% gross margin, the company will increase earnings by around 2.7% to 13.5% as well as revenue. This is a welcome change from the nearly 50% drop in net income and diluted EPS in 2023 from 2022 ($259.2M and $8.05 vs. $525.1M and $15.92 respectively).

Century Communities increased incentives on closed homes from 600 basis points in Q3 to 800 basis points in Q4, mostly in the form of mortgage rate buydowns. These incentives are key for entry-level buyers looking to reduce monthly payments. Falling mortgage rates have allowed Century Communities to reduce these incentives in December and January. Thus, the company expects to hold the line on Q4 gross margins, which came in at 21.6% (and increased from 17.6% in Q4 2022).

The delivery and revenue range is of course very wide, so buying CCS at current levels requires a belief that the company can get to the upper end of its guidance. Demand and supply trends hold out that possibility.

In Q4, deliveries hit a quarterly record with a 9% year-over-year gain. The resulting revenue of $1.2B was Century Communities' highest since Q4 of 2021. Deliveries increased for the third quarter in a row, with a 39% gain from Q3 to Q4. The company attributed the favorable trend to improved cycle times and a related increase in housing starts. Q4 contracts surged 86% year-over-year. Over the previous four years, net contracts averaged a 10% decline from Q3 to Q4, but in 2023 Century Communities benefited from a 9% sequential increase. Last month experienced a 30% year-over-year surge in sales.

On the supply side, the company is ready for increased demand. Century Communities closed out 2023 with 251 communities, the second-highest number in its history. Each region grew community count. However, Century Communities is particularly focused on more affordable markets with strong employment and population profiles (a common refrain from home builders). Accordingly, Century increased its share of lots in Texas and the Southeast from 43% to 50% year-over-year. More affordable markets are almost 75% of the company's owned and controlled lot and land supply.

Century Communities also expects to take share from capital-constrained private builders. This competition is a familiar theme in recessions, but even more important with high interest rates reducing the ability of some builders to develop lots and build homes. The company's Century Complete business acquires finished lots, usually just in time, with a focus on secondary markets with less competition from public home builders (implying that public home builders have the capital to compete better than private builders).

Competition will likely help generate more merger and acquisition (M&A) activity. The company explained, "part of it is, when you look at the private builders, the capital constraints are starting to become impactful on them, as well as you just look at it in many cases, the people who founded the business are starting to age a bit, and they'd like to be able to liquidate their holdings."

The impact of M&A is instructive. When Sekisui House took M.D.C. Holdings, Inc. (MDC) from a $3.9B to a $4.7B company in an all-cash acquisition deal, it set a valuation target on these mid-sized builders. MDC trades at 1.4 price/book and a forward P/E of 12.4. This pricing suggests CCS has upside room on its valuation.

The reversal of post-earnings gains provides a low-risk entry point to buy Century Communities relative to other home builders. While a trading range may be underway, I am targeting a breakout by the time of the next period of seasonal strength for the home builders. In the meantime, I like adding shares on a deeper pullback to around the $80 level where CCS broke out above the 2023 highs.