junak

junak

Some of you devoted tech investors and traders might have been surprised by how some great stocks have fallen seemingly through the floor. I believe that part of this is part of a sideways correction process where the high-flyers are giving up gains, but those funds are being distributed elsewhere. Corrections can happen in a downward swoop or stocks can correct in a sideways motion over time.

The indexes haven't shown us a typical 3% to 7% or even 10% correction that happens more than once a year. Instead, we are witnessing a rolling correction where certain sectors have gotten a bit over-bought, meaning everyone who wanted to buy that fantastic shooting star already bought some shares. The funny thing, when everyone's a believer and the hype is at its zenith that is when the seeds of destruction are planted.

Destruction is too dramatic a word, no one in their right mind would criticize Nvidia (NVDA) right now. Though it did drop 100 points off its high on Friday. There is an investor's day this week so perhaps it goes to infinity and beyond this week (Toy Story reference).

Back to my point, a sideways correction is much preferred to a sell-off that drops every stock all at once. So along with this sideways correction or perhaps even the direct cause of it, several fantastic tech stocks that are in the target sector for the correction have provided an extra reason for them to be targeted.

These are names of several stocks that I am quite confident when they have proven that they have finished dropping will make both excellent trades and investments. I say that these names have "sandbagged" their guidance, meaning they deliberately pulled back from the most optimistic guidance out there to make it easier to beat on the next quarterly report. Sandbagging is a real thing, and as you read on I quote the venerable Investopedia for their definition and to show this isn't a neologism of mine.

According to Investopedia; Sandbagging is a strategy of lowering the expectations of a company or an individual's strengths and core competencies in order to produce relatively greater-than-anticipated results.

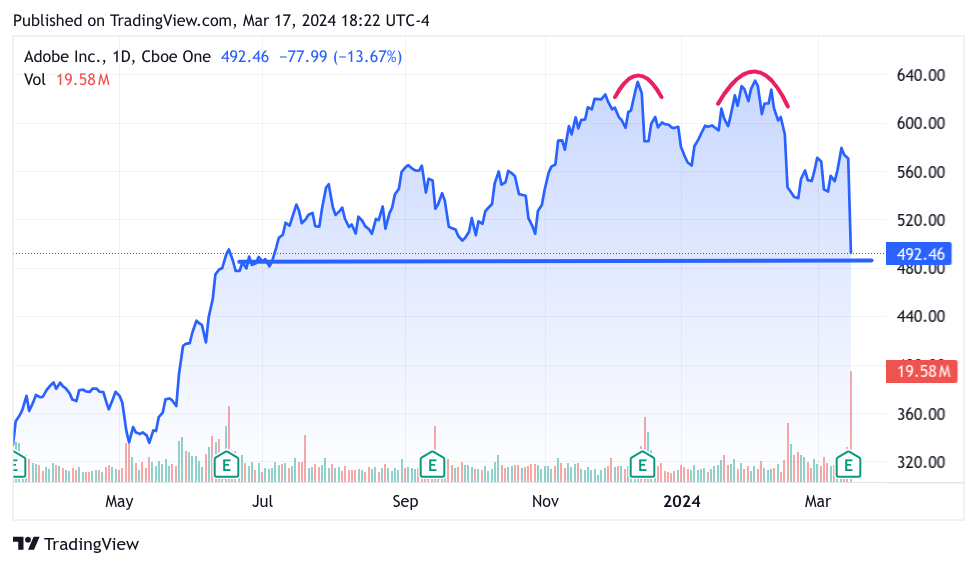

ADBE has challenges but dropping 23% might be overdone, that's right ADBE is down $145.79 from the all-time high of $638.25. I say it might be overdone because this is not a fundamental analysis. I think fundamental analysis as far as PE, GARP, and PEG ratios right now is not helpful. At least in this case where we are deciding where the absolute bottom will be. We must take into account human psychology as well. Also, part of the problem for us market participants is that the earnings beat expectations.

My approach is that I am simply surfacing the price action and comparing that to the narrative. This is a qualitative analysis instead of a quantitative one. Examining the price means charting the stock and looking for support levels. Traders are people and people can act irrationally, so again we could be dealing with even further selling before ADBE finds support. So this past Thursday after trading ADBE released their earnings.

Just a quick comment about how the current action is ruled by qualitative and not quantitative, just look at the headlines. The ones that are closest to the release are very positive about the earnings, but the guidance missed expectations. Then you see headlines criticizing the earnings as well. Then you see commentary that ADBE's AI strategy has missed the mark.

The last headline I see is calling into question the whole AI growth narrative writ large. This evolution in narrative probably follows market participants' real thought processes, after all, humans are still writing these articles, I am happy to note. Here is just a quick digest of the earnings

ADBE reported better-than-expected revenue in its latest quarter, and demand for products and services was boosted by generative artificial intelligence. ADBE posted net income of $620 million, or $1.36 a share, for the first quarter ended March 1r. Adjusted earnings were $4.48 a share, above analysts' estimates of $4.38 a share. Revenue climbed to $5.18 billion from $4.66 billion.

Analysts polled by FactSet expected $5.14 billion. The remaining performance obligations exiting the quarter were $17.58 billion. Chief Financial Officer Dan Durn said the quarterly results and record remaining performance obligation reflect strong customer adoption of Adobe's products and services.

For the current quarter, Adobe guided for revenue between $5.25 billion and $5.3 billion and adjusted earnings per share in the range of $4.35 and $4.40. Analysts polled by FactSet expected $5.3 billion in revenue and adjusted earnings per share of $4.38.

The upper range of the revenue guide hit the expectations exactly! Also look at the earnings, perfectly bracketing the estimate. The big disappointment was that they didn't raise guidance. On top of that ADBE authorized the buyback up to $25 billion in common stock after its board approved a new stock repurchase plan. That is a commanding show of confidence. Normally a buyback announcement of more than 10% of the market cap of a company would be cause for celebration but not today.

First, it is possible that ADBE had the misfortune of announcing earnings late when everyone was already piled into the Nasdaq-100 stocks, and this rolling correction started. Another reason is that people have just gotten inured to the AI hype and when ADBE didn't exceed the expected the stock got sold.

The big reason is that ADBE might be perceived as losing the AI game. The headlines said have started moving in that direction. There is SORA, which has been demoed that generates video from the written word.

There is Figma the software startup that ADBE failed to acquire that is a threat, and there are always tools being created to challenge ADBE. And you know what? Some day the great ADBE will fall, such is the vicissitudes of the free market, but that isn't happening today nor is it happening tomorrow. ADBE provides the essential tool - the Creative Cloud for creatives. Everyone is too invested, in training, and content to leave ADBE. Also, ADBE's generative AI strategy is rock solid, they have the intellectual property and copyright locked down, while these generative AI startups that are out there are acting like it's the Wild West.

Even if you were to start with a sora, I believe that will be great for generating ideas and storyboarding but then you want to bring it into the ADBE creative cloud and polish it up. This could help the creative world more than hurt it. Ok, so let's look at the chart and see what we got. I am going to start with the one month. I haven't looked at it yet because I wanted to share it with you all. Ouch, this was a nasty chart, I had to back to June of 2023 to find support. Also, we have a double top, so that will be difficult to overcome for new highs for a while.

TradingView

That support line is at 480 and if that is broken, we are talking 420ish for the next support level. That seems unimaginable to me, but stuff like this has happened. What could pressure the stock? Perhaps Figma going public, or Figma will license a Sora. The kryptonite from a narrative point of view is that a new competitor comes in and starts drawing in creatives, like Figma, which was drawing in a lot of users and generating revenue.

The key driver for Figma is not generative AI, but the ease of collaboration. ADBE while they were working on acquiring Figma adapted a lot of collaborative features. There are very smart people at Figma and I bet they are beavering away at getting generative AI going. There are plenty of others out there.

My conclusion is, that there isn't really a strong competitor out there, and that are out there really don't AI better, so there is a good chance 480 holds. AI competition, or the fact that ADBE doesn't have a strong AI strategy just is not evident. That said, if the bears do find an example of a superior AI, a more mature Sora, and show how to build useable video and stills that are copyright safe, then we could see ADBE at or below $420. If Figma, or I should say when, Figma IPOs, that could hurt the ADBE stock price.

MDB announced better-than-expected results in Q4 FY2024, with revenue up 26.8% year on year to $458 million (beat by 5.2%). Once again revenue guidance for the next quarter of $438 million was less coming in 2.5% below analysts' estimates. It made a non-GAAP profit of $0.86 (79% beat) per share, improving from its profit of $0.57 per share in the same quarter last year.

The miss on guidance was in this case significant - Management's revenue guidance for the upcoming financial year 2025 is $1.92 billion at the midpoint, missing analyst estimates by 5.8% and implying 13.8% growth (31.3% in FY2024).

I read the conference call and all of the misses were one-time adjustments and changes in how revenue was being recognized. I invite you to read the transcripts yourself. The fact remains, and this is my opinion, that MDB will continue to be the preferred development platform using their document model which is the leading edge for creating applications. They did speak about incorporating generative AI into their development environment.

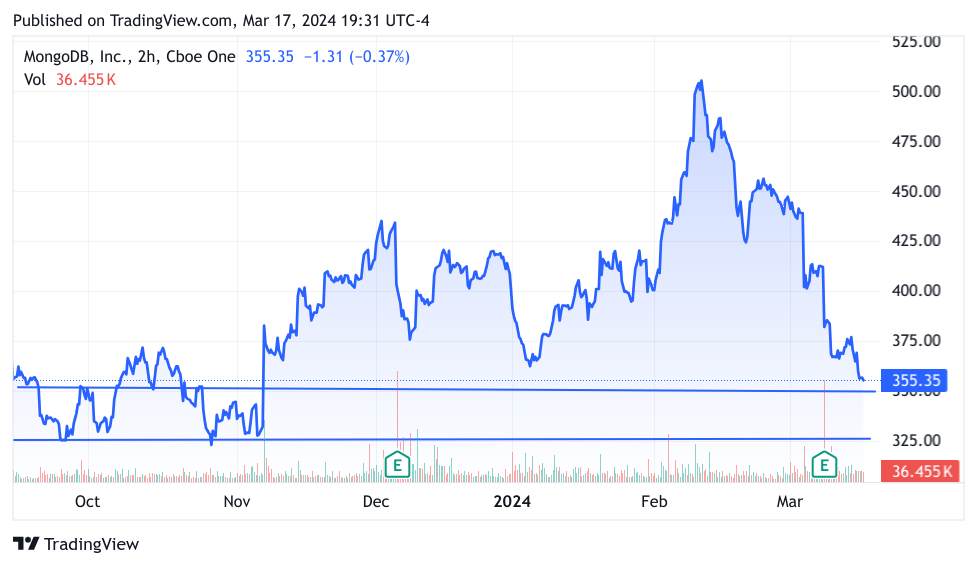

In any case, the stock has cratered losing about 154 from the peak of 509.62 to close at 355.44 down about 30%. Does MDB falling to this level have justification, let me leave you with this piece of data, Atlas, MDB's cloud platform grew by 34% revenue growth for their fiscal 2024. For this price drop of 30% to be justified this growth rate needs to be cut in half and I just don't see that. I see no reason why Atlas's growth doesn't keep rolling along. Let's look at the chart. This is the 6-month chart...

TradingView

MDB looks like it is coming to a support level right where it is currently if not then there are possibly another 25 points of downside.

SNOW is an interesting situation and not strictly a sandbag situation but more of a shocking plot twist. Frank Slootman has announced that he's retiring as CEO and Sridhar Ramaswamy has been named as the new CEO. Frank Slootman is a legendary figure in technology, he has shepherded ServiceNow (NOW) from a private company to an IPO, and he did the same thing with SNOW. To my recollection if not the most successful tech IPOs, then it is one of the top most successful IPOs.

Slootman also championed the consumption-based model which lowers the barrier to entry for prospective enterprise companies. So this was a very big shock to lose him, but Sridhar Ramaswamy is no slouch, and he started with the company as the Executive VP of AI, He led the $115B advertising division of Google Alphabet's (GOOGL) biggest money maker, he has an engineering background and was involved in AI development on the machine learning side from early days. So he is the right guy to take SNOW into AI.

I am pretty excited with this news, letting me get into SNOW at this current inexpensive level. That's right I guess I am letting the cat out of the bag, by saying that I am involved with SNOW, along with MDB, and I will be with ADBE, once I can be sure that it is finally basing.

Back to SNOW and sandbagging, because they have this consumption model for fiscal 2025 projects 22% year-over-year growth, lower than 2024's 36%. As I said the consumption model lowers the barrier to entry for enterprises but it also means it is easy to cut back. Most of the new budget allocation is going for AI server hardware, eventually, that means developing actual applications.

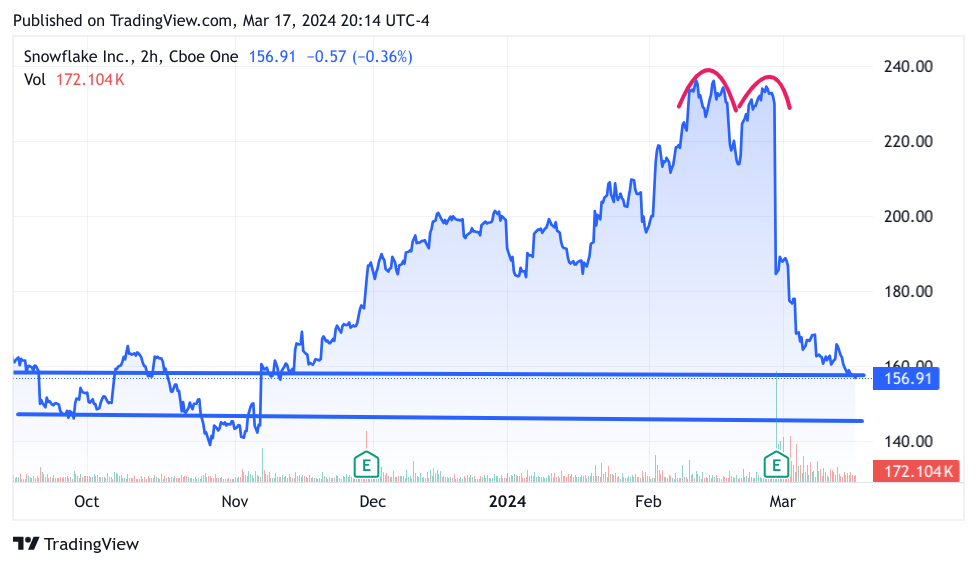

So with the new CEO, who is all about AI, and knows how to grow a huge organization and infuse it with AI like at GOOGL. Sridar Ramaswami has the chops to do it. If you are an organization that wants to use AI you want your data to be pristine, there can be no hallucinations like with ChatGPT you are going to want SNOW. Let's look at the chart for SNOW

TradingView

All three of these charts look so similar. Here though SNOW is right at support at this 156. If we do have more general selling pressure I could see getting close to the second line at 147, the peak is 237.72 which is a whopping 80.75 points! 34% now, I want to buy more shares at around this level.

I just thought I'd use CrowdStrike (CRWD) as a comparison since it is the most successful cybersecurity name now. S grew revenue 38% this Q4 year-over-year to $174.2 million. S's Annual Recurring Revenue grew by 39% compared to CRWD's Annual Recurring Revenue of +34% CRWD's total revenue grew by 33%.

S forward guidance was less than expectations but by a minuscule amount. Looking to fiscal 2025, SentinelOne expects sales projected to be between $812M and $818M, with the mid-point below the $817.5M that analysts were expecting. It expects adjusted gross margin to be between 77.5% and 78.5%. Here's an important metric showing adoption by large enterprises Customers with an ARR of $100,000 or more grew by 30% to 1,133. Once again the miss on forward guidance for 2025 revenue is miniscule.

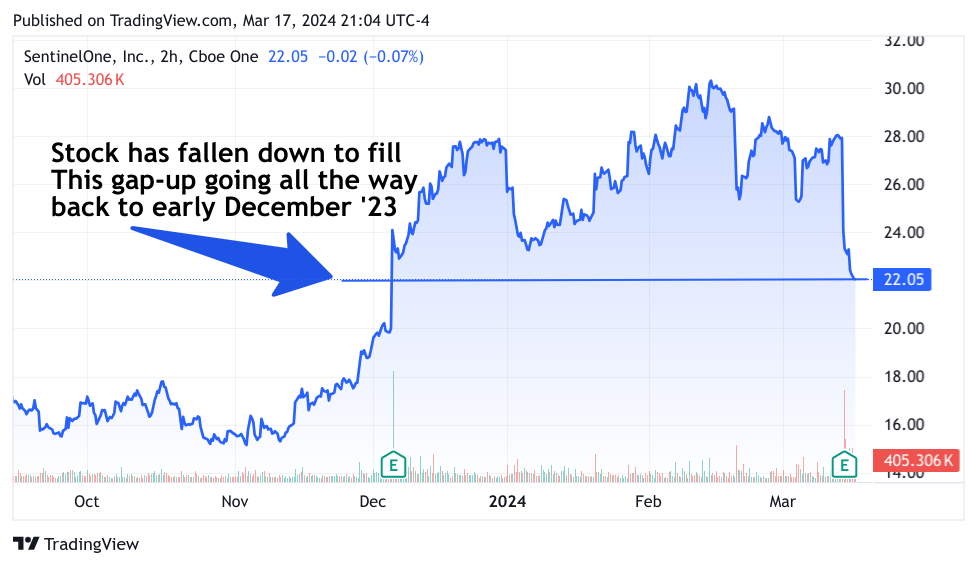

I believe that long-term S will gain in brand and credibility, continuing to rise in prominence. I am a long-term investor who has a pretty low-cost basis but I am now buying more S at 23, and now that it has closed at $22, I will buy more shares. Once it bases and finds a level I will add Call options as a trade. Let's look at the chart.

TradingView

Going back to the 6-month chart we see that the downward spike has filled the "Gap Up". It could still continue several more points but often a gap up or down is filled halfway. I will continue buying it. My cost basis was about 17 before I started adding shares during this sell-off, so the lower it goes it brings my cost basis back closer to where I started.

So in summary these are all great tech names that have been sold off hard. For the most part, this was not about the fundamentals of these stocks going forward, That is why I introduced this concept of "Sandbagging" though not every name here is 100% certainty in that category.

At this point, I would not advise getting into trades using Call options unless you have a very strong conviction and you go out to at least June/July, and perhaps a short call spread to offset decay. If you don't understand the last sentence fully just buy the shares.

Good luck everyone!