Hagerty: An Overlooked, Fast Growing Niche Insurance Stock

Summary

Hagerty, Inc. has experienced consistent growth since becoming a publicly traded company, with third quarter 2023 total revenue increasing by 27%.

The company's combined ratio, as a measure of profitability, is better than its peers.

Hagerty's unique business model and strong fundamentals make it a compelling choice for potential investors, despite concerns about its complex equity structure.

Douglas Sacha/Moment via Getty Images

Hagerty, Inc (NYSE:HGTY) is a multi-faceted automotive lifestyle brand, with a core offering of providing insurance service for vintage and classic cars.

Since becoming a publicly traded company through SPAC in December 2021, Hagerty has seen consistent growth. Third quarter 2023 total revenue increased 27% to $275.6 million compared to the prior year period. While insurance brings in the most revenue (around 90% of total revenue), Hagerty's membership program, online marketplace, and other exclusive entertainment contents are rapidly growing, contributing 37% more revenue year-over-year.

Adjusted EBITDA for the third quarter 2023 was $37.4 million, compared to the negative $10 million in the prior year period. Net income did decrease, but mainly due to non-recurring expenses.

Despite impressive metrics, Hagerty's stock price hasn't mirrored its growth. I believe that this disconnect suggests the market might be underestimating the company's potential.

Strong Future Growth:

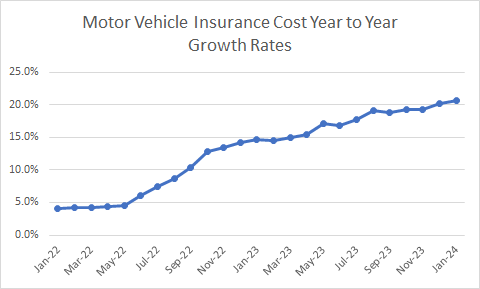

Accelerating premiums: The broader P&C insurance market is seeing a strong premium increase right now. Particularly, vehicle insurance costs are rising rapidly, exceeding 20% year-over-year growth. This trend, still accelerating, positions HGTY for continued revenue gains. Management's 2023 guidance of 15-16% growth seems conservative; 2024 could see even higher numbers.

Bureau of Labor Statistics

Beyond insurance: Non-insurance revenue grew even faster, with memberships and marketplace seeing a 37% jump. Paid member growth (8%) further solidifies this momentum.

Improving Margins:

Lower Loss Ratio: Compared to other insurers, HGTY boasts a favorable loss ratio (41.5% in 2023 YTD, lower than the loss ratio of 46.8% a year ago) thanks to well-maintained, rarely driven classic cars. This translates to significant cost savings versus the industry average (72%).

Controlled Expenses: After infrastructure investments, operating expense growth slowed down (9% in Q3 2023 vs. 43% a year ago). Wages and salaries saw minimal growth (2.4%), and general & administrative expenses even decreased (7.1%) despite strong revenue growth.

Equity Complexity:

Several Types of Warrants: Merging with a SPAC created numerous warrants. Up to September 30, 2023, HGTY had 5,750,000 Public Warrants, 257,500 Private Placement Warrants, 28,750 Underwriter Warrants, 1,300,000 OTM Warrants and 12,147,300 PIPE Warrants. While the OTM Warrants have an exercise price of $15, all other warrants have an exercise price of $11.5. Each warrant is exercisable for one share of Class A common stock at the exercise price. However, warrant holders can also convert to Class A common stock on a cashless basis.

Significant Number of Class V Common Stocks: As of September 30, 2023, HGTY had 84,588,536 shares of Class A common stock outstanding and 251,033,906 shares of Class V common stock outstanding. Class V Common Stock represents voting, non-economic interests in Hagerty. Each share of Class V common stock can be converted to one share of Class A common stock.

However, the effects of those derivatives were limited so far.

Voting Power Dynamics: Class V shares have 10 votes per share, giving large holders like State Farm and the Hagerty family significant control. Converting to Class A shares (1 vote per share) reduces their voting power.

Limited Dilution Impact: Despite potential dilution, no warrants were exercised in the nine months ended September 30, 2023 (unlike the previous year). The actual impact might be smaller than anticipated.

Unique Among Peers:

Moat in the Niche: HGTY's ecosystem, integrating insurance, marketplace, and media content, creates a powerful barrier against competitors. This unique value proposition attracts and retains car enthusiasts, fostering a loyal community. No other P&C insurers come close to its business model.

Better Growth and Better Profitability: While recovering from last year's losses, HGTY stands out among its insurance peers. Notably, it boasts the highest growth rate and enjoys a lower combined ratio, indicating stronger profitability. Though its Price/Cash Flow ratio suggests a higher valuation compared to some of its competitors, factoring in its impressive growth and profitability paints a positive picture. Considering these strengths, HGTY emerges as a compelling choice for potential investors.

SEC

Risk:

Unexpected events such as a major earthquake or a devastating hurricane could significantly impact HGTY’s operating results.

A large shareholder converts Class V common stocks to Class A common stocks.

Conclusion:

HGTY's strong fundamentals and untapped growth potential suggest the current stock price may not reflect its true value. While the complex equity structure raises concerns, investors seeking a future-proof company catering to a passionate niche should consider taking a closer look.