MATJAZ SLANIC

MATJAZ SLANIC

Metropolitan Bank Holding Corp. (NYSE:MCB), incorporated in 1997 and headquartered in New York, New York, is a bank holding company that provides banking services to commercial clients in the New York metropolitan area.

This company has a niche business supported by a strong long-term trend of profitability and growth, as well as a positive outlook to maintain it. Even though the market it operates in is currently under pressure, this bank enjoys a diversified and healthy loan portfolio and has the benefit of being well-capitalized with strong liquidity.

Most importantly, it appears that because of the market uncertainty and high interest rates, the stock price is currently trading around IPO levels, which may have made it overvalued back then, but represents great value today. Its unreasonably low P/E and P/B ratios reflect a lot of upside from here if they return to their means, which are also very conservative for this fast-growing business in my opinion.

I believe that value investors will be interested in what follows...

MCB has a relatively small business, both with respect to the asset size and the market in which it operates. It owns assets of $7.1 billion and operates through its subsidiary, Metropolitan Commercial Bank (a community bank) to serve middle-market corporations (annual revenue of $5 million to $400 million) and real estate entrepreneurs (with a net worth of more than $50 million) primarily in Manhattan and the outer boroughs, as well as Nassau County. It operates through six branches, four of which are in Manhattan, one in Brooklyn, and another in Great Neck, Long Island.

Its motto, "The Entrepreneurial Bank" serves as a hint of the personal touch the company intends to focus on within that area as its value proposition. With many of its competitors having higher lending limits and capital to attract customers, the emphasis it puts on building strong relationships with its clients makes sense.

The bank's revenue mainly comes from originating and servicing CRE and C&I loans that fall within $3 million to $30 million, a range the company believes allows them to focus on an underserved market segment. Though the company doesn't restrict itself regarding the loan term lengths, these generally fall between 3 to 5 years, with payments usually calculated based on a 25-30-year schedule. Also, MCB requires an LTV ratio lower than 75% to originate its CRE loans and most of the C&I loans are personally guaranteed by the principals of the borrower.

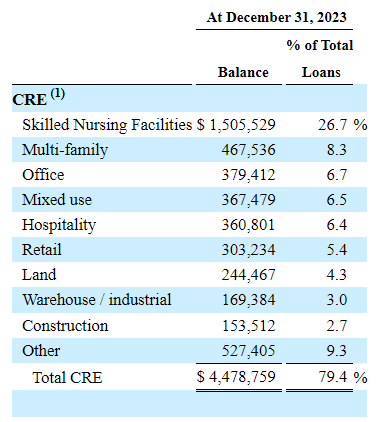

To get an idea of the CRE loan composition, take a look at the image below which indicates that though there is a wide diversification when it comes to the industries the borrowers operate in, about a third of the total loan portfolio is exposed to the healthcare industry:

10-K

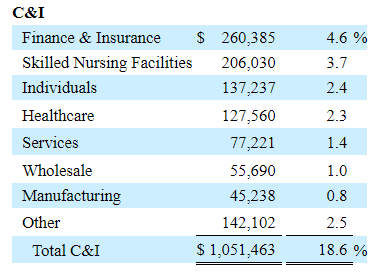

Healthcare is also the highest concentration of the C&I portfolio:

10-K

But the context that has been provided by the CEO in the last earnings call is useful here. He said that they were currently running a stress test on the industry and that they liked the risk profile and the economics of healthcare; so the exposure may not necessarily be a product of chance. He also mentioned that the segment represents a very diversified portfolio and it's not just skilled nursing homes and assisted living facilities.

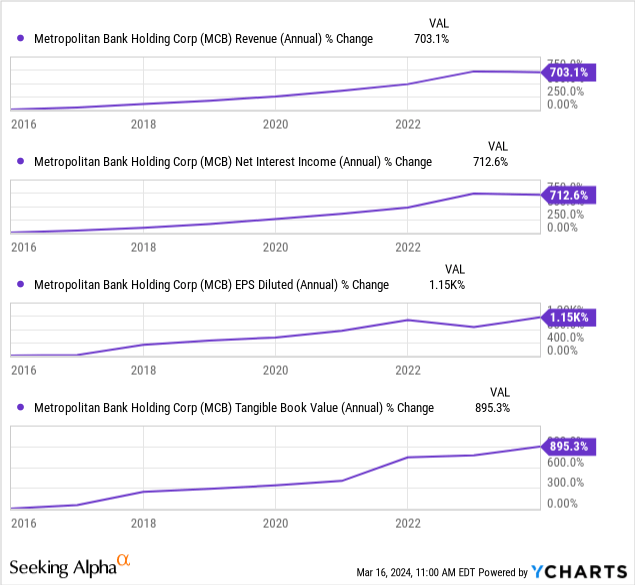

Moving to performance, things are pretty interesting here. First, since the company's shares started trading on NYSE about 8 years ago, the growth of its profitability has been remarkable and that may be an understatement considering the short period involved:

Similarly, its book value has increased by nearly 900%. Not only does that depict a fast-growing business, but the persistent upward trend inspires confidence.

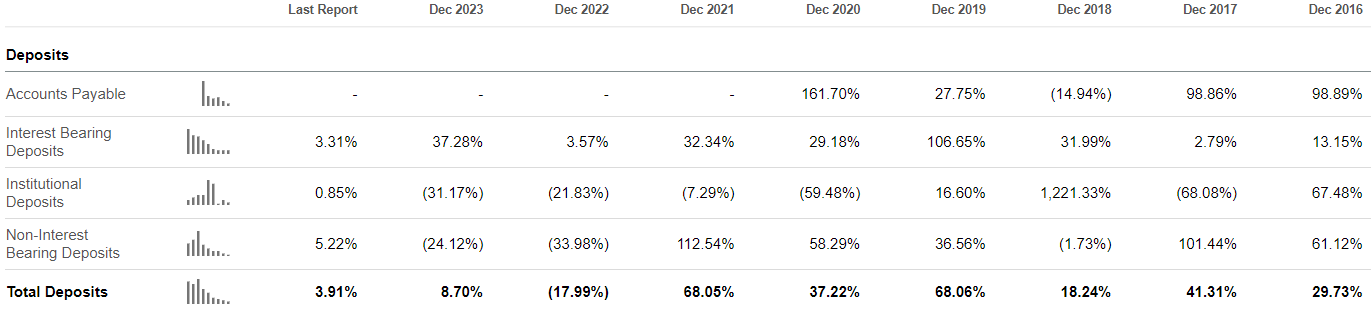

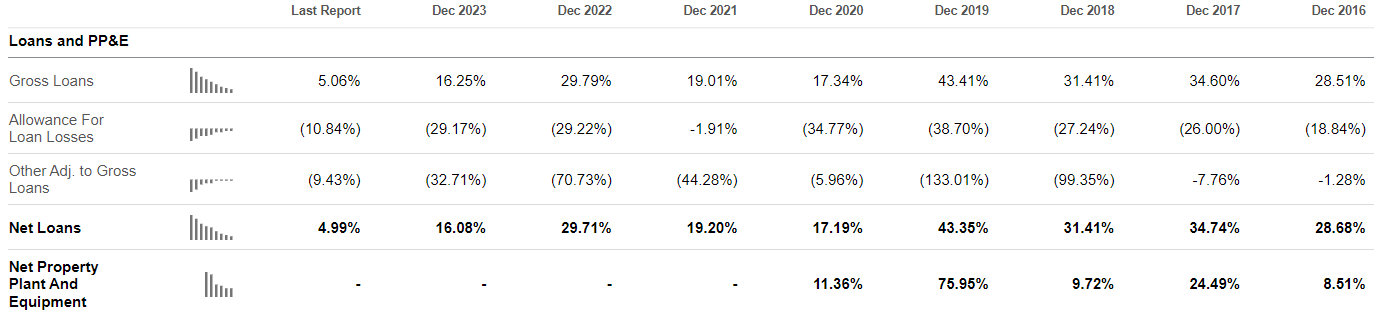

Of course, the basis for its growth was the unrelenting increase in its deposits, year after year (except for the year 2022, a period during which the bank started exiting the crypto-asset business). The table below shows the YoY changes of deposits since the IPO:

Seeking Alpha

In consequence, this expansion allowed MCB to fund the growth of its loan portfolio:

Seeking Alpha

The careful investor, however, will want to investigate further. So here it goes. The portfolio's yield increased to 6.7%, up from 5.32% and 4.77% in 2022 and 2021, respectively. Net interest spread, however, was compressed to 1.85% in 2023, down from 2.82% in 2022 (for context, 68% of deposits were interest-bearing in 2023). NIM remained unchanged YoY at 3.49%.

Moving to interest revenue, it climbed by 43.98% YoY. Nevertheless, net interest income after credit loss provisions was down 3.88% as deposit interest expenses more or less quadrupled since 2022 and wholesale funding costs increased from under a million dollars in 2022 to approximately $22 million in 2023. To be fair though, this is partly a reflection of MCB being liability-sensitive which is also the reason that as interest rates start decreasing, this "weakness" will become the driver for increased profitability. As for the wholesale funding interest expense, that was due to increased FHLB borrowings; the CFO explained that MCB's plan is to drive the borrowings down to more historic levels and implied that it has the means to do so soon as there is currently excess liquidity in the business.

Continuing, the bank witnessed a 4.93% YoY increase in its non-interest income, while net income surged by 30.03% since 2022. Similarly, diluted EPS climbed by 30.62% and tangible book value had a YoY increase of 14.43%. Lastly, the return on average tangible book value was 12.6% during 2023.

Now, it seems that in the future it can maintain such a fast pace of growth, if not increase it. Turning to some forward-looking statements, the CFO said they expect this year's earnings to reflect solid growth from those in 2023. More specifically, he expects NIM to expand by 20 bps in 2024, a forecast which oddly enough is not based on Fed rate cuts but on some deposit initiatives that should increase the number of low-cost deposits. In his own words:

[...] we're not just relying on the Fed to give us some expansion here. We're driving it ourselves, as we have historically. And you saw in this year that just passed, we had only two quarters of compression with the kind of tightening that we face. So we're not relying on the Fed. The Fed has many more cuts predicted. We only have two in our projections, but it is not the underpinning of that margin expansion. It's our deposit initiatives.

At year-end 2023, the bank complied with all of the regulatory capital requirements. Specifically, its CET 1 ratio was 11.5%; though 80 bps lower YoY, a lot higher than the minimum requirement of 6.5%. Similarly, its total risk-based capital ratio was 12.5%, 60 bps lower from 2022, but higher than the 10% required for well-capitalized status. Last, the Tier 1 leverage ratio experienced a modest decrease of 30 bps to 10.3% on a YoY basis, still well exceeding the minimum requirement of 5%, and though the LDR witnessed a YoY increase of 700 bps to 97% in 2023, liquidity remained strong, with cash and equivalents increasing by 4.68% YoY. With reasonable expectations of even more deposit growth, a generally stable deposit base, and strong liquidity, it's less likely that such an increase in the ratio represents much higher risk.

Moving on to the cost of those deposits, a combination of higher rates and an increase in the percentage of loans that were interest-bearing (54.1% in 2022 and 68% in 2023) drove it up. Money market deposits, which represented nearly all of the interest-bearing deposits in 2023, averaged an interest rate of 3.86% during that year, up from 1.08% in 2022. Again, this liability sensitivity has been expensive lately with interest rates peaking last year, but it should prove a boon if and when interest rates start declining.

Additionally, the average rate on the bank's purchased Federal funds was 5.53% at year-end 2023, but the amount represented around 1% of total liabilities. The FHLBNY advances though had an interest rate of 5.54% and represented 6.86% of total liabilities; regardless, it's likely that the company will drive that balance down as I already mentioned.

Now, 3.3% of the loan portfolio was classified as "Special Mention" by the end of 2023, while 1.3% was rated "Substandard". Also, the non-performing loans ratio was 0.92%, while there were almost none in 2022, reflecting the outcome of the high interest-rate pressure. The reserve coverage ratio was adjusted from 0.93% in 2022 to 1.03% in 2023. Fortunately, the net charge-off ratio was only 0.02% in 2023. So, while there is some potential deterioration in the value of the loans, the metrics that reflect it are a product of an unusually challenging year for many financial institutions and don't constitute the basis of a trend when it comes to MCB.

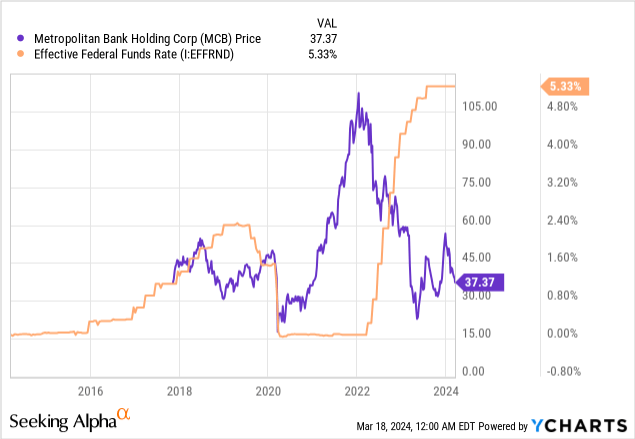

Now we come to the heart of this analysis. As you can see from the image below, since MCB IPO'd it demonstrated its sensitivity to interest rates through an inverse correlation between the Fed rate and its price:

While the business remained profitable throughout that period, the market responded accordingly to the rate which started climbing in 2018, which "allowed" the shares to recover during 2019 and flourish during 2020-2022, before the shares fell lower than IPO levels shortly after the rate started climbing again.

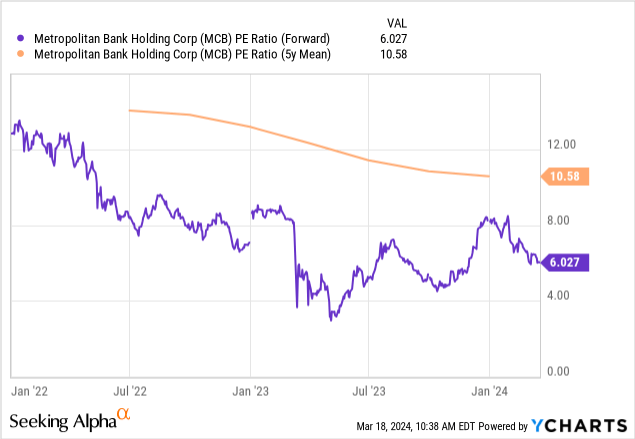

Higher interest rates, however, provide us with half the picture regarding market sentiment. New York City's Local Law 97 which came into effect this year partly contributes to the increasing expenses of landlords, while an over-supplied market coupled with slowed rent growth doesn't help with sentiment either. It's reasonable that the market doesn't want to be exposed to banks operating in the city today. But often the market overreacts and now that you understand that the fundamentals are solid, you may be able to see that the P/E ratio for the stock is too low right now:

Based on what we've observed so far, it's reasonable to assert that MCB deserves at least to be trading closer to its 5y mean earnings multiple of 10.58x which would imply a ~76% upside from here.

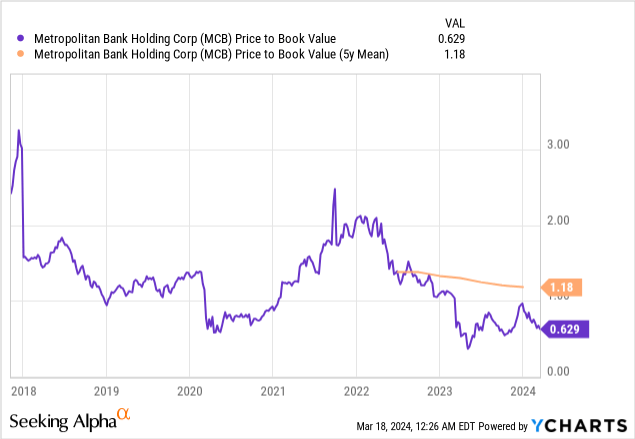

The same goes for the P/B ratio that today is at 0.62x, much lower than its 5y mean of 1.18x which suggests a ~90% upside:

Since profitability doesn't seem to be slowing down, I'm expecting that lower interest rates would at least help realize some of that upside, if not allow the price to reach its 2022 peak of ~$110.

Regardless, I wouldn't find this attractive if it were not for the tangible book value per share at $56. The current price reflects a discount of ~33% to tangible equity which in turn provides a more than decent margin of safety for value investors.

Be that as it may, there are a few risks to consider here. Being a bank, credit risk is the most important one; while there are no signs of a trend indicating a deteriorating credit profile of the loan portfolio, this can always change if interest rates keep increasing.

Speaking of which, even if higher interest rates don't result in increasing defaults (likely with this business), they can keep the market undervaluing the stock longer than you may be able to suffer an opportunity cost for. And since this bank doesn't pay a dividend and is unlikely to ever do so, there would be nothing to offset such cost. However, experts forecast a couple of Fed rate cuts during this year, which makes an opportunity risk less likely to be realized.

Another important risk has to do with changing regulatory standards. More stringent capital requirements can slow the bank's growth. Keeping your ears to the ground when it comes to New York City regulations is essential to monitoring that risk.

Notice that these are general risks that apply to the industry, which goes to show that there are no significant specific risks to MCB that other banks may enjoy the absence of.

All in all, the margin of safety provided here more than makes up for the risks. MCB runs a profitable business while remaining well-capitalized and maintaining strong liquidity. Additionally, some of its excess cash is likely to be used to drive the debt further down relatively fast.

And while it's true that mortgage loans in New York City are generally in a precarious position given the increased compliance and debt costs coupled with slowed rent growth, investors need to remember that MCB enjoys a niche business catering to high net-worth individuals and businesses operating in the Metropolitan area of the city. The strength of its customer base is also evident in its healthy loan portfolio that lacks any trend of deterioration based on its NPLs and charge-offs.

The significant upside which I believe is supported by the much-deserved, yet conservative, earnings multiple and premium to book value seals the deal and makes MCB a strong buy at current levels. I intend to keep monitoring this enterprise, however, in case something changes significantly regarding its business or the price reaches too optimistic levels.

Let me know your thoughts in the comments. Do you own the stock or are you considering it? I'll get back to you soon. Thank you for reading.