Nazar Rybak

Nazar Rybak

Following my coverage of Masco Corporation (NYSE:MAS), for which I recommended a buy rating as I turned positive on the outlook based on 3Q23 performance, this post is to provide an update on my thoughts on the business and stock. MAS 4Q23 performance reinforces my buy rating as the underlying demand appears to have stabilized, and FY24 could be a positive year if macro conditions continue to improve. Management has also done a great job of execution, leading to market share gains. With top line recovering, cost moderating, and management initiatives to improve productivity, I expect margins to expand faster than I originally assumed as well.

MAS 4Q23 performed well, reporting an adj. EPS of $0.83, beating consensus estimate of $0.66 by 25%. By segment, Decorative Architectural [DA] saw a revenue decline of 7%, as DIY paint declined by high single digits and Pro was down slightly. However, adj EBIT margin was up 87bps to 14.8%. For plumbing, revenue was up 1%, with North America up 1% and international down 3%. The plumbing segment adj EBIT margin was up 407 bps to 16.4%.

Own calculation

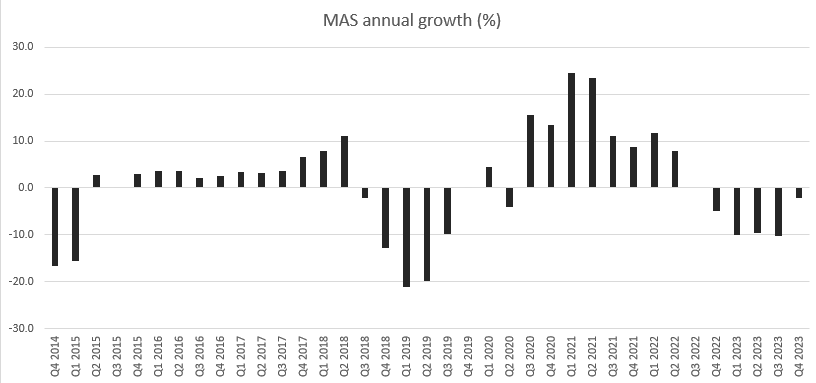

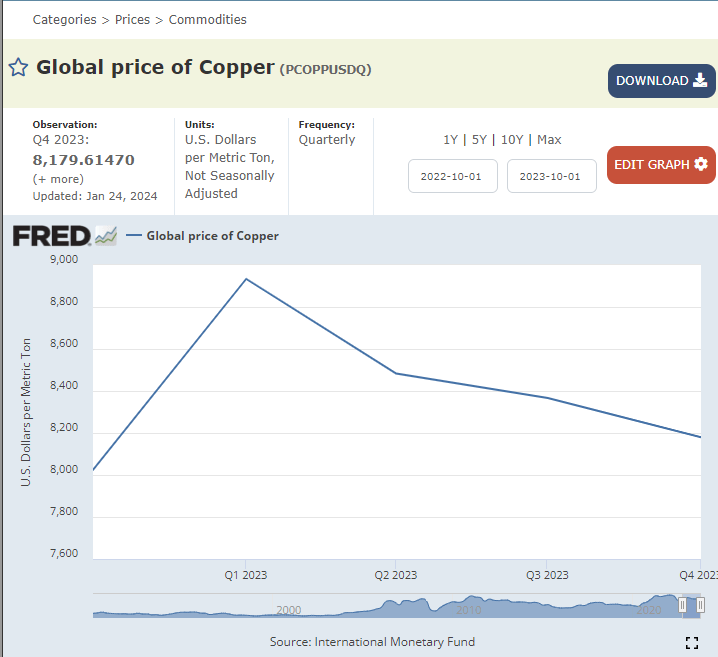

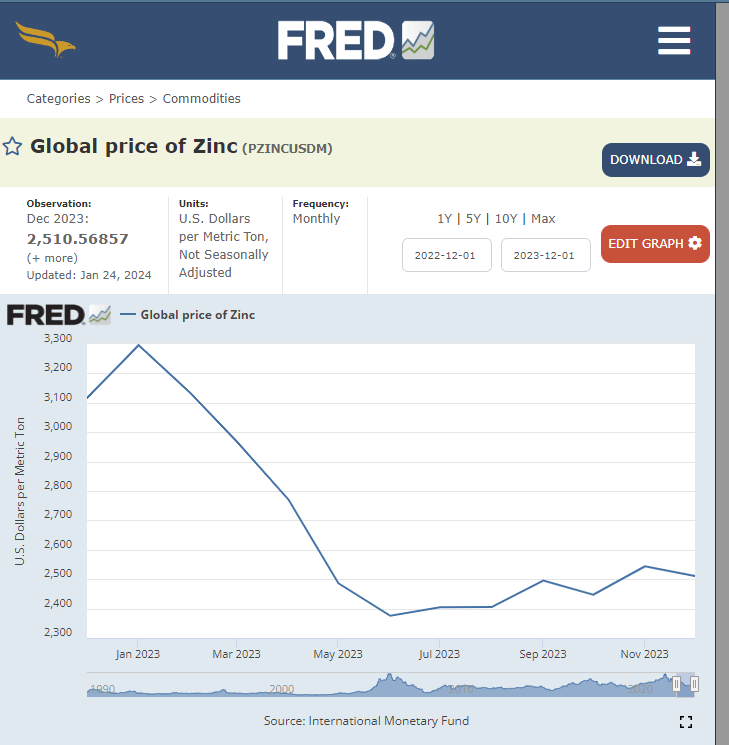

Based on 4Q23 performance and management’s comments during the call, I have become more confident that MAS is on track to continue riding this recovery growth cycle. According to management, demand remained stable in 4Q23, and they expect sales in 1Q24 to be flat to down compared to last year. However, they do expect sales to improve sequentially throughout the year. The former comment is a major indicator of how the underlying demand has improved (after five quarters of negative growth), and FY24 is going to be a year of positive growth. Another important sign that demand is on the upswing is that, despite a weak global macro in 4Q23, the wholesale channel drove mid-single-digit growth for Masco North America's plumbing brand Delta, and demand for brands in Europe and China is slowly but steadily leveling off. For FY24, management expects plumbing to outgrow the industry through its showroom gains driven by new products and the repricing of its products back to historical levels. The plumbing segment top line performance, driven by volume, coupled with a moderating cost structure due to lower raw material costs (copper and zinc prices coming down) and operating leverage (higher volume), should drive margin expansion as management guided (a 25–30% incremental margin). In the near-term, any reduction in input cost (zinc price expected to continue falling, and copper price to be flattish with a small increase in price), will surely help improve margins, until such time management decides to pass through all the cost-savings to consumers. In that case, while the improved-margin benefit is gone, lower product pricing should drive volume growth, which I expect to be next positive to the margins. All in all, these should pave the way for the plumbing segment to hit management's long-term target of a 20% EBIT margin by 2026.

And so, we felt pretty confident with regards to our 20% margin target in 2026. On Decorative, we just have a range of 19% to 20%, and as Mike pointed out, it's more consistent with kind of where we ranged historically. 4Q23 earnings results call

FRED FRED

As for the DA segment, a similar top-line dynamic is seen, where management expects FY24 demand for paint to be flat to down (DIY to see low-single-digit declines while Pro sees low-single-digit growth percentage growth). While DIY paint continues to see weakness from lower renovation and remodeling demand as interest rates stay high, the positive takeaway I got from the guide was that the positive growth in Pro Paint suggests that the investment in Home Depot collaboration is generating very positive results, which I also expect to allow MAS to gain market share. From a number perspective, as per management, pro paint sales continued to stay at around 60% on a 3-year stack basis, indicating the market share gained was structural and how effective the distribution partnership with Home Depot is.

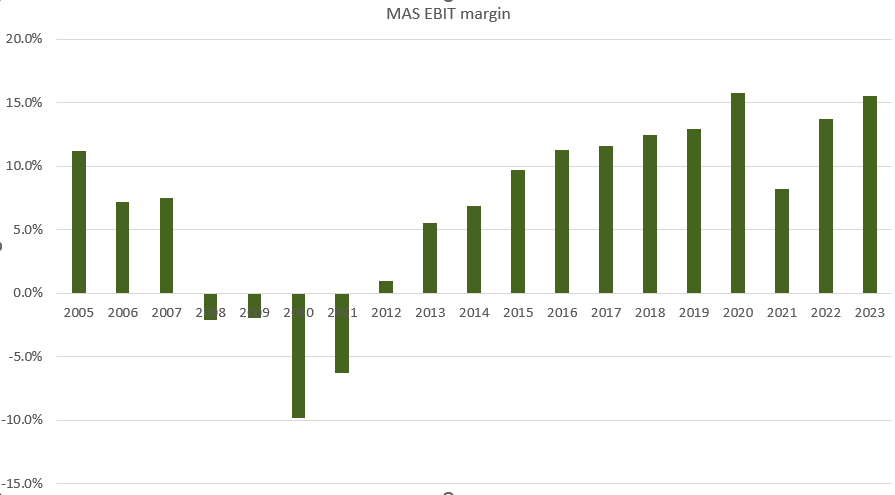

Overall, while revenue is expected to be down in 1Q24, I think it is increasingly evident that demand is stabilizing, and FY24 could be a positive year if macro conditions turn more favorable. With MAS's exposure to lower-priced items, I anticipate volume gains as a result of falling rates, increased housing activity, and sustained consumer confidence. Additionally, management is actively working on cost and productivity initiatives with a longer-term focus. These initiatives are expected to be completed in FY25/26 and will contribute to an estimated 150bps expansion of margin. Given the management track record of expanding EBIT margin, I believe these expectations will materialize.

Own calculation

Own calculation

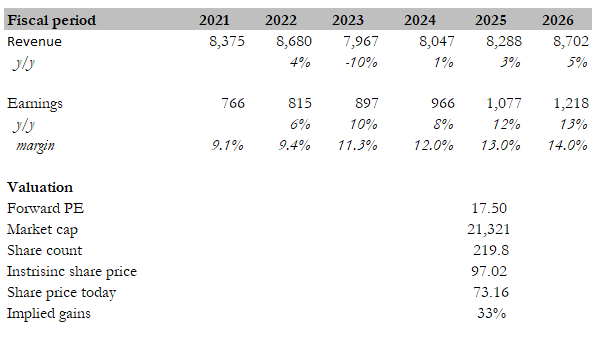

With a clearer view of underlying demand, I now have more confidence in projecting the business over the next few years. My target price for MAS based on my model is $97. The changes to my model are:

As I pointed out previously, the biggest risk for the MAS is how the macroeconomic system performs. Ideally, it should start to recover as inflation has come down (though still sticky) and the unemployment rate has moved up modestly from the lows of 2023. However, compared to my last write-up, I think the geopolitical situation has gotten a lot worse, especially in the Middle East, which could result in a full-blown conflict that could have a significant impact on global economies as supply chains get disrupted again.

I reiterate my buy rating for MAS following its impressive 4Q23 results. I think it is evident that MAS is seeing a stabilization of underlying demand, with FY24 poised for positive growth if macro conditions improve. Management's effective execution and market share gains, particularly in the plumbing and paint segments, make me confident that MAS is on track in its recovery growth. Margin expansion should also materialize through cost initiatives and volume gains. The primary risk remains macroeconomic uncertainties, exacerbated by geopolitical tensions.