JHVEPhoto/iStock Editorial via Getty Images

JHVEPhoto/iStock Editorial via Getty Images

Since Marriott (NASDAQ:MAR) was last covered in November 2022 (hold rating), Marriott has delivered a 56% shareholder return, outpacing the S&P which rose 31%. The company’s fundamentals remain intact but their valuation appears a bit stretched at this point. It could be viewed as a hold.

Marriott International is a leading operator and franchisor of hotel, vacation rental and other types of lodging under an extensive brand portfolio covering luxury and affordable markets. The company operates two business segments namely, (1) U.S. & Canada (which generates over 70% of revenues and segment profits); and (2) International.

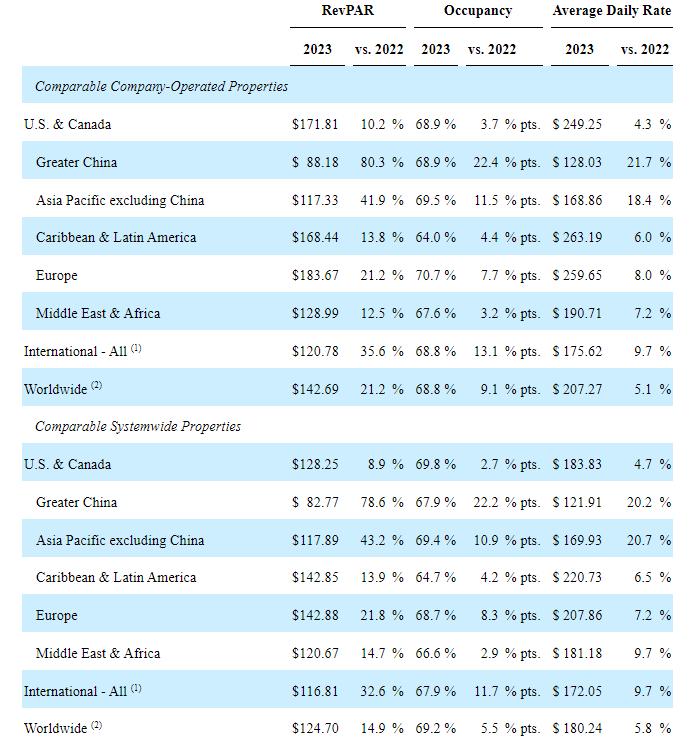

Worldwide RevPAR (room sales for comparable properties divided by room nights available during the period) increased 15% in 2023, driven by Average Daily Rate (ARD) growth of 5.8% and occupancy improvement of 5.5%. U.S. and Canada RevPAR increased 8.9% in 2023, driven by ADR growth of 4.7% and occupancy improvement of 2.7%. International RevPAR improved 32.6% driven by ADR growth of 9.7% and occupancy improvement of 11.7%. This was helped by continued post-covid recovery in room demand, particularly in Greater China and Asia Pacific excluding China which saw a lifting of covid restrictions imposed for much of 2022.

Macro challenges and a likely gradual waning of the ‘revenge travel’ phenomenon in the West, offset by continued recovery in Asia, notably China (domestic tourism has reached 80% of pre-pandemic levels in China but outbound tourism remains muted) suggests a moderation in RevPAR growth near term. Consultancy firm CBRE project global RevPAR growth to moderate to 3% in 2024. For the coming year, Marriott management is projecting worldwide RevPAR growth of 3%-5% and net room growth of 5.5%-6%.

Marriott International Fy2023, 10-K

Medium term industry prospects are generally positive. Lodging demand is forecast to grow across all segments. Demand for luxury hotel stays, Marriott's bread-and-butter business is forecast to grow at between 6%-10% according to forecasts (for instance Spherical Insights projects the market to grow 10.5% while Transparency Market Research projects 6.2%)

The midscale segment, which Marriott is increasing focus on, is emerging as a hot growth market driven by business travelers, and millennial travelers seeking comfortable stays without breaking the bank. Vacation Airbnb meanwhile appears to be going through a rough patch with regulatory hurdles in several countries potentially curtailing supply, which could provide a tailwind for hotel chains with exposure to the midscale segment.

Management’s growth strategy could help the hotel chain capture market share. Management is aiming to grow room share, with a targeted 5%-5.5% CAGR net room growth until 2025. Marriott added 64,000 organic gross rooms to their system in 2023 (bringing the total to nearly 1.6 million rooms) and their pipeline of 573,000 (up 15% from the previous year) keeps them ahead of peers whose pipelines are relatively smaller.

Room pipeline at December 2023 | |

Marriott | 573,000 |

Hilton | |

IHG | 297,000 |

Hyatt |

Additionally, management is expanding into underserved markets such as the fast-growing affordable midscale segment, and all-inclusives which are becoming increasingly popular. Marriott made a number of moves in the midscale space last year to bolster their brand portfolio which currently leans towards the premium end; last year the company launched a new budget-friendly brand StudioRes (management plans to launch 300 more StudioRes locations in the U.S.), and completed its acquisition of Mexican mid-scale brand City Express. Marriott's is aiming to expand City Express across the Caribbean and Latin America with new properties. Marriott launched Four Points Express by Sheraton, a conversion brand in the mid-scale segment for the Europe, Middle East, and Africa markets. Meanwhile, Marriott's first All-Inclusive resort, Marriott Cancun made its debut early this year. and another one in the Dominican Republic slated to open in 2025.

Marriott has been acquisitive over the past few years, its most recent acquisition being mid-scale hotel chain City Express which completed last year. Going forward, considering ongoing consolidation in the hotel space and relatively manageable balance sheet (see below), Marriott may remain acquisitive which could support market share gains.

Marriott's strategic partnership efforts could positively contribute towards defending market share and contribute to top line growth as well. Notable agreements include partnerships with MGM Resorts (MGM) (in which a number of MGM properties were converted under a new Marriott-MGM joint brand known as MGM Collection), Cathay Pacific and Singapore Airlines (which provides Marriott with access to the two airlines' respective loyalty program members). These partnerships help expand Marriott's hotel portfolio and strengthens their loyalty program, and increases opportunities to capture a greater wallet share of loyalty members' travel and entertainment spend.

Marriott, the market leader in terms of room number with a 16% market share in the U.S. and 4% internationally (source: FY2023 10-K), is ahead of peers like IHG, Hyatt, and Hilton in terms of global presence, number of brands, and loyalty program popularity. A wider global presence and locations, and a broader assortment of lodging brands catering to guest across various price points enhances the value of their loyalty program, Marriott Bonvoy, which at nearly 200 million is among the most popular rewards programs for frequent travelers. For perspective, if Marriott Bonvoy were a country, it would rank as the eighth-biggest country in the world in terms of population. Notably, Marriott’s relatively high member occupancy is indicative of the strength of Marriott Bonvoy’s value proposition. Marriot could leverage their loyalty program to launch new hotel brands, which in turn further enhances the program’s value proposition and therefore draws more members as well as more property owners, thereby creating a positive network effect.

Number of properties worldwide | Number of countries | Number of brands | Number of loyalty program members | Member share of room nights % | |

8,785 | 139 | More than 30 | 196 million | Over 60% | |

| Hilton (HLT) | 7,500 | 126 | |||

IHG (IHG) | 55% | ||||

| Hyatt (H) | 1,200 | 77 | 29 | 43.8 million | 43% |

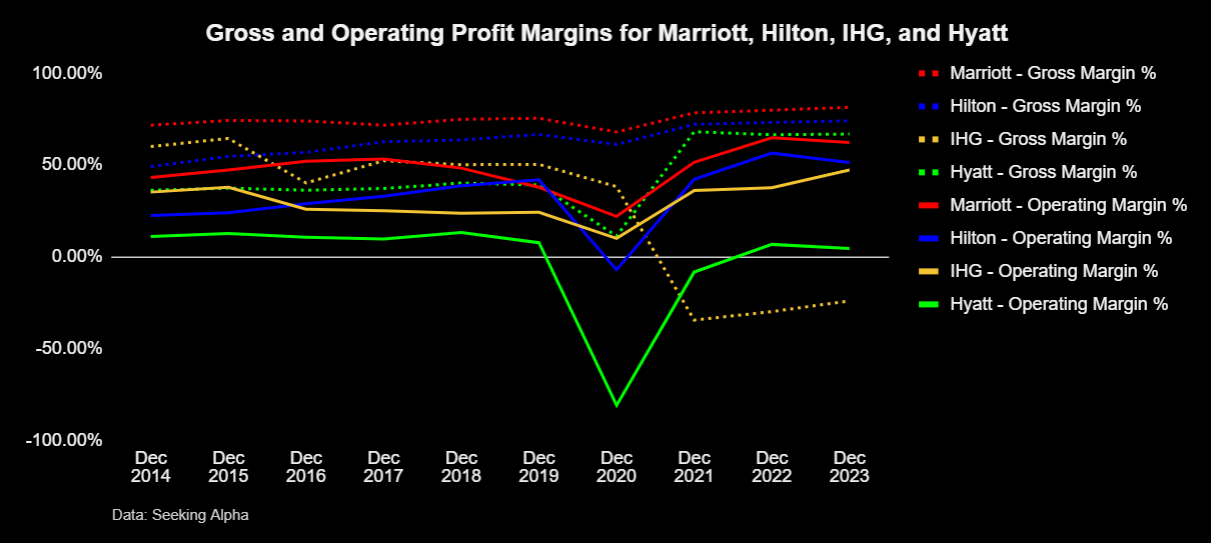

Marriott has demonstrated consistently better margins compared to rivals.

Author

The company’s balance sheet also stands out as being among the stronger ones relative to peers.

Debt to capital | |

105.6 | |

130 | |

216 | |

48.6 |

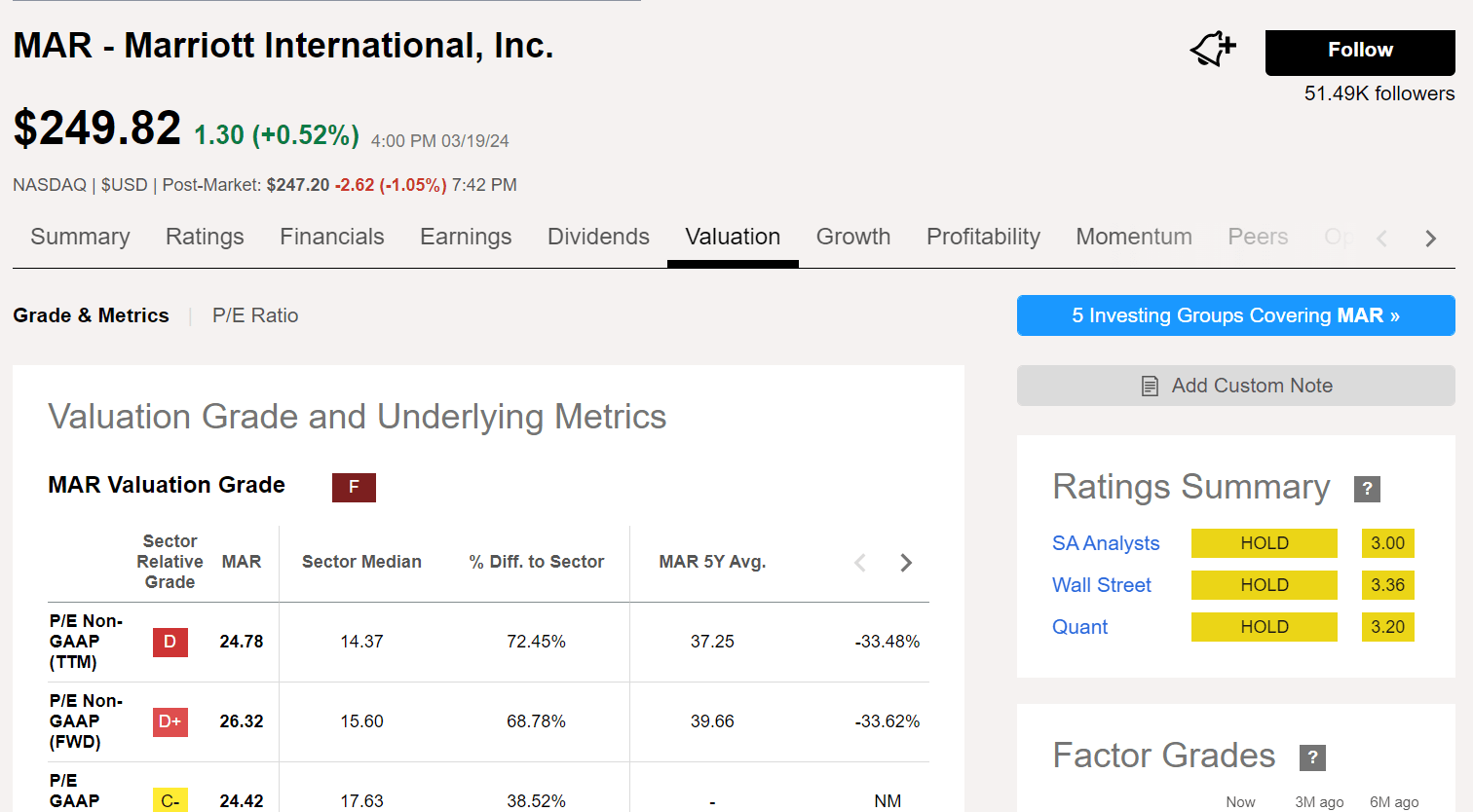

Marriott’s stock has appreciated 53% over the past year and currently trades at a forward P/E of 26, which is higher than the sector median of 15.6 and is higher or on par with tech stocks like Alphabet (forward P/E 22) and Apple (forward P/E 26). A premium may be justifiable considering Marriott’s market leading position and above average profitability, however their current valuation nevertheless appears to be on the pricey side for a company that is not exactly a growth stock. Marriott’s revenues have grown at a CAGR of over 8% over the past decade, and free cash flows have grown at over 12% during the same period.

Conservatively assuming FCF grows at around 6% annually over the next few years (in line with management’s targeted room growth medium term, along with RevPAR growth conservatively assumed at 1%, more on this later), a terminal growth rate of 2% and a discount rate of 10% suggests Marriott is worth around $36 billion, considerably lower than their $71 billion market value today. RevPAR growth of 1% is based on an occupancy rate of around 69% (unchanged from last year the reasoning being hotel chains have been adding thousands of rooms which may keep a lid on occupancy rates going forward), and ADRs roughly increasing 1% annually (to account for anticipated ADR recovery and growth in markets like Asia Pacific offset by increasing room supply and contribution from the midscale segment which typically carry lower room rates). Marriott's RevPAR was $124 for systemwide properties in FY2023, so my forecast conservatively assumes RevPAR would grow to roughly $129 by 2027.

Even if we take a bull case scenario with a more aggressive FCF growth assumption of 20% over the coming three years, and all other assumptions equal, Marriott would still be valued at roughly $51 billion.

Assumptions used are already quite conservative however if financial performance deteriorates significantly for reasons such as an unanticipated sharp and prolonged recession, a trade war that constrains international travel particularly between China and the U.S., a sharp drop in room growth for reasons such as room oversupply, or a black swan event such as a pandemic, Marriott's valuation and stock price could be materially impacted.

Marriott has a hold analyst consensus rating.

Seeking Alpha

Marriott's stock has had a good run over the past year (up 50%), possibly driven by investor exuberance over the travel sector's post-pandemic rebound. Near term prospects however are likely to be muted as travel demand normalizes. The valuation is quite demanding based on a few metrics, however good fundamentals do not make it a convincing sell unless investors have better opportunities elsewhere. The stock could be viewed as a hold.