joebelanger

joebelanger

MAG Silver Corp. (NYSE:MAG) is a silver mining company with a 44% ownership interest in Juanicipio, which is a Mexican mine that went into commercial production during 2023. Fresnillo (OTCPK:FNLPF) owns 56% of Juanicipio and is the operator. MAG Silver is listed in both the U.S. & Canada (TSX:MAG:CA) and the reporting currency is U.S. Dollars.

Figure 1 - Source: Corporate Presentation

The company also has the exploration projects Larder in Canada and Deer Trail in the U.S., but I would prescribe very little value to those projects today given their earlier exploration stages. This article will primarily be focused on Juanicipio, and the Q4 2023 result which was released earlier today.

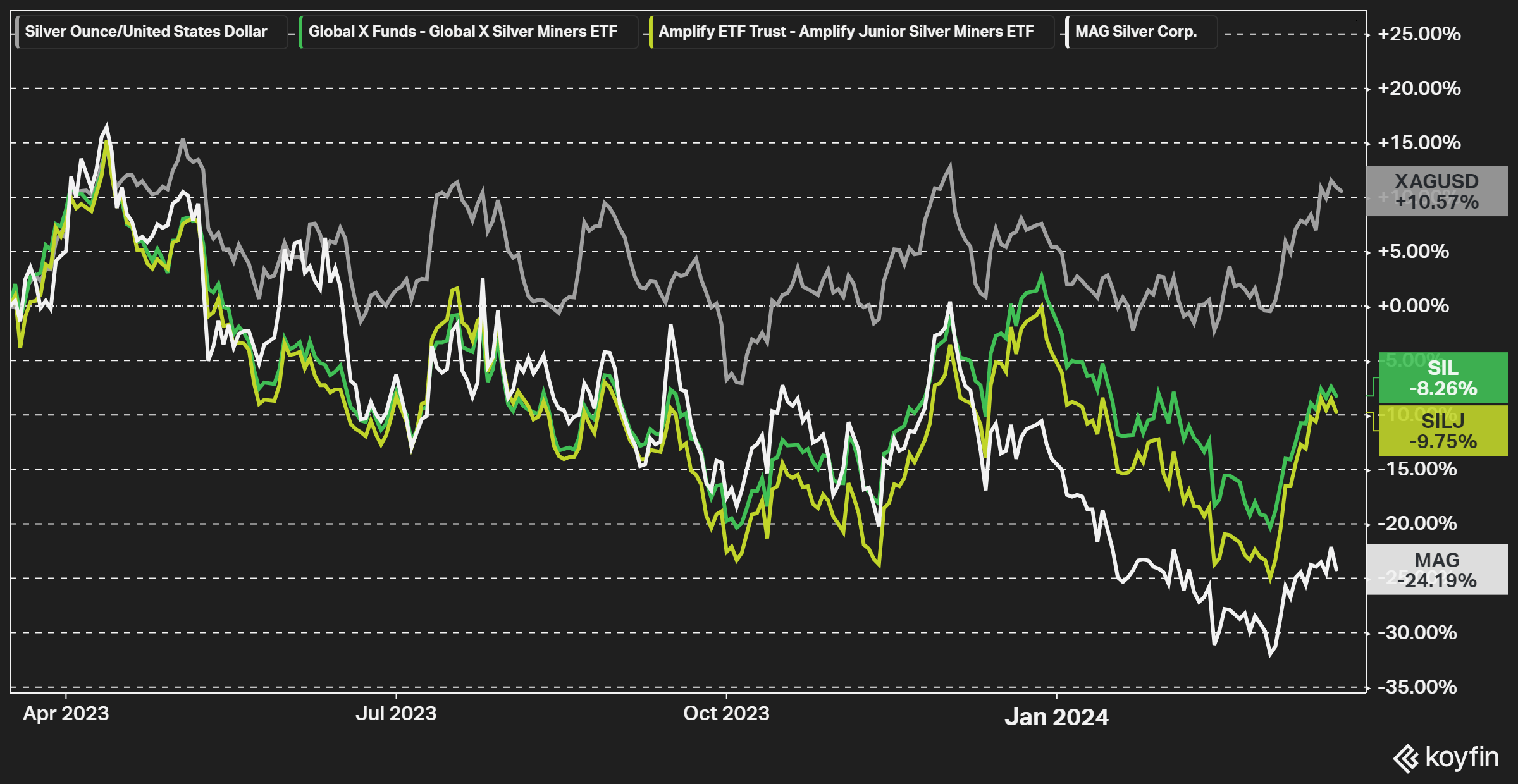

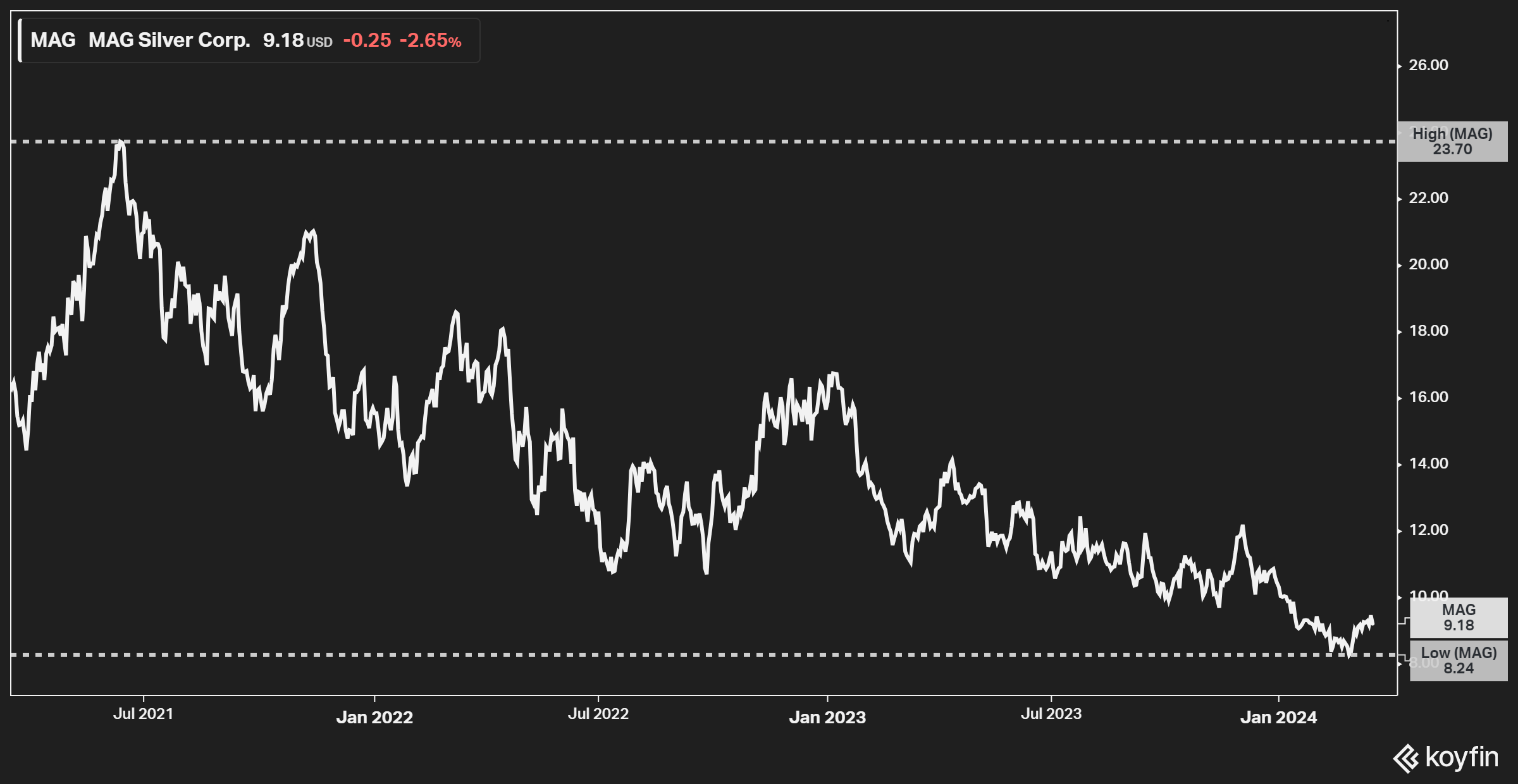

The stock price performance of MAG Silver has been very poor over the last year. Silver miners in general have lagged the metal, so it is not just MAG Silver which has performed poorly. With that said, the magnitude of the underperformance in MAG is surprising given that the ramp up of Juanicipio has over the last year gone according to the plan, even if there were more substantial delays in 2022.

Figure 2 - Source: Koyfin

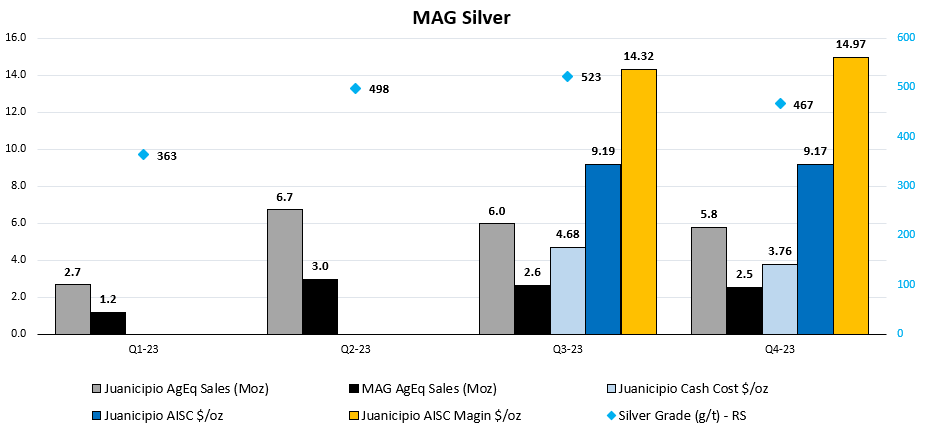

The throughout at Juanicipio did increase by about 8% in Q4 compared to Q3, but the silver equivalent production of Juanicipio declined slightly quarter-over-quarter. The silver grade decreased to 467 g/t in Q4 from 523 g/t in Q3, which no doubt played a part.

Figure 3 - Source: Quarterly Reports

The silver equivalent sales of Juanicipio, on a 100% basis, was 5.8Moz in Q4, which equals an annualized silver equivalent sale of 23Moz. The silver sales decreased in Q4 while the gold, zinc, and lead sales ticked up in the last quarter. However, as much as 70-75% of the Juanicipio revenues come from silver, which is why the gold and base metal increases didn't have that large of an effect on the silver equivalent figure.

The cash cost of Juanicipio was $3.76/oz in Q4 and the all-in sustaining cost ("AISC") was $9.17/oz. The realized silver equivalent price increased slightly in Q4 compared to Q3, which led to an extremely competitive AISC margin of $14.97/oz in Q4.

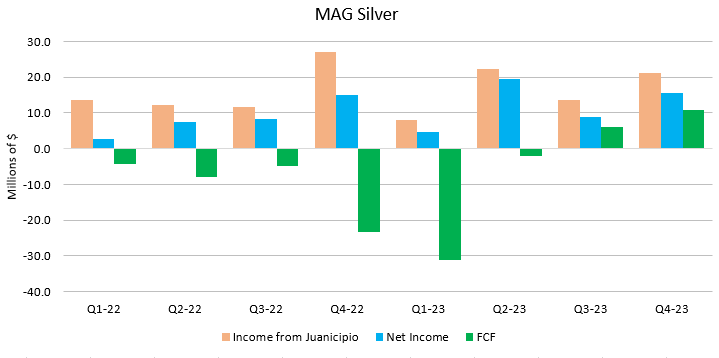

Juanicipio and MAG Silver have been generating relatively reliable earnings over the last two years, but the free cash flow has up until recently been negative. Free cash flow for MAG Silver turned marginally positive in Q3, and Q4 showed an even better free cash flow of $11M.

Figure 4 - Source: Quarterly Reports

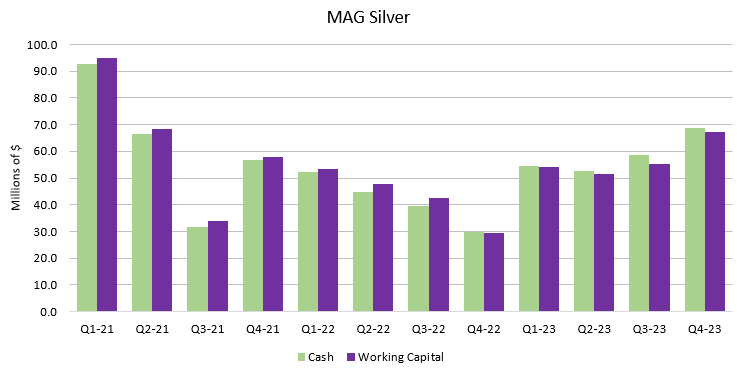

It is very encouraging to finally see one of the best silver mines in the world starting to generate solid free cash flow for MAG Silver. The balance sheet is very strong for MAG, with no debt, $69M in cash at the end of 2023, and $58M in working capital. The company did also get a $40M senior secured revolving credit facility during Q4, which further improves the liquidity position.

Figure 5 - Source: Quarterly Reports

MAG Silver is due to release an updated technical report for Juanicipio this quarter, but that report has yet to be released, and we didn't get any 2024 guidance figures from the company in conjunction with the Q4 report. So, there is still some uncertainty about production and cost levels going forward.

If we for 2024 assume a silver equivalent volume of 11Moz, an AISC of $10-11/oz, and $45M on top of that in other, general & administrative expenses, and exploration, MAG Silver is trading with a free cash flow yield around 12-14% for 2024.

The free cash flow yield is based on the enterprise value and current metal prices. That is a very attractive valuation for a company with some of the lowest costs in the industry and a mine-life of around 15 years. This is also well above what we normally see in the precious metals industry, so MAG Silver is very attractive relative to its peers as well.

Q4 was a good quarter for MAG Silver, where both Juanicipio and MAG Silver generated a positive free cash flow. However, we are still waiting for more clarity on the capital allocation strategy from MAG Silver, where the management team is in my view a minor concern with this company.

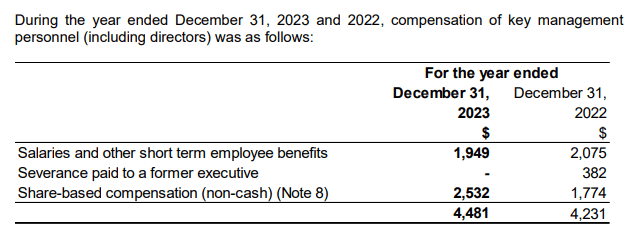

Figure 6 - Source: MAG Silver Q4-23 MDA

It is not the compensation levels, which are reasonable in my view. It is more the mindset, where management has frequently expressed views that the cash flow should primarily be used for exploration and if there is something left over, it will go to shareholders.

There is now sufficient liquidity to make sure any potential outages or unexpected capital requirements for Juanicipio are easily tackled. I do also support continued exploration, especially at Juanicipio. However, a shift in mindset with a focus on shareholder returns, which would still leave money for exploration, would likely do wonders for this depressed share price.

Figure 7 - Source: Koyfin

So, even if I have some reservations about the capital allocation decisions, I still think MAG Silver is a strong buy with the current valuation. It is one of the best silver mining companies around with its low operating costs, a relatively long reserve life, and a good balance sheet. If Juanicipio performs consistently over the next few quarters, I do expect we will see at least some buybacks or dividends later in 2024.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.