Flashpop/DigitalVision via Getty Images

Flashpop/DigitalVision via Getty Images

Readers may find my previous coverage via this link. My previous rating was a buy, as I believed Live Nation Entertainment, Inc. (NYSE:LYV) has a very strong competitive advantage that is hard to replicate. As the business scales in size, its flywheel effect enables it to grow even bigger. I am reiterating my buy rating for LYV as the business did a lot better than I expected for FY23. The outlook for FY24 is also very healthy, with multiple indicators that suggest growth can continue to be in the high single-digit range.

LYV reported on February 22nd 4Q23 total revenues of $5.84 billion, significantly higher than consensus expectations for $4.77 billion. Strength was seen across all segments. The concert segment generated $4.87 billion of revenue, with the growth mainly driven by the North American region, which saw a significant increase in events, up 24% y/y in 4Q23. Albeit, the international segment saw modest growth at 11% y/y in the quarter. The ticketing segment saw $740 million of revenue with an AOI [adjusted operating income] of $236 million. The sponsorship segment generated $255 million in revenue while generating $12 million in AOI. Overall, my takeaway for 4Q23 is that LYV demonstrated broad momentum for the company.

Based on author's own math

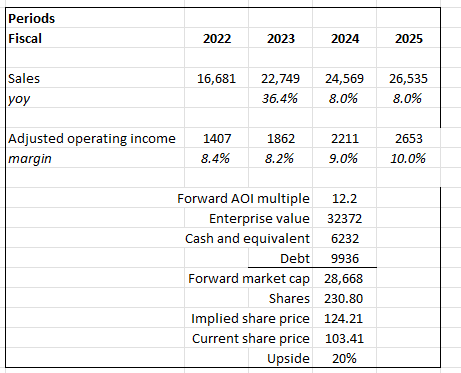

Based on my view of the business, LYV should be able to continue growing like it did historically (8% CAGR), bringing the business to a size of ~$26.5 billion in FY25. One adjustment I made here in this model is that I now expect a gradual step up to 10% AOI margin instead of a surge to 10% previously, as FY23 proved that it might take longer than expected for AOI margins to recover. However, because of the higher-than-expected growth rate seen in FY23 (reported 36.4% vs. my expectation of 21%), my current FY25 AOI expectation is ~$300 million higher at $2.65 billion vs. $2.35 billion previously. With a clearer outlook today, I think the market is going to continue supporting the current valuation that LYV is trading (12.2x forward EBITDA).

I expect LYV to continue its growth momentum, and there are multiple indicators that are pointing to this. For instance, LYV has already sold 57 million tickets for shows in 2024, up 6% vs. the same period last year (Jan to mid-Feb'23), with arena and amphitheater sales up double-digits. Remember that 1Q23 was a really strong quarter for the LYV, with revenue up 73.5% on a consolidated basis, and the performance through mid-Feb'23 is very encouraging as it shows that the business can still print mid-to-double digit growth rates. Moving past 1Q24, the comp set gets easier, and with the momentum so far, we should continue to see mid-single-digit ticket growth for FY24. I am pretty confident this is achievable given that event-related deferred revenue, a key leading indicator of future activity, was up 8% in 4Q23 to $2.9 billion (refer to supplement data provided by LYV). Moreover, LYV is expecting a strong show pipeline for FY24. Confirmed shows for large venues are up by a double-digit percentage, and roughly 65% of the expected show count is booked for large venues. This 65% is quite a big step up from the 50% over the last 2 years. In other words, there is fairly high visibility into FY24 ticket sales potential. I would also note that global ticketing fee-bearing gross transaction value is up a double-digit percentage to $13 billion for events in 2024, and Ticketmaster has signed 3 million net new enterprise tickets in January'24 so far.

Aside from concerts and tickets, LYV has also locked in a sizable amount of planned sponsorship for the full year (~75% accounted for as of mid-February), up a double-digit percentage vs. last year. Due to Ticketmaster's global digital platform, an increasing number of venues and festivals, and long-term monetization opportunities in Latin America and Asia, I think the demand coming from planned sponsorship is going to last for the long term. One key near-term catalyst that should boost sponsorship growth is the new Mastercard partnership.

With strong visibility and momentum coming into FY24, I believe it is safe to say for now that the topline is unlikely to disappoint. As for AOI growth, one thing that is important for readers to note is that revenue per attendee is likely to come down, and that's perfectly normal because of the growing mix towards amphitheater and arena. But AOI per attendee is going to shoot up because of huge fixed cost leverage (amphi and arena can hold more people, and there are more opportunities to monetize value-added products like beer, parking, etc.) This should lead to double-digit AOI growth, which was also mentioned by management during the call.

Regarding CAPEX, the fact that management has projected $540 million for FY24 is encouraging, in my opinion, because it indicates that the company is reaping good returns from its investment in Venue Nation. For reference, LYV's venue portfolio expanded to 373 venues as of FY23, up from 338 in FY22. While there is no major information about the actual unit economics so far, based on LYV's reported P&L, which shows improvement in margins, I would think that allocating capital to invest in Venue Nation's growth is a smart move.

As LYV steps up on expanding its portfolio of operated venues, it means more fixed costs are being embedded into the business. While this does improve profitability and control, it also means that if volume demand were to go down for any possible reason, like another pandemic, LYV would see high decremental margins, which is going to hurt its margin profile a lot more than in the past.

In conclusion, I am recommending a buy rating. The business showed excellent performance for FY23, exceeding my expectations. I expect the strong momentum to carry over into FY24, with multiple indicators pointing towards continued high single-digit growth. Ticket sales are pacing well ahead of last year, with a strong show pipeline and increasing sponsorship deals providing clear visibility into future performance. I am also positive about the investment strategy into operated venues, which should provide more margin growth potential and control.