batuhan toker/iStock via Getty Images

batuhan toker/iStock via Getty Images

LSI Industries (NASDAQ:LYTS) recently reported earnings. I wanted to take a look at the company's financial performance in the past and what it is going to do going forward. The company is positioned very well for growth with its Fast Forward initiative of reaching better sales numbers and efficiency. Furthermore, even with beaten-down estimates the company seems to be trading at a discount, therefore, I initiate my coverage of LSI with a buy rating.

The company has almost doubled its cash position from $1.8m to $3.5m, while reducing debt by around $6m during the same period from June 30th to September 30th '23. This is what I like to see in a company. The company still has a decent amount of debt for such a small company, around $25m, however, is it a problem? The way I assess if it is going to be a problem is by looking at the company's interest coverage ratio. As of Q1 '24, the interest coverage ratio stood at around 19x, meaning operating income, or EBIT, can cover annual interest expenses on debt 19 times. For reference, many analysts agree that an interest coverage of 2x is considered healthy. I don’t share the same views, as I would like to be a little more conservative and consider 5x to be much more comfortable because it allows for some bad years of performance. For example, when a company has a bad year in terms of sales, so it does not generate enough EBIT to cover interest expense on debt, if the coverage ratio stood at around 2x, then for that year it may look like the company is in trouble, whereas 5x ratio would allow for a higher margin of safety and even in the bad year, the company may still be able to pay the interest. So, with a coverage ratio of 19, it is safe to say the company is at no risk of insolvency anytime soon.

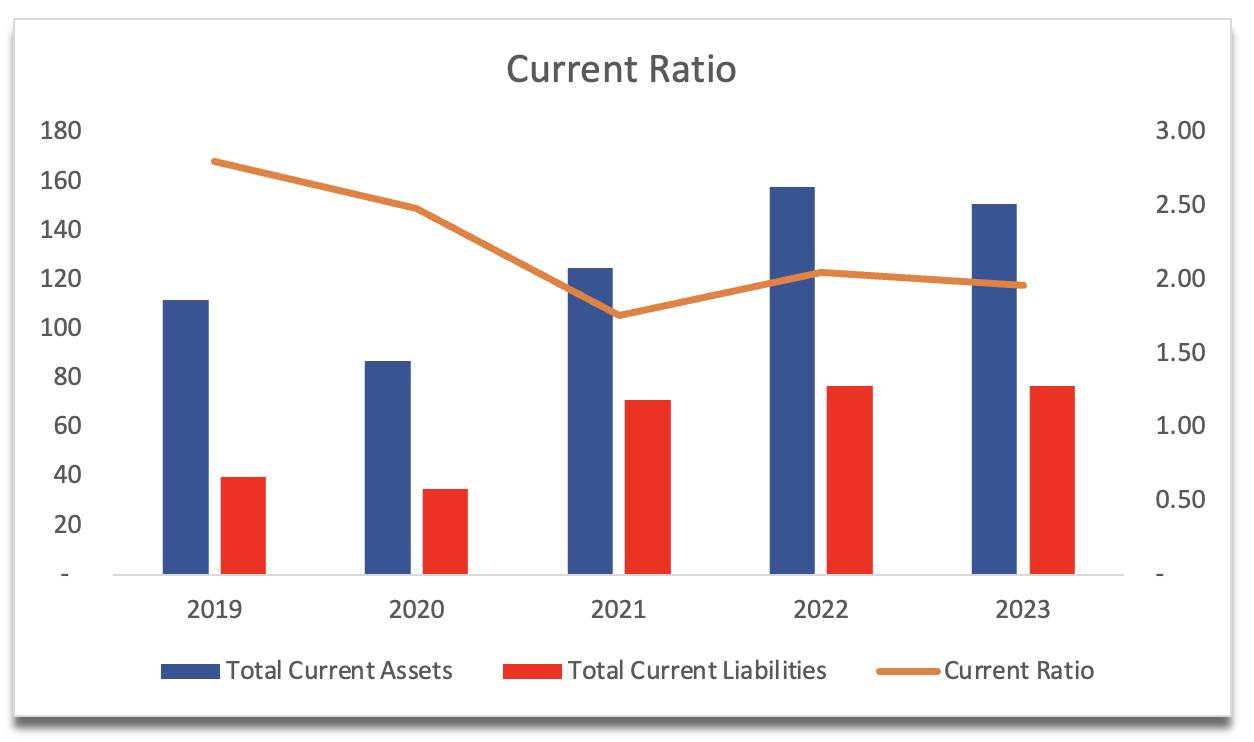

LSI's current ratio has been very healthy too over the years and is right at that range that I consider efficient, which is in the range of 1.5 to 2.0. In my opinion, this range is a good balance of having the ability to pay off short-term obligations and still have enough capital for further growth of the company. Anything over this range is a missed opportunity in my opinion and is not an efficient utilization of the company's assets. Therefore, I can safely say LYTS has no liquidity issues.

Current Ratio (Author )

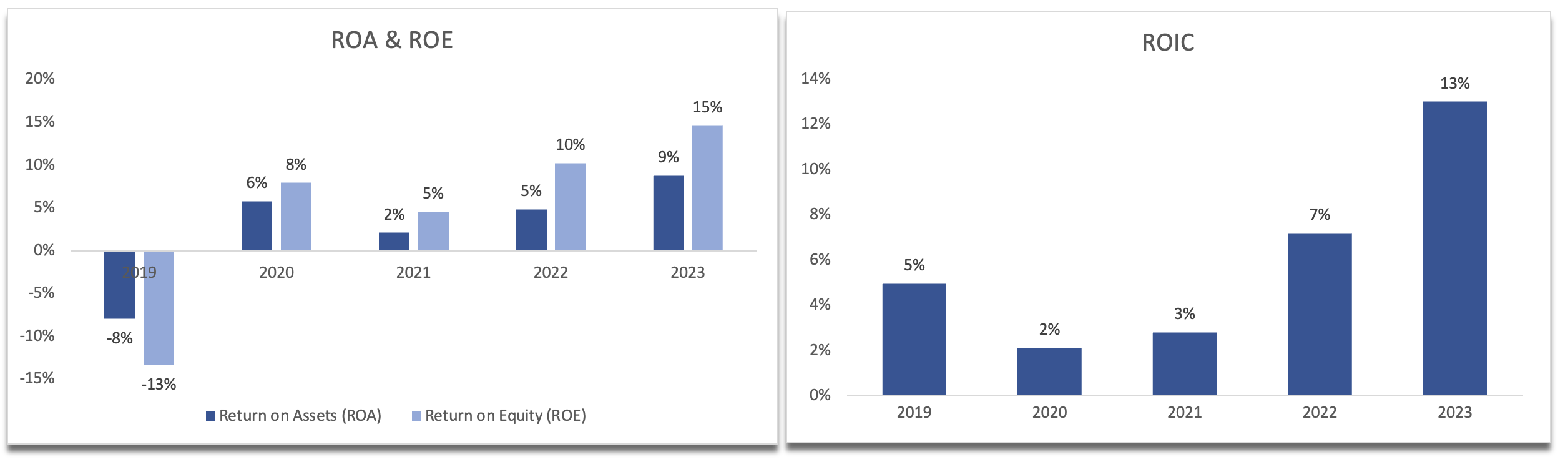

In terms of profitability and efficiency, the company's ROA and ROE have improved substantially in the last few years, to the point where these are quite decent, all of which can be attributed to the company's ability to improve margins and the bottom line. A similar trend can be observed in the company's return on invested capital, or ROIC, which has seen a steady uptrend since the bottom of the pandemic panic. The company has become more profitable and efficient in the last few years and the management is adept at using the capital available to invest in much more profitable projects, and I commend their efforts.

Profitability and Efficiency Metrics (Author)

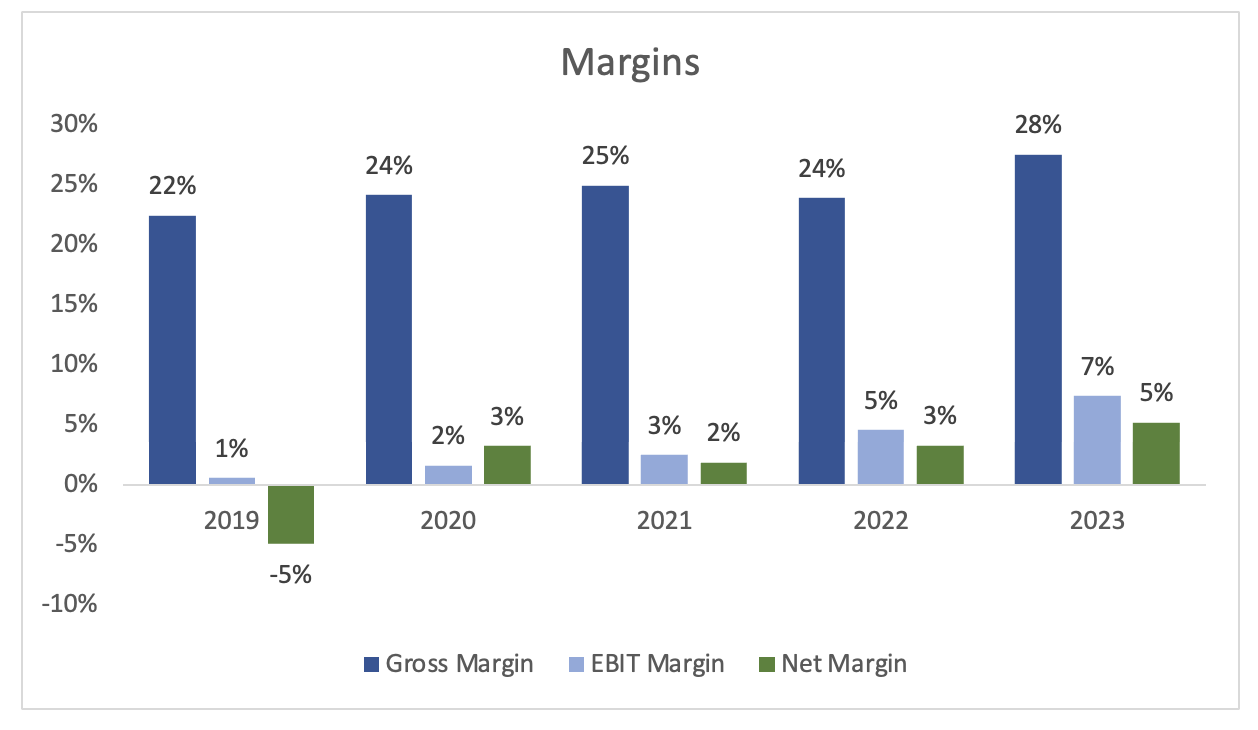

Speaking of margins, the company slowly but steadily managed to cut costs of production as its gross margins expanded around 600bps, or 6% in four years, which is not an easy task to do especially in such an industry.

Margins (Author)

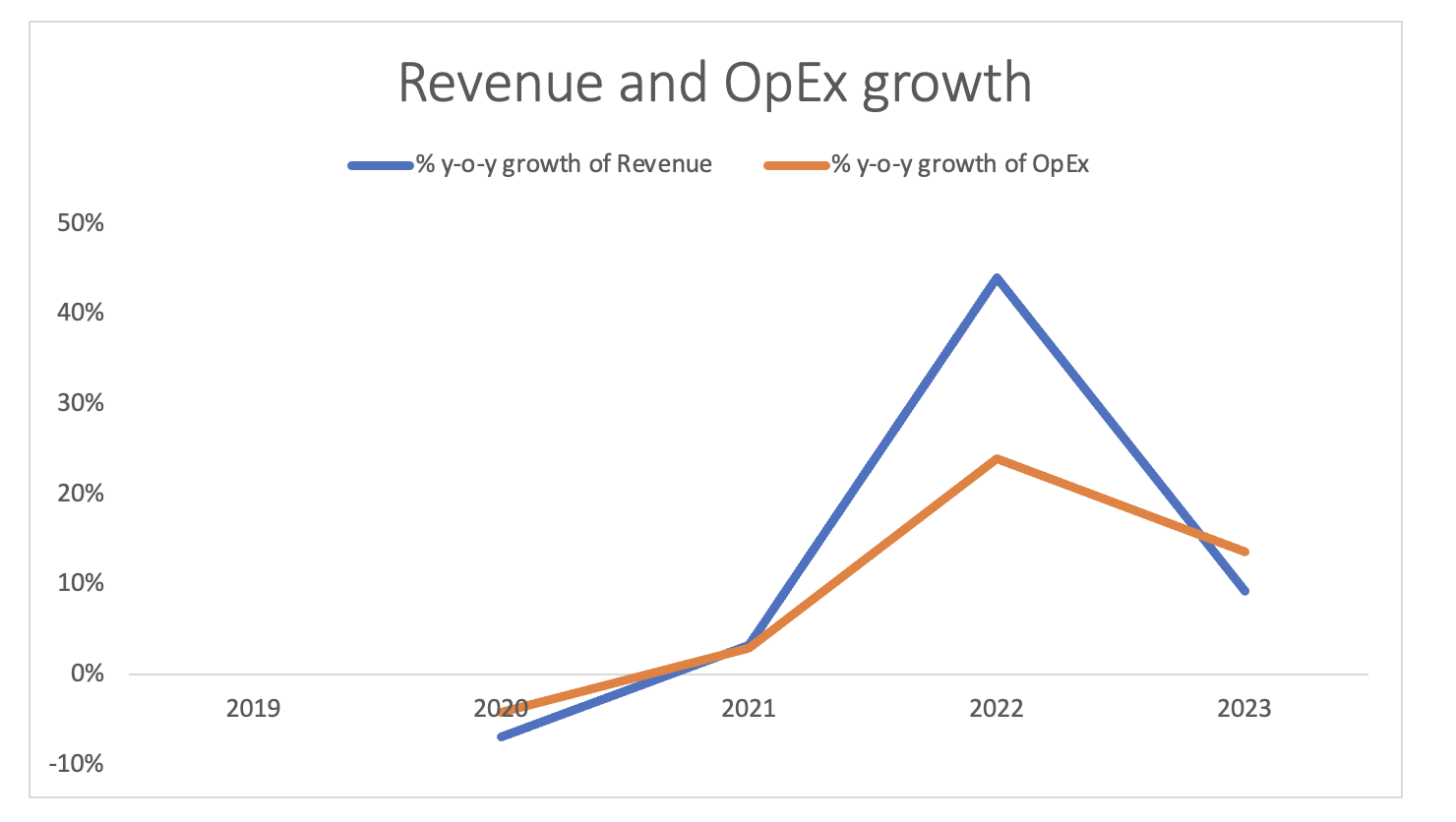

What's even more impressive is that the company managed to become profitable because it managed to control operating costs over the last few years to the point where OpEx increased by less than revenue growth, which can lead to sustained growth and profitability in the long run.

Revenue and OpEx growth (Author)

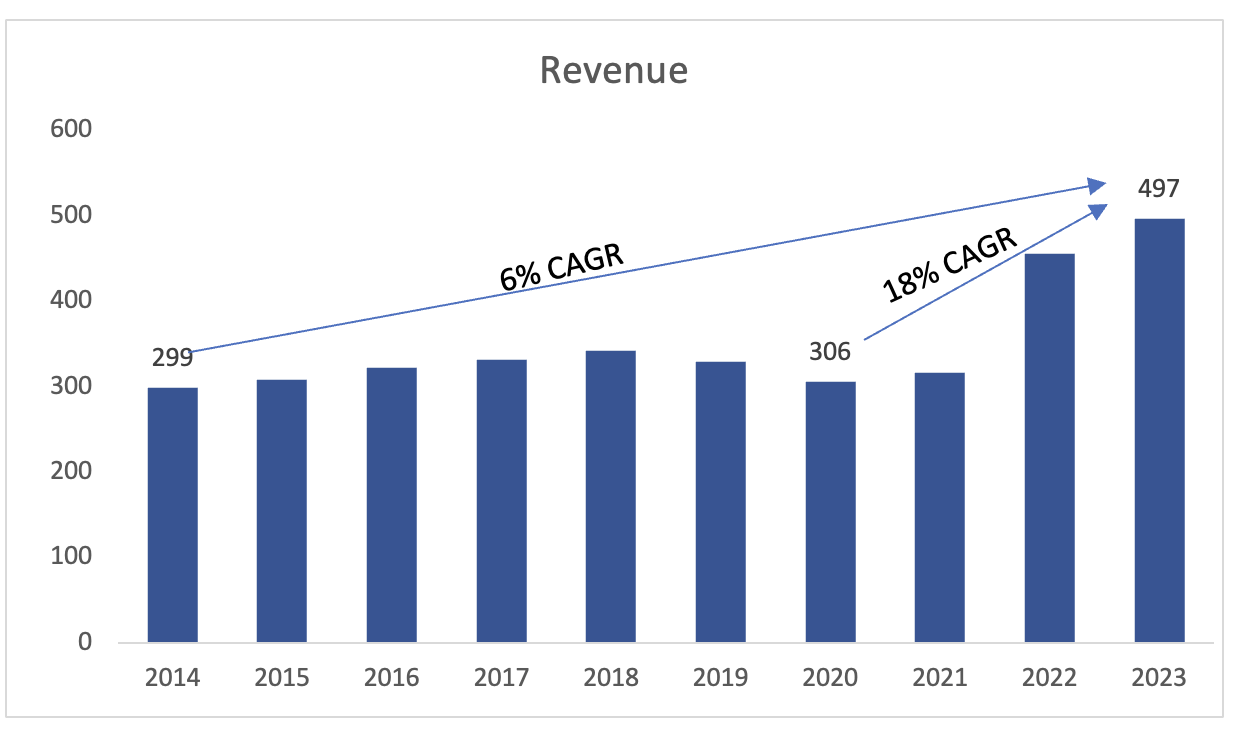

In terms of revenues, the company is not a high-growth tech company, only have achieved around 6% CAGR over the last decade. Will the company be able to achieve better performance going forward? Are there any catalysts in store? I will cover this in the later section, however, if we look at analysts' estimates, it is not looking particularly exciting. Furthermore, we cannot take these numbers too seriously since there aren’t many analysts covering this company on the Street. If we look at the last 3 years of performance, we can see that the company managed to achieve around 18% CAGR, driven by improved sales in the Lighting Segment, and a combination of improved organic sales of the Display Solutions and the acquisition of JSI Fixtures.

Historical Revenue Growth (Author)

Overall, the company has been doing very well in the last few years, driven by a good acquisition and management's ability to get the company to become profitable again. I would like to see more acquisitions in the future so that the company can grow its top line inorganically at least and not stagnate once again, as it did pre-FY20.

The biggest catalyst is the company's ambitious Fast Forward strategy. This plan seeks to expand the company's market share into new high-value verticals, improve the company's margins, and expand customer share within the current verticals of the company. The company aims to become an $800m net sales company by FY28, which is rather very ambitious considering how the company performed in the past. The past is not indicative of the future, as we can see that the company managed to achieve 18% CAGR in recent years, so it does look somewhat promising, and I will have to consider this when I'm constructing my valuation model.

With this strategy, if successful, the company may become a completely different company in the long run, and I'm sure this improvement will be reflected in appreciation of the stock price in the future. FY28 is still a long time from now, and there is a lot of uncertainty if the plan is going to be successful in the end.

So far, the company is trending in the right direction with the initiative, as margins, sales growth, and overall efficiency have been improving. I believe that the company is very likely to achieve this result. The reason is that, back at the beginning of 2021, the management had another ambitious plan. To become a $500m company by 2025. Fast forward to the company's fiscal 2023, it achieved $493m already, which is 2 years earlier than the plan's deadline. The company is going to lose some of that revenue by FY24, however, it will be right over that mark in the next year once again, and probably even further.

Besides this initiative, I do not see any other catalysts that could help the company achieve this goal in the next 5 years. Now we are going to play the waiting game and see how the plan evolves over the next year or two before we can judge its efficiency. So, let's look at what the numbers look like in the valuation section.

I decided to incorporate the management's ambitious plan into my model, however, with slight conservatism. In the base case, the company will just fall short of $800m in sales, just to give myself a little margin of safety. Below are my assumptions of revenues for the base, conservative, and optimistic cases.

Revenue Assumptions (Author)

In terms of margins and EPS, I modeled that the company will manage to improve gross margins further but only by very little around 400bps or 4% in the next decade while leaving operating margins stable over the period. Below are my assumptions for margins and EPS. I decided to be on the conservative side here because I wanted that extra little bit of margin of safety.

Margins and EPS Assumptions (Author)

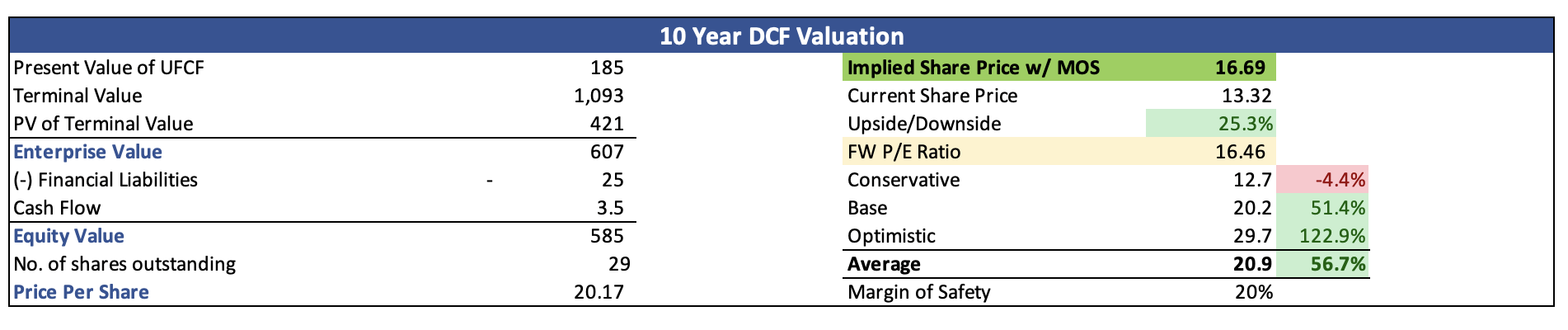

To be even more protected, I decided to go with a 10% discount instead of the company's WACC, which was around 7%. The company is slightly on the riskier side, being a small cap, so I thought I'd go with more risk management here. I also went with a 2.5 terminal growth rate. On top of these estimates, I added another 20% margin of safety to the final calculation just to have that sleep-well-at-night feeling when you buy a company at a deep discount to its fair value, and you know that the risk to the downside is minimized. With that said, LYTS's intrinsic value is $16.69 a share, meaning the company is trading at a discount to its fair value.

Intrinsic Value (Author)

The biggest risk is the company's ambitious plan that may underperform expectations. It is a very solid plan, but does the management have the ability to execute properly and reward shareholders in the long run? That remains to be seen, however, it is looking very promising given the company's ability to continue to expand margins every quarter.

The company operates in a very competitive environment, which means the company needs to be on top of innovation. If not able to, the company's products may become obsolete, and the competition will prevail and take the market share from LSI.

Price sensitivity is another risk that may affect the company's profits in the long run. Competition may try to undercut, which will force the company to match them, reducing sales.

Even with beaten-down estimates, the company seems to be on a discount and is a good buy, however, I am not sure how successful the Fast Forward plan will be, which poses the biggest risk to its future valuation. Nevertheless, I feel a lot safer knowing that I did approach the valuation with a conservative mindset, with plenty of adjustments to the margin of safety, therefore, I believe that the risk/reward here is rather enticing in the long run.

The management's ability to keep improving the company's efficiency and profitability will translate into long-term gains for the shareholders, and I am not ruling out that the company may perform very well relative to the overall stock market. I am going to open a small position to test the waters and see how the next quarter develops, after that, I will reassess to see whether I should add more or stay as it is and see how the share price evolves over the next year or two.