peepo

peepo

Following my coverage of Joby Aviation (NYSE:JOBY), for which I recommended a buy rating as the business was getting closer to commercialization, with a much clearer timeline of when it will start generating revenue, this post is to provide an update on my thoughts on the business and stock. I reiterate my buy rating for JOBY as execution on acquiring the necessary certificates continues to track well. Management also showed great foresight in acquiring the required certificates for offering aftermarket services, which I believe will have strong financial impacts over the long term. To accelerate the pace of adoption, JOBY has also pushed forward the electrification efforts in its key targeted cities.

While the share price has been volatile, I ask readers to focus on what matters for JOBY: its path toward commercialization, which has been progressing well. Just one day before the 4Q23 results on February 22, 2024, JOBY announced that it had completed the third of five stages of the FAA type certification process, making it the first eVTOL aircraft developer to do so. Stage three is crucial because it's when JOBY lays out its certification plans for the whole plane, including its electrical, structural, and mechanical systems, as well as how it will handle cybersecurity, human factors, and noise. The Federal Aviation Administration [FAA] has now examined and approved all of these certification plans. The implication of passing the 3rd stage is that JOBY is now able to submit test plans and begin testing across every area of its aircraft program - in other words, JOBY can now test the entire aircraft itself to show the FAA that it works as a whole. I view this progress very positively, as it (1) paves the way for commercialization and (2) dismisses concerns raised by investors regarding the change in the planned certification plan for electric vertical take-off and landing [eVTOL] aircraft. For background, Under 21.17a certification, US companies could have benefited from an easier route by using the current Part 23 aircraft certification regulations. However, there would have been additional uncertainty if the certification is under 21.17b, as eVTOL aircraft must be certified as "powered lift". While I am not a technical expert on this front, I take the end result as a positive sign that JOBY is on the right track, since the FAA has accepted the certification plan for its propulsion system.

The FAA really sets the standards and defines exactly what that is at the component level, at the system level, and at the aircraft level, which is really how you have to progress towards your certification and Stage 4 organization.

If you have not done that, there's no point in having that discussion with the FAA. And with the team now at the point where we close on all of Stage 3 and are working and submitting test plans on Stage 4 is exactly where we want to be. 4Q23 earnings results call

Apart from the core certification, I thought it was very positive to see that management is already thinking far ahead, setting the stage for more revenue streams by acquiring the necessary certificates today, which I take as further signs of great execution ability. Specifically, the FAA has granted JOBY its Part 145 Repair Station Certificate, allowing the company to carry out certain aircraft maintenance tasks. This is a significant milestone on the road to bringing Joby's electric air taxi service to a commercial scale. Once Joby's eVTOL aircraft is certified for commercial operations, it will be able to perform maintenance, repair, and overhaul [MRO] services thanks to the FAA Part 145 Certificate. I anticipate this will have a massive impact in the long run as eVTOL adoption increases, even though it will have little impact in the early years of commercialization (because there aren't many eVTOLs on the market). Also, since JOBY is a leading player on this front, it will also have a strong competitive advantage (against players that enter later) in terms of operating experience (compounded with its core business as an eVTOL operator). On the P&L, this will also reduce the volatility of revenue and earnings given that aftermarket services are more likely to occur once there is a large enough customer base.

One additional thing I would like to highlight that further highlights management foresight is their proactive steps in building up the underlying infrastructure for more eVTOL adoption. In January, JOBY announced multiple signed agreements with various entities to push forward the electrification progress in California and New York:

Looking ahead, management guided a higher 2024 cash spend of $440 million to $470 million, as JOBY will ramp aircraft builds, expand its Marina facility, begin work on the Dayton facility, and hire additional staff to support certification and manufacturing. This amount should not be a major concern, as JOBY still has $1 billion of cash sitting on the balance sheet.

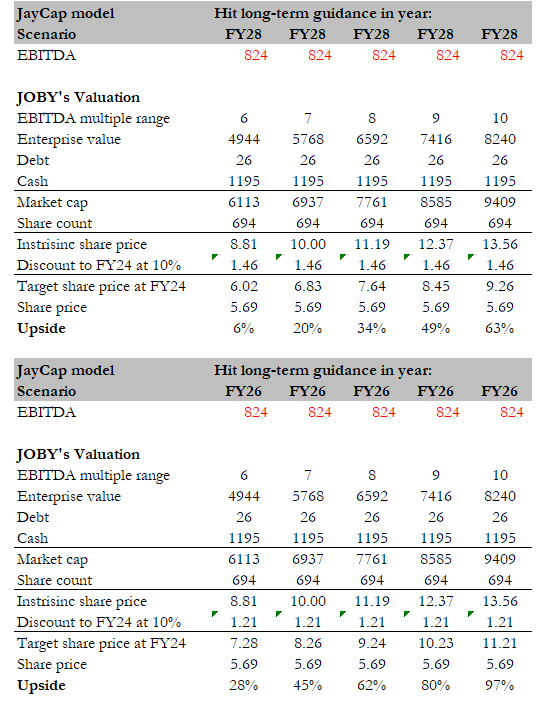

Own calculation

My opinion on how to value JOBY is still to use management long-term guidance as a baseline (I used this method in all my previous posts). Adjusting for the timeframe and current share price, I still think the upside is very attractive, even if JOBY were to achieve its EBITDA target 2 years later than what it guided for (in FY26). In my previous models, I have mainly used Lyft (LYFT) as a comparable for my exit multiple assumptions. I have widened the peer set to include OEM players like Boeing and Airbus (similar types of vehicles), and now that JOBY is going to offer aftermarket service, I have included Safran. Since these players are a lot more mature, it makes it easier to benchmark what multiples JOBY could trade at. Currently, these players trade in the low to mid-teens forward EBITDA range. Applying a huge discount, to be conservative, I assumed JOBY to trade below the low end of peers' multiple range (Airbus trading at 10x forward EBITDA). Then, I apply the same scenario analysis, assuming a range of multiples between 6 and 10x (using LYFT's lowest forward EBITDA of 6x as a benchmark for the low end).

JOBY

Since JOBY is getting closer to commercialization, I think the key risk for the near term is execution. JOBY needs to continue this positive track record of execution, and if any mishaps were to happen, it would not only impact sentiment but also add additional risk to the balance sheet. Remember that JOBY only has ~2 years of cash burn left; if they mess up FY24, they are likely to raise capital to ensure they don't get into a liquidity crisis in FY25.

I maintain a buy rating for JOBY as the company progresses positively toward commercialization, achieving key milestones in the FAA certification process and acquiring additional certificates for aftermarket services. The completion of the third stage of FAA certification is a significant step, allowing JOBY to initiate testing across all aspects of its aircraft program. Regarding balance sheet, despite expected increased 2024 cash spend, JOBY's $1 billion cash reserve provides a comfortable cushion.