PotaeRin/iStock via Getty Images

Editor's note: Seeking Alpha is proud to welcome contangoX as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

PotaeRin/iStock via Getty Images

I am initiating a Buy on Lamb Weston (NYSE:LW) as the company stands to benefit from a return in volume growth in Q4 with the aid of higher margin businesses. I believe volume growth will be driven by a return in restaurant traffic as interest rates decline later in the year. The decline in current quarter volumes is based on management's decision to exit lower margin businesses, so I think when volumes return with the higher margin businesses later this fiscal year, the company will benefit and become more profitable.

LW is a leading producer of frozen potato products and is headquartered in Eagle, Idaho. They have a strong market presence, being ranked #1 in North America and #2 globally for frozen potato products. Driven by a global supply chain with 27 factories in Europe, North America, Asia, and South America and 3 new factories under construction. Since 2017 they have increased headcount by 58% to over 10,000 employees and grown sales 9% compound.

In 2023 LW acquired the remaining interest in their European joint venture, which added 1,500 new colleagues, six processing facilities and nearly 2 billion pounds of capacity. The business integration is well underway, and this strategic transaction strengthens LW's capabilities to serve customers.

They also acquired a controlling interest in their joint venture in Argentina, and broke ground on a 250-million-pound capacity expansion, which will improve their ability to serve the growing South American market.

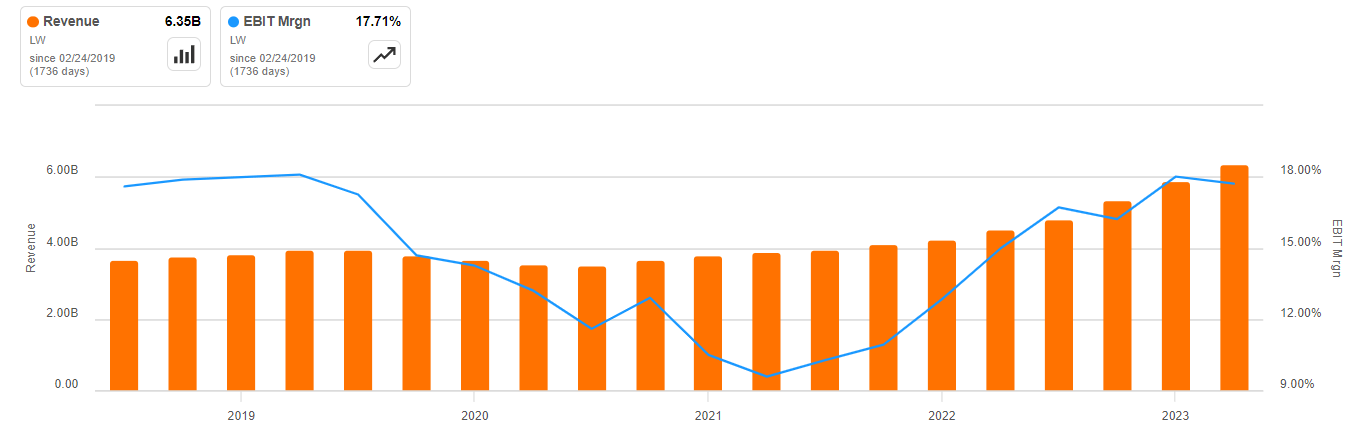

I think the income statement is strong, sales have grown 11.96% CAGR since 2018 in contrast to an industry median of 6.79%, bolstered by organic growth and strategic acquisitions. Gross Margins have rebounded, rapidly increasing from the lows of 2022, and have now reached record highs of 27%, driven by improved price/mix dynamics. Consequently, there has been a noteworthy 700 basis point move up in EBIT Margins, despite operating overheads gradually trending up since 2017.

seeking alpha

As it stands, I think the balance sheet could be stronger. After the acquisitions, the cash balance rests at $80 million, with upcoming principal payments of $80 million in December 2024 and $280 million in April 2025. That being said, I think there is a low risk of default, Net Margins are over 10%, and I think the recent crash in Free Cash Flow is due to the extra working capital and capex taken on from the two acquisitions. I believe they should normalize, and I think it will benefit cash flow going forward.

I can see that the company's capital structure has changed over the past 7 years, debt has increased 37% to $3.25 billion, but looking in terms of net debt to sales, financial leverage has declined, falling from over 70% to 55% in the latest fiscal year. Currently, the company holds the 7th highest financial leverage in the industry, and I think this high level of leverage has been instrumental in maximizing returns, especially considering the company's string of prosperous years.

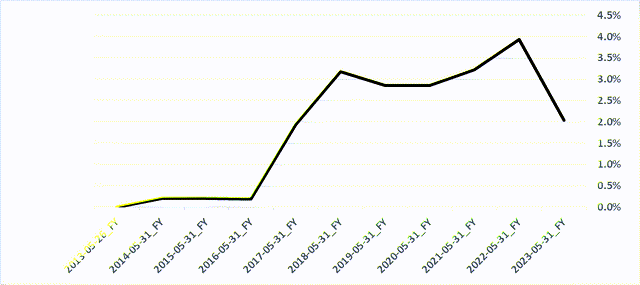

I think the rise in interest rates has led to an increase in the interest expense ratio, reaching 4% of sales in 2022. However, I think due to the two business combinations resulting from the previous joint ventures, the ratio has subsequently decreased to 2%. In my opinion, the increase in interest expense has put pressure on net margins and will continue to do so until interest rates decline later this year.

Source: Author's calculations

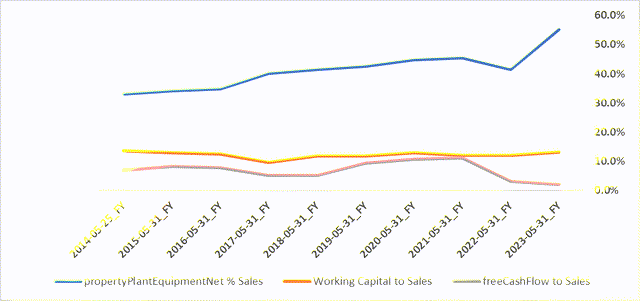

After both acquisitions and being a packaged food manufacturer the business has become more capital intensive, PPE to sales now stands at 55%, marking a significant increase from the prior year's 41%. In my view, this alongside the increase in Working Capital has pushed Free Cash Flow Negative in recent quarters, causing the valuation multiple to increase substantially. Between 2017 and 2021 the average Free Cash Flow ratio was 8.2%, but this has declined to 2% in the latest fiscal year due to what I believe is more capex and to a lesser extent more working capital.

Going forward, I expect Free Cash Flow to increase back to the historical average as Net Margins are forecast to increase and the incremental change in fixed assets and working capital returns to normal.

Source: Author's calculations

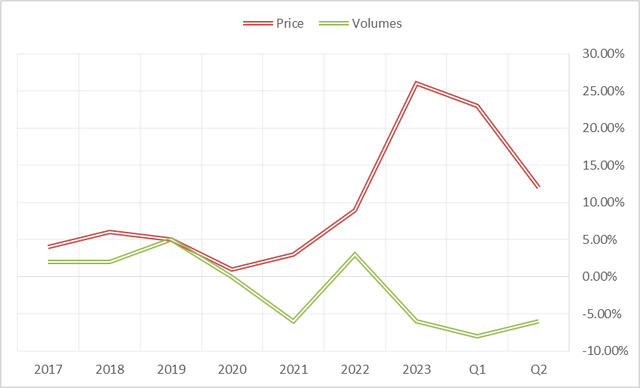

In the second quarter, LW delivered record sales, reflecting the consolidation of their EMEA business with robust price growth. Top line grew 32% to $1,732 million, excluding the acquisition, sales grew 6% which is slightly below the 10-year compound rate of 7.4%. In North America sales increased 12% driven by a 14% increase in prices offset by a -4% decline in volumes. Adjusted EBITDA margins came in lower due to writing off excess potato's, I think that charge should reverse next year resulting in an expansion in NA Adjusted EBITDA margins as I believe the company is going to apply similar price increases in 2024.

I think the surge in organic sales is linked to an improved price/mix in recent years. Inflation in the food sector witnessed a significant spike throughout 2021 and 2022, and I think LW passed this inflation on to consumers. While volumes have dropped and continue to contract, I believe a substantial portion of that is management's decision to exit lower margin businesses and to a lesser degree softening restaurant traffic.

I think management's decision to exit those businesses is welcome because Gross Margins are not as competitive as other metrics relative to the sector. In my view, this strategic move demonstrates that management are addressing one of the only areas where this company doesn't rank exceptionally in terms of profitability.

Source: Author's calculations

There are two reasons why I think volumes have declined, the first is management's decision to exit lower margin businesses and the second reason is because of softening restaurant traffic. Going forward I see volumes recovering, in fiscal Q2 volumes dropped -6%, an improvement on fiscal Q1's -8%, if this trend continues, I see volumes recovering and growing in fiscal Q4. Also, with interest rate cuts now expected in June, I think restaurant traffic should pick up in the second half of the year. I think this positive momentum suggests a favourable trajectory and recovery in demand, indicating a more optimistic outlook for the company in upcoming quarters.

I also believe prices should hold up in mid-single digits in the second half of the year as the company laps the effects of the previous year's pricing actions.

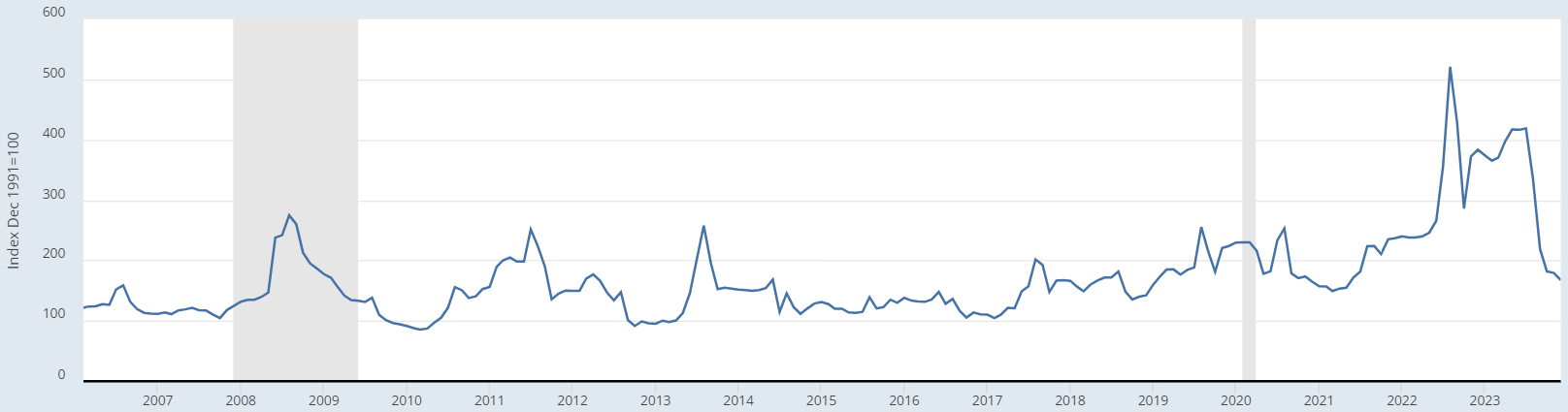

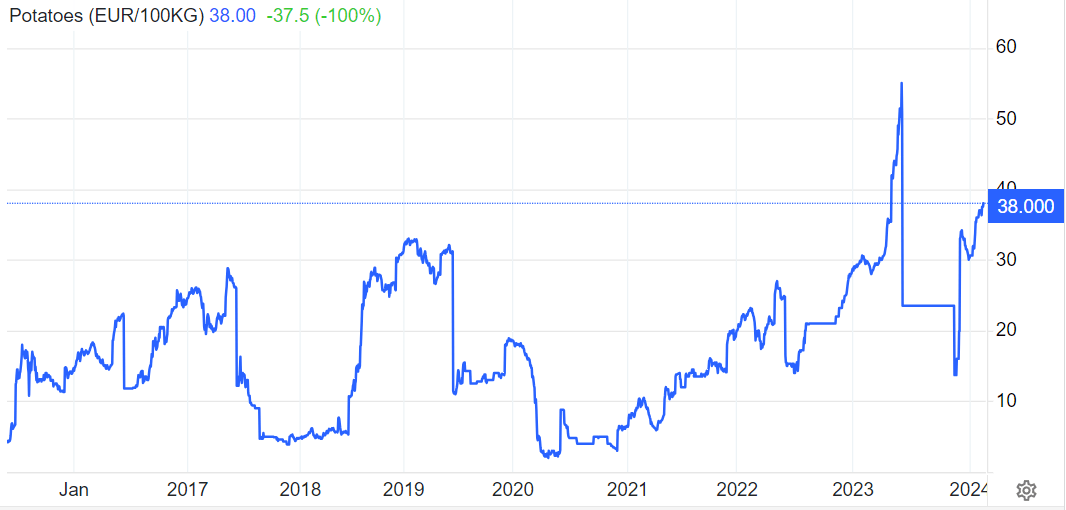

I think the charts below display two contrasting pictures, in the US Russet potato's prices have fallen back below 2020 levels, meanwhile in Europe they have fallen from the highs of 2023 but have continued up since calendar Q4 2023. In my view this will impact different parts of the business, internationally I think more price increases will occur, and in the US, I think prices will moderate, but we could see profits expand further as raw material costs have declined.

Russet potato price (FRED St Louis) Potato price chart (EUR) (Trading Economics)

In my opinion restaurant traffic at casual dining and full service remain soft, and the near term is expected to be choppy, the Restaurant index contracted -0.3% in December and remains in contraction territory due to a tougher economic climate. But I think with interest rate cuts forecast as early as June, we could see restaurant traffic begin to increase later in the year.

Source: Author's calculations

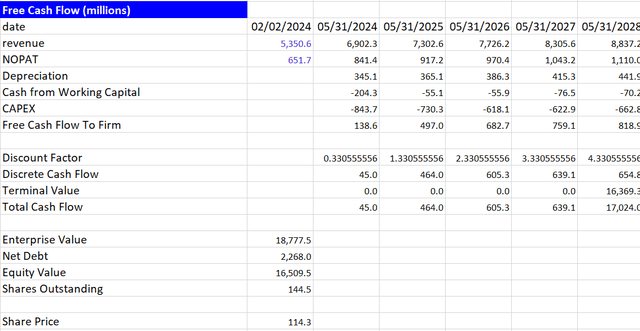

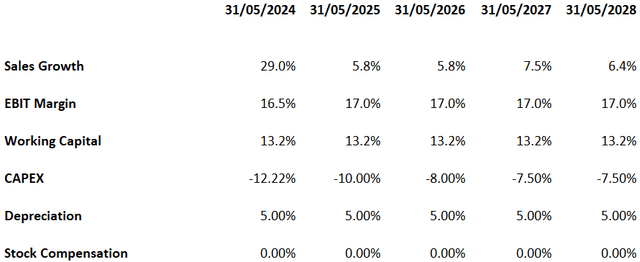

Modelled using the P/CF multiple of 25x, I have sales reaching $8.8 billion by 2028 and a price target of $114 which is an upside of 10% from today's price. The assumptions used include an expansion of EBIT margins to 17% as the company exits lower margin businesses and carries on benefiting from pricing, a higher level of capex due to the assets taken on from the acquisition and the expansion of the Argentinean operations which reverts to the long run average of 5% by 2027.

Using the perpetuity method with the same assumptions, we get a share price target of $141. This is with a terminal growth assumption of 2% which is at the lower bound of the 2%-4% range.

Assumptions

Source: Author's calculations

In Q3 I expect more moderate pricing as the company laps the effects of last year's pricing actions. I also think volumes will decline somewhere in the range of 0% to -5%, but management commentary will be optimistic around future volume growth. The higher margin businesses should drive more profitability for the business, and in the longer term we should see EBIT Margins top 18%.

Currently, the trailing PE Ratio is near all-time lows because of the increase in profitability. Expectations are that profits will continue to grow, but I think the risk is that volumes don't return, and profits begin to contract. I believe this will occur if there is a further deterioration in restaurant traffic due to higher for longer interest rates or management have been too optimistic in future guidance.

Also, I think the up-trending SG&A Margins coupled with a fall in volumes could put significant pressure on profit margins. I don't think costs are out of control, but they are increasing as a percent of revenue. If volumes fail to recover in the later stages of this year, I think that could spell trouble for the company and I would downgrade my outlook.

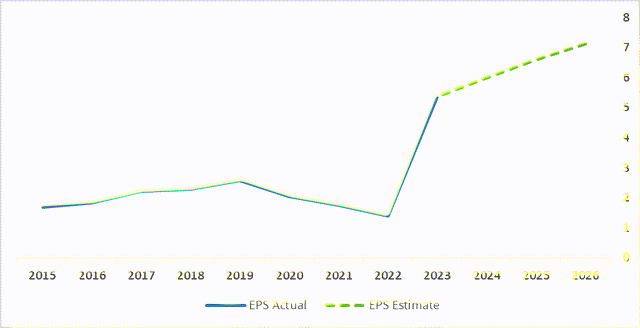

Earnings per share (seeking alpha data)

I rate LW a Buy, the valuation points to a potential 34% upside when using the perpetuity approach, and the acquisitions strengthen LW's supply chain. While there is a risk the ongoing softening of restaurant traffic will affect volumes, I think the consumer backdrop remains stable and gross profits will expand.