Motortion/iStock via Getty Images

Motortion/iStock via Getty Images

With U.S. inflation recently accelerating from already intolerable rates, the American economy currently needs Jerome Powell to assume a strict "paternal" role as Chairman of the Federal Reserve.

In modern parlance, Powell needs to step up and become a real "daddy." I am not talking about one of those post-modern permissive push-over "dads," - i.e., the type of persons that set few or no absolute rules and that only inconsistently enforce ad hoc orders. What the U.S. economy desperately needs right now is an old-school and prototypical "daddy." I am talking about the sort of person that sets absolute, no-exception rules that are engraved into their children's brains, and that nobody dares to test because they absolutely know what they will have coming.

In this article, I will explain why the U.S. currently needs its Federal Reserve Chairman to become a real "daddy," and specifically what this would entail. If we get anything less than that on Wednesday, then investors had better start making preparations for the possibility of another big surge in inflation during the second half of 2024.

In 2022, when the market participants were betting heavily on a Fed Policy "pivot," and financial conditions eased substantially in the midst of an inflation surge, Chairman Powell came out aggressively in a series of public statements and slammed down those dovish expectations.

That "strict" and "disciplinarian" version of Chairman Powell has been conspicuously absent during the past few months. And this is giving rise to a major problem for the U.S. economy. Stocks and bonds fell and financial conditions tightened - just as Powell had intended.

Now, fast forward to late 2023. As soon as the Fed started to publicly ruminate about the timing of interest rate cuts, the market promptly went wild, pricing in 125 basis points of Fed cuts in 2024, starting in March of 2024. The problem is that this market reaction directly contradicted the Fed's Survey of Economic Projections (SEP) which anticipated only 75 basis points of Fed cuts, starting in the second half of 2024.

Like when a parent gives an inch and their child takes a mile, as soon as the Fed showed the slightest hint of (conditionally and gradually) tapering its monetary policy, financial markets participants proceeded to make an absolute mockery of the Fed's putatively "restrictive" monetary policy to combat inflation.

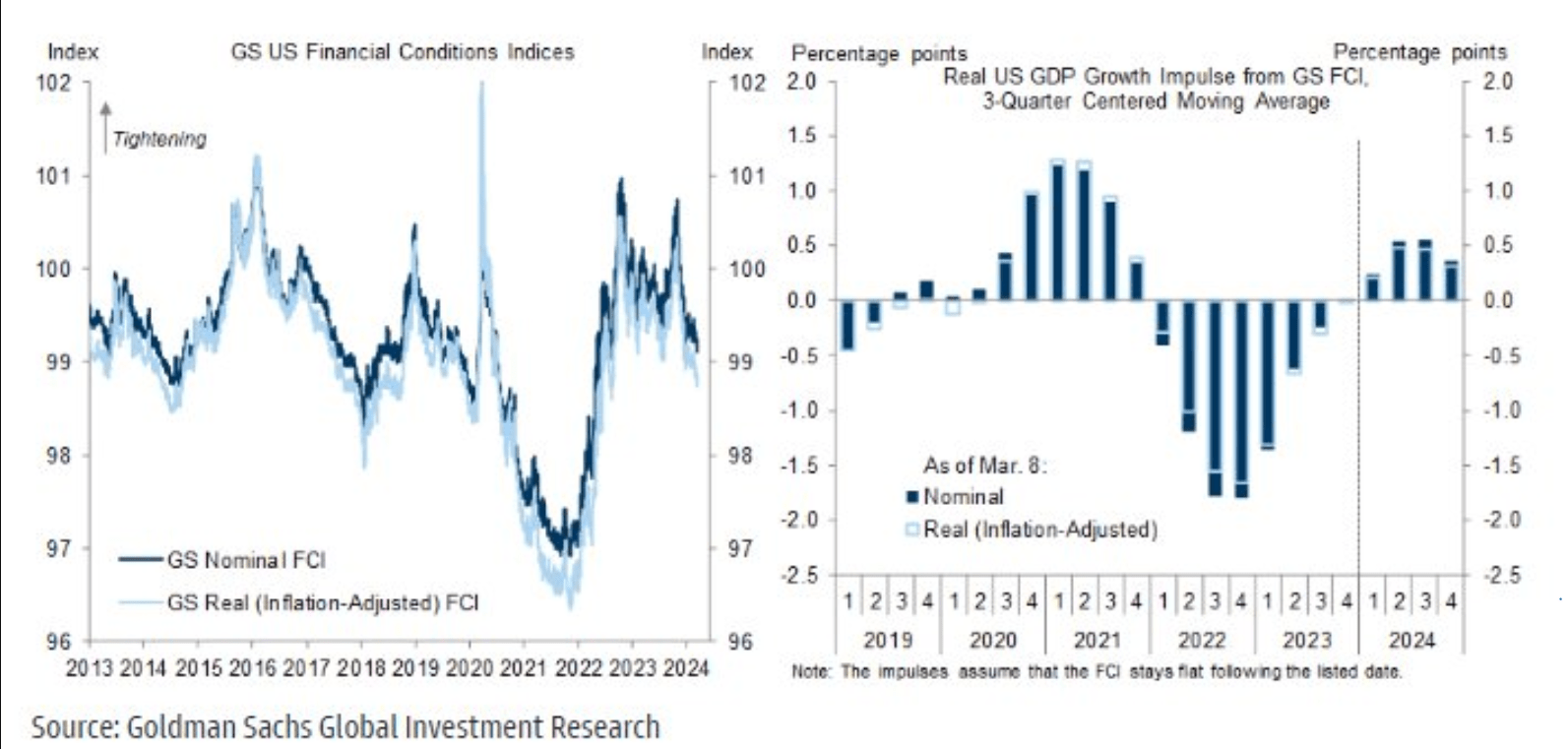

Broad financial conditions, according to the Goldman Sachs Financial Conditions Index, as well as the Fed's own FCI-G model, went from being substantially restrictive during the first three quarters of 2023 to very accommodative currently - in a record amount of time. Indeed, the easing of financial conditions that has occurred in the past few months has been almost unprecedented, with financial conditions now looser than they have been at any time since August 2022, according to the Goldman model. According to both the Fed and Goldman models, the current looseness of financial conditions is stimulating aggregate demand at a rate of approximately 0.5% of GDP.

Godman Sachs Financial Conditions Index (Goldman Sachs)

A different set of Financial Condition Index models constructed by the Chicago Fed shows that U.S. financial conditions are currently easier than at any time since February 2022.

Under current conditions of extremely tight labor and capital resource utilization, this looseness of financial conditions poses extreme risks in terms of inflation.

So, where the heck is Daddy? Why is he letting financial conditions ease so much, thereby greatly increasing inflation risk?

It is very hard to square the extraordinary loosening of financial conditions in the U.S. since October 2023 with Chairman Powell's public statements. Not only has the Fed Funds futures market grossly overshot the Fed's SEP estimates of the Fed Funds rate, market action more generally, in bond and equity markets, has made a mockery of Powell's repeated statements that if inflation did not decelerate as anticipated, that the Fed could choose to raise rates.

One can speculate endlessly on what Powell has been thinking and why he has reacted (or failed to react) the way he has. In this regard, it is important to remember that he is the leader of a large committee of people with disparate views. It is probably a good bet that he has chosen to remain silent due to the inclination of many members of the FOMC to lower rates, ideally before the election, in order to try to pull off a "soft landing," for the U.S. economy. I don't interpret this desire of many FOMC members to enable a soft landing as being overly "partisan"; I see this desire as very understandable under any circumstances.

However, with the worrisome uptick in inflation in CPI and PPI in the last couple of months, the inflation outlook has changed substantially relative to what it has been since October. Most importantly, the extraordinary easing of financial conditions during the last few months poses an unambiguously clear and present inflationary threat to the US economy.

Core Services Ex Housing CPI - i.e., supercore - is running at a 3-month annualized rate of +6.40%. This represents an acceleration relative to the already extremely high 6-month annualized rate of +5.78%. This rate of supercore inflation, and its acceleration, is blatantly incompatible with the Fed's stated 2.0% inflation target. If the Fed fails to address this problem quickly and aggressively, the Fed will lose credibility and long-term inflation expectations will rise more than they already have since the last CPI report.

Powell has to act, and he has to act now.

Powell's basic task is very clear. First and foremost, he needs to unambiguously reassert the Fed's commitment to getting inflation down to 2.0% on a sustained basis. In order to make this commitment credible, Powell must deliver a significant "shock" to financial markets which causes a substantial tightening of financial conditions that is consistent with the Fed's stated objective.

There are many ways that Powell could deliver such a "shock." Here is how I would do it:

All of this is consistent with Powell's previous public statements, so there will be no loss of credibility. Powell simply needs to say that the 2.0% objective has never changed. Furthermore, the Fed's next move was always going to be data-dependent. Indeed, Chairman Powell can credibly claim that the only thing that has changed in the last two months is the inflation data.

Core Goods prices are currently in deflation. Unlike prior Fed speculations, such deflation is clearly transitory and unsustainable. Therefore, on an ongoing basis, this deflation in core goods is currently masking the risk of high inflation in the U.S. economy in the intermediate term. If Core Services Ex Housing were to merely remain stuck at the current rate of inflation of around +5.0% to +6.0%, an acceleration of Core Goods prices from their current deflation of -1.50% on a 6-month annualized basis, to a more normal rate of +1.0% to +2.0%, would cause overall core CPI to explode, rising extremely far above the Fed's overall target of 2.0% core inflation to somewhere around the 4.0% range.

Even more concerning that this is the fact that with such a high rate of inflation, the U.S. economy will be extremely vulnerable to an exogenous inflationary shock, such as the supply-chain shock caused by the Ukraine war or the oil price shock of 2022. As explained in more detail in this article, given that the inertial force of inflation will already be quite strong, and inflation expectations would be significantly un-anchored, any exogenous inflationary shock would quickly cause the rate of U.S. inflation to challenge or even surpass the peak CPI All-Items inflation rate of 9.0% reached in 2022. Indeed, given that services inflation would be moving off of a much higher base, core CPI could rather easily exceed the peak reached in 2022.

The problem with this risk scenario is the following: In 2022, when the Fed was forced to respond to the inflationary shock, the Fed Funds rate was moving up from 0% and QT was draining liquidity from extremely high levels. If the Fed is forced to respond to another inflationary shock, the Fed could be forced to raise the Fed Funds rate from the current 5.25%-5.5% range (a 23-year high) to somewhere in the 10% range. Furthermore, QT has brought overall liquidity down from extremely high levels to levels not much higher than they were pre-COVID. Any acceleration of QT from the current point would have a much more pronounced negative impact on the economy than it has had in the past couple of years.

Therefore, an exogenous inflationary shock that forced the Fed to substantially tighten monetary policy along the lines just described would have a disastrous impact on the U.S. economy. The U.S. economy will certainly crash if interest rates rise to anywhere near 10% and if there is any substantial contraction of liquidity from current levels. Indeed, in the context of a recessionary shock, a major tightening of financial conditions could unleash a major financial crisis.

In sum, the urgency to bring inflation down and re-anchor inflation expectations is not due to the idea that high inflation is inevitable; it is that the U.S. economy is currently highly vulnerable to an inflationary shock.

Of course, nobody knows if such a shock is forthcoming. The point is that, under current conditions, the Fed has a duty to protect the American people from the risk of such a disastrous shock. The issue is one of risk control. The Fed needs to tighten up financial conditions now, even if it risks a minor recession, in order to drastically diminish the risk of another major round of inflation that could have devastating consequences for the economy.

America needs the Chairman of the Federal Reserve to step up and be a daddy.

Chairman Powell needs to announce extremely strict expectations regarding the path of inflation. Furthermore, he needs to clearly communicate what the consequences will be if inflation does not behave in accordance with the Fed's projected path.

In my view, Chairman Powell needs to state unambiguously that the Fed will not cut interest rates nor taper QT until overall and core inflation are down to 2.0% and super-core is decelerating rapidly below 3.0%. In addition, the Fed needs to warn the market that if overall inflation or core services ex housing inflation accelerate any more from their current rates, the Fed will move swiftly to raise the Fed Funds rate and take any additional necessary steps to get inflation moving in accordance with the Fed's projected path.

So, will Chairman Powell step up and be Daddy? I don't pretend to know. What I do know is that if he does not, investors need to start preparing for the possibility of a very dangerous inflation shock in the second half of 2024.