lucigerma/iStock via Getty Images

lucigerma/iStock via Getty Images

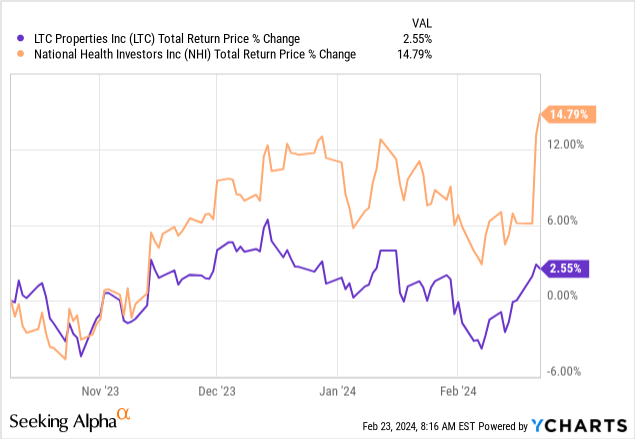

On our last coverage of LTC, we examined the fundamentals after Q3-2023 and admitted that we were a tad too bearish on the REIT. It had survived, if not thrived, and there were reasons to believe it was coming out on the other side of pandemic induced stresses. That said, we deferred to (NHI) as our choice in the sector and made no bones about it.

NHI has the same multiple as LTC and we prefer it here for a couple of reasons. The first being that it is a larger firm with an investment grade credit rating. Both the fixed charge coverage and net debt to EBITDA are also far superior. So if we had to pick one here it would be NHI. LTC remains a hold but we have to acknowledge that the firm has done far better than what we anticipated.

Source: Seeking Alpha

Now that turned out to be one our better calls as NHI just blew away LTC since then.

We examine the setup post Q4-2023 results from LTC and tell you where we would look to pick up this laggard.

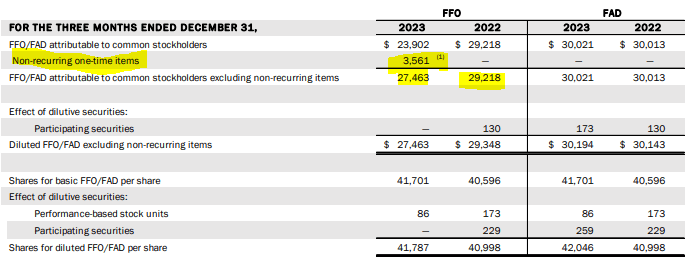

Q4-2023 was one of LTC's most active quarters in years. There were asset sales, new lease agreements and transfers of properties to new operators. The end result was the funds from operations (FFO) came in substantially lower than Q4-2022. It was lower, even if you excluded the rather large write-off of $3.561 million.

LTC Q4-2023 Presentation

This right off was associated with 10 properties that LTC had to move away from an operator they deemed unworthy.

LTC Q4-2023 Presentation

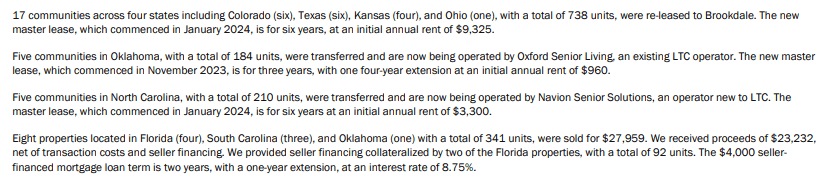

The full details of the capital transactions that took place in Q4-2023 can be seen in the 10-K, but the snapshot below shows just how incredibly busy things were.

LTC Q4-2023 Presentation

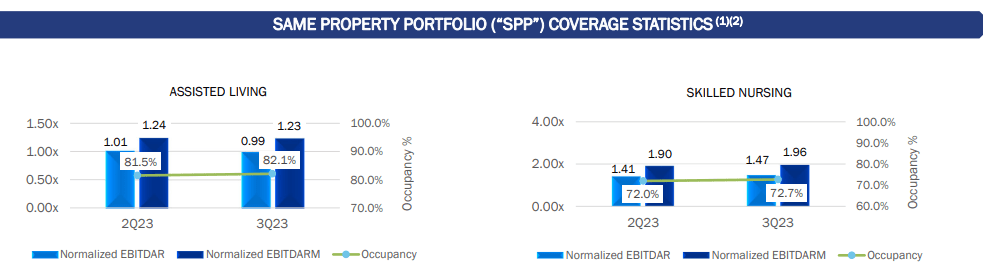

Through all of this, LTC has achieved some improvement in its key metrics for rent coverage. Here by rent coverage, we mean the ability of its tenants in skilled nursing segment to pay rent.

LTC Q4-2023 Presentation

Assisted living still looks poor, but since this is a trailing 12 month metric, we expect improvements in the quarters ahead as occupancy has ticked up.

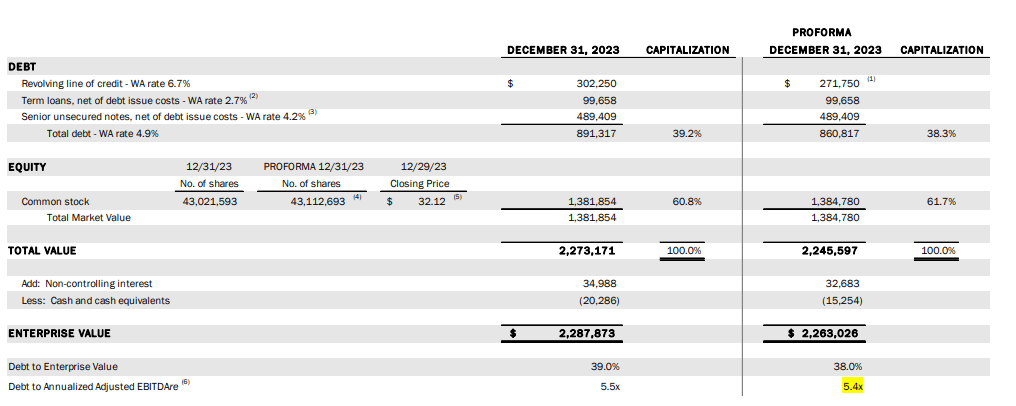

If you recall, in our last work we were a bit uncomfortable with the leverage for LTC. LTC seems to have read that and worked hard to get it down. There was a lot of stock issuance during the quarter.

Source: Q4-2023 LTC Earnings Press Release

There was a little bit subsequent to the quarter as well.

Source: Q4-2023 LTC Earnings Press Release

That got LTC down to 5.4X alongside the asset sales that were done during Q4-2023.

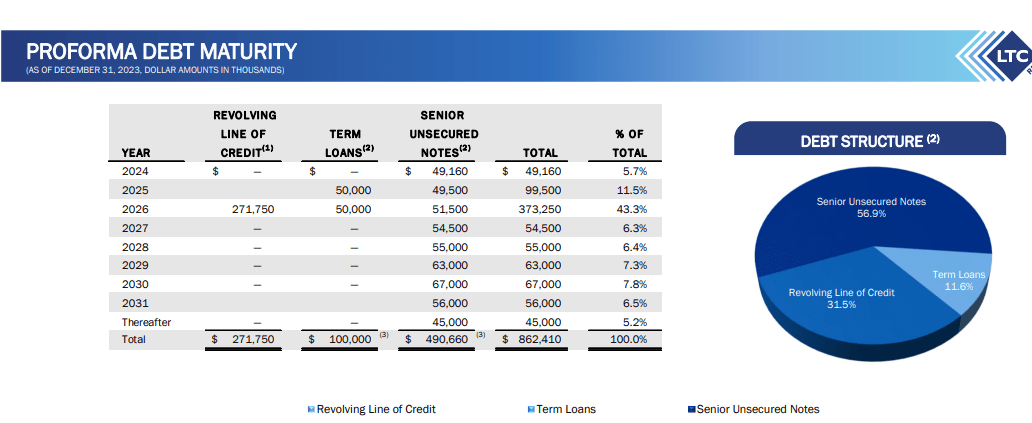

LTC Q4-2023 Presentation

This leaves LTC in a far better position to deal with further stresses in their portfolio.

LTC Q4-2023 Presentation

And there always are stresses as most tenants have extremely poor rent coverage. When those properties get transitioned, rent drops and it has a hard time climbing back to previous levels. Below we can see one brief discussion on the conference call about a property that was paying $14 million in rent, going to $8 million. The rent will move up, but likely not get back anywhere near $14 million.

Michael Carroll

And then, how are those assets performing? I know that they took over those, was it early 2023 when they took those over? I guess how have they recovered since they've been operating them?

Clint Malin

It was in '21 after they took over. Occupancy has been fairly flat, but they've improved. Labor agency utilization has gone down. So cash flow has improved but occupancy has been a little bit flat. So that's really where we see the potential for growth is occupancy gains.

Michael Carroll

Okay. And I know that I mean, I guess, SEC's contractual rent was significantly higher. I mean, when you kind of set a new rate, is it going to be closer to that $14 million, $15 million run rate? Or is it going to be closer to this $8 million run rate?

Clint Malin

Somewhere in between. I don't think you're going to get all the way back to the 14 and 8.

Source: LTC Q4-2023 Press Release

You are seeing this in the guidance for Q1-2024 and the analyst estimates for 2024.

Seeking Alpha

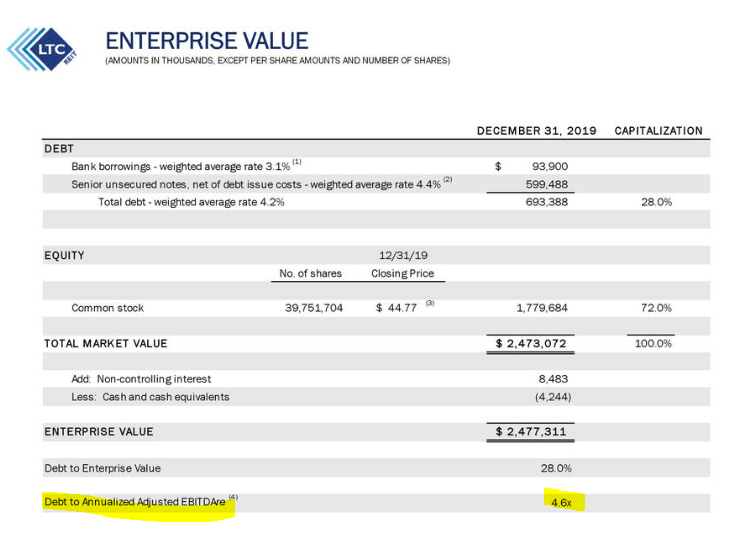

LTC was running at a $3.00 plus annual clip in 2019. So 5 years later, despite built in lease escalators and running higher net debt to EBITDA, we are below that.

LTC Q4-2023 Presentation

Yes interest rates are higher but LTC had plenty of opportunities to go all fixed rate and did not do it. So you have to be careful here in just assuming that you got a growing FFO stream that is safe. At present, the monthly dividend looks well covered. 17 cents a month is still well below the expected FFO. The leverage has also been taken down and most of the risky transitions are behind us. Occupancy is rising in senior homes. The construction drought coupled with aging population should be a tailwind here. We think the dividend looks safe for at least the 12 months and possibly beyond. The stock is still not very cheap. At around 12X FFO, you are paying about in line with what you would pay for Omega Healthcare Investors, Inc. (OHI) or NHI. Both those run lower leverage metrics and give you an investment grade metric to tap credit markets should the occasion call for it. We think the most you can pay for this is around 10X FFO and we would look to buy if we saw $27.00 per share.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.