15703083

Editor's note: Seeking Alpha is proud to welcome Lorenzo Micheletti as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

15703083

Liberty SiriusXM (NASDAQ:LSXMA) has a market capitalization of 9.71 billion and 326.58 million outstanding shares. In recent years, it has demonstrated strong financial results. The company is capable of generating value and managing its debt, and as we'll see, it is highly proactive in terms of its strategy.

One of the interesting aspects Liberty SiriusXM is that it owns the Formula One Group, which oversees the F1 races.

I believe there's a chance for some growth in the future due to multiple factors that I will analyze in this article.

The first thing we need to understand is how the company's business works. Liberty Media operates by acquiring interests in various media, communications, and entertainment businesses. They form partnerships within these sectors and generate content through their subsidiaries. They then sell the broadcast rights to various broadcasters worldwide. Their revenue comes from these sales and from advertising and sponsorship deals. While they own the rights to the content, they typically do not directly stream the events to consumers. Instead, they allow other broadcasters to handle the distribution of the content. Therefore, it will be crucial for the company to apply a differentiation strategy to the content it decides to broadcast

Liberty Media controls 2 major groups and has a significative interest in a third:

In addition to that the company also control Braves Group that indirectly owns the Atlanta Braves Major League Baseball club and the associated mixed-use development project, The Battery Atlanta.

SiriusXM Group is the oldest company held by Liberty Media. It operates in North America, providing satellite radio and online radio services. Its revenue streams are primarily based on advertising and subscriptions. F1 Group is a more recent addition, having been founded in 2016. Despite its relative youth, it's experiencing rapid growth and is becoming increasingly influential in the company's performance year after year.

Let me clarify that Liberty Media Corporation has a 6.5 billion investment in Liberty Live Group. However, this investment does not confer control over the company but just an interest.

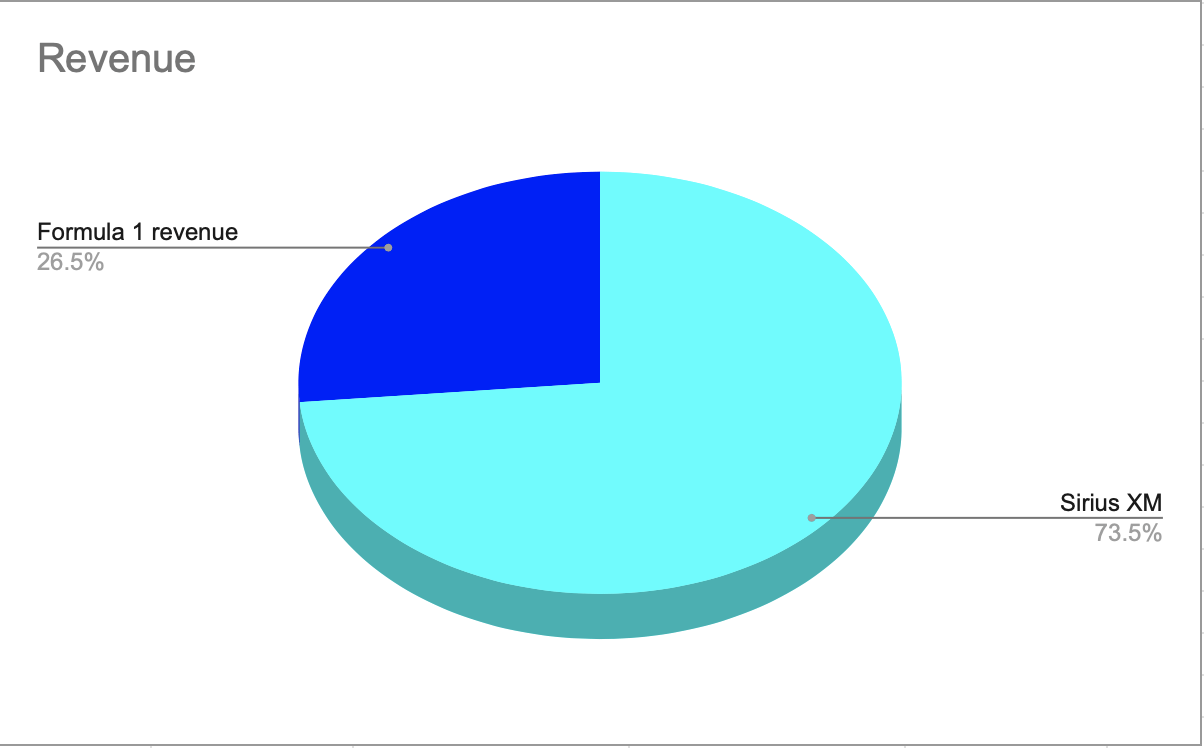

This is why in the consolidated financial statements of Liberty Media Corporation, the revenues from Liberty Live Group are accounted using the equity method. This means that these revenues are not directly included in Liberty Media's consolidated income statement and any internal transactions between Liberty Media and Liberty Live Group are eliminated to avoid double-counting. So in the next pie chart I'll consider just the F1 group's revenues and the Sirius XM's revenues.

Major divisions by revenue ( Author's calculation)

In 2023 the F1 Group contributes revenues of over 3 billion, while SiriusXM has generated almost 9 billion in revenues. For the sake of completeness, the Liberty Live Group has generated more than 11 billion in revenues. However, we must remember that these revenues do not contribute to the total revenue of Liberty Media Corporation.

An important point I want to focus on is, as I mentioned in the overview, that the company is proactive in its strategy. It has recently acquired Quint, a fact that has been commented on by the CEO, Greg Maffei:

Quint is a great addition to Liberty Media, extending our reach in premium experiences and capitalizing on continued growth in the global experiential economy.

What I appreciate about this company is its focus on expanding the variety of events it wants to stream, as well as its desire to increase efficiency in the ticketing distribution ecosystem - an interesting move that could boost sales in the next year.

Another element that in my opinion could positively affect the company in 2024 is the enforcement of anti-piracy measures. In the United States, the Protecting Lawful Streaming Act of 2020 aimed to block pirate broadcasting services, creating a more secure environment for companies operating in the media broadcasting services.

In 2024, I'm expecting an even stronger enforcement against piracy. I say this because global trends show an increase in the level of punishment for those who consume streaming media illegally. For example, in Italy, the government recently decided to apply a fine not only to pirate broadcasters but also to people who watch the content.

Liberty SiriusXM could potentially benefit from this scenario. For instance, stronger anti-piracy measures could lead to an increase in subscription and advertising revenue for legitimate broadcasters. Secondly, the value of broadcasting rights, which are crucial for a streaming company, could increase significantly.

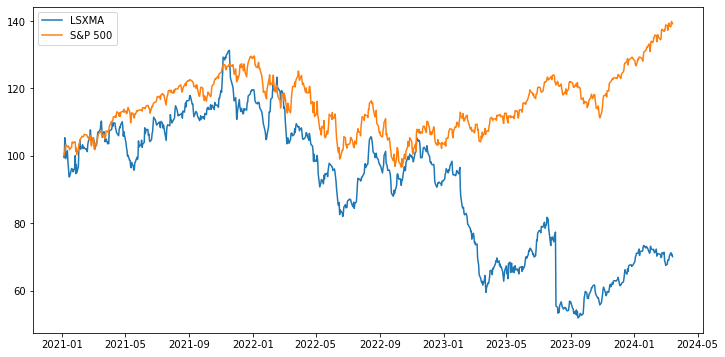

Now let's focus on the evolution of the stock price from 2021 to 2024 compared to the evolution in the same period of the S&P500, both of the time series are transformed in BASE100.

Liberty media vs S&P (2021 to 2024) (yfinance python library)

From the plot, we can observe that the highest price was reached in the latter part of 2021, which, in my opinion, was due to COVID-19. In fact, during that period, the popularity of streaming services increased significantly. Following that, we see a period of decline. However, our focus will now shift to what I believe will happen to the price in the near future.

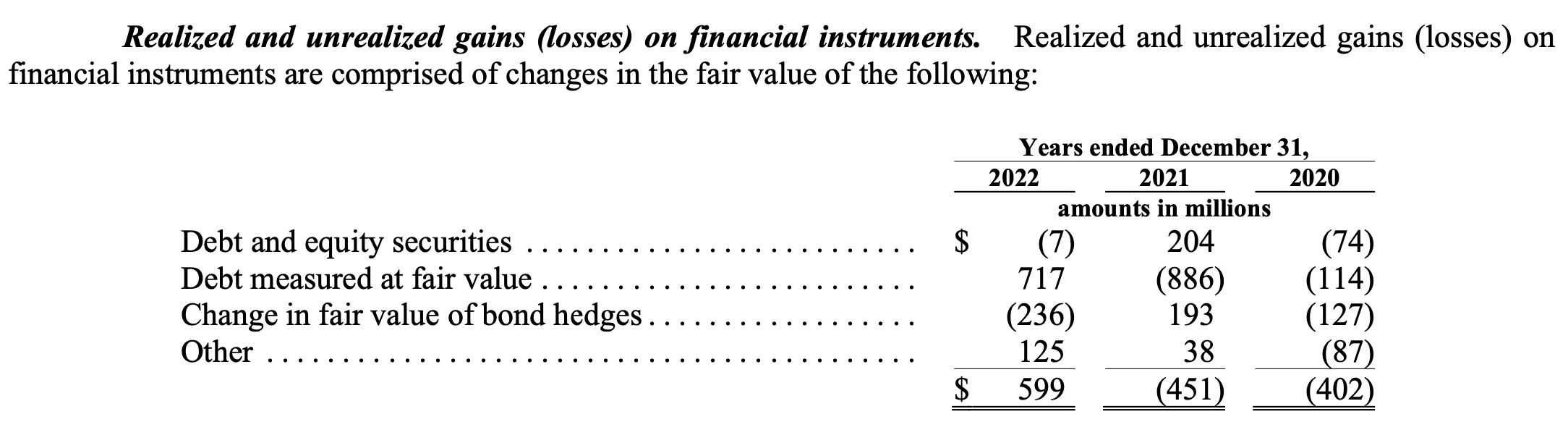

When I firstly observed the accounting information of this company I noticed an interesting fact, the company has a pretty high non-operating revenue and eventually losses. So I assume that the company has some financial investment that are not strictly related to its operating activity but that they have an effect on the company profitability.

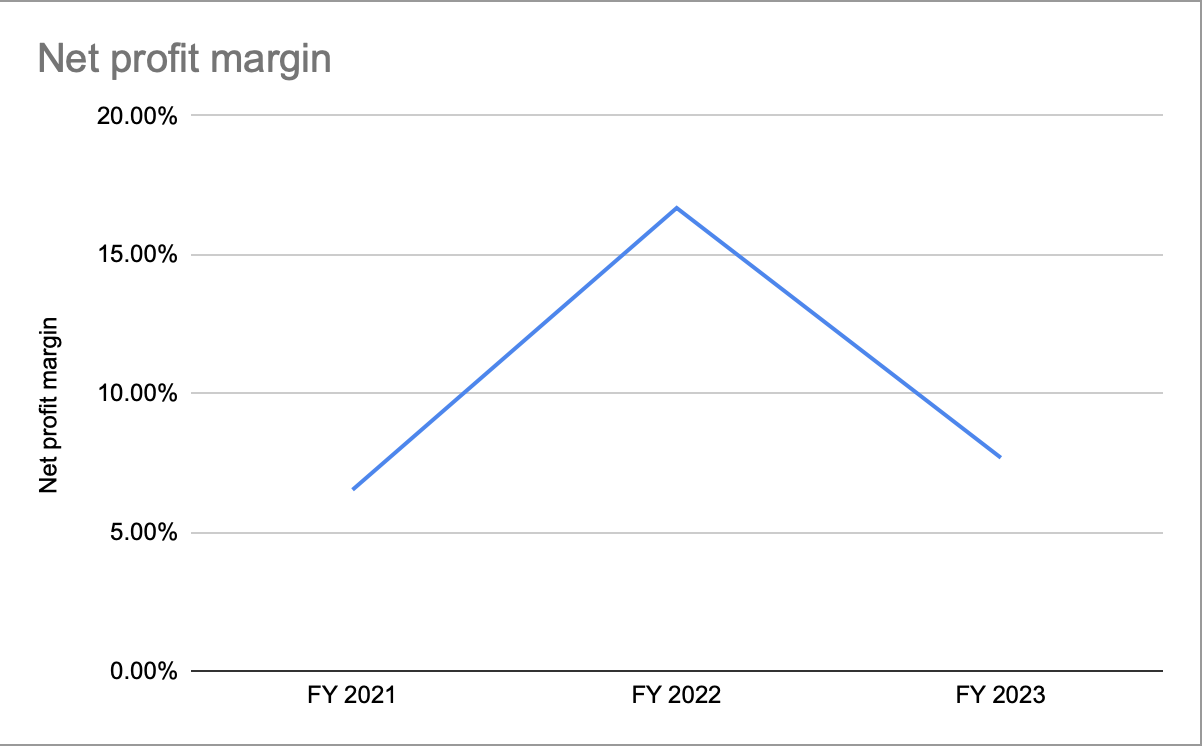

Net Profit Margin ( Author's calculation)

As we can see from the plot, the profitability of Liberty Media peaked in 2022. To evaluate this performance, I compared it with the average profitability of the sector and found that in 2023, the average profitability in the communication and media sector was around 12%. However, when considering some peer competitors of the company, I found that some were operating at a loss, while others were more profitable. This suggests a high variance in the profitability of this sector, which I believe is to be expected. It's challenging to compare these companies since their results depend on a variety of different factors.

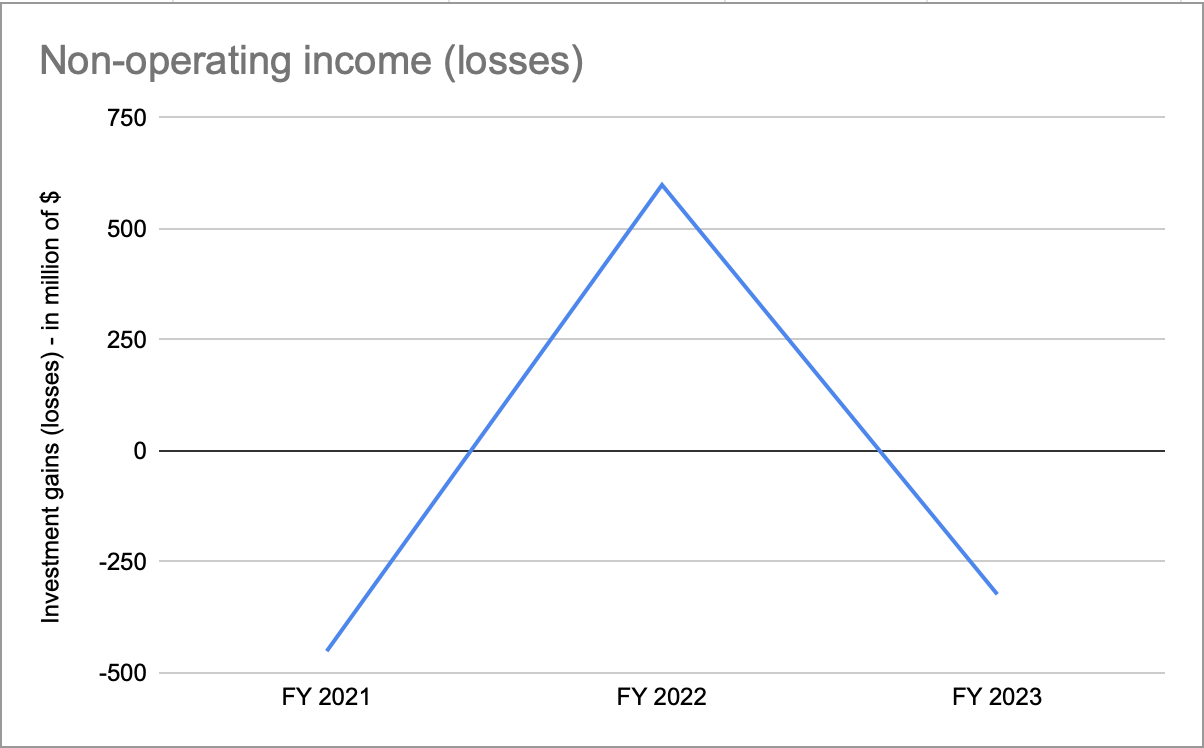

But now lets return back to the non-operating income of Liberty Media:

Non-operating income ( Author's calculation)

In 2022, when profitability was at its peak, we observed that the non-operating income was strongly positive. However, in 2023, the non-operating income turned negative, and profitability was lower. This raises a small red flag for me because a company's profitability should not be partially dependent on its non-operating activities.

Non-Operating financial investments (Company financial report)

From the financial report of the company, we can see that the non-operating income (or losses) is predominantly due to investments in financial instruments, such as Debt and Equity securities. Liberty Media may invest in equity and debt securities for diversification and income generation. These investments can provide strategic advantages, such as capital appreciation and liquidity management while the downside is that the company might register some losses from the use of these instruments, as they are exposed to market risk.

Looking ahead to 2024, I would like to see this company rely more on its core business for results. I am confident that with the anticipated increase in services and events that the company will broadcast, this goal can be achieved.

Even though the company tends to rely on its non-operating activities, it's noteworthy that the profits remained positive during periods of negative non-operating results. Although slightly below average of the sector, the consistent positive profitability, in my view, highlight the company's solidity.

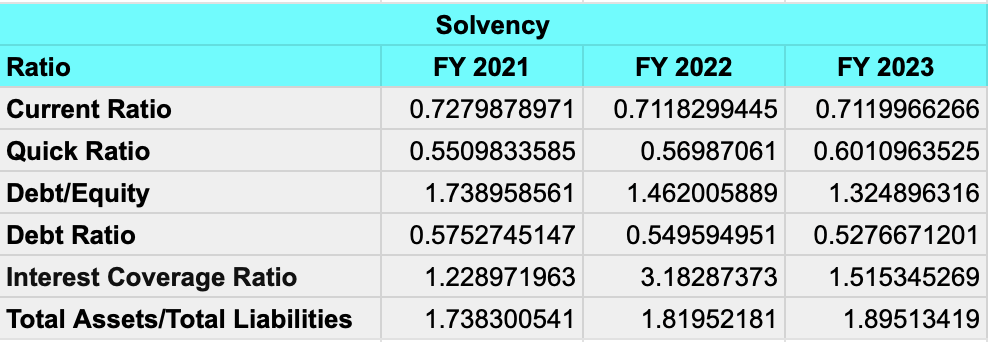

Another red flag regard the ability of the company to manage its short term debt:

Solvency analysis ( Author's calculation)

As we can see, both the current and quick ratios have low values. A current ratio less than one shows that the company has more short-term liabilities than current assets, suggesting potential short-term pressures and difficulties in meeting its obligations.

The reason for this, I believe, is related to market in which the company operates. Unlike a manufacturing company, where revenue streams are more predictable in the short term, Liberty Media's revenues are tied to intangible goods. These depend on factors such as the number of people following an F1 championship or listening to the radio or the revenues coming from the advertising. Based on this, I hypothesize that it's normal for the company to face some uncertainty in its short-term revenue streams, which translates into difficulties in managing short-term obligations.

In the long term the solvency values are good. The company has sufficient long-term assets to cover its debt.

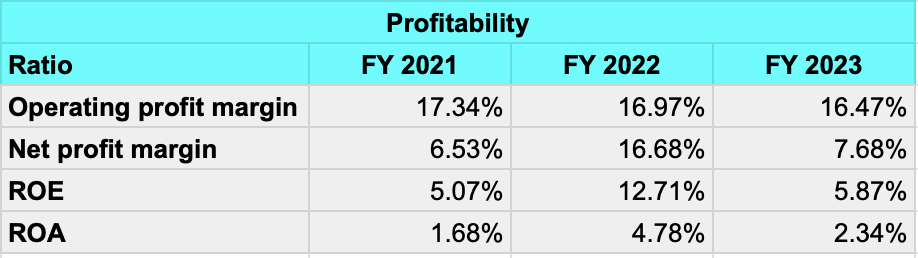

Upon analyzing the company's profitability, we observe that the company exhibits positive values in both Return on Equity (ROE) and Return on Assets (ROA). These positive outcomes are indicative of the consistent profitability that the company achieves year after year, as I mentioned earlier.

Profitability ( Author's calculation)

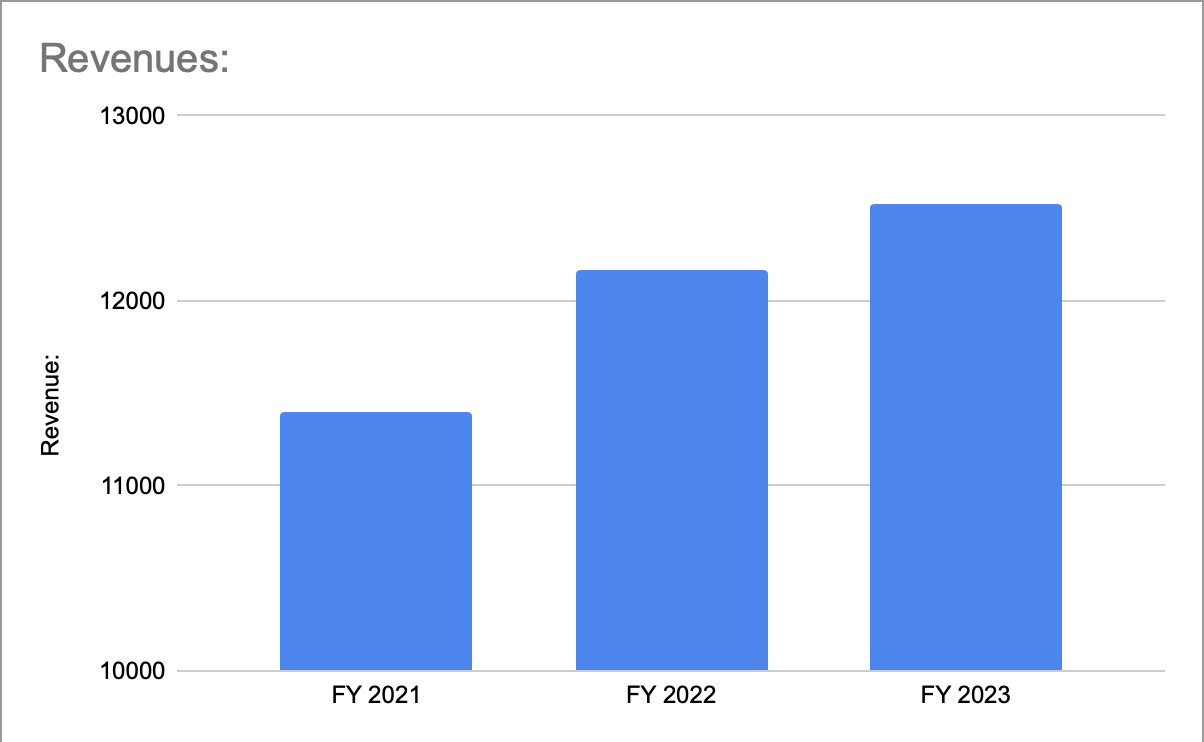

Besides the positive profitability demonstrated over the years, we can also observe a steady growth in the company's revenues over the past three years.

Revenues ( Author's calculation)

In 2021, the company generated revenues of 11.4 billion while in 2022 the revenues amounted to 12.164 billion and finally last year the revenues were at 12.525 billion. Over this period, the company achieved a Compound Annual Growth Rate (CAGR) of 3.18%.

This is a good trend, given the challenges of maintaining consistent results in the communication and media sector. When we compare this with competitors, we often see a pattern of good growth years followed by years of negative results. What sets Liberty Media apart is the consistency of its results over the years. This consistency suggests that the management has a firm grasp on its business model and that capable of executing its strategy for 2024.

Now, I want to focus on the details of the strategy that the company wants to pursue in 2024 and why I think this could be a good opportunity for growth. Firstly, the most intriguing event that the company owns is the F1 race, which has seen an increase in revenues, rising from 754 million to 1.2 billion (quarterly). The company has announced that it wants to increase the number of sprint races to be broadcasted in the coming year. I believe this will increase the number of views from F1 fans, so I'm expecting that in 2024, the F1 group will register further growth in revenues.

Another aspect that I want to analyze is the acquisition of Quint and why I believe this can be a clever strategic move. Quint is a company that operates in the sports events sector as a ticket provider and offers hospitality at some of the most famous sports events. Therefore, it's a company that operates globally across various sports events like the NBA, MotoGP, and many more. The acquisition of Quint will certainly increase diversification, not only from the perspective of the events but also from the business model standpoint. In fact, Quint is not a broadcasting company and this in my opinion is very important as it allows Liberty Media to diversify its business beyond the traditional broadcasting. By acquiring Quint, Liberty Media is expanding into the live event sector, which could provide a different revenue stream that can increase the stability of its income.

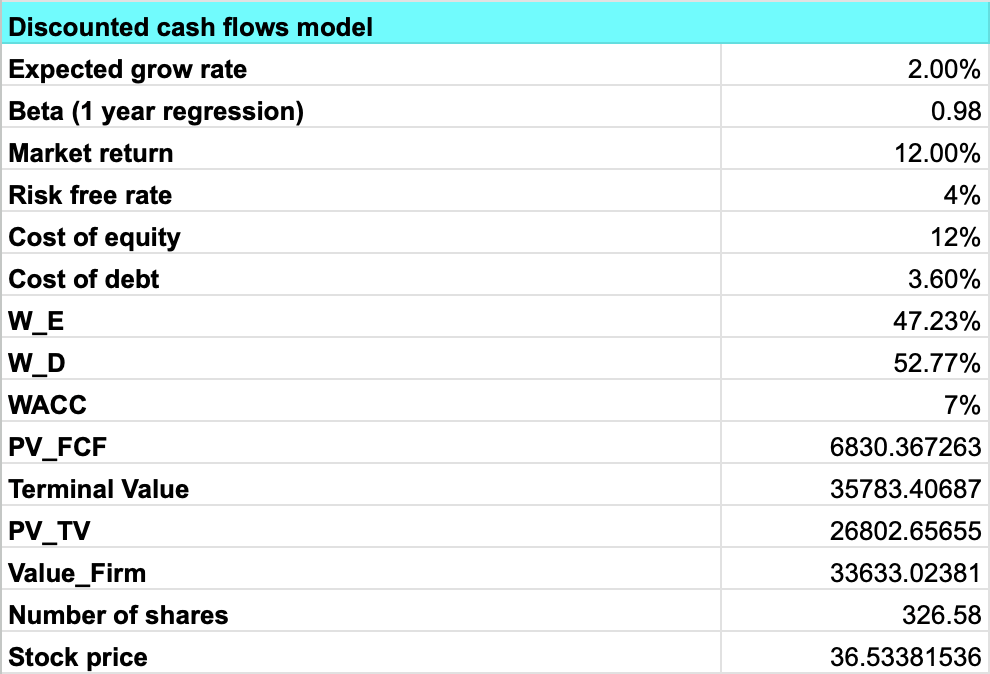

Since the company does not pay any dividends, I'll use the discounted cash flows model. The most difficult part is to estimate the future cash flows of the company. We then use the WACC (Weighted Average Cost of Capital) to discount them to find the Total Firm Value and dividing this by the number of shares should lead to the fair stock price. In the case of Liberty Media, it's tricky to make a projection of the future cash flows because the variance in past data is high. So, what I've decided to do here is to use the average of the cash flows from the last three years and apply a growth rate of 2% per year, which seems realistic to me considering that the forecasted CAGR of the communication and media services is estimated at 1.43%.

Projection cash flows ( Author's calculation)

In order to make the model work, we need some inputs, in this case the most crucial ones other than the projected cash flows are the cost of equity and the cost of debt of the company. In the case of the cost of the debt is easy to quantify it because we need just to divide the interest expenses by the total debt of the company, while in the estimation of the cost of equity is a more difficult and to do so I have used the well-known formula derived from the capital asset pricing model.

For Liberty Media, the cost of debt is approximately 3.6%, which isn't particularly high. Conversely, the cost of equity is 12%, which is considerably high. In my view, this validates my previous assertion that the company operates in a sector where revenue streams are unpredictable. Therefore, stakeholders demand a premium for this risk, which explains the high cost of equity.

After determining the cost of debt and the cost of equity, I used them to compute the WACC. Then, I used the WACC as a discount factor to calculate the present value (PV) of the Free Cash Flow (FCF). In addition to that, I estimated the terminal value of the firm and finally I summed them to get the total value of the company.

Discounted cash flows model ( Author's calculation)

Using this value for the cashflows, a grow rate of 2% and the other inputs we get a share price of $36 that is more than the actual observed price in the market ($29).

So, based on the model's result, the stock appears to be slightly underpriced. However, we need to remember that in this case, the cash flow projections are a result of my assumptions and beliefs, and changing them will lead to a different price. All things considered, the fact that the model shows that the company is underpriced seems compelling to me. If the company can effectively implement its strategy, it might be possible to see the price reach $40, especially considering that in mid-2022, the price was around $45.

To conclude, I would say that this stock represents a good investment opportunity for the mid-to-long term. I also think that this kind of business could lead to high variance in results, which can increase the risk of the investment. We also have to consider that, as I have shown before, the company's businesses are diversified, but in my opinion the F1 group is the segment that has the potential for rapid growth. This is because the F1 division is relatively new and has not yet fully realized its potential. In contrast, the SiriusXM division, which is older, has shown some stagnation in recent years. Even if the company has planned to increase the streams of sprint races, this will not automatically translate into a larger audience. So, if in the current year the F1 group is not able to generate enough revenues, this will have a significant effect on the group's overall results. This is why I think it's so important for the company to successfully develop the investment in Quint, but it's possible that this will require more than one year.

Therefore, I would consider allocating a small fraction of the portfolio to this stock. Based on recent stock prices, it seems that the stock is experiencing a slightly negative trend in recent days and it might be wise to wait a bit longer and try to secure a more favorable price, like $25 or less.