davit85

davit85

Lightspeed Commerce Inc. (NYSE:LSPD) went public in the U.S. in 2020, selling its subordinate voting shares for $30.50.

I previously wrote about Lightspeed in August 2023 with a Neutral Hold outlook on continued high operating losses amid growing revenue.

My outlook is Bearish [Sell] due to a poor international macroeconomic environment, continued high operating losses, and free cash burn.

Lightspeed operates in the point-of-sale hardware and software market in North America and Europe, selling a variety of software functionalities and transaction processing for businesses in the retail, restaurant, golf and ecommerce industries.

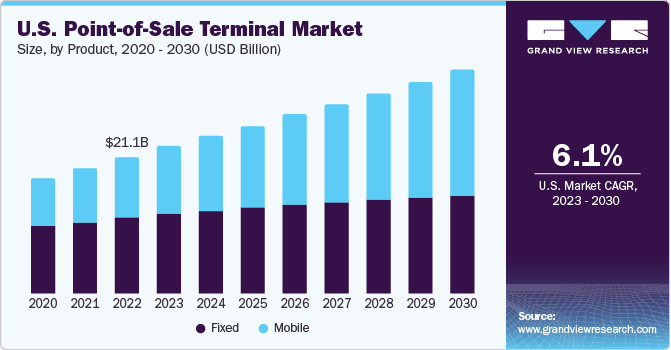

According to a market research report by Grand View Research, the global POS terminal market was an estimated $104 billion in 2023 and is expected to reach $181 billion by 2030.

If achieved, this would represent a CAGR (Compound Annual Growth Rate) of 8.3% from 2023 to 2030, a reasonably strong growth rate.

The chart below shows the U.S. POS terminal market’s historical and projected future growth trajectory through 2030, by product type:

Grand View Research

The global POS software market was an estimated $21.1 billion in 2023 and is expected to grow to $74.7 billion by 2032, representing a much higher forecasted growth rate of 15.1% from 2024 to 2032. (Source: Market.us research report.)

The software POS market is producing higher growth due to demand for cloud-based systems, integrated transaction processing and a trend toward digitalizations across numerous industry sectors.

Significant traditional vendors include:

NCR

Oracle (Micros)

Verifone

Ingenico.

Newer cloud-based entrants:

Shopify

Block

Toast

Clover

Lightspeed.

Newer aspects for these system providers include providing mobile capabilities, omnichannel integration, self-service functions including kiosks and AI-enabled activity such as recommendations, inventory management and predictive analytics.

Lightspeed’s customers value its omnichannel features, customer engagement, ease of use and scalability and its specialized capabilities for retail and restaurant use cases.

The company also has an extensive partner integration network that adds value to special requirements depending on the customer.

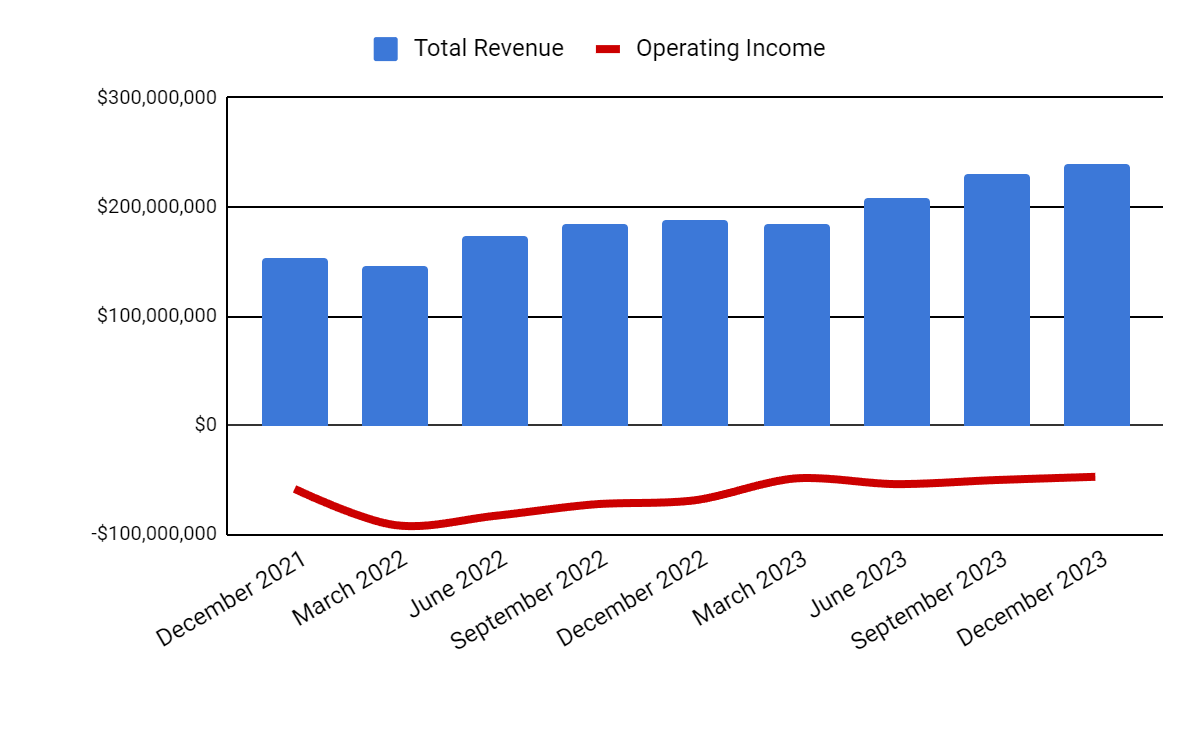

Total revenue by quarter (columns) has resumed growth after a flatter period during late 2022 and early 2023; Operating income by quarter (line) has remained heavily negative, with no progress toward breakeven in recent quarters.

Seeking Alpha

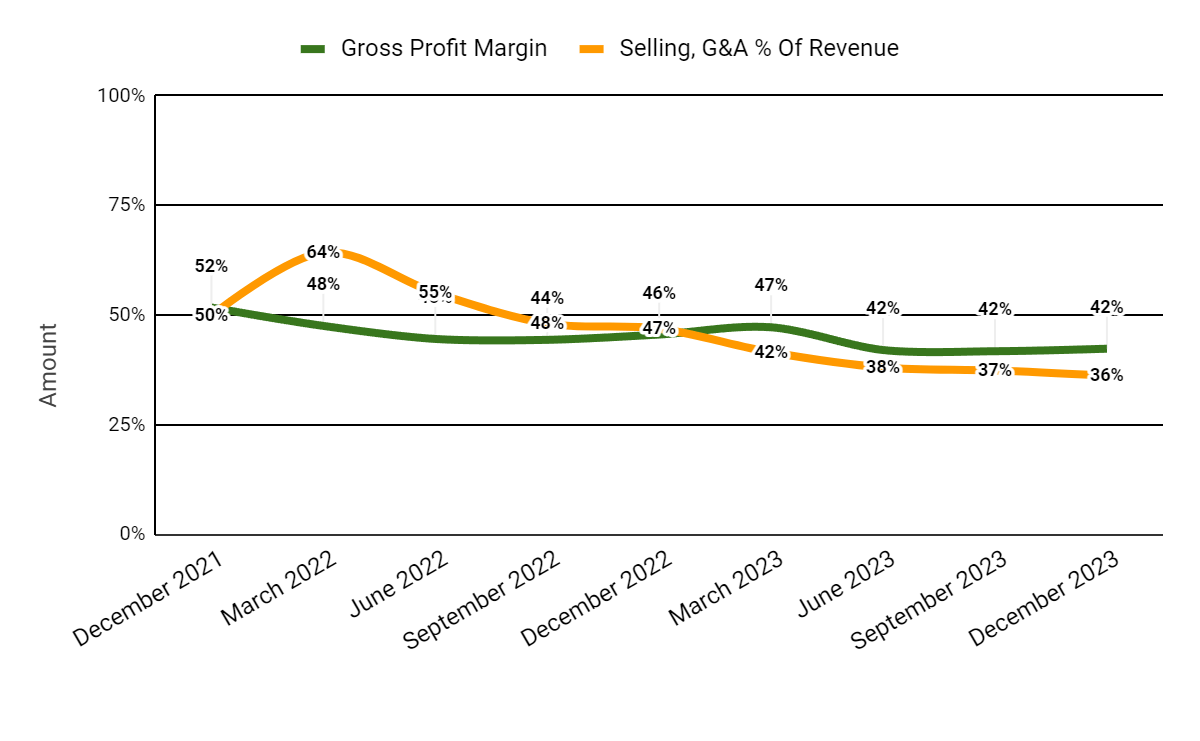

Gross profit margin by quarter (green line) has stabilized as a result of declining referral fees for transaction revenue; Selling and G&A expenses as a percentage of total revenue by quarter (orange line) have dropped due to reduced share-based compensation and reassignment toward selling its unified payments solutions.

Seeking Alpha

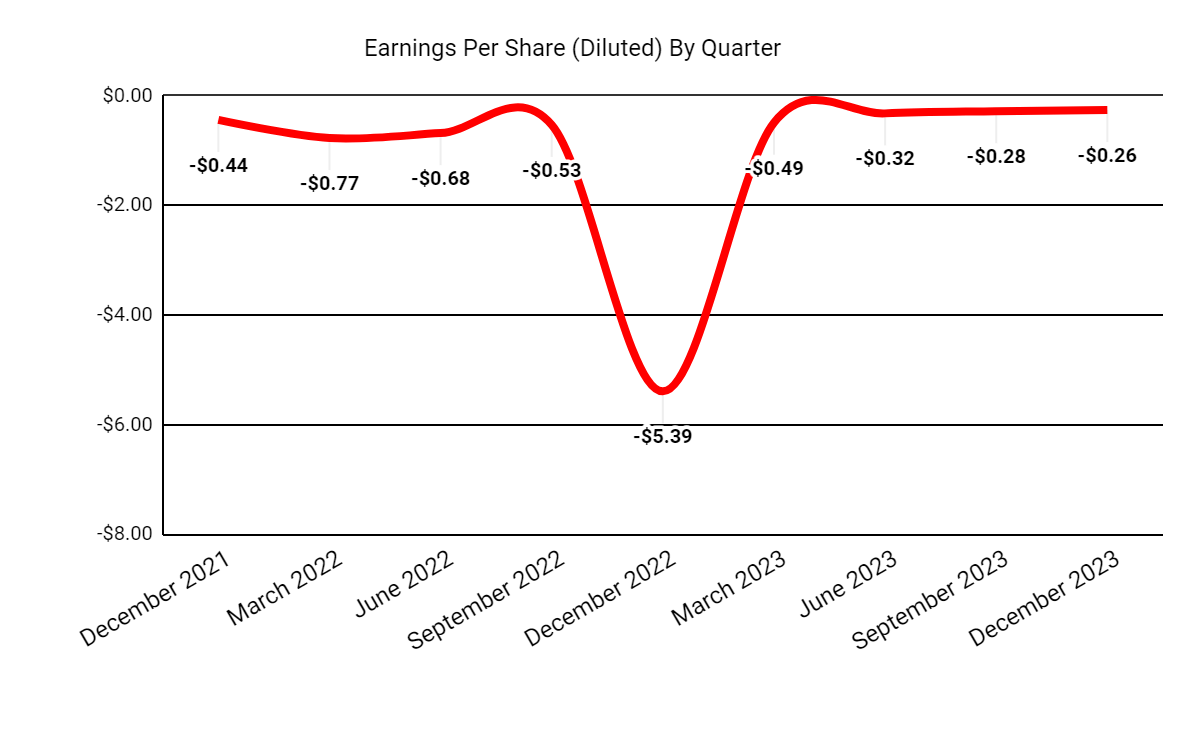

Earnings per share (Diluted) have remained heavily negative, with slowing progress toward breakeven.

Seeking Alpha

(All data in the above charts is GAAP.)

Compared to competitor Block (SQ), the market is valuing LSPD at a lower EV/Sales multiple despite growing faster but producing far higher net losses and using significant operating cash, per the table shown here:

Metric | Block | Lightspeed Commerce | Variance |

EV/Sales ("FWD") | 1.8 | 1.5 | -16.2% |

EV/EBITDA ("FWD") | 23.4 | 1,550.7 | 6524.1% |

Rev. Growth Estimate ("FWD") | 12.0% | 27.1% | 125.7% |

Net Income Margin | -1.4% | -23.9% | 1653.7% |

Operating Cash Flow | $944,250,000 | -$110,720,000 | --% |

(Source: Seeking Alpha Data.)

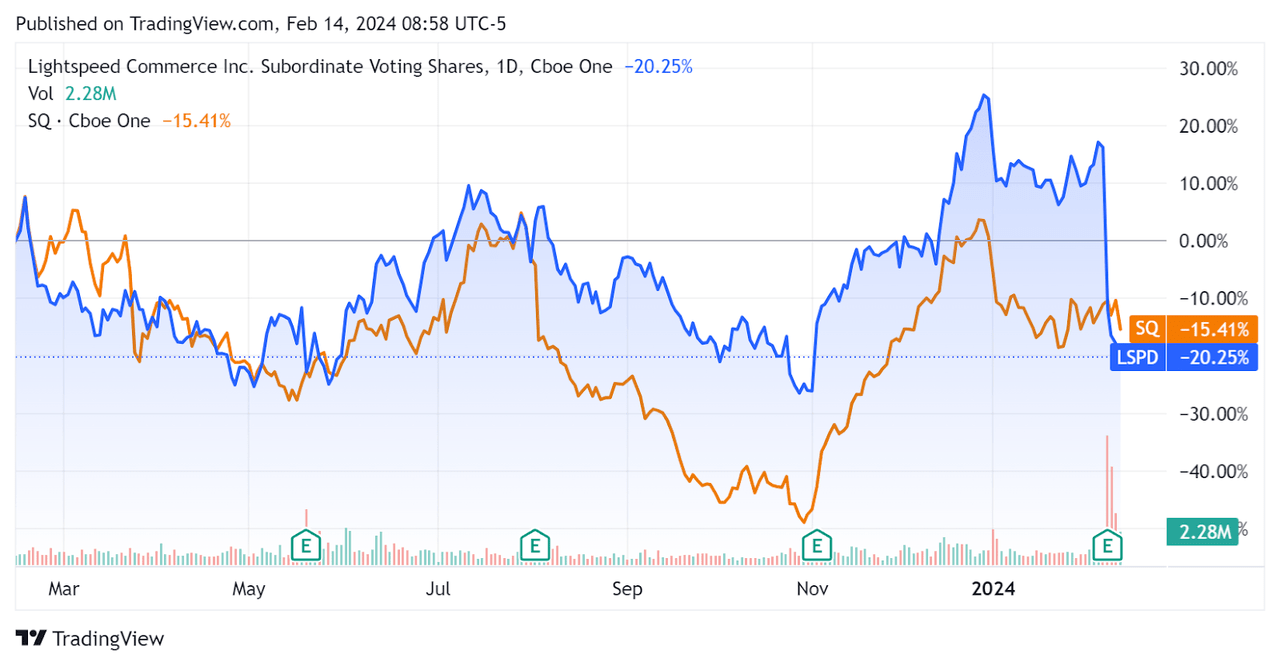

Also, the stocks of the two companies have largely tracked each other over the past year, although LSPD’s recent drop after a soft outlook has pushed its 12-month return to below that of Block’s, as the chart shows below:

Seeking Alpha

The company's major metrics are shown in the table below:

Metric | Amount |

EV/Sales ("FWD") | 1.5 |

EV/EBITDA ("FWD") | 1550.7 |

Price/Sales ("TTM") | 2.4 |

Revenue Growth ("YoY") | 24.6% |

Net Income Margin | -23.9% |

EBITDA Margin | -16.2% |

Market Capitalization | $2,060,000,000 |

Enterprise Value | $1,350,000,000 |

Operating Cash Flow | -$110,720,000 |

Earnings Per Share (Fully Diluted) | -$1.35 |

FY 2024 FWD EPS Estimate | $0.16 |

Rev. Growth Estimate ("FWD") | 27.1% |

Free Cash Flow/Share ("TTM") | -$0.82 |

Seeking Alpha Quant Score | Hold - 3.21 |

(Source: Seeking Alpha Data.)

The firm’s Rule of 40 performance has improved only marginally over FQ1 2024’s results, as the table shows here:

Rule of 40 Performance (Unadjusted) | FQ1 2024 | FQ3 2024 |

Revenue Growth % | 26.3% | 24.6% |

Operating Margin | -23.6% | -19.7% |

Total | 2.7% | 4.9% |

(Source: Seeking Alpha Data.)

Lightspeed recently sold off after comments from management about a challenging adoption cycle for its bundled software and unified payments system in Europe.

The firm is seeking to grow its payments gross transaction value [GTV] and the number of locations with high GTV metrics.

It appears the European operation is experiencing slower-than-expected growth as it needs to educate the market on the benefits of its system, which can take a while.

As a result, founder and Executive Chairman Dax Dasilva has replaced CEO Chauvet, effective immediately.

This appears to be an emergency move designed to reinvigorate the company's growth efforts internationally.

The problem for LSPD is that macro conditions are worsening. The UK has just entered recession, Germany is well into recession, and France will be lucky to grow at 0.1% after recession quarters earlier in 2023.

Europe is once again the "sick man" economically, likely dragging down LSPD’s ambitions for growth there, customer education requirements aside.

The company's only hope is a strong-than-expected growth trajectory in the U.S. & Canada to make up for a sagging international picture.

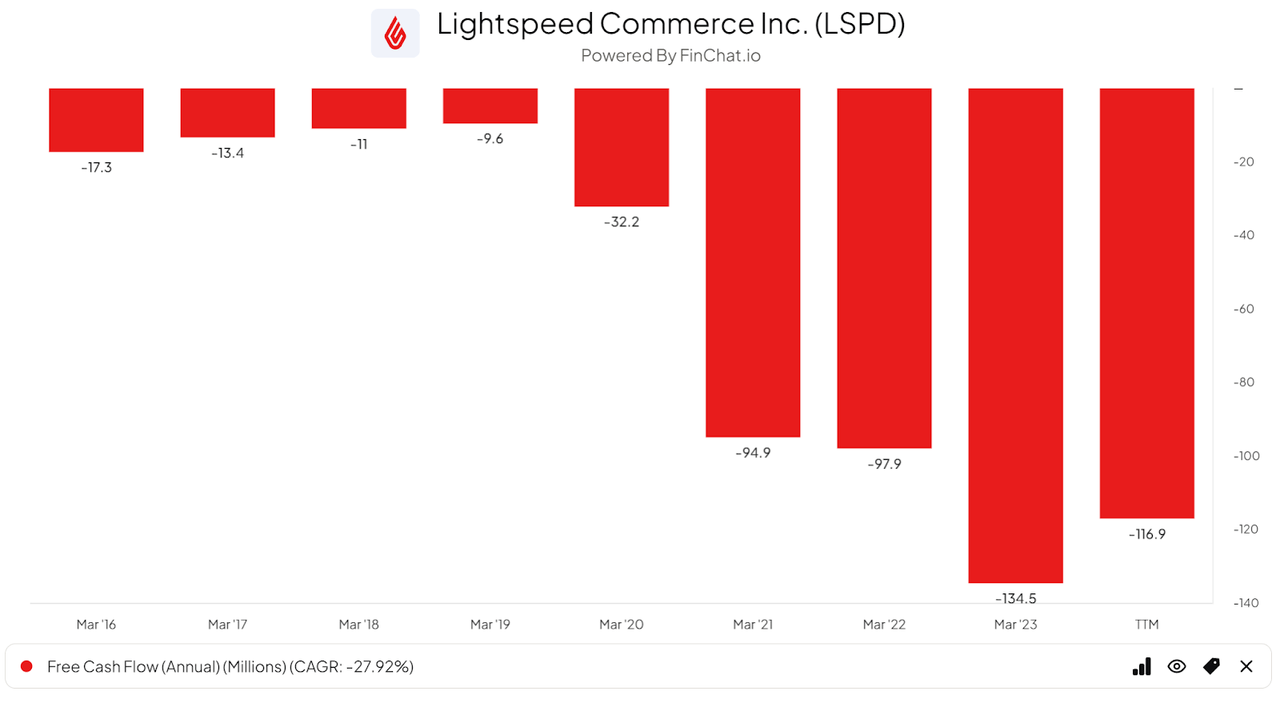

But LSPD continues to use free cash to buy revenue growth, as the chart shows here:

FinChat.io

Add to that continued high operating losses and intense competition from other industry upstarts and legacy players and the stock may be damaged goods for some time ahead.

With challenged growth prospects, high free cash burn and a dour international macroeconomic environment, my outlook on Lightspeed Commerce Inc. is to put money elsewhere.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.